Bce Inc. 2013 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CHANNEL LISTING FIBE TV from Your Smartphone

Now you can watch your Fibe TV Download the Fibe TV content and manage recordings app today at CHANNEL LISTING FIBE TV from your smartphone. bell.ca/fibetvapp. CURRENT AS OF FEBRUARY 25, 2016. E MUCHMUSIC HD ........................................1570 TREEHOUSE ...................................................560 GOOD E! .............................................................................621 MYTV BUFFALO (WNYO) ..........................293 TREEHOUSE HD .........................................1560 E! HD ...................................................................1621 MYTV BUFFALO HD ..................................1293 TSN1 ....................................................................400 F N TSN1 HD ..........................................................1400 A FOX ......................................................................223 NBC - EAST .................................................... 220 TSN RADIO 1050 ..........................................977 ABC - EAST .......................................................221 FOX HD ............................................................1223 NBC HD - EAST ...........................................1220 TSN RADIO 1290 WINNIPEG ..................979 ABC HD - EAST ............................................. 1221 H NTV - ST. JOHN’S .........................................212 TSN RADIO 990 MONTREAL ................980 A&E .......................................................................615 HGTV................................................................ -

Grille Des Canaux Classique Février 2019

Shaw Direct | Grille des canaux classique février 2019 Légende 639 CTV Prince Albert ..................................... 092 Nat Geo WILD HD..................................... 210 ICI Télé Montreal HD ............................... 023 CTV Regina HD .......................................... 091 National Geographic HD ...................... 707 ICI Télé Ontario .......................................... Chaînes HD 648 CTV Saint John ........................................... 111 NBA TV Canada HD ................................. 221 ICI Télé Ottawa-Gatineau HD ............ ...............Chaîne MPEG-4 378 CTV Saskatoon .......................................... 058 NBC East HD (Detroit) ........................... 728 ICI Télé Quebec.......................................... La liste des chaînes varie selon la région.* 641 CTV Sault Ste. Marie ................................ 063 NBC West HD (Seattle) ............................... 732 ICI Télé Saguenay ..................................... 356 CTV Sudbury .................................................... 116 NFL Network HD....................................... 223 ICI Télé Saskatchewan HD ................... 650 CTV Sydney ................................................. 208 Nickelodeon HD ........................................ 705 ICI Télé Trois-Rivieres ............................. 642 CTV Timmins ............................................... 489 Northern Legislative Assembly ........ 769 La Chaîne Disney ..................................... -

2011 BCE Annual Information Form

Annual Information Form BCE Inc. For the year ended December 31, 2011 March 8, 2012 In this Annual Information Form, Bell Canada is, unless otherwise indicated, referred to as Bell, and comprises our Bell Wireline, Bell Wireless and Bell Media segments. Bell Aliant means, collectively, Bell Aliant Inc. and its subsidiaries. All dollar figures are in Canadian dollars, unless stated otherwise. The information in this Annual Information Form is as of March 8, 2012, unless stated otherwise, and except for information in documents incorporated by reference that have a different date. TABLE OF CONTENTS PARTS OF MANAGEMENT’S DISCUSSION & ANALYSIS AND FINANCIAL STATEMENTS ANNUAL INCORPORATED BY REFERENCE INFORMATION (REFERENCE TO PAGES OF THE BCE INC. FORM 2011 ANNUAL REPORT) Caution Regarding Forward-Looking Statements 2 32-34; 54-69 Corporate Structure 4 Incorporation and Registered Offices 4 Subsidiaries 4 Description of Our Business 5 General Summary 5 23-28; 32-36; 41-47 Strategic Imperatives 6 29-31 Our Competitive Strengths 6 Marketing and Distribution Channels 8 Our Networks 9 32-34; 54-69 Our Employees 12 Corporate Responsibility 13 Competitive Environment 15 54-57 Regulatory Environment 15 58-61 Intangible Properties 15 General Development of Our Business 17 Three-Year History (1) 17 Our Capital Structure 20 BCE Inc. Securities 20 112-114 Bell Canada Debt Securities 21 Ratings for BCE Inc. and Bell Canada Securities 21 Ratings for Bell Canada Debt Securities 22 Ratings for BCE Inc. Preferred Shares 22 Outlook 22 General Explanation 22 Explanation of Rating Categories Received for our Securities 24 Market for our Securities 24 Trading of our Securities 25 Our Dividend Policy 27 Our Directors and Executive Officers 28 Directors 28 Executive Officers 30 Directors’ and Executive Officers’ Share Ownership 30 Legal Proceedings 31 Lawsuits Instituted by BCE Inc. -

