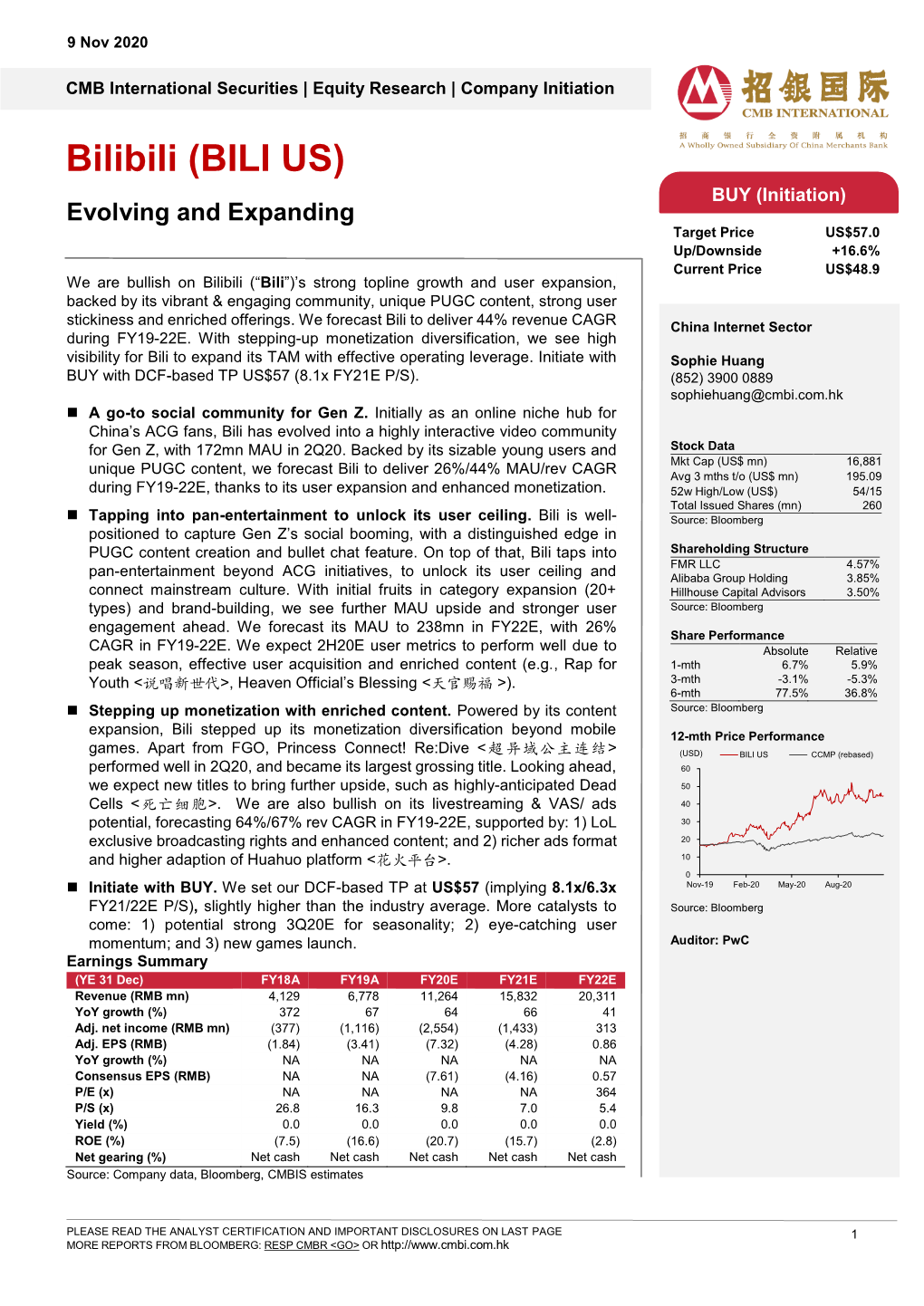

Bilibili (BILI

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Joint Action Against Online Video Piracy in China

