The Remington Senior Apartments

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Atlanta Public Schools Middle Schools Zones 2008 Neighborhoods

City of Atlanta A t l a n t a P u b l i c S c h o o l s M i d d l e S c h o o l s Z o n e s 2 0 0 8 N e i g h b o r h o o d s A R K S R E C R R D N O E J W D E R D S Y E D T T NOR S T TH A D B K A WA T Y L D N P D L E W R W R E L L U M D A H D F FRANK A LIN RD C A R T H R P D O L V L C T H D R R A D E R Y E D H C Y ST LA T O R K Y B R Y T E T E H O T T R G L I N E C D D C A E R R N R R R O O O D K C F N I S T B D L IC L N T B R U T O Y W M R T D S R B A V Y S Y M S L Y Y W Y R I P H L N W R 0 Sandy Springs N D I Y W M N O R A C V L M U A I S W S K D Y O T L R L 0 K D S H L B A A O E R E R T E N RN RD I 4 RHO R DE T W A D EAST POW A Y O L ST A N P Y W E L IC L M T O P L L O P N N S A K I F C N E E L N D R T T S G D R S R DR O J S D T S H E A R R R D IG I E L E D R D AR T D AT T E EY CA T R A ROLWOOD LN I RIV R R L S D T L T H S P L GELO C R ST G A AN E A A R V W R PRING L A D N S S E H N D Chamblee R TWI ED E C M I R W DEN H D ST O A D T G N O S L L G S E R N T R U D M W T D E L A D B A A E O R D N R E D T D S L R O L R R H T LUB C D R PINE FOREST RD E R E T M C I C W R T PARAN PW A R G R R N E U A M P Y D O N O E L H A R W M Y L C H D HIT R W T E P D R D Y W B O S LE A U WO L AL T D K N V R E B E T R UC MEADOWBROOK DR RE U R T O IA C R SWIMS VA ALLEN M L PW E A C L LLEY DR N E I C M O R T G D N ARM SOMERSET DR TROY O CHASTAI W R L ON COC D DR U Y HRAN DR T F WES D A N N R R L D O E W HAR W ER D RIS V T B V V A N E VAL R L HSID D LEY GREEN DR A U L M T I C L A L R E O CT C E E E S O K E H N C C W N Y R ID IE K I T U S K C R T R H S G Y A A N ME A I O R D R N D M L U E R P E S L D S O L A Mt. -

Neighborhood Associations Are the Foundation of Atlanta's

Neighborhood Associations are the foundation of Atlanta’s Neighborhood Planning System. The Mayor, the City Council and various City agencies rely on Neighborhood Associations for comments and suggestions concerning the City’s growth and development. The Directory contains a listing of more than 150 neighborhood organizations along with contact information, meeting times and meeting locations. In addition, the Directory provides a listing of neighborhood organizations within each NPU and Council District. The information contained in this publication is generated from updates received from the Neighborhood Planning Units (NPUs) and neighborhood organizations. We encourage your assistance in maintaining accurate records. NPU - A 1 NPU - N 18 NPU - B 2 NPU - O 19 NPU - C 4 NPU - P 20 NPU - D 7 NPU - Q 21 NPU - E 8 NPU - R 22 NPU - F 10 NPU - S 23 NPU - G 11 NPU - T 24 NPU - H 12 NPU - V 26 NPU - I 13 NPU - W 27 NPU - J 14 NPU - X 28 NPU - K 15 NPU - Y 29 NPU - L 16 NPU - Z 30 NPU - M 17 W. Brinkley Dickerson, Jr. [email protected] 1st Tuesday, 7:00pm Atlanta Speech School City Council District 8 3160 Northside Pkwy Atlanta, GA 30327 Chastain Park Civic Association Tejas Patel / Jason White (704) 557-6328 [email protected] 4th Mondays Meeting Location Varies City Council District 8 Margaret Mitchell Civic Association Nikki Klein (404) 969-6622 [email protected] www.mmca-atlanta.org Meeting Date Varies Meeting Location Varies City Council District 8 Mount Paran Neighborhood Association Craig Viergever (404) 442-2843 [email protected] Meeting Date Varies Meeting Location Varies City Council District 8 Townsend Place Condominium Association, Inc. -

