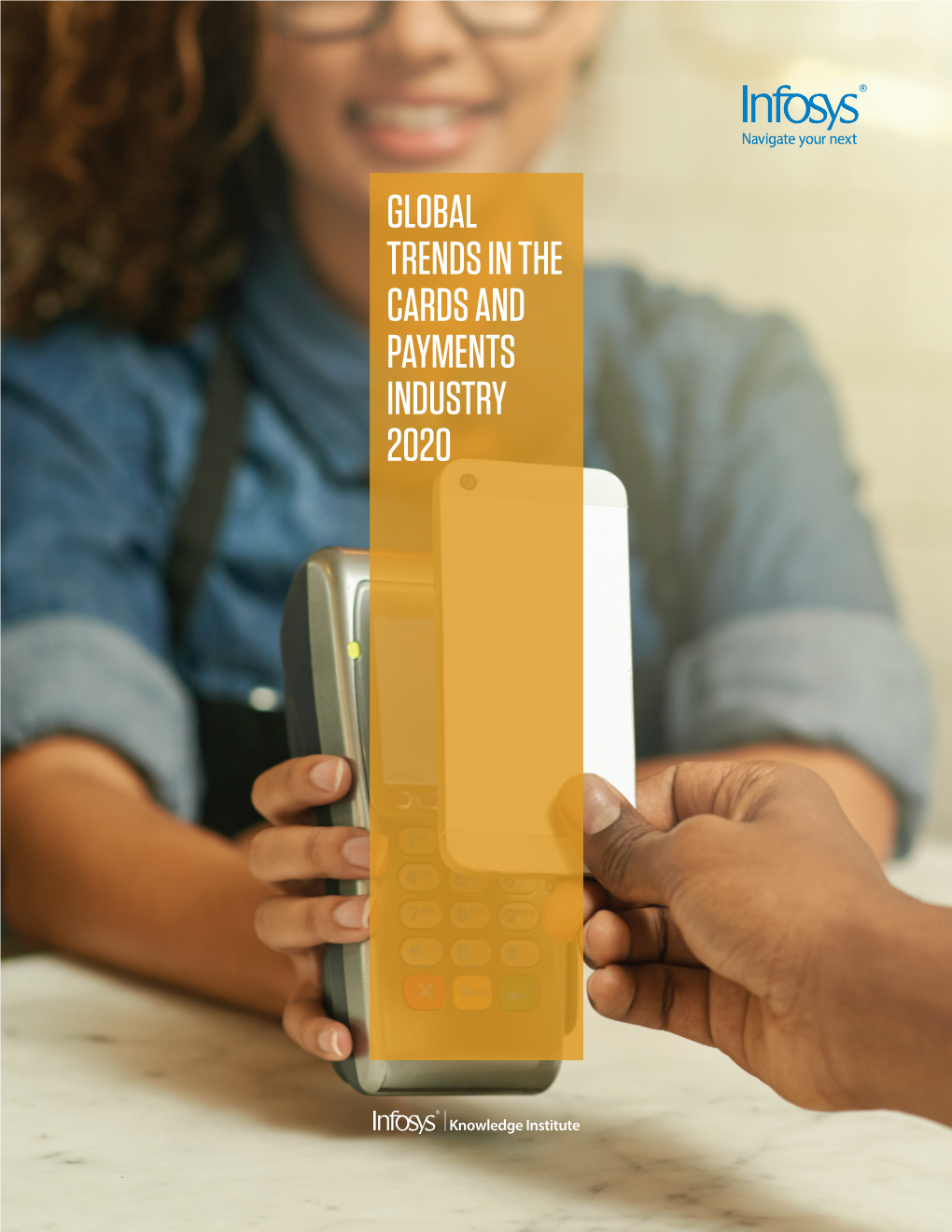

Global Trends in Cards and Payments Industry 2020 External Document © 2020 Infosys Limited Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Wolfefintechforum DAY 1 AGENDA

