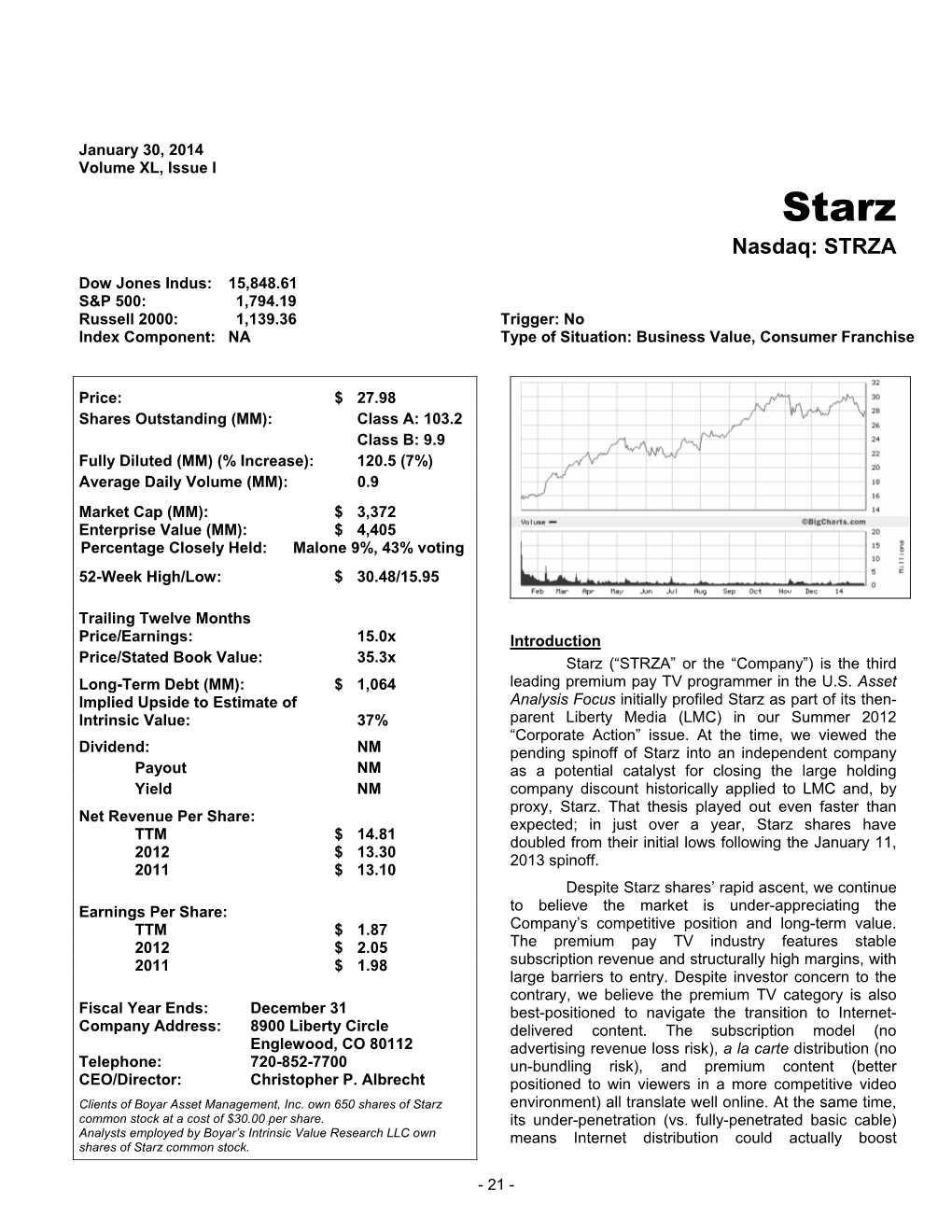

Starz Nasdaq: STRZA

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pr-Dvd-Holdings-As-Of-September-18

