2019 State of Downtown Pittsburgh

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

In Case You Need a Few More Examples of Tonya Payne on “The Record”

In case you need a few more examples of Tonya Payne on “The Record”... Councilwoman tables plans to exempt colleges from rental unit registration Thursday, February 12, 2009 By Rich Lord, Pittsburgh Post-Gazette Councilwoman Tonya Payne, who proposed the exemption two weeks ago, said the city must consider "the consequences that might happen if an exemption is granted here or anywhere else." And by month's end, at least two property owners' groups expect to decide whether to file suit to halt parts of Mayor Luke Ravenstahl's effort to register rental properties and, where necessary, fine landlords for tenant behavior. Williams family helping redevelop Uptown In past at odds with leaders over vast real estate holdings Sunday, February 01, 2009 By Mark Belko, Pittsburgh Post-Gazette City Councilwoman Tonya Payne, who now represents Uptown and who received campaign contributions from the owners of Williams Real Estate in 2005, spoke highly of Sal Williams. "He's definitely good for Uptown and he's always been," she said Hill District pastor who fought hockey arena retiring Sunday, January 25, 2009 By Ann Rodgers, Pittsburgh Post-Gazette That pitted him against Councilwoman Tonya Payne, who in 2005 had defeated his friend, Mr. Udin. She saw the casino as a good deal. But, after the casino plan failed, she believes Dr. Monroe's group made unrealistic demands on the group that emerged to build an arena. His group wanted $10 million to revitalize the Hill. Ms. Payne's group had a lead role in negotiations that yielded $3 million. "I'm still convinced that the community did not get a good deal," Dr. -

URA 2014-2016 Report

2014-2016 Report The Urban Redevelopment Authority is here for Pittsburgh. Washington’s Landing Pedestrian Bridge URA completed 1999 Photo: Rob Larson In the 412. In the neighborhoods. In the businesses that keep Pittsburgh strong. In the jobs that keep people thriving. Here is investment. Here is technology. Here is leadership. Over the past few years, the We danced in Allentown, sipped coffee OUR BOARD Urban Redevelopment Authority in Homewood, wrote code with children of Pittsburgh continued leading in Oakland, and shot clay hockey pucks transformative growth in at a senior housing site in Carrick. We cut neighborhoods throughout the ribbon to expand manufacturing in the City of Pittsburgh. Under the West End, hiked what will be Pittsburgh’s leadership and vision of Mayor largest park in Hays, listened to poetry in William Peduto, the URA Central Northside, and waited no longer implemented many new initiatives than one minute for a bus in East Liberty’s aimed at creating the “Next Pittsburgh,” – new transit center. These are but a small one that’s more affordable, inclusive, sustainable, handful of the activities and projects competitive, and works for all. the Urban Redevelopment Authority of The Honorable The Honorable Pittsburgh undertook in 2014-2016. Ed Gainey Jim Ferlo Affordable and mixed-income housing remains a top priority so that Pittsburgh can truly become a We have weathered 15 years of steady Vice Chair Treasurer most livable city for all residents. Long-struggling declines in Federal and State resources neighborhoods saw the financial assistance and which are ever so critical to neighborhood resources needed to strengthen and grow. -