#WolfeFinTechForum DAY 1 AGENDA - TUESDAY, MARCH 9, 2021 Opening Remarks 7:50-8:00am ET Wolfe Research – Darrin Peller, Managing Director, Payments, Processors, and IT Services Shift4 Payments 8:00-8:35am ET Jared Isaacman - CEO Fiserv 8:40-9:15am ET Frank Bisignano – President & CEO JP Morgan Chase 9:20-9:55am ET Max Neukirchen – CEO of Merchant Services Mastercard 10:00-10:35am ET Sachin Mehra - CFO B2B Payments: Living Through an Inflection Billtrust – Mark Shifke, CFO Discover Financial Services 10:40-11:15am ET MineralTree – Chris Sands, CFO John Greene – EVP & CFO Repay Holdings Corporation – Jake Moore, EVP Corporate Development & Strategy Fidelity National Information Services 11:20-11:55am ET Gary Norcross – President & CEO Woody Woodall - CFO PayPal 12:00-12:40pm ET Dan Schulman - CEO 12:40-1:00pm ET BREAK Square 1:00-1:35pm ET Amrita Ahuja - CFO Jack Henry & Associates, Inc. 1:40-2:15pm ET David Foss – President & CEO Synchrony 2:20-2:55pm ET Brian Wenzel, Sr – EVP & CFO Paychex, Inc. 3:00-3:35pm ET Efrain Rivera – Sr. VP, CFO & Treasurer Walker & Dunlop 3:40-4:15pm ET Willy Walker - CEO Cross-Border B2B: Still So Hard to Reach 4:20-4:55pm ET Credorax - Benny Nachman, Founder & Chairman of the Board Tipalti Inc. - Sarah D. Spoja, CFO COMPANIES HOSTING 1X1s ONLY – MARCH 9 Cielo S/A - Daniel Henrique de Sousa Diniz, Head of IR Coro Global Inc - David Dorr, Co-Founder & Mark Goode, CEO Finix Payments - Emanuel Pleitez, Head of Business Development FleetCor Technologies - Jim Eglseder, SVP, IR Global Blue Far Peak Acquisition Corporation - Thomas Farley, Chairman & CEO of Far Peak Acquisition Corporation Houlihan Lokey, Inc. -

CRYPTONAIRE WEEKLY CRYPTO Investment Journal

CRYPTONAIRE WEEKLY CRYPTO investment journal CONTENTS WEEKLY CRYPTOCURRENCY MARKET ANALYSIS...............................................................................................................5 TOP 10 COINS ........................................................................................................................................................................................6 Top 10 Coins by Total Market Capitalisation ...................................................................................................................6 Top 10 Coins by Percentage Gain (Past 7 Days)...........................................................................................................6 Top 10 Coins added to Exchanges with the Highest Market Capitalisation (Past 30 Days) ..........................7 CRYPTO TRADE OPPORTUNITIES ...............................................................................................................................................9 PRESS RELEASE..................................................................................................................................................................................14 ZUMO BRINGS ITS CRYPTOCURRENCY WALLET TO THE PLATINUM CRYPTO ACADEMY..........................14 INTRODUCTION TO TICAN – MULTI-GATEWAY PAYMENT SYSTEM ......................................................................17 ADVERTISE WITH US........................................................................................................................................................................19 -

Rev. Rul. 2019-24 ISSUES (1) Does a Taxpayer Have Gross Income Under

26 CFR 1.61-1: Gross income. (Also §§ 61, 451, 1011.) Rev. Rul. 2019-24 ISSUES (1) Does a taxpayer have gross income under § 61 of the Internal Revenue Code (Code) as a result of a hard fork of a cryptocurrency the taxpayer owns if the taxpayer does not receive units of a new cryptocurrency? (2) Does a taxpayer have gross income under § 61 as a result of an airdrop of a new cryptocurrency following a hard fork if the taxpayer receives units of new cryptocurrency? BACKGROUND Virtual currency is a digital representation of value that functions as a medium of exchange, a unit of account, and a store of value other than a representation of the United States dollar or a foreign currency. Foreign currency is the coin and paper money of a country other than the United States that is designated as legal tender, circulates, and is customarily used and accepted as a medium of exchange in the country of issuance. See 31 C.F.R. § 1010.100(m). - 2 - Cryptocurrency is a type of virtual currency that utilizes cryptography to secure transactions that are digitally recorded on a distributed ledger, such as a blockchain. Units of cryptocurrency are generally referred to as coins or tokens. Distributed ledger technology uses independent digital systems to record, share, and synchronize transactions, the details of which are recorded in multiple places at the same time with no central data store or administration functionality. A hard fork is unique to distributed ledger technology and occurs when a cryptocurrency on a distributed ledger undergoes a protocol change resulting in a permanent diversion from the legacy or existing distributed ledger. -