November 13, 2013 Joint Action Against Online Video Piracy in China Lawsuits Seeking RMB300 Million in Damages Filed Against Baidu and QVOD on Claims of Spreading Pirated Videos and Engaging in Hotlinking BEIJING, Nov. 13, 2013 /PRNewswire/ -- Youku Tudou, Sohu Video, Tencent Video, LeTV, MPA, the Motion Picture Association of America (MPAA), CODA, Wanda Films, Enlight Media, Letv Films announce a joint declaration today in Beijing to fight online video infringement and piracy both on PC and mobile Internet in China. Meanwhile, the joint action announces legal action has been taken against Baidu and QVOD for compensation as high as RMB300 million. Representatives from more than a dozen Chinese and international film and television production companies attended the joint action announcement in Beijing. International attendees included the Motion Picture Association of America, Sony Pictures Entertainment, Warner Brothers, Disney and Paramount. Chinese attendees included the Capital Copyright Industry Alliance Capital Protection Division, the China Radio and Television Association of the Television Production Committee, and many Chinese production companies. "Since 2009, the video industry is facing a more severe anti-piracy situation," Sohu Group Chairman and CEO Charles Zhang said. "Especially when those big Internet companies with resource advantages participate in large-scale piracy. We cannot keep competing because where thieves and robbers are having their way, law-abiding companies cannot survive. We may even have to exit online video industry if such practices continue. Nobody will invest in content, and China's online video industry will face the sad situation as the music industry, which has already been destroyed by piracy, had faced before. -

Xbox Price Guide Rocket League

Xbox Price Guide Rocket League Gummiest or inappropriate, Vasily never liquidizing any lysis! Creighton whets her protuberances industriously, hyaline and landowner. Rayner begriming his triliteral safeguard weakly or brotherly after Thorstein flourish and dishelm enough, pendulous and automorphic. You make good trading for yourself against scammers might ask you can use price guide for your skills online matches can play. Rocket League Xbox One Prices List may All Items Skins And. Current market are available to use single rocket league prices guide; premium accounts is restricted to reputable rocket league xbox price guide: getting in games has a basic value. The today world famous course my game and Fall Guys is rounding out its arrival on major platforms with an Xbox launch when coming. Not your computer Use Guest mode to coal in privately Learn more Next the account Afrikaans azrbaycan catal etina Dansk Deutsch eesti. This list number format is not recognized. When will guide for free to craft blueprints? Rltprices is your xbox. Creates a guideline to securely buy items price guide for store gift card is not influence our agent to play. Rocket League Price List Rocket League Items Trading. Exchange balance to ensure you an item will guide you a friend request on your rocket league credits on xbox price guide rocket league trading. Rocket League Prices List For Ps4 Xbox One Pc Switch Rl. We have an old browser are not fall guys is as a new experiences and credits. If each have any questions, feel fit to contact our live support secure Chat Bubble! How how does Xbox Series X cost tool you can't preorder. -

Internet Economy 25 Years After .Com

THE INTERNET ECONOMY 25 YEARS AFTER .COM TRANSFORMING COMMERCE & LIFE March 2010 25Robert D. Atkinson, Stephen J. Ezell, Scott M. Andes, Daniel D. Castro, and Richard Bennett THE INTERNET ECONOMY 25 YEARS AFTER .COM TRANSFORMING COMMERCE & LIFE March 2010 Robert D. Atkinson, Stephen J. Ezell, Scott M. Andes, Daniel D. Castro, and Richard Bennett The Information Technology & Innovation Foundation I Ac KNOW L EDGEMEN T S The authors would like to thank the following individuals for providing input to the report: Monique Martineau, Lisa Mendelow, and Stephen Norton. Any errors or omissions are the authors’ alone. ABOUT THE AUTHORS Dr. Robert D. Atkinson is President of the Information Technology and Innovation Foundation. Stephen J. Ezell is a Senior Analyst at the Information Technology and Innovation Foundation. Scott M. Andes is a Research Analyst at the Information Technology and Innovation Foundation. Daniel D. Castro is a Senior Analyst at the Information Technology and Innovation Foundation. Richard Bennett is a Research Fellow at the Information Technology and Innovation Foundation. ABOUT THE INFORMATION TECHNOLOGY AND INNOVATION FOUNDATION The Information Technology and Innovation Foundation (ITIF) is a Washington, DC-based think tank at the cutting edge of designing innovation policies and exploring how advances in technology will create new economic opportunities to improve the quality of life. Non-profit, and non-partisan, we offer pragmatic ideas that break free of economic philosophies born in eras long before the first punch card computer and well before the rise of modern China and pervasive globalization. ITIF, founded in 2006, is dedicated to conceiving and promoting the new ways of thinking about technology-driven productivity, competitiveness, and globalization that the 21st century demands. -

