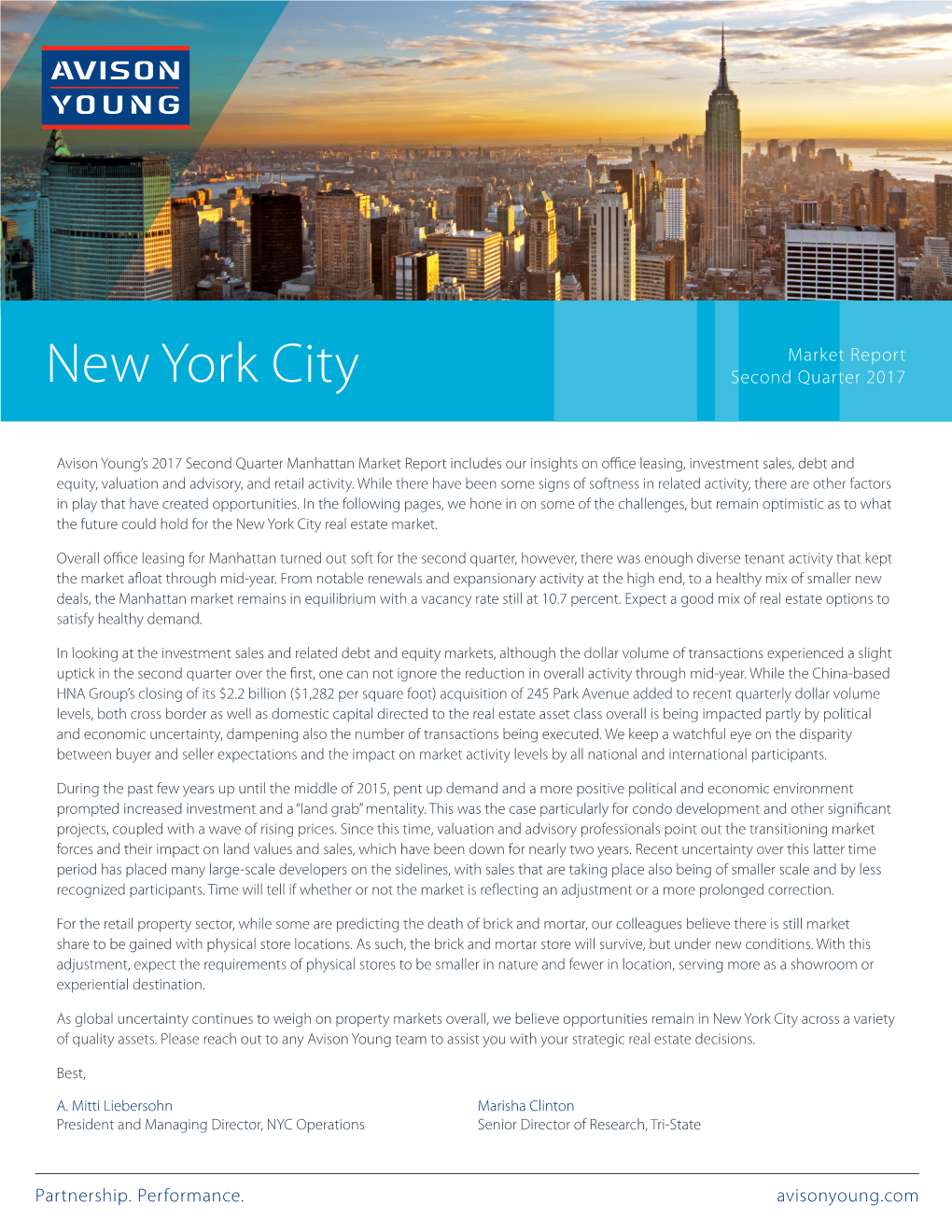

Manhattan Market Overview (Q2 2017)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Seagram Building, First Floor Interior