Laser-Marked Document Showing a Colour-Shift Effect

(19) & (11) EP 2 174 797 A1 (12) EUROPEAN PATENT APPLICATION (43) Date of publication: (51) Int Cl.: 14.04.2010 Bulletin 2010/15 B42D 15/00 (2006.01) B42D 15/10 (2006.01) B41M 5/24 (2006.01) B41M 3/14 (2006.01) (21) Application number: 08017527.6 (22) Date of filing: 07.10.2008 (84) Designated Contracting States: • Klein, Sylke AT BE BG CH CY CZ DE DK EE ES FI FR GB GR 64380 Rossdorf (DE) HR HU IE IS IT LI LT LU LV MC MT NL NO PL PT • Montag, Heidemarie RO SE SI SK TR 64289 Darmstadt (DE) Designated Extension States: AL BA MK RS (74) Representative: Luderschmidt, Schüler & Partner Patentanwälte (71) Applicant: European Central Bank John-F.-Kennedy-Strasse 4 60311 Frankfurt am Main (DE) 65189 Wiesbaden (DE) (72) Inventors: • Arrieta, Antonio Jesús 60311 Frankfurt am Main (DE) (54) Laser-marked document showing a colour-shift effect (57) Document comprising a coating containing at the coated area with a pulsed laser beam at a rate of least one sort of effect pigments, wherein said document greater than 500 mm/s and a laser mark having a colour also comprises at least one laser mark having a high shift effect is obtained. contrast and a strong colour shift effect The authenticity of the document can be easily Said document is obtainable by a process, wherein, checked by visual inspection from different viewing an- a document comprising a coating containing at least one gles. sort of effectpigments which show differentcolours under different viewing angles is treated on at least a part of EP 2 174 797 A1 Printed by Jouve, 75001 PARIS (FR) EP 2 174 797 A1 Description BACKGROUND OF THE INVENTION 5 1. -

User Manual Ledger Nano S

User Manual Ledger Nano S Version control 4 Check if device is genuine 6 Buy from an official Ledger reseller 6 Check the box contents 6 Check the Recovery sheet came blank 7 Check the device is not preconfigured 8 Check authenticity with Ledger applications 9 Summary 9 Learn more 9 Initialize your device 10 Before you start 10 Start initialization 10 Choose a PIN code 10 Save your recovery phrase 11 Next steps 11 Update the Ledger Nano S firmware 12 Before you start 12 Step by step instructions 12 Restore a configuration 18 Before you start 19 Start restoration 19 Choose a PIN code 19 Enter recovery phrase 20 If your recovery phrase is not valid 20 Next steps 21 Optimize your account security 21 Secure your PIN code 21 Secure your 24-word recovery phrase 21 Learn more 22 Discover our security layers 22 Send and receive crypto assets 24 List of supported applications 26 Applications on your Nano S 26 Ledger Applications on your computer 27 Third-Party applications on your computer 27 If a transaction has two outputs 29 Receive mining proceeds 29 Receiving a large amount of small transactions is troublesome 29 In case you received a large amount of small payments 30 Prevent problems by batching small transactions 30 Set up and use Electrum 30 Set up your device with EtherDelta 34 Connect with Radar Relay 36 Check the firmware version 37 A new Ledger Nano S 37 A Ledger Nano S in use 38 Update the firmware 38 Change the PIN code 39 Hide accounts with a passphrase 40 Advanced Passphrase options 42 How to best use the passphrase feature 43 -

Bitcoin: a Seemingly Rampant Elevator, Or Is Someone Pushing Its Buttons?