Directions to West Penn Hospital 4800 Friendship Avenue, Pittsburgh, PA 15224

Allegheny Health Network Directions to West Penn Hospital 4800 Friendship Avenue, Pittsburgh, PA 15224 From the North: From the South: Follow I-279 South to Route 28 North. Cross the 40th Follow Route 51 North to West Liberty Ave. Turn right onto Street Bridge. Continue on 40th Street to Liberty Ave. Turn West Liberty Ave. and continue through the Liberty Tunnel left onto Liberty Ave. West Penn Hospital is located at the and across the Liberty Bridge. Follow I-579 North to the intersection of Liberty and South Millvale Avenues. Bigelow Blvd. exit (Rte. 380). Follow Bigelow Blvd. and take the Liberty Ave./Bloomfield exit, crossing the Bloomfield From the Northeast: Bridge. Bear right at the end of bridge onto Liberty Ave. Follow Route 28 South to the 40th Street Bridge. Continue West Penn Hospital is located at the intersection of Liberty on 40th Street to Liberty Ave. Turn left onto Liberty Ave. and South Millvale Avenues. West Penn Hospital is located at the intersection of Liberty and South Millvale Avenues. From the West and Pittsburgh International Airport: From the East: Follow I-376 East through the Fort Pitt Tunnel and across Follow I-376 West to Wilkinsburg exit. Follow Ardmore the Fort Pitt Bridge. Take Liberty Ave. exit. Follow Liberty Blvd. (Rte. 8) to Penn Ave. Turn left onto Fifth Ave. and Ave. through Pittsburgh to Bloomfield. West Penn Hospital follow to South Aiken Ave. Turn right onto South Aiken and is located at the intersection of Liberty and South Millvale follow to Baum Blvd. Stay straight onto Liberty Ave. -

Frederick C. Leech

Frederick C. Leech issuance of equity securities in connection with the acquisition of multi-family assets in select U.S. markets utilizing general solicitation private placement exemptions authorized under the JOBS Act. Fred also regularly represents SEC and state registered investment advisers in regulatory, compliance and acquisition matters. Fred is an active firm leader. He currently is Chair of Leech Tishman’s Corporate Practice Group and has served on the firm’s Management Committee. Prior to joining Leech Tishman, Fred was Partner with Reed Smith, and served for 15 years as Practice Leader of Reed Smith’s Financial Services and Investment Management Practice Groups. Academics J.D., Northeastern University School of Law B.A., with high honors, Phi Beta Kappa, University of Michigan PARTNER Admissions [email protected] Pennsylvania, Supreme Court of Pennsylvania U.S. District Court, Western District of Pennsylvania Experience – Reed Smith 412.261.1600 Recent Speaking Engagements 525 WILLIAM PENN PLACE “Fifty Shades of Green – Capital Formation Opportunities PITTSBURGH, PA 15219 under the JOBS Act,” MIT Enterprise Forum-Pittsburgh, Nov. 15, 2016 Fred Leech is a Partner with Leech Tishman’s Corporate Practice Group, and is also a member of the LaunchPad “Personal Securities Trading, Ethics and Compliance,” legal group. Fred focuses on providing legal advisory The Knowledge Group, Feb. 26, 2016 services to business clients on acquisition transactions, securities matters and financings. “The JOBS Act and Rule 506(c) – Opportunities -

1 FINAL REPORT-NORTHSIDE PITTSBURGH-Bob Carlin

1 FINAL REPORT-NORTHSIDE PITTSBURGH-Bob Carlin-submitted November 5, 1993 TABLE OF CONTENTS Page I Fieldwork Methodology 3 II Prior Research Resources 5 III Allegheny Town in General 5 A. Prologue: "Allegheny is a Delaware Indian word meaning Fair Water" B. Geography 1. Neighborhood Boundaries: Past and Present C. Settlement Patterns: Industrial and Cultural History D. The Present E. Religion F. Co mmunity Centers IV Troy Hill 10 A. Industrial and Cultural History B. The Present C. Ethnicity 1. German a. The Fichters 2. Czech/Bohemian D. Community Celebrations V Spring Garden/The Flats 14 A. Industrial and Cultural History B. The Present C. Ethnicity VI Spring Hill/City View 16 A. Industrial and Cultural History B. The Present C. Ethnicity 1. German D. Community Celebrations VII East Allegheny 18 A. Industrial and Cultural History B. The Present C. Ethnicity 1. German a. Churches b. Teutonia Maennerchor 2. African Americans D. Community Celebrations E. Church Consolidation VIII North Shore 24 A. Industrial and Cultural History B. The Present C. Community Center: Heinz House D. Ethnicity 1. Swiss-German 2. Croatian a. St. Nicholas Croatian Roman Catholic Church b. Javor and the Croatian Fraternals 3. Polish IX Allegheny Center 31 2 A. Industrial and Cultural History B. The Present C. Community Center: Farmers' Market D. Ethnicity 1. Greek a. Grecian Festival/Holy Trinity Church b. Gus and Yia Yia's X Central Northside/Mexican War Streets 35 A. Industrial and Cultural History B. The Present C. Ethnicity 1. African Americans: Wilson's Bar BQ D. Community Celebrations XI Allegheny West 36 A. -