District 9 Newsletter

Fall 2015 DISTRICT 9 NEWSLETTER Council Member Felicia A. Moore Atlanta City Council District 9 Office (404) 330-6044 [email protected] 55 Trinity Avenue, Suite 2900 Atlanta, Georgia 30303 Fax (404) 658-7966 TABLE OF CONTENTS Page 2----District 9 Community Clean-ups Page 5----------------------For Your Information Page 3 --- Car Seat Give-A-Way/Jazz Day in the Park Insert -----------------------Resource Guide Page 4-----NPU Meeting Information Page 6----Letter from Council Member Moore DISTRICT 9 TACKLING CODE ENFORCEMENT ISSUES Council Member Moore is proud to announce the addition of Dustin R. Hillis, a District 9 & Riverside Neighborhood resident, to her staff. Dustin will be focusing on Code Enforcement, which the constituents have voiced as a top concern, & other quality of life issues. Felicia recruited Dustin after noting his success with getting properties complied in their Riverside Neighborhood. As a result of his effort, the open complaints now number around 10, which is down from a high 2167 Main Street-before 2167 Main Street-after of 60. Dustin was also appointed in fall 2014 to serve on the City of Atlanta’s Code Enforcement Commission. This body seeks to improve Code Enforcement in the City and is co-chaired by city (Continued on page 4.) NORTHWEST LIBRARY AT SCOTTS CROSSING GRAND OPENING The ribbon cutting ceremony for the new Northwest Library at Scotts Crossing took place on Thursday, July 9, which numerous residents of District 9 came out to celebrate the grand opening. Northwest Library, located at 2489 Perry Boulevard, is 25,000 square-ft wide and it includes a public art display, entitled Northwest Atlanta Globe that sits in front of the library. -

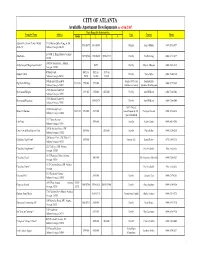

Available Apartment Developments As of 06/2007 Rent Range by Bedroom Size Property Name Address Type Contact Phone Studio 1 2 3 4

CITY OF ATLANTA Available Apartment Developments as of 06/2007 Rent Range by Bedroom Size Property Name Address Type Contact Phone Studio 1 2 3 4 Adamsville Senior Center (Misty 3712 Martin Luther King, Jr. Dr. $581-$675 $664-$800 Family Atrice Hardy (404) 696-0757 Amber)* Atlanta, Georgia 30310 2640 M. L. King Atlanta, Georgia Alta Pointe $675-$760 $825-$850 $900-$925 Family Tia Flanning (404) 691-2499 30310 180 Flat Shoals Ave., Atlanta, Amberwood Village Apartments* $490 Family Myron Johnson (404) 525-4130 Georgia 30316 49 Boulevard $692 or $822 or $939 or Auburn Glenn Family Turea Fulks (404) 584-1300 Atlanta, Georgia 30308 $890 $1240 $1340 500 Richard Allen Blvd. Senior @55+ yrs Tonya Miller Big Bethel Village $710.00 $750.00 $955.00 (404) 699-5665 Atlanta, Georgia 30331 (utilities included) Quianna Washington 1935 Allison Court, SW Brentwood Heights $399.00 $550.00 $650.00 Family Ann Williams (404) 768-6344 Atlanta, Georgia 30311 1935 Allison Court, SW Brentwood Meadows $550-$575 Family Ann Williams (404) 768-6344 Atlanta, Georgia 30311 100% Project 1050 Ponce de Leon Briarcliff Summit $669.00 $735.00 $815.00 based/Senior @ 62+ Carolyn Howard (404) 872-8214 Atlanta, Georgia 30306 yrs or Disabled 133 Trinity Avenue City Plaza $990.00 Family Kathy Harris (404) 681-4750 Atlanta, Georgia 30303 259 Richardson Street, SW City View at Rosa Burney Park $674.00 $800.00 Family Doris Kirby (404) 524-0286 Atlanta, Georgia 30312 220 Bowen Circle, SW, Unit 311, Columbia High Point* $574.00 Seniors 62+ Kandi Parker (678) 565-3716 Atlanta, Georgia -