Södertörn University | Institution for Social Sciences Bachelor Thesis (15 hp) | Business Studies - Finance | Spring Semester 2014 Bitcoin: A Seemingly Rampant Elevator, or is Someone Pushing its Buttons? - A Case Study on Bitcoin’s Fluctuations in Price and Concept. Author: Oscar Wandery Supervisor: Maria Smolander Stockholm Södertörn University Business Studies Abstract This study looks at the price mechanism of the digital quasi-currency bitcoin. Through statistical analysis of secondary data a probable significant results regarding correlation and regression between price and different independent variables have been established. The final analysis is pointing towards network effects being a part of the determinants for the crypto-currency’s price. Complimentary to the quantitative study explained above, an implementation of hermeneutic analysis based on secondary theoretical sources, journalistic opinion and a professional qualified judgment has aided the author and study in conceptual understanding. This interpretation has semantic character, and takes a Socratic kickoff regarding the nature of bitcoin as a financial instrument. The analysis runs back and forth throughout the course of the study and finally intertwines with qualitative results in the discussion. It is the author’s impression that a significant dimorphism surrounds bitcoin, calling for a conceptual differentiation leading to practical rethinking. The study takes the shape of a case-study conducted over four months. The author’s location during the process of writing was Stockholm Sweden, but the gathered data is of transnational character. Keywords: Bitcoin, crypto-currency, money, digital money, price fluctuations, financial instruments, financial systems. 2 Stockholm Södertörn University Business Studies Sammanfattning Den här studien tittar på prismekanismen hos den digitala kvasi-valören bitcoin. -

VISA Europe AIS Certified Service Providers

Visa Europe Account Information Security (AIS) List of PCI DSS validated service providers Effective 08 September 2010 __________________________________________________ The companies listed below successfully completed an assessment based on the Payment Card Industry Data Security Standard (PCI DSS). 1 The validation date is when the service provider was last validated. PCI DSS assessments are valid for one year, with the next annual report due one year from the validation date. Reports that are 1 to 60 days late are noted in orange, and reports that are 61 to 90 days late are noted in red. Entities with reports over 90 days past due are removed from the list. It is the member’s responsibility to use compliant service providers and to follow up with service providers if there are any questions about their validation status. 2 Service provider Services covered by Validation date Assessor Website review 1&1 Internet AG Internet payment 31 May 2010 SRC Security www.ipayment.de processing Research & Consulting Payment gateway GmbH Payment processing a1m GmbH Payment gateway 31 October 2009 USD.de AG www.a1m.biz Internet payment processing Payment processing A6IT Limited Payment gateway 30 April 2010 Kyte Consultants Ltd www.A6IT.com Abtran Payment processing 31 July 2010 Rits Information www.abtran.com Security Accelya UK Clearing and Settlement 31 December 2009 Trustwave www.accelya.com ADB-UTVECKLING AB Payment gateway 30 November 2009 Europoint Networking WWW.ADBUTVECKLING.SE AB Adeptra Fraud Prevention 30 November 2009 Protiviti Inc. www.adeptra.com Debt Collection Card Activation Adflex Payment Processing 31 March 2010 Evolution LTD www.adflex.co.uk Payment Gateway/Switch Clearing & settlement 1 A PCI DSS assessment only represents a ‘snapshot’ of the security in place at the time of the review, and does not guarantee that those security controls remain in place after the review is complete. -