Calculation M90-0021, 'Building Spray and Decay Heat Pump Npsha/R, Revision 13, Attachment

PROGRESS ENERGY FLORIDA, INC. CRYSTAL RIVER UNIT 3 DOCKET NUMBER 50 - 302/ LICENSE NUMBER DPR - 72 ATTACHMENT CALCULATION M90-0021 BUILDING SPRAY AND DECAY HEAT PUMP NPSHa/r REVISION 13 Systems WD, DH, BS, MU Calc. Sub-Type Priority Code 4 Quality Class SR NUCLEAR GENERATION GROUP ANALYSIS I CALCULATION M90-0021 (Calculation #) Building Spray and Decay Heat Pump NPSHa/r (Title including structures, systems, components) IZBNP UNIT 0CR3 0HNP Z1RNP aNES aJALL APPROVAL Rev Prepared By ReviewedBy SupervisorB signatur Signature S 13 T.V. Austin D.A. Wise Date Date -gate S- Is Ca0 I oIa A. l (For Vendor Calculations) Vendor N/A Vendor Document No. Owners Review By N/A Date Calculation No. M90-0021 BS & DH Pump NPSH Page i of vii Revision 13 List Of Effective Pages Page Rev Page Rev Page Rev Page Rev i-vii 13 1-101 13 Attachments Attach. Pages Rev Attach. Pages Rev Attach. Pages Rev Number Number Number 1 1 11 12 2 11 24 11 13 2 5 13 13 2 11 25 12 13 3 1 11 14 2 11 26 12 13 4 6 11 15 2 11 27 12 13 5 3 11 16 4 11 28 12 13 6A 1 11 17 1 11 29 2 13 6B 1 11 18 12 13 30 1 13 7 1 11 19 12 13 31 10 13 8 1 11 20 23 13 32 1 13 9 2 11 21 12 13 10 2 11 22 12 13 11 1 13 23 18 11 Amendments Rev& No of Rev & No of Rev & No of Rev & No of Letter Pages Letter Pages Letter Pages Letter Pages I N/A I I I I I I I Calculation No. -

47058.00 BCE Eng Cover

Bell Canada Enterprises Annual Report 1999 say hello to the internet economy Who could have predicted this? Not just the exhilarating vistas unfolding on the Internet, but the speed with which it’s changed how we live, work and play. But wait... there’s more on the way. And BCE is at the centre of it all. We’re Canada’s leading communications services company, at the crossroads where information, e-commerce and entertainment intersect. Through Bell Canada, we help to shape how Canadians access, view and use the Internet. 4 report to shareholders We do this through Bell Nexxia, our national fibre optic backbone; Bell ActiMedia with Sympatico-Lycos, the 16 chairman’s message leading source of Internet content and high-speed access; 18 management’s discussion Bell Mobility, Canada’s foremost wireless company; and and analysis Bell ExpressVu, the leading satellite-TV service. We’re also 37 consolidated financial statements the country’s leading provider of e-commerce solutions, 62 board of directors and delivered by BCE Emergis and CGI. And now, through corporate officers Teleglobe, our business services are also going global. 63 committees of the board 64 shareholder information key indicators ($ millions, except per share amounts) 1999 1998 Revenues 14,214 27,207 Revenues excluding Nortel Networks 14,214 13,579 Net earnings 5,459 4,598 Baseline earnings(1) 1,936 1,592 Baseline earnings per common share (before goodwill expense)(1) 3.26 2.65 1 Excluding special items price range of common shares 1999 1998 High Low Close High Low Close Toronto -

