CFA Society Sydney Abercrombie & Co

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PIPE Networks Prospectus 2006 Annual Report 2005

PIPE Networks Prospectus 2006 ANNUAL REPORT 2005 PIPE Networks PIPE Networks Prospectus 2006 FOR AN OFFER OF 4,392,857 ORDINARY SHARES BY WAY OF A RENOUNCEABLE RIGHTS ISSUE AT AN APPLICATION PRICE OF $1.50 EACH TO RAISE $6,589,286 FOR THE ISSUE OF UP TO 200,000 OPTIONS IN ACCORDANCE WITH THE COMPANY EMPLOYEE SHARE OPTION PLAN PIPE Networks Limited ABN 21 099 104 122 Underwriter and Lead Manager ABN AMRO Morgans Corporate Limited ABN 32 010 539 607 Broker to the Offer ABN AMRO Morgans Limited ABN 49 010 669 726 TaBLE OF CONTENTS Important Information 5 Key Investment Highlights 6 Key Rights Issue Statistics 7 Chairman’s Letter 8 Details of Offers 9 Company Overview 13 Financial Information 18 Investigating Accountant’s Report 22 Directors And Officers 3 Risk Factors 5 Additional Information 9 Definitions 56 “We succeed where others fail because we continue to ignore the limitations of technology and create new and innovative solutions to the problems that stand in our way.” Bevan Slattery CEO PAGE PROSPECTUS 2005/2006 IMANNUPORTAANTL REPO INFORRMAT 2005TION This Prospectus is dated 4 January 2006. A copy of this Prospectus has been Privacy lodged with ASIC. ASIC takes no responsibility for the contents of this Prospectus. If you make an Application, you will be required to provide personal information to the Company and the Share Registrar. The Company and the Share Registrar No Shares or Options will be issued or allotted on the basis of this Prospectus will collect, hold and use your personal information to assess your Application, later than 13 months after the date of this Prospectus. -

State of Mobile Networks: Australia (November 2018)

State of Mobile Networks: Australia (November 2018) Australia's level of 4G access and its mobile broadband speeds continue to climb steadily upwards. In our fourth examination of the country's mobile market, we found a new leader in both our 4G speed and availability metrics. Analyzing more than 425 million measurements, OpenSignal parsed the 3G and 4G metrics of Australia's three biggest operators Optus, Telstra and Vodafone. Report Facts 425,811,023 31,735 Jul 1 - Sep Australia Measurements Test Devices 28, 2018 Report Sample Period Location Highlights Telstra swings into the lead in our download Optus's 4G availability tops 90% speed metrics Optus's 4G availability score increased by 2 percentage points in the A sizable bump in Telstra's 4G download speed results propelled last six months, which allowed it to reach two milestones. It became the the operator to the top of our 4G download speed and overall first Australian operator in our measurements to pass the 90% threshold download speed rankings. Telstra also became the first in LTE availability, and it pulled ahead of Vodafone to become the sole Australian operator to cross the 40 Mbps barrier in our 4G winner of our 4G availability award. download analysis. Vodafone wins our 4G latency award, but Telstra maintains its commanding lead in 4G Optus is hot on its heels upload Vodafone maintained its impressive 4G latency score at 30 While the 4G download speed race is close among the three operators milliseconds for the second report in row, holding onto its award in Australia, there's not much of a contest in 4G upload speed. -

Separation of Telstra: Economic Considerations, International Experience

WIK-Consult Report Study for the Competitive Carriers‟ Coalition Separation of Telstra: Economic considerations, international experience Authors: J. Scott Marcus Dr. Christian Wernick Kenneth R. Carter WIK-Consult GmbH Rhöndorfer Str. 68 53604 Bad Honnef Germany Bad Honnef, 2 June 2009 Functional Separation of Telstra I Contents 1 Introduction 1 2 Economic and policy background on various forms of separation 4 3 Case studies on different separation regimes 8 3.1 The Establishment of Openreach in the UK 8 3.2 Functional separation in the context of the European Framework for Electronic Communication 12 3.3 Experiences in the U.S. 15 3.3.1 The Computer Inquiries 15 3.3.2 Separate affiliate requirements under Section 272 17 3.3.3 Cellular separation 18 3.3.4 Observations 20 4 Concentration and cross-ownership in the Australian marketplace 21 4.1 Characteristics of the Australian telecommunications market 22 4.2 Cross-ownership of fixed, mobile, and cable television networks 27 4.3 The dominant position of Telstra on the Australian market 28 5 An assessment of Australian market and regulatory characteristics based on Three Criteria Test 32 5.1 High barriers to entry 33 5.2 Likely persistence of those barriers 35 5.3 Inability of other procompetitive instruments to address the likely harm 38 5.4 Conclusion 38 6 The way forward 39 6.1 Regulation or separation? 40 6.2 Structural separation, or functional separation? 42 6.3 What kind of functional separation? 44 6.3.1 Overview of the functional separation 44 6.3.2 What services and assets should be assigned to the separated entity? 47 6.3.3 How should the separation be implemented? 49 Bibliography 52 II Functional Separation of Telstra Recommendations Recommendation 1. -