I.andmarks Preservation Commission october 3, 1989; Designation List 221 IP-1665 SEAGRAM BUIIDING, FIRST FLOOR INTERIOR consisting of the lobby and passenger elevator cabs and the fixtures and interior components of these spaces including but not limited to, interior piers, wall surfaces, ceiling surfaces, floor surfaces, doors, railings, elevator doors, elevator indicators, and signs; 375 Park Avenue, Manhattan. Designed by Ludwig Mies van der Rohe with Philip Johnson; Kahn & Jacobs, associate architects. Built 1956-58. Landmark Site: Borough of Manhattan Tax Map Block 1307, Lot 1. On May 17, 1988, the landmarks Preservation Commission held a public hearing on the proposed designation as a Landmark of the Seagram Building, first floor interior, consisting of the lobby and passenger elevator cabs and the fixtures and interior components of these spaces including but not limited to, interior piers, wall surfaces, ceiling surfaces, floor surfaces, doors, railings, elevator doors, elevator indicators, and signs; and the proposed designation of the related I.and.mark Site (Item No. 2). The hearing had been duly advertised in accordance with the provisions of law. Twenty witnesses, including a representative of the building's owner, spoke in favor of designation. No witnesses spoke in opposition to designation. The Commission has received many letters in favor of designation. DFSCRIPI'ION AND ANALYSIS Summary The Seagram Building, erected in 1956-58, is the only building in New York City designed by architectural master Iudwig Mies van der Rohe. Constructed on Park Avenue at a time when it was changing from an exclusive residential thoroughfare to a prestigious business address, the Seagram Building embodies the quest of a successful corporation to establish further its public image through architectural patronage. -

51-16-President's Personal Files Invitees to Tricia's Wedding 6-12-71

Richard Nixon Presidential Library Contested Materials Collection Folder List Box Number Folder Number Document Date No Date Subject Document Type Document Description 51 16 6/12/1971Personal Other Document Guest List to Tricia's Wedding (1 of 4). Tuesday, June 12, 2012 Page 1 of 1 Presidential Materials Review Board Review on Contested Documents Collection: President's Personal Files Box Number: 144 Folder: Invitees to Tricia's Wedding 6/12/71 Document Disposition 86 Return Private/Personal DOCUMENT WITHDRAWAL RECORD [NIXON PROJECT] DOCUMENT DOCUMENT SUBJECT/TITLE OR CORRESPONDENTS DATE RESTRIC NUMBER TYPE ./. :t. <!~ /.:<, 1971 /V. :J?/ pL.£.C> ~~ - ~oLG~-;:Z I O/.A/J·'V V. c... C<ES k] [ ?~;"a /o-M.-. .£U idzc.6. '>'l ~ (J FILE GROUP TITl.E BOX NUMBER PPF ]Af.l.../ FOLDER TITLE ~.7U.J~~ ,4, RESTRICTION CODES A. Release would violate a Federal statute or Agency Policy. E, Release would disclose trade secrets or confidential com mer, B. National security classified information. financial information. C. Pending or approved claim that release would violate an individual's F. Release would disclose investigatory information compiled f( rights. enforcement purposes. D. Release would constitute a clearly unwarranted invasion of privacy G. Withdrawn and return private and personal matarial. or a libel of a living person. H. Withdrawn and returned non-historical material. NATIONAL ARCHIVES AND RECORDS ADMINISTRATION NA FORM 1421 I " GUEST LIST - Saturday, June 12, 1971 ------------- The President & Mrs. Nixon Miss Patricia, Nixon Mr. Edward Finch Cox Ensign & Mrs. Dwight D. Eisenhower Mr. & Mrs. Robert H. Abplanalp C 10 Hewitt Avenue Bronxville, New York 10708 Mr. -