Luke Ravenstahl Mayor Noor Ismail, AICP Director ACKNOWLEDGEMENTS

Luke Ravenstahl Mayor Noor Ismail, AICP Director ACKNOWLEDGEMENTS The South Metro Area Revitalization through Transit / Transit Revitalization Investment District (SMART TRID) Corridor Planning Study was generously funded by the State of Pennsylvania Department of Community and Economic Development, Pittsburgh Partnership for Neighborhood Development, Mount Washington Community Development Corporation, City of Pittsburgh, and Chelsa Wagner – Pennsylvania State House of Representatives – District 22. Special thanks to the interest, input, and commitment made to this effort by the following political representatives and community organizations: Mayor Luke Ravenstahl State Representative Chelsa Wagner City of Pittsburgh Councilwoman Natalia Rudiak City of Pittsburgh Councilman Bruce Kraus Director of City Planning Noor Ismail, AICP Mount Washington Community Development Corporation Beltzhoover Neighborhood Council Allentown Community Development Corporation Community Leaders United for Beechview (CLUB) TRID Planning Team Interface Studio LLC Scott Page, Principal Mindy Watts, Associate, AICP, PP Stacey Chen, Urban Designer & Planner Ashley Di Caro, Urban & Landscape Designer Real Estate Strategies, Inc. Meg Sowell Beth Beckett Sam Schwartz Engineering Mark de la Vergne, Associate Community Technical Assistance Center Karen Brean, Director Marjorie Howard April Clisura Sci-Tek Consultants, Inc. Charles Toran, President Jamille Ford, Manager Kevin Clark, P.E. CORRIDOR STUDY Steering Committee Members Joy Abbott, Assistant Director, City of -

2 Mount Royal

2 MOUNT ROYAL P13 MOUNT ROYAL FLYER SERVICE NOTES MONDAY THROUGH FRIDAY SERVICE MONDAY To Millvale - Etna - Shaler - Hampton - Route P13 does not operate on Saturdays, To Downtown Pittsburgh THROUGH McCandless Sundays, New Year's Day, Memorial Day, FRIDAY Independence Day, Labor Day, Thanksgiving SERVICE or Christmas. To Downtown Pittsburgh North Hills Village Target Ross Rd McKnight past Ross Park Mall Dr Ross Park Mall (at shelter) Hampton Ferguson Rd at Blvd Royal Mt at Etna Butler St opp. Freeport St Millvale North Ave at Grant Ave East Deutschtown E Ohio St past ChestnutSt Downtown St 9th at Penn Ave Downtown St 9th at Penn Ave East Deutschtown E Ohio St St Heinz at Millvale North Ave at Lincoln Ave Etna Butler St at Freeport St Hampton Ferguson Rd past Mt Royal Blvd Ross Rd McKnight opp. Ross Park Mall Dr Ross Park Mall (at shelter) Ross Rd McKnight at North Hills Village North Hills Village Target 3:53 4:00 .... 4:15 4:27 4:37 4:44 4:50 4:50 4:58 5:06 5:14 5:25 5:38 .... 5:41 5:44 4:18 4:24 .... 4:40 4:53 5:04 5:13 5:20 5:20 5:28 5:36 5:44 5:55 6:08 .... 6:11 6:14 4:48 4:54 .... 5:10 5:23 5:34 5:43 5:50 5:50 5:58 6:06 6:14 6:25 6:38 .... 6:45 6:48 5:05 5:12 .... 5:27 5:41 5:52 6:03 6:10 6:10 6:19 6:29 6:37 6:50 ... -