In This Issue

Welcome to the January edition of ACT News. This complimentary service is provided by ACT Canada; "building an informed marketplace". Please feel free to forward this to your colleagues. In This Issue 1. Editorial - payment innovation: where is the bar? 2. Desjardins and MasterCard bring new payment options to Canadians 3. Nanopay acquires MintChip from the Royal Canadian Mint 4. Canadian payments market transition: a study by the Canadian Payments Association 5. Suretap and EnStream take big steps forward with Societe de Transport de Montreal in mobile ticketing 6. New credit union association launches in Canada: Canadian Credit Union Association 7. Global study shows increasing security risks to payment data and lack of confidence in securing mobile payment methods 8. Samsung Pay to move online in 2016 9. Elavon delivers Apple Pay for Canadian businesses 10. Beware alleged experts’ scare tactics on mobile payments 11. Ingenico Group accelerates EMV and NFC acceptance in unattended environments with new partner program 12. Paynet delivers a safer payment service with Fraudxpert to its customers 13. VeriFone expands services offering for large retailers in the US and Canada with agreement to acquire AJB Software 14. VISA checkout added to Starbucks, Walmart, Walgreens 15. Gemalto is world's first vendor to receive complete MasterCard approval for cloud based payments 16. ICC Solutions offers a time-saving method and free guide for training staff to process card payments correctly ready for the new year! 17. Walmart adds masterpass as online payment method 18. Equinox and ACCEO partner to deliver integrated retail payment solution 19. UL receives UnionPay qualification for Chinese domestic market 20. -

Directors' Report

Directors’ Report I. ECONOMIC BACKDROP AND BANKING ENVIRONMENT GLOBAL ECONOMIC The global trade slowed down to 2.2% in 2016 As a result of very good rainfall during owing to sluggish investment and inventory monsoon 2016 and various policy initiatives SCENARIO adjustment. However, it is likely to benefit taken by the Government, the country has from expected increase in global demand, Global growth remained stagnant at 3.1%. witnessed record foodgrain production in albeit increasing protectionist policies remain On the global level, while the advanced FY2017. As per Third Advance Estimates for a matter of concern. The overall world GDP is economies’ performance eased modestly in FY2017, total foodgrain production in the expected to grow by 3.5% in 2017. However, 2016 when compared to 2015, the emerging country is estimated at 273.38 million tonnes, deepening geo-political tensions in the market and developing economies performed which is higher by 8.34 million tonnes than Middle East and North Africa region, faster somewhat better. The US experienced a the previous record foodgrain production than expected Fed rate hike and increase lower GDP growth since 2011, thereby, of 265.04 million tonnes achieved during in protectionism policies by the advanced acting as a drag on the overall advanced FY2014 and significantly higher by 21.81 economies are the key risks that can put economies’ growth. UK slowed down against million tonnes than the last year’s foodgrain downward pressure on global economic the backdrop of weaker net exports. Euro production. activity. Area as a whole, however, registered a tad higher growth in 2016 when compared to Both Wholesale Price Index (WPI) and Another aspect that influences global growth 2015. -

AUTOMATED TELLER MACHINE (Athl) NETWORK EVOLUTION in AMERICAN RETAIL BANKING: WHAT DRIVES IT?

AUTOMATED TELLER MACHINE (AThl) NETWORK EVOLUTION IN AMERICAN RETAIL BANKING: WHAT DRIVES IT? Robert J. Kauffiiian Leollard N.Stern School of Busivless New 'r'osk Universit,y Re\\. %sk, Net.\' York 10003 Mary Beth Tlieisen J,eorr;~rd n'. Stcr~iSchool of B~~sincss New \'orl; University New York, NY 10006 C'e~~terfor Rcseai.clt 011 Irlfor~i~ntion Systclns lnfoornlation Systen~sI)epar%ment 1,eojrarcl K.Stelm Sclrool of' Busir~ess New York ITuiversity Working Paper Series STERN IS-91-2 Center for Digital Economy Research Stem School of Business Working Paper IS-91-02 Center for Digital Economy Research Stem School of Business IVorking Paper IS-91-02 AUTOMATED TELLER MACHINE (ATM) NETWORK EVOLUTION IN AMERICAN RETAIL BANKING: WHAT DRIVES IT? ABSTRACT The organization of automated teller machine (ATM) and electronic banking services in the United States has undergone significant structural changes in the past two or three years that raise questions about the long term prospects for the retail banking industry, the nature of network competition, ATM service pricing, and what role ATMs will play in the development of an interstate banking system. In this paper we investigate ways that banks use ATM services and membership in ATM networks as strategic marketing tools. We also examine how the changes in the size, number, and ownership of ATM networks (from banks or groups of banks to independent operators) have impacted the structure of ATM deployment in the retail banking industry. Finally, we consider how movement toward market saturation is changing how the public values electronic banking services, and what this means for bankers. -