50Th Anniversary Celebration

STA SUBCONTRACTORS TRADE ASSOCIATION CELEBRATING 50 YEARS 1966-2016 SUBCONTRACTORS TRADE ASSOCIATION 2016 ANNUAL CONSTRUCTION AWARDS DINNER AND 50TH ANNIVERSARY CELEBRATION WEDNESDAY, APRIL 6, 2016 | 6:00PM THE PIERRE HOTEL 2 EAST 61ST STREET, NEW YORK, NY Celebrate the 50th Anniversary with Us and Honor the Accomplishments of Our 2016 Industry Leaders 2016 ANNUAL CONSTRUCTION AWARDS DINNER STA 50TH ANNIVERSARY CELEBRATION SUBCONTRACTORS TRADE ASSOCIATION WE CONGRATULATE THE 2016 HONOREES BUILDER OF THE YEAR CHRIS ZEGLER TURNER CONSTRUCTION SILVER SHOVEL AWARD LINDA CHIARELLI NEW YORK UNIVERSITY CAPITAL PROJECTS & FACILITES THE RONALD BERGER SUBCONTRACTOR OF THE YEAR CHRISTINE DONALDSON BOCCIA JD TRADITIONAL INDUSTRIES LABOR LEADER OF THE YEAR TERRY MOORE LOCAL 46 METALLIC LATHERS JOSEPH F. AZARA JR. • MITCHELL I. MERDINGER • BRIAN J. AZARA 321 39TH STREET • BROOKLYN, NY 11232 718.788.1040 • CDEAIR.COM 2 2016 ANNUAL CONSTRUCTION AWARDS DINNER STA 50TH ANNIVERSARY CELEBRATION SUBCONTRACTORS TRADE ASSOCIATION Dear Members & Friends of the STA, It is my great pleasure to welcome you to the 2016 Subcontractors Trade Association Construction Awards Dinner and 50th Anniversary Celebration. The Subcontractors Trade Association (STA) was founded in 1966 by a group of New York City subcontractors and suppliers who recognized the need for greater representation. Now, 50 years later, the STA represents over 350 companies in every field within the construction industry. In those 50 years, the STA has had a large hand in making a positive difference for subcontractors in many different aspects. The STA advocates on behalf of its members with public and private owners, construction managers and general contractors to ensure that subcontractors receive fair and equitable treatment on their jobs. -

TM 3.1 Inventory of Affected Businesses

N E W Y O R K M E T R O P O L I T A N T R A N S P O R T A T I O N C O U N C I L D E M O G R A P H I C A N D S O C I O E C O N O M I C F O R E C A S T I N G POST SEPTEMBER 11TH IMPACTS T E C H N I C A L M E M O R A N D U M NO. 3.1 INVENTORY OF AFFECTED BUSINESSES: THEIR CHARACTERISTICS AND AFTERMATH This study is funded by a matching grant from the Federal Highway Administration, under NYSDOT PIN PT 1949911. PRIME CONSULTANT: URBANOMICS 115 5TH AVENUE 3RD FLOOR NEW YORK, NEW YORK 10003 The preparation of this report was financed in part through funds from the Federal Highway Administration and FTA. This document is disseminated under the sponsorship of the U.S. Department of Transportation in the interest of information exchange. The contents of this report reflect the views of the author who is responsible for the facts and the accuracy of the data presented herein. The contents do no necessarily reflect the official views or policies of the Federal Highway Administration, FTA, nor of the New York Metropolitan Transportation Council. This report does not constitute a standard, specification or regulation. T E C H N I C A L M E M O R A N D U M NO. -

Office Windows Getting Smarter

Breaking: Office Windows Getting Smarter The success of companies such as View, as well as demand for more energy-efficient buildings, means glass is increasingly more than a means to a view BY DAVID M. LEVITT JANUARY 5, 2021 8:00 AM THE SO-CALLED WALKIE TALKIE TOWER AT 20 FENCHURCH STREET IN LONDON WAS DERIDED EARLY ON FOR THE SCORCHING GLARES THAT ITS GLASS PRODUCED. ALBERTO PEZZALI/NURPHOTO VIA GETTY IMAGES All over the world, glass boxes have not only become inevitable but they’ve gotten smarter than ever before. It’s the material of choice to wrap skyscrapers in, whether they be for office space or luxury condominiums. You even see floor-to-ceiling glass in people’s bathrooms, high up in the sky, so folks can face the world secure in the knowledge that they can only be viewed by those with telescopes or, this being the 2020s, the occasional drone. One World Trade Center, the tallest tower in the Western Hemisphere, is a glass box. So in fact are all the towers—4 and 3 World Trade Center—that have been built in the wake of the terrorist act that destroyed the Twin Towers, killing more than 2,600. So is One Vanderbilt, the 1,500-foot tower built next to Grand Central Terminal, the height of office luxury Over at Hudson Yards, the towers are all glass-dominant, be they office buildings or residential ones. Increasingly, too, this isn’t your grandfather’s glass. The glass used to sheath buildings today is treated and coated with reflective materials to reduce its most unfriendly aspect—that it refracts sunlight and makes buildings, and the tenants inside them, hotter—while maintaining its most positive aspect. -