CALL # LOCATION TITLE AUTHOR BINGE BOX COMEDIES prmnd Comedies binge box (includes Airplane! --Ferris Bueller's Day Off --The First Wives Club --Happy Gilmore)[videorecording] / Princeton Public Library. BINGE BOX CONCERTS AND MUSICIANSprmnd Concerts and musicians binge box (Includes Brad Paisley: Life Amplified Live Tour, Live from WV --Close to You: Remembering the Carpenters --John Sebastian Presents Folk Rewind: My Music --Roy Orbison and Friends: Black and White Night)[videorecording] / Princeton Public Library. BINGE BOX MUSICALS prmnd Musicals binge box (includes Mamma Mia! --Moulin Rouge --Rodgers and Hammerstein's Cinderella [DVD] --West Side Story) [videorecording] / Princeton Public Library. BINGE BOX ROMANTIC COMEDIESprmnd Romantic comedies binge box (includes Hitch --P.S. I Love You --The Wedding Date --While You Were Sleeping)[videorecording] / Princeton Public Library. DVD 001.942 ALI DISC 1-3 prmdv Aliens, abductions & extraordinary sightings [videorecording]. DVD 001.942 BES prmdv Best of ancient aliens [videorecording] / A&E Television Networks History executive producer, Kevin Burns. DVD 004.09 CRE prmdv The creation of the computer [videorecording] / executive producer, Bob Jaffe written and produced by Donald Sellers created by Bruce Nash History channel executive producers, Charlie Maday, Gerald W. Abrams Jaffe Productions Hearst Entertainment Television in association with the History Channel. DVD 133.3 UNE DISC 1-2 prmdv The unexplained [videorecording] / produced by Towers Productions, Inc. for A&E Network executive producer, Michael Cascio. DVD 158.2 WEL prmdv We'll meet again [videorecording] / producers, Simon Harries [and three others] director, Ashok Prasad [and five others]. DVD 158.2 WEL prmdv We'll meet again. Season 2 [videorecording] / director, Luc Tremoulet producer, Page Shepherd. -

Document View

Document View http://proquest.umi.com.ezproxy1.lib.asu.edu/pqdweb?index=5... Databases selected: Los Angeles Times Television; TELEVISION; Dane Cook, pain-free comedian; Ever wonder what would happen if comedy lost its angst? Just take a look at its new smiley face.; [HOME EDITION] Paul Brownfield. Los Angeles Times. Los Angeles, Calif.: Sep 3, 2006. pg. E.1 Abstract (Summary) "Tourgasm" was a conspicuously slight and infomercial-like ad to boost [Cook]'s rabid popularity among college-age fans; the rest was filler, Cook and his three comedian underlings in various states of homoerotic, roughhousing repose. It seemed more than a little symbolic, in fact, that Cook was blowing up last year while Mitch Hedberg, a comedian whose following mirrored Cook's (Internet fan base, transcendent rock-star aura), died of a drug overdose in a New Jersey motel. Onstage, Hedberg cut an odd Kurt Cobain-like figure -- tall, skinny, beatnik clothes, hair over his eyes. He talked in idiosyncratic, absurdist mumbles ("I tried to walk into a Target, but I missed"; "I don't own a microwave, but I do have a clock that occasionally cooks [things]") and was afraid to lock eyes with the audience. He feared the very thing at which Cook excels -- tearing down the wall between the audience and himselfbut he loved that which Cook doesn't: the economy, the importance, of words. MULTIMEDIA SPLASH: On the comedian's slate is a film costarring pop star [Jessica Simpson]. Above, the pair at the MTV Movie Awards in June.; PHOTOGRAPHER: Chris Carlson Associated Press; ON THE UP AND UP: Cook avoids the dark side, he says, to put "a more positive, productive take on what a comic is."; PHOTOGRAPHER: Damian Dovarganes Associated Press; ASCENDING: On the heels of Cook's tourbased reality show comes an HBO special.; PHOTOGRAPHER: John P. -