2014 Urban Tree Canopy Study Here

Assessing Urban Tree Cover in the City of Atlanta: Phase 2 (Detecting Canopy Change 2008-2014) Prepared by: Center for Spatial Planning Analytics and Visualization (formerly known as the Center for Geographic Information Systems or CGIS) 760 Spring St Atlanta, GA 30332-0695 Office: 404-894-0127 Georgia Institute of Technology Investigators: Anthony Giarrusso, Associate Director (CSPAV), [email protected] Sponsor: City of Atlanta in the City of Atlanta 1 Acknowledgements Project Team: Principal Investigator: Anthony J. Giarrusso, Associate Director, Senior Research Scientist Center for Spatial Planning Analytics and Visualization ( Georgia Institute of Technology 760 Spring Street, Suite 230 Atlanta, GA 30308 Office: 404-894-0127 [email protected] Graduate Research Assistant Jeremy Nichols Center for Spatial Planning Analytics and Visualization Georgia Institute of Technology 760 Spring Street, Suite 230 Atlanta, GA 30308 The contents of this report reflect the views of the authors who are responsible for the facts and the accuracy of the data presented herein. The contents do not necessarily reflect the official views or policies of the City of Atlanta. This report does not constitute a standard, specification, or regulation. The project team would like to acknowledge and thank the following individuals for their assistance on this project. Kathryn A. Evans, Senior Administrative Analyst, Tree Conservation Commission, Department of Planning and Development, Arborist Division Assessing Urban Tree Cover in the City of Atlanta The 2014 Canopy -

Predicting Revitalization a Descriptive Narrative and Predictive Analysis of Neighborhood Revitalization in Atlanta, Georgia

Georgia Institute of Technology Predicting Revitalization A Descriptive Narrative and Predictive Analysis of Neighborhood Revitalization in Atlanta, Georgia Caroline E. Burnette Applied Research Paper Advisor: Dr. Subhrajit Guhathakurta May 4, 2017 Over the past two decades, revitalization has been transforming many of Atlanta’s unique neighborhoods and attracting new residents, businesses, and investments to the city’s urban core. This has resulted in positive and negative effects that are important to consider as redevelopment continues throughout Atlanta, especially in low‐income or disadvantaged communities. In order to mitigate the consequences of redevelopment while highlighting opportunities for growth and innovation, it is important to investigate how and why some Atlanta neighborhoods undergo revitalization earlier or at a more rapid pace than others. This paper seeks to identify significant physical, sociodemographic, and policy‐related factors that may catalyze or otherwise predict revitalization in certain communities, and then apply these indicators to Atlanta’s remaining neighborhoods to classify those with a greater potential to revitalize in the coming years. To achieve this, a time‐lagged probit model was developed to measure hypothesized revitalization indicators within each of Atlanta’s Neighborhood Statistical Areas across multiple time periods. This model suggests that revitalization often occurs in Atlanta neighborhoods that overlap with designated historic districts, those that are within walking distance of transit stations and the Beltline, those that are adjacent to other revitalized neighborhoods, those with lower percentages of renter‐occupied housing units, and those with greater proportions of jobs in creative, higher education, and professional and technical service industries. Using these results, the model identified other neighborhoods that contain a combination of factors which make them susceptible to revitalization. -

NPU POLICIES NPU-A Policies

NPU POLICIES NPU-A Policies A-1: Preserve the single-family character of NPU ‘A’, including the following neighborhoods: Paces, Mount Paran- Northside, Chastain Park, Tuxedo Park, Moores Mill, Margaret Mitchell, Randall Mill, and West Paces Ferry- Northside. Maintain the historic and residential character of West Paces Ferry Road. A-2: Maintain the boundaries of the I-75/West Paces Ferry commercial node. Incorporate pedestrian amenities and encourage street-level retail uses in order to maximize pedestrian activity. Treat low- and medium- density residential areas as buffers for surrounding single-family neighborhoods. Maintain the existing scale of the structures in the commercial district. A-3: Preserve the single family residential character of the neighborhoods surrounding Chastain Park, a unique single-family residential and historic area, as well as the only significant park and green space in North -At lanta. Maintain the boundaries of the Roswell Road commercial area as a medium density corridor. Maintain the maximum allowable density of the Chastain Park Civic Association neighborhoods at the current R-3 zoning. Recognize the historic Sardis Church and the Georgia Power substation as the established buffers between Roswell Road commercial area and the single-family residential areas surrounding Chastain Park. Preserve the current residential zoning of all gateway streets from Roswell Road to Chastain Park, including West Wieuca, Interlochen, Laurel Forest, Le Brun, and Powers Ferry Roads. A-4: Limit the development of office-institutional uses to the northwest quadrant of the I-75/Mount Paran Road/I-75 Interchange and prevent the development of additional commercial use property in this area. -