Commercial Real Estate Thursday, January 17, 2019

A1 The biggest Trophy towers Flushing’s new New York Post, leasing year in flood the sales development decades, p.A22 market, p.A10 boom, p.A6 Commercial Real Estate Thursday, January 17, 2019 Bloomingdale’s gave its sprawling 24-PAGE first-floor REBNY cosmetics and beauty section a nypost.com GALA SPECIAL snazzy makeover FROM THE that debuts today. Bloomingdale’s; COVERGIRL (inset) COVERGIRL Bloomingdale’s; Thanks to new stores and expansions, cosmetics and skincare retail is booming By LOIS WEISS notes David LaPierre of CBRE. lineonly natural brand Innisfree This is in part due to Instagram and — one of over 30 owned by Customers at ROM a retail perspective, YouTube, where social media stars South Korean conglomerate Covergirl’s Times beauty opportunities and celebrities alike can market di Amorepacific — has already Square flagship, never looked better. As rectly to consumers. “Instagram leased four stores in Manhat which opened in consumers crave makeup has become a way of learning about tan, including in the Oculus. November as the and skincare products, new brands,” says Richard Skulnik Represented in its US rollout brand’s first-ever cosmetic companies are of Ripco Real Estate. by Christian Stanton at Cush physical store. finding nooks and crannies Following their customers, man & Wakefield, it just leased a in all parts of the city, innovating many online labels are eager to store at JEMB’s Herald Center, Fnew experiences in the process. make their mark on Manhattan. “New brands are catching fire,” For example, the formerly on See COSMETICS on Page A4 A2 nypost.com Conveniently Thursday, January 17, 2019 Creative New York Post, Artist rendering Partial Fifth Floor 19,587rsf Available 2020 Proposed 112,592 rsf Seventh Floor ▪ Built open creative space Terrace ▪ Exposed ceilings Entire Seventh Floor: 32,826 rsf ▪ Light on three sides Entire Sixth Floor: 49,731 rsf ▪ Move-in condition Partial Fifth Floor: 30,035 rsf ▪ Steps from Grand Central Gary Rosen, Sr. -

Annual Report 2018

ANNUAL REPORT 2018 44415 AR2018__draft_color_rev.indd 1 4/30/19 5:27 PM Contents From the President 2 Speaking Out for Preservation 3 Providing Technical Expertise 8 Preserving Sacred Sites 14 Funding Historic Properties 20 Honoring Excellence 23 Celebrating Living Landmarks 25 Tours and Other Events 29 Our Supporters 31 Financial Statements 37 Board of Directors, Advisory Council, and Staff 38 Our Mission The New York Landmarks Conservancy is dedicated to preserving, revitalizing, and reusing New York’s architecturally significant buildings. Through pragmatic leadership, financial and technical assistance, advocacy, and public education, the Conservancy ensures that New York’s historically and culturally significant buildings, streetscapes, and neighborhoods continue to contribute to New York’s economy, tourism, and quality of life. On the Cover Lucy G. Moses Preservation Award winner - 462 Broadway, Manhattan - Owner Meringoff Properties has returned a French Renaissance-style building to its original glory in the SoHo-Cast Iron Historic District. Platt Byard Dovell White Architects oversaw the restoration. Photo by Francis Dzikowski. 1 44415 AR2018__draft_color_rev.indd 2 4/30/19 5:27 PM From the President Dear Friend of the Conservancy: We celebrated our 45th anniversary in 2018. It’s an in-between number so we weren’t going to go all out with celebrations. Then we realized that there was no guarantee 45 years ago that we’d still be here—let alone have developed our range of programs and skills. So we decided that a little horn tooting was in order. Our founders had a vision: an organization that would focus on preservation and have technical skills that could actually help people fix their buildings. -