Defendant Apple Inc.'S Proposed Findings of Fact and Conclusions Of

Case 4:20-cv-05640-YGR Document 410 Filed 04/08/21 Page 1 of 325 1 THEODORE J. BOUTROUS JR., SBN 132099 MARK A. PERRY, SBN 212532 [email protected] [email protected] 2 RICHARD J. DOREN, SBN 124666 CYNTHIA E. RICHMAN (D.C. Bar No. [email protected] 492089; pro hac vice) 3 DANIEL G. SWANSON, SBN 116556 [email protected] [email protected] GIBSON, DUNN & CRUTCHER LLP 4 JAY P. SRINIVASAN, SBN 181471 1050 Connecticut Avenue, N.W. [email protected] Washington, DC 20036 5 GIBSON, DUNN & CRUTCHER LLP Telephone: 202.955.8500 333 South Grand Avenue Facsimile: 202.467.0539 6 Los Angeles, CA 90071 Telephone: 213.229.7000 ETHAN DETTMER, SBN 196046 7 Facsimile: 213.229.7520 [email protected] ELI M. LAZARUS, SBN 284082 8 VERONICA S. MOYÉ (Texas Bar No. [email protected] 24000092; pro hac vice) GIBSON, DUNN & CRUTCHER LLP 9 [email protected] 555 Mission Street GIBSON, DUNN & CRUTCHER LLP San Francisco, CA 94105 10 2100 McKinney Avenue, Suite 1100 Telephone: 415.393.8200 Dallas, TX 75201 Facsimile: 415.393.8306 11 Telephone: 214.698.3100 Facsimile: 214.571.2900 Attorneys for Defendant APPLE INC. 12 13 14 15 UNITED STATES DISTRICT COURT 16 FOR THE NORTHERN DISTRICT OF CALIFORNIA 17 OAKLAND DIVISION 18 19 EPIC GAMES, INC., Case No. 4:20-cv-05640-YGR 20 Plaintiff, Counter- DEFENDANT APPLE INC.’S PROPOSED defendant FINDINGS OF FACT AND CONCLUSIONS 21 OF LAW v. 22 APPLE INC., The Honorable Yvonne Gonzalez Rogers 23 Defendant, 24 Counterclaimant. Trial: May 3, 2021 25 26 27 28 Gibson, Dunn & Crutcher LLP DEFENDANT APPLE INC.’S PROPOSED FINDINGS OF FACT AND CONCLUSIONS OF LAW, 4:20-cv-05640- YGR Case 4:20-cv-05640-YGR Document 410 Filed 04/08/21 Page 2 of 325 1 Apple Inc. -

A Behavioral Economics Approach to Regulating Initial Coin Offerings

A Behavioral Economics Approach to Regulating Initial Coin Offerings NATHAN J. SHERMAN* INTRODUCTION Initial coin offerings (ICOs) are an outgrowth of the cryptocurrency space in which companies raise capital by issuing their own cryptocurrency coin to investors. Although ICOs are an innovative method of raising capital, the growth of the ICO market is troubling considering no investor protection regulations govern the ICO process. Investors pour large amounts of money into these offerings, which are issued by companies that typically have no history of producing a product or revenue, and the prices of coins issued in ICOs are only rising because other investors also funnel money into them.1 This pattern is markedly similar to that of a speculative bubble. A speculative bubble occurs when there are “‘unsustainable increases’ in asset prices caused by investors trading on a pattern of price increases rather than information on fundamental values.”2 In a bubble, “smart money”—informed investors—bid up prices in anticipation of “noise traders” entering the market.3 The noise traders then enter the market due to the psychological biases they encounter in making their investment decisions.4 Eventually, the smart money investors sell their holdings and the bubble bursts. 5 Thus, regulators should create a framework that adequately protects investors in ICOs. The behavioral economics theory of bounded rationality provides insights for building this regulatory framework. Bounded rationality implies that humans make suboptimal choices.6 By understanding the psychological biases that influence investors’ choices, regulators will be able to help investors adopt habits that reduce the harmful effects of speculative bubbles.