Bell MTS Fibe TV Brochure Instore Printable April1.Indd

Fibe TV & Internet Bell MTS MyAccount Manage your services online, anytime. • Change your TV channels and enjoy them in minutes. • Record your favourite shows while you’re away Fibe TV & from home with MyPVR. • Pay your monthly bill. Internet • Access up to 2 years of billing history. Sign up today at bellmts.ca/myaccount • 4K – with 4x the detail of Full HD, it’s the very best picture quality available.1 • Restart shows in progress or from the past 30 hours.2 • Watch or record up to 4 live HD shows at the same time. • Watch your favourite shows with CraveTM and stream Netflix directly from your set-top box.3 • Worry-free usage with unlimited Internet.4 • Whole Home Wi-Fi – smart and fast Wi-Fi to every room of your home. • Internet access at Bell MTS Wi-Fi hotspots. March, 2019 Channels and pricing listed are subject to change. (1) 4K picture quality requires 4K TV, 4K programming, wired set-top box plus 4K service, and a subscription to Fibe 50 or faster Internet service with Bell MTS. Availability of 4K content is subject to content availability and device capabilities (4K TV). Bell MTS 4K TV Service only available on one TV per household. Residential customers only. (2) Available with select channels/content, excluding US networks and non-local content, and subject to viewing limitations. (3) Netflix and Crave membership required. Crave and all associated logos are trademarks of Bell Media Inc. All rights reserved. (4) Use of the service, including unlimited usage, is subject to compliance with the Bell MTS Terms of Service; BellMTS.ca/legal. -

Small Business Fibe TV Channel List for Current Pricing, Please Visit: Bell.Ca/Businessfibetv

Ontario | May 2016 Small Business Fibe TV Channel List For current pricing, please visit: bell.ca/businessfibetv Starter MTV . 573 HLN Headline News . 508 Investigation Discovery (ID) . 528 Includes over 25 channels MTV HD . 1,573 HLN Headline News HD . 1508 Investigation Discovery (ID) HD . 1528 MuchMusic . 570 KTLA . 298 Lifetime . 335 AMI audio . 49 MyTV Buffalo . 293 KTLA HD . 1298 Lifetime HD . 1335 AMI télé . 50 MyTV Buffalo HD . 1,293 M3 . 571 Love Nature . 1661 AMI TV . 48 Météo Média . 105 M3 HD . 1571 MovieTime . 340 APTN . 214 Météo Média HD . 1105 Mediaset Italia . 698 MovieTime HD . 1340 APTN HD . 1214 NTV - St . John’s . 212 MTV2 . 574 MSNBC HD . 1506 CBC - Local . 205 Radio Centre-Ville . 960 National Geographic . 524 NBA TV Canada . 415 CBC - Local HD . 1205 Radio France Internationale . 971 National Geographic HD . 1524 NBA TV Canada HD . 1415 CHCH . 211 Space . 627 NFL Network . 448 Nat Geo Wild . 530 CHCH HD . 1211 Space HD . 1627 NFL Network HD . 1448 Nat Geo Wild HD . 1530 Citytv - Local . 204 Sportsnet - East . 406 Nuevo Mundo . 865 NBC - West . 285 Citytv - Local HD . 1204 Sportsnet - East HD . 1406 OLN . 411 NBC - West HD . 1285 CPAC - English . 512 Sportsnet - Ontario . 405 OLN HD . 1411 Nickelodeon . 559 CPAC - French . 144 Sportsnet - Ontario HD . 1405 PeachTree TV . 294 Oprah Winfrey Network . 526 CTV - Local . 201 Sportsnet - Pacific . 407 PeachTree TV HD . 1294 Oprah Winfrey Network HD . 1526 CTV - Local HD . 1201 Sportsnet - Pacific HD . 1407 Russia Today . 517 OutTV . 609 CTV Two - Local . 501 Sportsnet - West . 408 Showcase . 616 OutTV HD . -