Telstra Corporation Limited (‘Telstra’) Welcomes the Opportunity to Make a Submission to the USPTO on Prior User Rights

Introduction Telstra Corporation Limited (‘Telstra’) welcomes the opportunity to make a submission to the USPTO on prior user rights. As Australia’s leading telecommunications and information services company, Telstra provides customers with a truly integrated experience across fixed line, mobiles, broadband, information, transaction, search and pay TV. Telstra BigPond is Australia’s leading Internet Service Provider offering retail internet access nationally, along with a range of online and mobile content and value added services One of our major strengths in providing integrated telecommunications services is our vast geographical coverage through both our fixed and mobile network infrastructure. This network and systems infrastructure underpins the carriage and termination of the majority of Australia's domestic and international voice and data telephony traffic. Telstra has an extensive intellectual property portfolio, including trade mark and patent rights in Australian and overseas. Telstra is also a licensor and a licensee of intellectual property, including a licensee of online and digital content. The prior user exemptions to infringement under Australian and other countries’ (such as Japanese, EU and Canadian) law are important mechanisms that allow companies or individuals to continue activities legitimately undertaken prior to the grant of a third party patent. It’s Telstra’s submission that harmonisation of US laws to recognise and adopt similar prior user provisions would be welcomed to similarly provide certainty for commercial practices and investment. Our response below focuses on those aspects of the study into prior user rights that are of particular interest or concern to Telstra. 1a. Please share your experiences relating to the use of prior user rights in foreign jurisdictions including, but not limited to, members of the European Union and Japan, Canada, and Australia. -

Getting to Know Your Telstra Pre-Paid 3G Wi-Fi Let’S Get This Show on the Road

GETTING TO KNOW YOUR TELSTRA PRE-PAID 3G WI-FI LET’S GET THIS SHOW ON THE ROAD You must be excited about your brand new Telstra Pre-Paid 3G Wi-Fi. This guide will help you get connected as quickly and as easily as possible. It’ll guide you through installation and run through all the handy extra features that are included. If all goes to plan you’ll be up and running in no time, so you can get connected while you’re on the move. 2 WHAT’S INSIDE 03 Safety first 06 Let’s get started 13 Getting connected 25 Wi-Fi home page 20 Extra features 22 Problem solving 25 Extra bits you should know 2 SAFETY FIRST Please read all the safety notices before using this device. This device is designed to be used at least 20cm from your body. Do not use the device near fuel or chemicals or in any prescribed area such as service stations, refineries, hospitals and aircraft. Obey all warning signs where posted. RADIO FREQUENCY SAFETY INFORMATION The device has an internal antenna. For optimum performance with minimum power consumption do not shield the device or cover with any object. Covering the antenna affects signal quality, may cause the router to operate at a higher power level than needed, and may shorten battery life. RADIO FREQUENCY ENERGY Your wireless device is a low-power radio transmitter and receiver. When switched on it intermittently transmits radio frequency (RF) energy (radio waves). The transmit power level is optimised for best performance and automatically 3 4 reduces when there is good quality reception. -

The State of 5G Trials

The State of Trials Courtesy of 5G Data Speeds Shows the highest claimed data speeds reached during 5G trials, where disclosed 36 Gb/s Etisalat 35.46 Gb/s Ooredoo 35 Gb/s M1 35 Gb/s StarHub 35 Gb/s Optus 20 Gb/s Telstra 20 Gb/s Vodafone UK 15 Gb/s Telia 14 Gb/s AT&T 12 Gb/s T-Mobile USA 11.29 Gb/s NTT DoCoMo 10 Gb/s Vodafone Turkey 10 Gb/s Verizon 10 Gb/s Orange France 9 Gb/s US Cellular 7 Gb/s SK Telecom 5.7 Gb/s SmartTone 5 Gb/s Vodafone Australia 4.5 Gb/s Sonera 4 Gb/s Sprint 2.3 Gb/s Korea Telecom 2.2 Gb/s C Spire 5G Trial Spectrum Shows the spectrum used by operators during 5G trials, where disclosed Telstra Optus NTTDoCoMo AT&T AT&T AT&T AT&T Verizon Vodafone Korea Vodafone Bell Vodafone StarHub UK Telecom Turkey Canada Turkey Sonera China SmarTone C Spire Verizon Mobile M1 Vodafone Sprint Korea Australia Telecom Optus Telia NTT DoCoMo Sprint Turkcell SK Telecom US Cellular T-Mobile USA Verizon US Cellular Verizon SUB 3 3.5 4.5 SUB 6 15 28 39 64 70 70-80 71-76 73 81-86 60-90 GHTZ Operator 5G Trials Shows the current state of 5G progress attained by operators Announced 5G trials Lab testing 5G Field testing 5G Operators that have announced timings of Operators that have announced Operators that have announced that they trials or publicly disclosed MoUs for trials that they have lab tested 5G have conducted 5G testing in the field Equipment Providers in 5G Trials Shows which equipment providers are involved in 5G trials with operators MTS T-Mobile USA SK Telekom Verizon Batelco Turkcell AT&T Bell Canada Sonera SmarTone Vodafone Orange BT Taiwan Germany Telia Mobile Telstra C Spire Vodafone US Cellular Vodafone Turkey M1 Australia MTS Ooredoo M1 NTT Docomo Optus Orange China StarHub Mobile Korea Telecom 5G trials with all five equipment providers Telefonica Deutsche Telekom Etisalat Telus Vodafone UK Viavi (NASDAQ: VIAV) is a global provider of network test, monitoring and assurance solutions to communications service providers, enterprises and their ecosystems. -