1 World Trade Center Llc, Et Al

1 WORLD TRADE CENTER LLC, ET AL. - DETERMINATION - 12/03/09 In the Matter of 1 WORLD TRADE CENTER LLC, ET AL. TAT(H)07-34 (CR), ET AL. - DETERMINATION NEW YORK CITY TAX APPEALS TRIBUNAL ADMINISTRATIVE LAW JUDGE DIVISION COMMERCIAL RENT TAX – THE LESSEES' PAYMENTS TO THE PORT AUTHORITY AFTER SEPTEMBER 11, 2001 DID NOT CONSTITUTE BASE RENT PAID FOR TAXABLE PREMISES BECAUSE THE LESSEES NO LONGER HAD THE RIGHT TO OCCUPY SPECIFIC SPACE AFTER THE GOVERNMENT TAKEOVER OF THE WORLD TRADE CENTER SITE ON SEPTEMBER 11, 2001. THUS, THE COMMERCIAL RENT TAX DOES NOT APPLY TO THOSE PAYMENTS. DECEMBER 3, 2009 NEW YORK CITY TAX APPEALS TRIBUNAL ADMINISTRATIVE LAW JUDGE DIVISION : In the Matter of the Petition : DETERMINATION : of : : TAT(H)07-34(CR), et al. 1 World Trade Center LLC, et al. : : Schwartz, A.L.J.: Petitioners, 1 World Trade Center LLC, 2 World Trade Center LLC, 4 World Trade Center LLC and 5 World Trade Center LLC (now known as 3 World Trade Center LLC) (“Petitioners” or the “Silverstein Lessees”) filed Petitions for Hearing with the New York City (“City”) Tax Appeals Tribunal (“Tribunal”) seeking redeterminations of deficiencies of City Commercial Rent Tax (“CRT”) under Chapter 7 of Title 11 of the City Administrative Code (“Code”) for the five tax years beginning June 1, 2001 and ending May 31, 2006 (“Tax Years”). A hearing was held and various documents were admitted into evidence. Petitioners were represented by Elliot Pisem, Esq. and Joseph Lipari, Esq. of Roberts & Holland LLP. The Commissioner of Finance (“Respondent” or “Commissioner”) was represented by Frances J. -

80Story 3 World Trade Center to Open After Years of Delays

9/11/2018 American Press | Monday, June 11, 2018 | A5 80story 3 World Trade Center to open after years of delays BY THE ASSOCIATED PRESS Associated Press In this June 22, 2016, file photo, workers guide a boom pouring concrete on the top floor of 3 World Trade Center in New York. Behind them is One World Trade Center. The new skyscraper opens Monday. NEW YORK — An 80story office building set to open this week at the World Trade Center will be the third completed skyscraper at the site where the twin towers stood. Monday’s ribboncutting for the 1,079foot 3 World Trade Center marks a http://digital.olivesoftware.com/Olive/APA/AmPress/Print.Article.aspx?mode=text&href=AMP%2F2018%2F06%2F11&id=Ar00503 1/2 9/11/2018 American Press | Monday, June 11, 2018 | A5 major step in the rebuilding of the site, stalled for years by disputes among government agencies, trade center developer Larry Silverstein, insurers and 9/11 victims’ family members who wanted the entire site to be preserved for eternity as a memorial. The new $2.7 billion building, designed by Pritzker Prizewinning architect Richard Rogers, has been the fifthtallest building in New York City since construction topped out in 2016. That designation seemed elusive in 2009 when the Port Authority of New York and New Jersey, which owns the trade center site and was battling with Silverstein over costs associated with rebuilding, sought to reduce 3 World Trade to a fourstory “stump.” After arbitration in the dispute between the developer and the property owner, construction started in 2010 but was halted at seven stories due to a lack of financing. -

Marcus Rosenberg & Diamond

MARCUS ROSENBERG & DIAMOND LLP 488 MADISON A VENUE NEW YORK, NEW YORK 10022 Telephone: (212) 755-7500 Telefax: (212) 755-8713 April 14, 2016 First Deputy Commissioner Technical Affairs Unit New York City Department of Buildings 280 Broadway, Fifth Floor New York, New York 10007 Re: I RCNY §101-15(b)(l) Community Challenge To March 30, 2016 Potential Zoning Challenge Determination As To Construction Permits Issued To Congregation Shearith Israel ("CSI") 8 West 70'h Street, New York, New York (the "Property") Block 1122, Lot 3 7 Department of Buildings ("DOB") Job No.: 121328919 (the "Project") Our Matter No.: 89628.003 Dear Commissioner: This letter, with the accompanying Zoning Challenge Form and attachments, constitutes a Zoning Challenge and a 1 RCNY §101-15(b)(l) appeal on behalf of Landmark West! other parties named in the June 18, 2015 Zoning Challenge that I filed, and other property owners and residents in the immediate vicinity of the Property, each of which directly and particularly will be affected by the Project. As will be explained, this I RCNY §101-15(b)(l) "Community Challenge" seeks review of a DOB March 30, 2016 letter (the "March 30 Letter" Exhibit A) addressed to the undersigned to the extent that the March 30 Letter might be deemed to be a determination of the Zoning Challenge filed on June 18, 2015. The March 30 Letter is so unclear and ambiguous that it is virtually impossible to determine whether, and what type of, response might be required. April 14, 2016 Page 2 To avoid any inference that a failure to respond to the March 30 Letter be deemed to evidence consent or waiver of previously asserted rights and claims, the response will provide material background facts resulting in the present appeal. -