Broadcasting and Telecommunications Legislative Review

BROADCASTING AND TELECOMMUNICATIONS LEGISLATIVE REVIEW APPENDIX 4 TO SUBMISSION OF CANADIAN NETWORK OPERATORS CONSORTIUM INC. TO THE BROADCASTING AND TELECOMMUNICATIONS LEGISLATIVE REVIEW PANEL 11 JANUARY 2019 BEFORE THE CANADIAN RADIO-TELEVISION AND TELECOMMUNICATIONS COMMISSION IN THE MATTER OF RECONSIDERATION OF TELECOM DECISION 2017-56 REGARDING FINAL TERMS AND CONDITIONS FOR WHOLESALE MOBILE WIRELESS ROAMING SERVICE, TELECOM NOTICE OF CONSULTATION CRTC 2017-259, 20 JULY 2017 SUPPLEMENTAL INTERVENTION OF ICE WIRELESS INC. 27 OCTOBER 2017 TABLE OF CONTENTS EXECUTIVE SUMMARY ...................................................................................................................... 1 1.0 INTRODUCTION .......................................................................................................................... 8 1.1 A note on terminology ................................................................................................................ 9 2.0 SUMMARY OF DR. VON WARTBURG’S REPORT ............................................................... 10 3.0 CANADA’S MOBILE WIRELESS MARKET IS NOT COMPETITIVE .................................. 13 3.1 Canada’s mobile wireless market is extremely concentrated in the hands of the three national wireless carriers ........................................................................................................................ 14 3.2 Mobile wireless penetration rates and mobile data usage indicate that the mobile wireless market is not sufficiently competitive...................................................................................... -

Australian Journal of Telecommunications and the Digital Economy

Australian Journal of Telecommunications and the Digital Economy Volume 5 Issue 4 December 2017 Published by Telecommunications Association Inc. ISSN 2203-1693 Australian Journal of Telecommunications and the Digital Economy AJTDE Volume 5, Number 4, December 2017 Table of Contents Editorial Telecommunications is an Essential Service ii Mark A Gregory Articles Tony Newstead (1923-2017) 87 Mark Newstead, Clemens Pratt, John Burke, Peter Gerrand The Potential for Immersive Technology combined with Online Dating 125 David Evans Bailey Review Preparing the next generation for the Machine Age 1 Peter Gerrand An Introduction to Telecommunications Policy in Canada 97 Catherine Middleton History of Telecommunications Alice Springs Telecommunications Facilities 9 Simon Moorhead Telstra's Future Mode of Operation - the transformation of the Telstra's Network - 1992/93 18 Ian Campbell Historical paper: The 2004 Proposal for the Structural Separation of Telstra 70 Peter Gerrand Australian Journal of Telecommunications and the Digital Economy, ISSN 2203-1693, Volume 5 Number 4 December 2017 Copyright © 2017 i Australian Journal of Telecommunications and the Digital Economy Telecommunications is an Essential Service Editorial Mark A Gregory RMIT University Abstract: The Australian Government has responded to the Productivity Commission inquiry into the Universal Service Obligation (USO). The primary issues identified by the Government include the cost of providing the USO and how it’s provision might be competitively distributed. Secondary issues and issues that did not get a guernsey include improved access to telecommunications (and broadband) for the socially disadvantaged, improved service reliability and quality and an acknowledgement that telecommunications is an essential service. Over the next decade telecommunications will take centre stage as the way that we live, interact with our family and friends and the things around us changes faster than at any time in history. -