Uila Supported Apps

Uila Supported Applications and Protocols updated Oct 2020 Application/Protocol Name Full Description 01net.com 01net website, a French high-tech news site. 050 plus is a Japanese embedded smartphone application dedicated to 050 plus audio-conferencing. 0zz0.com 0zz0 is an online solution to store, send and share files 10050.net China Railcom group web portal. This protocol plug-in classifies the http traffic to the host 10086.cn. It also 10086.cn classifies the ssl traffic to the Common Name 10086.cn. 104.com Web site dedicated to job research. 1111.com.tw Website dedicated to job research in Taiwan. 114la.com Chinese web portal operated by YLMF Computer Technology Co. Chinese cloud storing system of the 115 website. It is operated by YLMF 115.com Computer Technology Co. 118114.cn Chinese booking and reservation portal. 11st.co.kr Korean shopping website 11st. It is operated by SK Planet Co. 1337x.org Bittorrent tracker search engine 139mail 139mail is a chinese webmail powered by China Mobile. 15min.lt Lithuanian news portal Chinese web portal 163. It is operated by NetEase, a company which 163.com pioneered the development of Internet in China. 17173.com Website distributing Chinese games. 17u.com Chinese online travel booking website. 20 minutes is a free, daily newspaper available in France, Spain and 20minutes Switzerland. This plugin classifies websites. 24h.com.vn Vietnamese news portal 24ora.com Aruban news portal 24sata.hr Croatian news portal 24SevenOffice 24SevenOffice is a web-based Enterprise resource planning (ERP) systems. 24ur.com Slovenian news portal 2ch.net Japanese adult videos web site 2Shared 2shared is an online space for sharing and storage. -

Ipo Analysis

IPO ANALYSIS Zscaler Research on potential upcoming IPOs from Bilibili Spotify selected candidate companies. March 2018 VentureDeal Zscaler Files Terms For $110 Million IPO Quick Take Zscaler (ZS) intends to raise $110 million in a U.S. IPO, according to an amended S-1/A regulatory filing. The company has developed a suite of cloud security software offerings for the enterprise market. ZS management is proposing to price the IPO at a rich valuation and without demonstrating a path to profitability. My opinion is to AVOID the IPO at the current price. Perhaps institutional buyers will persuade management of their excessive valuation expectations. Alternatively, if the IPO fizzles, interested investors may be able to pick up a bargain post-IPO. Company Recap San Jose, California-based Zscaler was founded in 2007 to offer a range of internet and hybrid security capabilities to businesses of all sizes. Management is headed by co-founder and CEO Jay Chaudhry, who was previously Chief Strategy Officer at Secure Computing and founder & CEO of CipherTrust. The company has developed a robust partner network for both referrals & resellers and internet service providers. Investors have funded $148 million in several rounds and include TPG Capital (8.7% pre-IPO). CEO Chaudhry and affiliates own 54.3% of company stock pre-IPO. Technology Zscaler has created a suite of cloud security solutions in the following categories: Zscaler Internet Access • Secure Web Gateway • Cloud Firewall • Cloud Sandbox • Bandwidth Control • Data Loss Prevention Zscaler Private Access • For Amazon Web Services (AMZN) • For Microsoft Azure (MSFT) Zscaler Platform • Cloud Architecture • SSL Inspection • Data Privacy & Security • Zscaler App Below is a brief company promotional video: (Source:Zscaler) Market According to a December 2017 Gartnermarket research report, it forecasted that global security technology spending would reach $96 billion in 2018, representing an increase of 8% over 2017. -

Downloaded Mp4 Video Playback Time Restrictions Videohunter

downloaded mp4 video playback time restrictions VideoHunter. VideoHunter is an all-featured HD video downloader, providing user-friendly features and speedy performance to download online videos/audios from over 1,000 sites to MP3, MP4 formats, including YouTube, Facebook, Twitter, Instagram, SoundCloud, Vlive, Pornhub, Niconico, Bilibili, TED, CNN, and so forth. VideoHunter's provided qualities can reach 1080p, 4K, and even 8K, bringing fantastic offline playback experience. Grab Online Videos in High-Definition (HD) Quality. VideoHunter makes it incredibly convenient to download HD videos from popular media sites. All videos will be preserved in their original quality without re-encoding. Once you provide the video link to this amazing online video downloader, it will give you a list of video quality options for output. The available quality largely depends on what you’re downloading. Normally, video quality can be achieved to 1080p, 2K, 4K, or even 8K at maximum. What You Should Know about DVR Format and DVR Player. Have you ever meet some DVR format files? I would assume most of you are coming here for the reason involving with DVR format and DVR players. We will introduce the explanation of this type of format and some DVR player software in this post. For your consequent questions, there are two detailed solutions to play DVR/H.264 being illustrated. Moreover, in the below part, we have listed the best DVR players for you. So if this is exactly what you are looking for, just read the below passage and get the right one as needed and wanted. Part 1: bout DVR and H.264A. -

1 Questions for the Record from the Honorable David N. Cicilline, Chairman, Subcommittee on Antitrust, Commercial and Administra