Glenn-Garland-Editor-Credits.Pdf

GLENN GARLAND, ACE Editor Television PROJECT DIRECTOR STUDIO / PRODUCTION CO. WELCOME TO THE BLUMHOUSE: BLACK BOX Emmanuel Osei-Kuffour Amazon / Blumhouse Productions EP: Jay Ellis, Jason Blum, Aaron Bergman PARADISE CITY*** (series) Ash Avildsen Sumerian Films EP: Lorenzo Antonucci PREACHER (season 3) Various AMC / Sony Pictures Television EP: Sam Catlin, Seth Rogen, Evan Goldberg ALTERED CARBON** (series) Various Netflix / Skydance EP: Laeta Kalogridis, James Middleton, Steve Blackman STAN AGAINST EVIL (series) Various IFC / Radical Media EP: Dana Gould, Frank Scherma, Tom Lassally BANSHEE (series) Ole Christian Madsen HBO / Cinemax Magnus Martens EP: Alan Ball THE VAMPIRE DIARIES (series) Various CW / Warner Bros. Television EP: Julie Plec, Kevin Williamson Feature Films PROJECT DIRECTOR STUDIO / PRODUCTION CO. BROKE Carlyle Eubank Wild West Entertainment Prod: Wyatt Russell, Alex Hertzberg, Peter Billingsley THE TURNING Floria Sigismondi Amblin Partners 3 FROM HELL Rob Zombie Lionsgate FAMILY Laura Steinel Sony Pictures / Annapurna Pictures Official Selection: SXSW Film Festival Prod: Kit Giordano, Sue Naegle, Jeremy Garelick SILENCIO Lorena Villarreal 5100 Films / Prod: Beau Genot 31 Rob Zombie Lionsgate / Saban Films Official Selection: Sundance Film Festival Prod: Mike Elliot, Andy Gould THE QUIET ONES John Pogue Lionsgate / Exclusive Media LORDS OF SALEM Rob Zombie Blumhouse / Anchor Bay Entertainment LOVE & HONOR Danny Mooney IFC Films / Red 56 HALLOWEEN 2 Rob Zombie Dimension Films BUNRAKU* Guy Moshe Snoot Entertainment Official -

Cinedigm Corp. (Exact Name of Registrant As Specified in Its Charter) ______

Dear Stockholders, Cinedigm put together a remarkable series of accomplishments over the last fiscal year, completing the Company’s business transformation by solidifying our unique position as a key player in the explosively growing OTT/streaming business. Here’s what we accomplished this year: First, we developed several new streaming channels including Comedy Dynamics and The Bob Ross Channel to build our portfolio to 16 premium streaming channels either launched or under contract to launch. We will soon be at 20 channels and plan to get to 30 in the next 18 months. This gives Cinedigm a large, meaningful and growing channel share on the program guide for every key streaming platform and device. Most of these new channels will be set up in a similar fashion to our recent Bob Ross, All 3 Media,, Team Whistle and LiveXLive channel deals, where we partnered with established branded entertainment companies that bring huge amounts of content to the table and then we operate and launch with our major distribution partners like Roku, Amazon, Tubi, and Samsung. We have a robust deal pipeline of these potential premium new partners and channels now because we have clearly established Cinedigm as the “go to” independent streaming company that can employ our state-of-the-art proprietary Matchpoint technology, an enormous streaming distribution platform and device reach, and a huge digital content library to help launch streaming channels across the entire OTT ecosystem. We can do all that quickly, cost effectively and with almost ubiquitous distribution potential on every device and platform. The quality of the business partners reflected in our new channel deals clearly demonstrates that the entertainment industry understands the advantages of doing business with Cinedigm in the exploding streaming space. -

Portsmouth, NH October 14.15.16.17 2010 the Tenth Annual

The Tenth Annual Portsmouth, NH October 14.15.16.17 2010 nhfilmfestival.com october 14.15.16.17 2010 1 We have everything. That’s what makes us Rule. We love gear. Film or video, production or post. We get to play with all the latest technology and figure how to best put it to work for our incredibly creative customers. We sell, rent, install, integrate and architect all kinds of equipment and solutions. And guess what? We get to do it every day. Sweet! www.rule.com | 1.800.rule.com 2 The Tenth Annual Portsmouth, NH October 14.15.16.17 2010 WELCOME TO the 2010 neW hamPshiRe film FESTIVAL! You can call it our 10th anniversary or you can call it our 10th Jodi Foster. Our roster of anticipated short films, which include birthday; either way, a great celebration is in order! It is an Academy Award nominees and a new narrative film by James exceptional year for the New Hampshire Film Festival and we Franco, is also making waves. are proud and excited to have y ou here with us! To mark the festival’s special occasion, you may notice our Beginning with the festival’s strong and heartfelt kickoff during highlight on comedy, both on screen, live on stage, and through the week of September 11, 2001, we have been delighted and entertaining panel discussions. We are certain you’ll also take honored to present a full decade of film appreciation to New note of our new preferred restaurant program, emphasizing Hampshire and to the world. -