An Introduction to Telecommunications Policy in Canada

Australian Journal of Telecommunications and the Digital Economy An Introduction to Telecommunications Policy in Canada Catherine Middleton Ryerson University Abstract: This paper provides an introduction to telecommunications policy in Canada, outlining the regulatory and legislative environment governing the provision of telecommunications services in the country and describing basic characteristics of its retail telecommunications services market. It was written in 2017 as one in a series of papers describing international telecommunications policies and markets published in the Australian Journal of Telecommunications and the Digital Economy in 2016 and 2017. Drawing primarily from regulatory and policy documents, the discussion focuses on broad trends, central policy objectives and major players involved in building and operating Canada’s telecommunications infrastructure. The paper is descriptive rather than evaluative, and does not offer an exhaustive discussion of all telecommunications policy issues, markets and providers in Canada. Keywords: Policy; Telecommunications; Canada Introduction In 2017, Canada’s population was estimated to be above 36.5 million people (Statistics Canada, 2017). Although Canada has a large land mass and low population density, more than 80% of Canadiansi live in urban areas, the majority in close proximity to the border with the United States (Central Intelligence Agency, 2017). Telecommunications services are easily accessible for most, but not all, Canadians. Those in lower-income brackets and/or living in rural and remote areas are less likely to subscribe to telecommunications services than people in urban areas or with higher incomes, and high-quality mobile and Internet services are simply not available in some parts of the country (CRTC, 2017a). On average, Canadian households spend more than $200 (CAD)ii per month to access mobile phone, Internet, television and landline phone services (2015 data, cited in CRTC, 2017a). -