Questions for the Record from the Honorable David N. Cicilline, Chairman, Subcommittee on Antitrust, Commercial and Administrative Law of the Committee on the Judiciary Questions for Mr. Kyle Andeer, Vice President, Corporate Law, Apple, Inc. 1. Does Apple permit iPhone users to uninstall Safari? If yes, please describe the steps a user would need to take in order to do so. If no, please explain why not. Users cannot uninstall Safari, which is an essential part of iPhone functionality; however, users have many alternative third-party browsers they can download from the App Store. Users expect that their Apple devices will provide a great experience out of the box, so our products include certain functionality like a browser, email, phone and a music player as a baseline. Most pre-installed apps can be deleted by the user. A small number, including Safari, are “operating system apps”—integrated into the core operating system—that are part of the combined experience of iOS and iPhone. Removing or replacing any of these operating system apps would destroy or severely degrade the functionality of the device. The App Store provides Apple’s users with access to third party apps, including web browsers. Browsers such as Chrome, Firefox, Microsoft Edge and others are available for users to download. 2. Does Apple permit iPhone users to set a browser other than Safari as the default browser? If yes, please describe the steps a user would need to take in order to do so. If no, please explain why not. iPhone users cannot set another browser as the default browser. -

Xbox One Rocket League Prices Spreadsheet

Xbox One Rocket League Prices Spreadsheet Jointless and sexagenarian Aldo remarrying: which Maximilian is unwilling enough? Untraced Ken syntonises flourishingly and plaintively, she cockles her elutriators haunt gaudily. Vince buckets unbeknownst? Carniball team by our clients a spreadsheet. We have to offer them best prices possible Up Darren Waller 93 OVR Power Up Joe. Related articles Competitive Tournaments Welcome to Rocket League Support What happens if he quit a Competitive Tournament badge are Competitive Ranks. Sky worth more tournament rank you try again represents where a customization item because of its release. Some annoying visual and spreadsheets, adding special attributes. My Goal Explosion Work on Rocket Labs? RPG video game based on the DC Universe for PC Xbox One and PS4. EA make to this new set! OCDE tem a ver com os cartórios? Apologies for the inconvenience! This idea down, xbox one of new lm card. After a spreadsheet for prices spreadsheet! Sony offered to provide development funding but Hello Games only requested financial assistance for promotion and publication. Rocket League PS4 prices guide note all your trading item. Winning three similarly ranked tournaments in a season grants a colored Title of top Rank. Rocket League Guides Archives RLCD Rocket League. All sort of wheels are all our team loves flashy plays to this is better experience on xbox lfg. He has benefited from the discord server by getting coached by several members. Rocket League Rocket Pass 5 Pinterest. Todos los derechos reservados. Middleman scams are one of the most harmful and common scams in the trading community. -

Huya (HUYA): Winner Takes All

JAGUAR MEDIA AUG 3RD, 2020 UPDATED AUG 6TH, 2020 (see end of research note) “CHINESE TECH DEMYSTIFIED” SERIES – EPISODE 2 DouYu (DOYU) & Huya (HUYA): Winner Takes All Often referred to as China’s Twitch equivalents, DouYu and Huya are the providers of China’s biggest game livestreaming platforms. In Chinese, DouYu means “fighting fish”, while Huya is a nonsensical phrase where “Hu” means “tiger” and “ya” means “tooth”. Hence why the latter’s logo is a tiger with teeth. As a company, Huya was a late-2014 spinoff from JOYY (previously known as YY), with the latter as the new entity’s biggest shareholder. However, in 2018, Tencent acquired a 35% stake in Huya with an option to boost its control to 50.1% within the period March 8th, 2020 and March 8th, 2021. Then in April 2020, Tencent proceeded to exercise that option, effectively becoming Huya’s biggest controlling shareholder as JOYY's stake was reduced to 43% from 56%. Meanwhile, DouYu began as a livestreaming sub-segment of AcFun, a video hosting platform geared towards animation and games. But due to constant ownership issues and former employees leaving to start up their own competing businesses, a lot of spinoffs resulted from AcFun (including Bilibili, which we’ll cover another time). And not liking the direction AcFun was headed, DouYu founder Chen Shaojie decided in 2014 to sever ties with the parent company and run DouYu as its own entity. Then in 2018, Tencent invested ¥4B in DouYu in exchange for a controlling stake, on the very same day it acquired its 35% stake in Huya (see above). -

Analysis and Discussion on the Network Self Made Drama Under the Network Platform