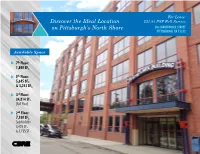

Discover the Ideal Location on Pittsburgh's North Shore

For Lease: Discover the Ideal Location $21.95 PSF Full Service on Pittsburgh’s North Shore 503 MARTINDALE STREET PITTSBURGH, PA 15212 Available Space 7th Floor: 1,800 SF+ 5th Floor: 5,345 SF+ & 3,243 SF+ 3rd Floor: 34,814 SF+ (Full Floor) 2nd Floor: 7,180 SF+ Subdividable 3,425 SF+ & 3,755 SF+ 7th Floor: 1,800 SF+ Prime Location 5th Floor: 5,345 SF+ 3,243 SF+ Located on Martindale Street between PNC Park and Heinz field, the D. L. Clark Building is just steps away from many new restaurants, nighttime activities, 3rd Floor: and ongoing North Shore Full Floor: 34,814 SF+ projects and redevelopments. The D.L. Clark Building has 2nd Floor: excellent access to downtown 7,180 SF+ (Subdividable) Pittsburgh and all major arteries. Building Specifics Historic Building on the North Shore Building Size: 197,000 SF+ Six Floors: 32,540 SF+ to 34,084 SF each with a 5,000 SF+ Penthouse Great views of Pittsburgh, the North Shore & North Side and Allegheny Commons Park 2,000 Parking Spaces Available Surrounding the Building at Monthly Rates Attractive Interiors Fire Protection: Security guards provide tenants’ employees with escort Building Specifications The Building is completely protected by modern fire suppression, service to the designated parking areas upon request. The emergency lighting and fire alarm systems. Building is 100% building has twenty-nine (29) security cameras mounted sprinklered by an overhead wet system. for viewing at the guard’s desk. The elevators have a key- lock system after 6 p.m. The D. L. Clark Office Building offers the finest quality equipment and state-of-the-art building Windows: Amenities: systems. -

Performance Audit

Performance Audit Citizen Police Review Board Report by the Office of City Controller MICHAEL E. LAMB CITY CONTROLLER Rachael Heisler, Deputy Controller Gloria Novak, Performance Audit Manager Bette Ann Puharic, Performance Audit Assistant Manager Mark Ptak, Research Assistant May 2021 TABLE OF CONTENTS Executive Summary ................................................................................................................... i-iii Introduction and Overview ...........................................................................................................1 History and Review of Independent Police Oversight in the U.S ............................................ 1 Establishment of Pittsburgh’s Citizen Police Review Board ................................................... 2 Subpoena Power ................................................................................................................. 2 Objectives........................................................................................................................................3 Scope and Methodology .................................................................................................................3 FINDINGS AND RECOMMENDATIONS Police Review Boards in the U.S. ..................................................................................................5 Key Characteristics ..............................................................................................................5 Potential Key Strengths........................................................................................................5 -