Accepted Manuscript Version

Research Archive Citation for published version: Kim Akass, and Janet McCabe, ‘HBO and the Aristocracy of Contemporary TV Culture: affiliations and legitimatising television culture, post-2007’, Mise au Point, Vol. 10, 2018. DOI: Link to published article in journal's website Document Version: This is the Accepted Manuscript version. The version in the University of Hertfordshire Research Archive may differ from the final published version. Copyright and Reuse: This manuscript version is made available under the terms of the Creative Commons Attribution-NonCommercial- NoDerivatives License CC BY NC-ND 4.0 ( http://creativecommons.org/licenses/by-nc-nd/4.0/ ), which permits non-commercial re-use, distribution, and reproduction in any medium, provided the original work is properly cited, and is not altered, transformed, or built upon in any way. Enquiries If you believe this document infringes copyright, please contact Research & Scholarly Communications at [email protected] 1 HBO and the Aristocracy of TV Culture : affiliations and legitimatising television culture, post-2007 Kim Akass and Janet McCabe In its institutional pledge, as Jeff Bewkes, former-CEO of HBO put it, to ‘produce bold, really distinctive television’ (quoted in LaBarre 90), the premiere US, pay- TV cable company HBO has done more than most to define what ‘original programming’ might mean and look like in the contemporary TV age of international television flow, global media trends and filiations. In this article we will explore how HBO came to legitimatise a contemporary television culture through producing distinct divisions ad infinitum, framed as being rooted outside mainstream commercial television production. In creating incessant divisions in genre, authorship and aesthetics, HBO incorporates artistic norms and principles of evaluation and puts them into circulation as a succession of oppositions— oppositions that we will explore throughout this paper. -

Concevoir Et Animer Pour L'acceptation De Robots

Concevoir et animer pour l’acceptation de robots zoomorphiques Adrien Gomez To cite this version: Adrien Gomez. Concevoir et animer pour l’acceptation de robots zoomorphiques. Art et histoire de l’art. Université Toulouse le Mirail - Toulouse II, 2018. Français. NNT : 2018TOU20048. tel- 02466318 HAL Id: tel-02466318 https://tel.archives-ouvertes.fr/tel-02466318 Submitted on 4 Feb 2020 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. Délivré par Université Toulouse – Jean Jaurès Adrien Gomez Le 30 Août 2018 Concevoir et Animer pour l’Acceptation de Robots Zoomorphiques École doctorale et discipline ou spécialité ED ALLPH@: Études audiovisuelles Unité de recherche LARA (Université Toulouse Jean Jaurès) – LIRMM (Université Montpellier) Directeur(s) de Thèse M. Gilles METHEL M. René Zapata Co-encadrant de Thèse M. Sébastien Druon Jury Chu-Yin Chen, Professeure, université Paris 8 Sylvie Lelandais, Professeure, Université Evry-Val d’Essonnes Gilles Methel, Professeur, Université Toulouse2-Jean Jaurès René Zapata, Professeur, LIRMM Montpellier Sébastien -