Task 2 Memo Appendix B: Driving Tour Summary

SCAPE GRESHAM SMITH BIOHABITATS GOOD THINKING ATLANTA NEW SOUTH ASSOCIATES DR. NA'TAKI OSBORNE JELKS DR. RICHARD MILLIGAN EDWARDS-PITMAN CHATTAHOOCHEE RIVER GREENWAY STUDY FOR THE CHATTAHOOCHEE RIVERLANDS TASK 2 MEMO APPENDIX B: DRIVING TOUR SUMMARY SUBMITTED ON 05/03/2019 TABLE OF CONTENTS DRIVING TOUR SUMMARY ........................................................................................................................................................................................................................................................................................................................................................ 4 DAY 1........................................................................................................................................................................................................................................................................................................................................................................................... 6 : ’ , + 12 DAY 2 .........................................................................................................................................................................................................................................................................................................................................................................................14 # # # # 28 DAY 3.........................................................................................................................................................................................................................................................................................................................................................................................30 -

Assessing Urban Tree Canopy in the City of Atlanta; a Baseline Canopy Study

Final Report Assessing Urban Tree Canopy in the City of Atlanta; A Baseline Canopy Study City of Atlanta Department of Planning and Community Development Arborist Division Spring 2014 Prepared by: Tony Giarrusso, Associate Director of the Center for GIS, Georgia Institute of Technology Sarah Smith, Research Scientist II, Center for Quality Growth and Regional Development, Georgia Institute of Technology Acknowledgements Project Team: Principal Investigator: Anthony J. Giarrusso, Associate Director, Senior Research Scientist Center for Geographic Information Systems (CGIS) Georgia Institute of Technology 760 Spring Street, Suite 230 Atlanta, GA 30308 Office: 404-894-0127 [email protected] Co-Principal Investigator: Sarah M. Smith, Research Scientist II Center for Quality Growth & Regional Development (CQGRD) 760 Spring Street, Suite 213 Atlanta, GA 30308 Office: 404-385-5133 [email protected] Research Assistants: Amy Atz Gillam Campbell Alexandra Frackelton Anna Harkness Peter Hylton Kait Morano The contents of this report reflect the views of the authors who are responsible for the facts and the accuracy of the data presented herein. The contents do not necessarily reflect the official views or policies of the City of Atlanta. This report does not constitute a standard, specification, or regulation. The project team would like to acknowledge and thank the following individuals for their assistance on this project. Kathryn A. Evans, Senior Administrative Analyst, Tree Conservation Commission, Department of Planning and Development, Arborist Division Chuck Schultz, Principle Planner, GIS, City of Atlanta Jim Kozak, Davey Resource Group, a Division of the Davey Tree Expert Company - Davey Trees Assessing Urban Tree Cover in the City of Atlanta A Baseline Canopy Study 2 Table of Contents Table of Contents Table of Contents ......................................................................................................................................... -

About Proctor Creek Newsletter

Stories and upcoming events from the Proctor Creek watershed in northwest Atlanta Testing the Soil for Green Infrastructure Earlier this month, a team of EPA hydrologists and soil scientists visited Proctor Creek as part of the national Urban Soils Assessment, a research initiative aimed at informing green infrastructure development. The team collected soil cores at 13 locations in the watershed and used specialized tools to measure how water moves into and through the soil. Little is known about urban soils, and the goal of the research is to characterize urban soils and help city planners design green infrastructure to address environmental challenges related to stormwater. While they were in town, the researchers also visited a 4th grade class at M. Agnes Jones Elementary, a group of 2nd graders from Woodson Elementary, a group of Clark Atlanta students, and Greening Youth Foundation’s Atlanta Youth Corps to discuss hydrology and soils. In total, the research team has collected samples and tested soil hydrology in 11 cities around the country and plans to use the information they gather to: (1) provide soil management options that support successful use of parks and green spaces for green infrastructure; (2) assist city planners in creating healthier, more sustainable communities; and (3) offer guidance on using green infrastructure to visually enhance city landscapes and improve quality of life for city residents and visitors. For more information about the Urban Soils Assessment click here. A Resident Forum for Engagement in Proctor Creek On the first Friday of every month, residents from northwest Atlanta communities surrounding Proctor Creek come together to discuss the watershed. -