The Frick Building

THE FRICK BUILDING 437 GRANT STREET | PITTSBURGH, PA HISTORIC BUILDING. PRIME LOCATION. THE FRICK BUILDING Located on Grant Street across from the Allegheny County court house and adjacent to Pittsburgh City Hall, the Frick Building is just steps away from many new restaurants & ongoing projects and city redevelopments. The Frick Building is home to many creative and technology based fi rms and is conveniently located next to the Bike Pittsburgh bike rental station and Zipcar, located directly outside the building. RESTAURANT POTENTIAL AT THE HISTORIC FRICK BUILDING Grant Street is becoming the city’s newest restaurant district with The Commoner (existing), Red The Steak- house, Eddie V’s, Union Standard and many more coming soon Exciting restaurants have signed on at the Union Trust Building redevelopment, Macy’s redevelopment, Oliver Building hotel conversion, 350 Oliver development and the new Tower Two-Sixty/The Gardens Elevated location provides sweeping views of Grant Street and Fifth Avenue The two levels are ideal for creating a main dining room and private dining facilities Antique elevator, elegant marble entry and ornate crown molding provide the perfect opportunity to create a standout restaurant in the “Foodie” city the mezzanine AT THE HISTORIC FRICK BUILDING 7,073 SF available within a unique and elegant mezzanine space High, 21+ foot ceilings Multiple grand entrances via marble staircases Dramatic crown molding and trace ceilings Large windows, allowing for plenty of natural light Additional space available on 2nd floor above, up to 14,000 SF contiguous space Direct access from Grant Street the mezzanine AT THE HISTORIC FRICK BUILDING MEZZANINE OVERALL the mezzanine AT THE HISTORIC FRICK BUILDING MEZZANINE AVAILABLE the details AT THE HISTORIC FRICK BUILDING # BIGGER. -

893780-SHH 2015 Annual Report.Indd

ANNUAL REPORT 2015 “It is the small things children’s wellbeing and safety while they may be at work. The rural setting of our residential camp uniquely offers opportunities that matter the most.” to be continuously active and to learn about environmental stewardship. The positive influence of friendships built during Staff and volunteers typically these experiences can have a say this when asked what helps lifelong impact. our members have fun and learn new things when they Empowering all youth, especially those who need us most, is a come to Sarah Heinz House BIG mission. But we know it is achievable by doing many small each day. things exceedingly well. The small things which cause them to joyfully come through our door each day to be part of activities It can start with a simple hug to that improve their fitness and health, deepen learning and build say hello, a spontaneous 30 second chat in a hallway to convey new friendships. how special a child really is, or the longer discussion at the table during the nightly dinner to simply listen to what’s on their Sarah Heinz House is extremely proud of our team of innovative minds. Encouragement and recognition are also given during employees, amazing volunteers and seasonal staff whose individual and group projects or fitness activities so our kids find collective talents and care for our youth resulted in over 100 a way to push themselves to new levels of achievement. different after school programs and 8 weeks of summer camp for 1,800 youth in 2015. -

Guiding Change in the Strip

Guiding Change in the Strip Capstone Seminar in Economic Development, Policy and Planning Graduate School of Public and International Affairs (GSPIA) University of Pittsburgh December 2002 GUIDING CHANGE IN THE STRIP University of Pittsburgh Graduate School of Public and International Affairs Capstone Seminar Fall 2002 Contributing Authors: Trey Barbour Sherri Barrier Carter Bova Michael Carrigan Renee Cox Jeremy Fine Lindsay Green Jessica Hatherill Kelly Hoffman Starry Kennedy Deb Langer Beth McCall Beth McDowell Jamie Van Epps Instructor: Professor Sabina Deitrick i ii MAJOR FINDINGS This report highlights the ongoing nature of the economic, social and environmental issues in the Strip District and presents specific recommendations for Neighbors in the Strip (NITS) and policy makers to alleviate problems hindering community development. By offering a multitude of options for decision-makers, the report can serve as a tool for guiding change in the Strip District. Following is a summary of the major findings presented in Guiding Change in the Strip: • The Strip has a small residential population. As of 2000, the population was on 266 residents. Of these residents, there is a significant income gap: There are no residents earning between $25,000 and $35,000 annually. In other words, there are a limited amount of middle-income residents. Furthermore, nearly three-quarters of the 58 families living in the Strip earned less than $25,000 in 1999. These figures represent a segment of the residential population with limited voice in the development of the Strip. There is an opportunity for NITS, in collaboration with the City of Pittsburgh, to increase the presence of these residents in the future of the Strip.