DANIEL CLANCY Production Designer Danielbclancydesign.Com

DANIEL CLANCY Production Designer danielbclancydesign.com PROJECTS Partial List DIRECTORS STUDIOS/PRODUCERS 61ST STREET Various Directors BBC / AMC Limited Series Steph Accetta, Jeff Freilich Peter Moffat ORDINARY JOE Adam Davidson 20TH CENTURY FOX TV / NBC Pilot Jason Roberts, Craig Hill NEXT Glenn Ficarra 20TH CENTURY FOX TV Pilot & Season 1 John Requa Sean Williamson PROVEN INNOCENT Various Directors 20TH CENTURY FOX TV Season 1 Jane Bartelme, Craig Hill AN ACCEPTABLE LOSS Joe Chappelle CORRADO MOONCOIN Feature Film PRODUCTIONS Colleen Griffen CONTROVERSY John Requa 20TH CENTURY FOX TV Pilot Glenn Ficarra Jane Bartelme, Charlie Gogolak CHICAGO JUSTICE Various Directors DICK WOLF Season 1 UNIVERSAL TELEVISION Carla Corwin Michael Chernuchin AMERICAN PASTORAL Ewan McGregor LAKESHORE ENTERTAINMENT Feature Film Andre Lamal, Zane Weiner I AM WRATH Chuck Russell PATRIOT FILMS Feature Film Rich Cowan THE HOLLARS John Krasinski SYCAMORE PICTURES Feature Film Allyson Seeger FATHERS AND DAUGHTERS Gabriele Muccino VOLTAGE PICTURES Feature Film RIchard Middleton DOUBT Thomas Schamme SONY PICTURES TELEVISION Pilot ABC Gerrit van der Meer THE MOB DOCTOR Various Directors FOX TELEVISION Season 1 Iain Paterson PROMISED LAND Gus Van Sant FOCUS FEATURES Feature Film Ron Schmidt BOSS Gus Van Sant LIONSGATE / STARZ Pilot & Season 1 Farhad Safinia SO UNDERCOVER Thomas Vaughan EXCLUSIVE MEDIA Feature Film Steven Pearl, Alan Loeb THE DILEMMA Ron Howard IMAGINE Feature Film UNIVERSAL PICTURES Todd Hallowell, Brian Grazer NOTHING LIKE THE HOLIDAYS Alfredo DeVilla OVERTURE FILMS Feature Film Bob Teitel Mr. Clancy is local in Chicago. INNOVATIVE-PRODUCTION.COM | 310.656.5151 . -

Unmasking the Devil: Comfort and Closure in Horror Film Special Features

Unmasking the Devil: Comfort and Closure in Horror Film Special Features ZACHARY SHELDON While a viewer or critic may choose to concentrate solely on a film’s narrative as representative of what a film says, some scholars note that the inclusion of the supplementary features that often accompany the home release of a film destabilize conceptions of the text of a film through introducing new information and elements that can impact a film’s reception and interpretation (Owczarski). Though some special features act as mere advertising for a film’s ancillary products or for other film’s or merchandise, most of these supplements provide at least some form of behind-the-scenes look into the production of the film. Craig Hight recognizes the prominent “Making of Documentary” (MOD) subgenre of special feature as being especially poised to “serve as a site for explorations of the full diversity of institutional, social, aesthetic, political, and economic factors that shape the development of cinema as a medium and an art form” (6). Additionally, special features provide the average viewer access to the magic of cinema and the Hollywood elite. The gossip or anecdotes shared in interviews and documentaries in special features provide viewers with an “insider identity,” that seemingly involves them in their favorite films beyond the level of mere spectator (Klinger 68). This phenomenon is particularly interesting in relation to horror films, the success of which is often predicated on a sense of mystery or the unknown pervading the narrative so as to draw out visceral affective responses from the audience. The notion of the special feature, which unpacks and reveals the inner workings of the film set and even the film’s plot, seems contradictory to the enjoyment of what the horror film sets out to do. -

Activision Publishing Announces 10 Minute Solution, an Upcoming Video Game for Wii™ Based on Anchor Bay Entertainment's Hit Fitness Dvds