Flyer for the Proctor Creek Community Showcase

PROCTOR CREEK COMMUNITY SHOWCASE @ GROVE PARK SATURDAY, SEPTEMBER 26, 2015 PROTECT WATERS. CHANGE LIVES. Urban Revitalization as a Collaborative FUN FOR THE WHOLE FAMILY! Health Screenings + SATURDAY, SEPTEMBER 26, 2015 10AM – 4PM GROVE PARK Nutritious CONTACT TODAY! F d & For more information: Drinks Al Bartell, Facilitator (470) 222-5855 [email protected] COMMUNITY PROTECT WATERS. SHOWCASE @ CHANGE LIVES. GROVE PARK SATURDAY, SEPTEMBER 26, 2015 Proctor Creek Fact Sheet ABOUT COMMUNITY SHOWCASE: A collaborative of community and government partners has organized a showcase event for demonstrations, workshops, soil and water testing, information sharing regarding the many efforts going on in the Proctor Creek watershed, plus healthy food and drinks. You are invited to join us as we gather local knowledge about what is working, what is not, what are the possibilities and what services are available to the communities, in partnership with numerous in-residents of the Proctor Creek Watershed Basin 38 11 Neighborhood Planning Units, neighborhoods, nonprofits, academic 38 Neighborhood Associations and 15 Small Business Corridors and faith-based institutions, small interconnected by 300 tributaries and 1 main spine make up the businesses, plus government, private Proctor Creek Watershed Basin in Northwest Atlanta foundations and corporations are Almond Park Downtown Mozley Park supporting this community showcase to focus on the protection of Human Ashview Heights English Avenue Penelope Neighbors Health and the Environment in Proctor -

(Early) Voting Locations, Dates & Times

ADVANCE (EARLY) VOTING LOCATIONS, DATES & TIMES CITY OF ATLANTA NOVEMBER 7, 2017 GENERAL ELECTION City of Atlanta Voters (in Fulton or Dekalb County) May Vote at Any Location Shown Below Monday thru Friday October 16 -November 3, 2017 8:30 am - 5:00 pm Including two full weekends at all locations Saturday October 21 & 28 2017 Sunday October 22 & 29 2017 OPERATING LOCATION ADDRESS DATES HOURS 130 Peachtree Street Fulton County Monday – Friday Suite 2186 8:30 AM – 5:00 PM Government Center October 16 – November 3 Atlanta, GA 30303 5600 Stonewall Tell Road Fulton County Monday – Friday Room 108 8:30 AM – 5:00 PM South Fulton Annex October 16 – November 3 College Park, GA 30349 Fulton County 7741 Roswell Road, NE Monday – Friday North Fulton Annex Suite 224 8:30 AM – 5:00 PM October 16 – November 3 Sandy Springs, GA 30350 City of Atlanta 3201 Martin Luther King Jr. Dr., Monday – Friday Adamsville 8:30 AM – 5:00 PM SW Atlanta, GA 30311 October 28 – November 3 Recreation Center City of Atlanta 1530 Woodbine Avenue, SE Monday – Friday Wesley Coan 8:30 AM – 5:00 PM Atlanta, GA 30317 October 28 – November 3 Recreation Center City of Atlanta 308 Peachtree Hills Avenue, NE Monday – Friday Peachtree Hills 8:30 AM – 5:00 PM Atlanta, GA 30305 October 28 – November 3 Recreation Center Alpharetta Branch 10 Park Plaza Monday- Friday 8:30 AM – 5:00 PM Library Alpharetta Ga. 30009 October 16 – November 3 Buckhead Branch 269 Buckhead Avenue Monday – Friday 8:30 AM -5:00 PM Library Atlanta Georgia 30305 October 16 -November 3 Johns Creek 8100 Holcomb Bridge Road Monday – Friday Environmental 8:30 AM – 5:00 PM Alpharetta Georgia 30022 October 16 – November 3 Campus Southeast Atlanta 1463 Pryor Road Monday – Friday 8:30 AM- 5:00 PM Branch Library Atlanta Georgia 30315 October 16 – November 3 Northwest Branch at 2489 Perry Boulevard N.W.