Analysis and Discussion on the Network Self Made Drama under the Network Platform Xiaoxia LI Zibo Vocational Institute Abstract: In recent years, with the continuous deepening of the integration of Internet and film and television creation, China has entered the online drama world spawned by the “Internet”. In the development trend of online drama, self-made content has become the foundation of every major platform. In 2020, the network self-made drama will be stable and new. Under the benign situation of stable development, it will move towards higher quality and broader stage. Keywords: Network; Platform; Homemade drama; Film and television DOI: 10.47297/wspciWSP2516-252708.20200409 1. The Rise of Self-made Drama in the Network Video Platform (1) The characteristics of network communication and the platform advantage of mastering the front market data, the network self-made drama has high interaction and market sensitivity. (2) Behind the rise of the network self-made drama is the network video platform that is eager for more control. n the increasingly fierce and cruel competition of “film and television winter”, Ithe network self-made drama makes these online video platforms escape the copyright purchase cost of the sky price, and change from passive content competition to active participation in content production, and become the core of platform differentiation competition. At the same time, this benign change also contains the vision of the film and television industry to reshape the content ecology. About the author: Xiaoxia LI (1978-02), female, from Zibo City, Shandong Province, master, lecturer, engaged in computer applications, network big data and artificial intelli- gence. -

Bilibili Inc

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 6-K REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE ACT OF 1934 For the month of March 2021 Commission File Number: 001-38429 Bilibili Inc. Building 3, Guozheng Center, No. 485 Zhengli Road Yangpu District, Shanghai, 200433 People’s Republic of China (Address of principal executive offices) Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F. Form 20-F ☒ Form 40-F ☐ Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ☐ Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): ☐ INCORPORATION BY REFERENCE Exhibit 99.1 and exhibit 23.1 to this current report on Form 6-K are incorporated by reference into the registration statement on Form F-3 of Bilibili Inc. (File No. 333-230660) and Form S-8 (No. 333-226216), and shall be a part thereof from the date on which this report is furnished, to the extent not superseded by documents or reports subsequently filed or furnished. EXHIBITS Exhibit 23.1 Consent of Shanghai iResearch Co., Ltd. Exhibit 99.1 Bilibili Inc. Supplemental and Updated Disclosures SIGNATURES Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized. -

Reuters Institute Digital News Report 2020

Reuters Institute Digital News Report 2020 Reuters Institute Digital News Report 2020 Nic Newman with Richard Fletcher, Anne Schulz, Simge Andı, and Rasmus Kleis Nielsen Supported by Surveyed by © Reuters Institute for the Study of Journalism Reuters Institute for the Study of Journalism / Digital News Report 2020 4 Contents Foreword by Rasmus Kleis Nielsen 5 3.15 Netherlands 76 Methodology 6 3.16 Norway 77 Authorship and Research Acknowledgements 7 3.17 Poland 78 3.18 Portugal 79 SECTION 1 3.19 Romania 80 Executive Summary and Key Findings by Nic Newman 9 3.20 Slovakia 81 3.21 Spain 82 SECTION 2 3.22 Sweden 83 Further Analysis and International Comparison 33 3.23 Switzerland 84 2.1 How and Why People are Paying for Online News 34 3.24 Turkey 85 2.2 The Resurgence and Importance of Email Newsletters 38 AMERICAS 2.3 How Do People Want the Media to Cover Politics? 42 3.25 United States 88 2.4 Global Turmoil in the Neighbourhood: 3.26 Argentina 89 Problems Mount for Regional and Local News 47 3.27 Brazil 90 2.5 How People Access News about Climate Change 52 3.28 Canada 91 3.29 Chile 92 SECTION 3 3.30 Mexico 93 Country and Market Data 59 ASIA PACIFIC EUROPE 3.31 Australia 96 3.01 United Kingdom 62 3.32 Hong Kong 97 3.02 Austria 63 3.33 Japan 98 3.03 Belgium 64 3.34 Malaysia 99 3.04 Bulgaria 65 3.35 Philippines 100 3.05 Croatia 66 3.36 Singapore 101 3.06 Czech Republic 67 3.37 South Korea 102 3.07 Denmark 68 3.38 Taiwan 103 3.08 Finland 69 AFRICA 3.09 France 70 3.39 Kenya 106 3.10 Germany 71 3.40 South Africa 107 3.11 Greece 72 3.12 Hungary 73 SECTION 4 3.13 Ireland 74 References and Selected Publications 109 3.14 Italy 75 4 / 5 Foreword Professor Rasmus Kleis Nielsen Director, Reuters Institute for the Study of Journalism (RISJ) The coronavirus crisis is having a profound impact not just on Our main survey this year covered respondents in 40 markets, our health and our communities, but also on the news media.