Activision Publishing Announces 10 Minute Solution, An Upcoming Video Game For Wii™ Based On Anchor Bay Entertainment's Hit Fitness DVDs Total-Body 10-Minute Workouts for a Healthier, Fitter You! MINNEAPOLIS, March 8, 2010 /PRNewswire via COMTEX News Network/ -- Activision Publishing, Inc. (Nasdaq: ATVI) today announced an agreement with Anchor Bay Entertainment to release 10 Minute Solution, a video game for Wii(TM) based on the popular exercise DVDs. Coming this Spring, 10 Minute Solution will bring focused exercise activities to fitness fans with busy schedules, in an affordable and fun way. "10 Minute Solution DVDs give users a unique fitness experience: customizable routines that fit into any lifestyle," said David Oxford, Activision Publishing. "We've taken this concept and combined it with the interactivity of the Wii, creating a new kind of workout that gets results." 10 Minute Solution combines the ease of the popular fitness DVDs with casual gaming fun. The game allows players to construct regimens from a wide variety of 10 minute routine blocks, organized into three main categories: cardio boxing, mixed games and aerobics. 10 Minute Solution is designed to captivate fitness enthusiasts and gamers alike with intense routines that play as a game, unlike other fitness games that simply have the player following a trainer on screen. The game is enhanced when played with the Wii Balance Board(TM), but still offers a fantastic workout without it. "Our legions of 10 Minute Solution DVD users will tell you these simple 10 minute exercises work," said Julie Cartwright, SVP Marketing at Anchor Bay Entertainment. -

Signature Redacted

Perspectives on Film Distribution in the U.S.: Present and Future By Loubna Berrada Master in Management HEC Paris, 2016 SUBMITTED TO THE MIT SLOAN SCHOOL OF MANAGEMENT IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF SCIENCE IN MANAGEMENT STUDIES AT THE MASSACHUSETTS INSTITUTE OF TECHNOLOGY JUNE 2016 OFTECHNOLOGY 2016 Loubna Berrada. All rights reserved. JUN 08 201 The author hereby grants to MIT permission to reproduce and to distribute publicly paper and electronic LIBRARIES copies of this thesis document in whole or in part ARCHIVES in any medium now known or hereafter created. Signature of Author: Signature redE cted MIT Sloan School of Management May 6, 2016 Certified by: Signature redacted Juanjuan Zhang Epoch Foundation Professor of International Management Professor of Marketing MIT Sloan School of Management Thesis Supervisor Accepted by: Signature redacted Rodrigo S. Verdi Associate Professor of Accounting Program Director, M.S. in Management Studies Program MIT Sloan School of Management 2 Perspectives on Film Distribution in the U.S.: Present and Future By Loubna Berrada Submitted to MIT Sloan School of Management on May 6, 2016 in Partial fulfillment of the requirements for the Degree of Master of Science in Management Studies. Abstract I believe film has the power to transform people's lives and minds and to enlighten today's generation like any other medium. This is why I wanted to write my thesis about film distribution as it will determine the future of the industry itself. The way films are distributed, accessed and consumed will be critical in shaping our future entertainment culture and the way we approach content. -

Video Resources Feature Films Boiler Room

Video Resources Feature Films Boiler Room. New Line Cinema, 2000.A college dropout, attempting to win back his father's high standards he gets a job as a broker for a suburban investment firm, which puts him on the fast track to success, but the job might not be as legitimate as it once appeared to be. Margin Call. Before the Door Pictures, 2011. Follows the key people at an investment bank, over a 24- hour period, during the early stages of the 2008 financial crisis. The Wolf of Wall Street. Universal Pictures, 2013. Based on the true story of Jordan Belfort, from his rise to a wealthy stock-broker living the high life to his fall involving crime, corruption and the federal government. The Big Short. Paramount Pictures,2015. In 2006-7 a group of investors bet against the US mortgage market. In their research they discover how flawed and corrupt the market is. The Last Days of Lehman Brothers. British Broadcasting Corporation, 2009. After six months' turmoil in the world's financial markets, Lehman Brothers was on life support and the government was about to pull the plug. Documentaries Enron: The Smartest Guys in the Room. Jigsaw Productions, 2005. A documentary about the Enron Corporation, its faulty and corrupt business practices, and how they led to its fall. Inside Job. Sony Pictures Classics, 2010. Takes a closer look at what brought about the 2008 financial meltdown. Too Big to Fail. HBO Films, 2011. Chronicles the financial meltdown of 2008 and centers on Treasury Secretary Henry Paulson. Money for Nothing: Inside the Federal Reserve.