Annual Report

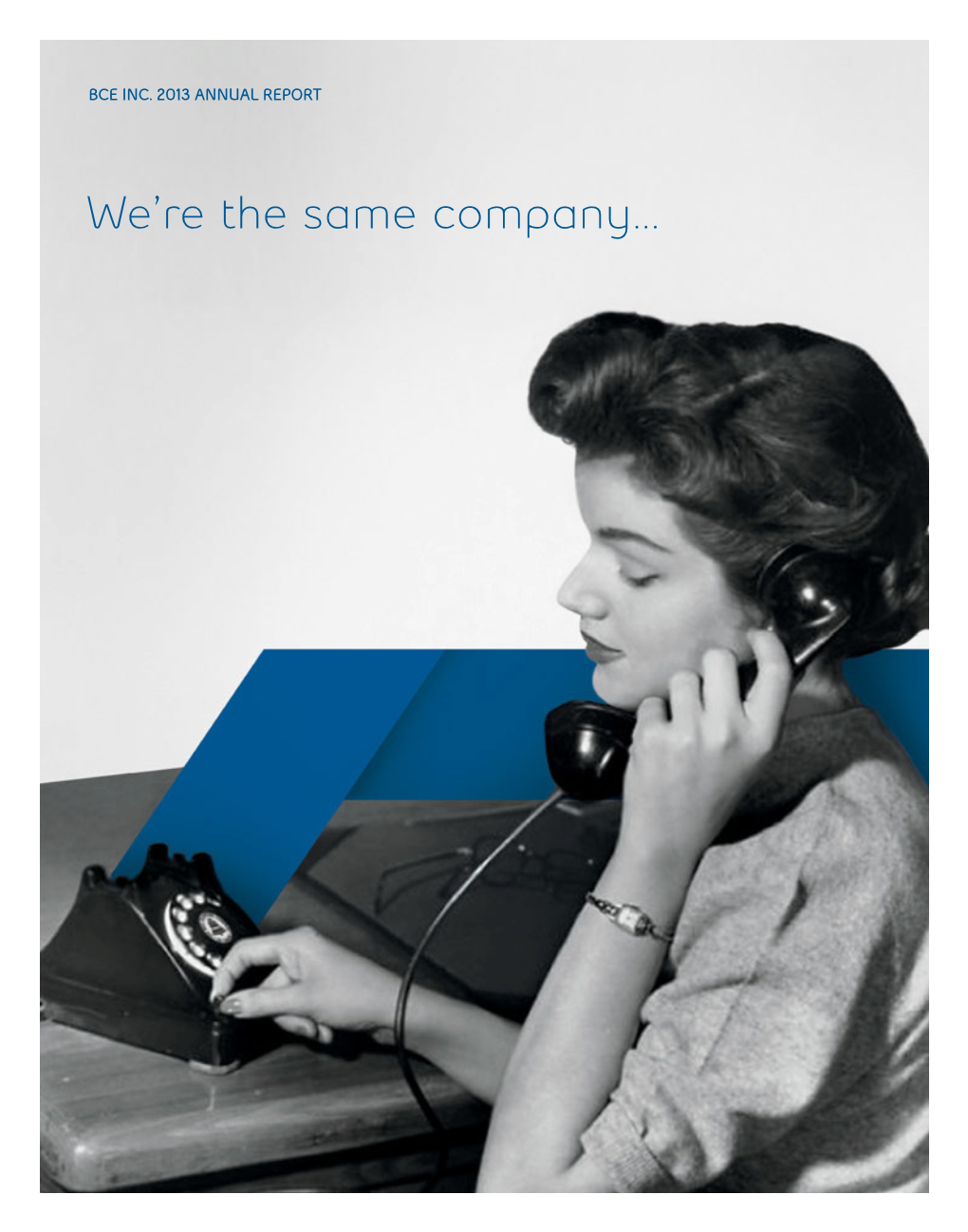

BCE INC. 2013 ANNUAL REPORT We’re the same company… … just totally different. Bell has connected Canadians since 1880, leading the innovation and investment in our nation’s communications networks and services. We have successfully embraced the rapid changes in communications technology, competition and opportunity, building on our 134-year record of service to Canadians with a clear goal, and the strategy and team execution required to achieve it. Our goal: To be recognized by customers as Canada’s leading communications company. Our 6 strategic imperatives 1. Accelerate wireless 10 2. Leverage wireline momentum 12 3. Expand media leadership 14 4. Invest in broadband networks and services 16 5. Achieve a competitive cost structure 17 6. Improve customer service 18 Bell is delivering the next generation of communications and an enhanced service experience to our customers across Canada. In the last five years, our industry-leading investments in world-class networks and communications services like Fibe and LTE, coupled with strong execution by the national team, have re-energized Bell as a nimble competitor setting the pace in TV, Internet, Wireless and Media growth services. We achieved all financial targets in 2013, delivering for our customers and shareholders and giving us strong momentum going into 2014. Financial and operational highlights 4 Letters to shareholders 6 Strategic imperatives 10 Community investment 20 Bell archives 22 Management’s discussion and analysis (MD&A) 24 Reports on internal control 106 Consolidated financial statements 110 Notes to consolidated financial statements 114 Successfully executing our strategic imperatives in a competitive marketplace, Bell achieved all 2013 financial targets and continued to deliver value to shareholders. -

BCE Inc. 2015 Annual Report

Leading the way in communications BCE INC. 2015 ANNUAL REPORT for 135 years BELL LEADERSHIP AND INNOVATION PAST, PRESENT AND FUTURE OUR GOAL For Bell to be recognized by customers as Canada’s leading communications company OUR STRATEGIC IMPERATIVES Invest in broadband networks and services 11 Accelerate wireless 12 Leverage wireline momentum 14 Expand media leadership 16 Improve customer service 18 Achieve a competitive cost structure 20 Bell is leading Canada’s broadband communications revolution, investing more than any other communications company in the fibre networks that carry advanced services, in the products and content that make the most of the power of those networks, and in the customer service that makes all of it accessible. Through the rigorous execution of our 6 Strategic Imperatives, we gained further ground in the marketplace and delivered financial results that enable us to continue to invest in growth services that now account for 81% of revenue. Financial and operational highlights 4 Letters to shareholders 6 Strategic imperatives 11 Community investment 22 Bell archives 24 Management’s discussion and analysis (MD&A) 28 Reports on internal control 112 Consolidated financial statements 116 Notes to consolidated financial statements 120 2 We have re-energized one of Canada’s most respected brands, transforming Bell into a competitive force in every communications segment. Achieving all our financial targets for 2015, we strengthened our financial position and continued to create value for shareholders. DELIVERING INCREASED