Condominium Offering Plan Condominium

Part II of the Condominium Offering Plan of The New York Arts Building Condominium Exhibit 6(A)) Purchase Agreement PURCHASE AGREEMENT 3os EAST 6rsr sTREET GRoUP LLC Sponsor wirh Purchaser Unit Number THE NEW YORK ARTS BUILDING CONDOMINIUM 305 EAST 615T STREET NEW YORK. NEWYORK 10065 purchase agreement bb rev v2 nov 2.doc TABLE OF CONTENTS Section Page SCHEDULE A -............... PE,RMITTED ENCUMBRANCES SCHEDULE B _................ INSPECTION STATEMENT PAGE ii OF PURCHASE AGREEMENl purchase agreement bb tev v2 nov 2.doc PURCHASE AGREEMENT UNIT NUMBER THE NEW YORK ARTS BUILDING CONDOMINIUM 305 EAST 615T STREET NEW YORK, Nf,W YORK 10065 AGREEMENT. made as of between Sponsor and Purchaser (defined below). WITNESSETH: I. THEPLAN Purchaser acknowledges having received and read a copy of the Offering Plan for The New York Arts Building Condominium and all amendments thereto, if any, filed prior to the date hereof with the Deparffnent of Law of the State of New York (hereinafter, collectively, refened to as the "Plan") at least 3 business days prior to Purchaser's signing this Agreement. IfPruchaser has not received and read the Plan and all amendments thereto at least 3 business days prior to Purchaser's signing this Agreement, Purchaser shall have the right to rescind this Agreement, by sending written notice ofsuch rescission to Sponsor by certified or registered mail, retum receipt requested, or by personal delivery, in either case within 7 days from the date Purchaser delivers an executed Purchase Agreement together with the required Deposit to the Selling Agent. The Plan is incorporated herein by reference and made a part hereof with the same force and effect as if set forth at length. -

Chapter 11 INTELLITRAVEL MEDIA, INC. Case

12-14815-alg Doc 190 Filed 09/10/14 Entered 09/10/14 13:13:09 Main Document Pg 1 of 23 UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK In re: Chapter 11 INTELLITRAVEL MEDIA, INC. Case No. 12-14815 (ALG) d/b/a Budget Travel, Debtor. CERTIFICATE OF SERVICE STATE OF CALIFORNIA } } ss.: COUNTY OF LOS ANGELES } CATHERINE NOWNES-WHITAKER, being duly sworn, deposes and says: 1. I am employed by Rust Consulting/Omni Bankruptcy, located at 5955 DeSoto Avenue, Suite 100, Woodland Hills, CA 91367. I am over the age of eighteen years and am not a party to the above-captioned action. 2. On September 5, 2014, I caused to be served the: a. Order Approving (I) Disclosure Statement, (II) Form and Manner of Notices, (III) Form of Ballots, And (IV) Solicitation Materials and Procedures [Docket No. 184], (the “Order”), b. First Amended Plan of Liquidation of Intellitravel Media, Inc. D/B/A Budget Travel Pursuant to Chapter 11 of the Bankruptcy Code [Docket No. 185], (the “First Amended Plan”), c. First Amended Disclosure Statement for First Amended Plan of Liquidation of Intellitravel Media, Inc. D/B/A Budget Travel Pursuant to Chapter 11 of the Bankruptcy Code [Docket No. 187], (the “First Amended Disclosure Statement”), d. Letter from the Committee of Unsecured Creditors, (the “Committee Letter”), 1 e. Ballot for Accepting or Rejecting the Plan of Liquidation of Intellitravel Media Inc. D/B/A Budget Travel Pursuant to Chapter 11 of the Bankruptcy Code, (the “Ballot”), f. Form W-9 Request for Taxpayer Identification Number and Certification, (the “W-9 Form”), ____________________________________________________________________________________________________________________________________________________________ 1 A copy of the Committee Letter is attached hereto as Exhibit F.