Copy of TP-Concession to Customers R Final 22.04.2021.Xlsx

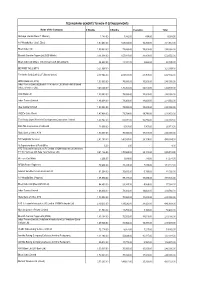

TECHNOPARK-BENEFITS TO NON-IT ESTABLISHMENTS Name of the Company 6 Months 3 Months Esclation Total Akshaya (Kerala State IT Mission) 1,183.00 7,332.00 488.00 9,003.00 A V Hospitalities ( Café Elisa) 1,97,463.00 1,08,024.00 16,200.00 3,21,687.00 Bharti Airtel Ltd 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Bharath Sanchar Nigam Ltd (BSS Mobile) 3,14,094.00 1,57,047.00 31,409.00 5,02,550.00 Bharti Airtel Ltd (Bharti Tele-Ventures Ltd (Broad band) 26,622.00 13,311.00 2,662.00 42,595.00 BEYOND THE LIMITS 3,21,097.00 - - 3,21,097.00 Fire In the Belly Café L.L.P (Buraq Space) 4,17,066.00 2,08,533.00 41,707.00 6,67,306.00 HDFC Bank Ltd (ATM) 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Indus Towers Limited [Bharti Tele-Ventures Ltd (Mobile-Airtel) Bharti Infratel Ventures Ltd] 3,40,524.00 1,70,262.00 34,052.00 5,44,838.00 ICICI Bank Ltd 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Indus Towers Limited 1,46,604.00 73,302.00 14,660.00 2,34,566.00 Idea Cellular Limited 1,50,000.00 75,000.00 15,000.00 2,40,000.00 JODE's Cake World 1,47,408.00 73,704.00 14,741.00 2,35,853.00 The Kerala State Women's Development Corporation Limited 1,67,742.00 83,871.00 16,774.00 2,68,387.00 RAILTEL Corporation of India Ltd 13,008.00 6,504.00 1,301.00 20,813.00 State Bank of India, ATM 1,50,000.00 75,000.00 15,000.00 2,40,000.00 SS Hospitality Services 2,81,190.00 1,40,595.00 28,119.00 4,49,904.00 Sr.Superintendent of Post Office 6.00 3.00 - 9.00 ATC Telecom Infrastructure (P) Limited (VIOM Networks Ltd (Wireless TT Info Services Ltd, Tata Tele Services Ltd) 3,41,136.00 -

LTE-M & NB-Iot Measurements in Australia

Audit Report. LTE-M & NB-IoT measurements in Australia umlaut report umlaut report Foreword umlaut has tested the quality of the Mobile Networks in the Australian The company is headquartered in market and took a detailed look into Aachen, Germany and is a world the LTE-M & NB-IoT scanner mea- leader in mobile network testing and surements of the operators offering benchmarking. these services. 2 3 umlaut report umlaut report Report facts Testing Area 48,000 km States measured driven km Australian Capital Territory Victoria Northern Territory W43 2019 Western Australia to W48 2019 South Australia Data collection Queensland time period Tasmania The map shows the total driving area for Australia. The routes were independently selected by umlaut. 4 5 umlaut report umlaut report Overall coverage comparison per region NB-IoT and LTE-M technologies overall NB-IoT coverage comparison LTE-M coverage comparison coverage comparison per region per region per region Telstra Vodafone Telstra Vodafone Telstra Vodafone 100 100 100 The observation period was between CW43 2019 and CW48 2019. Telstra shows a higher NB-IoT coverage than Vodafone in [%] [%] [%] all eight Australian regions. Telstra is the only operator to deploy LTE-M technology in Australia showing high signal network coverage country wide. 0 0 0 South South South Overall Overall Overall Victoria Victoria Victoria Western Western Western Territory Territory Territory Australia Australia Australia Australia Australia Australia Northern Northern Northern Tasmania Tasmania Tasmania New South New South New South Queensland Queensland Queensland Wales & ACT Wales & ACT Wales & ACT 6 7 umlaut report umlaut report Signal coverage level and quality comparison per region (total) Telstra shows higher average values for NB-IoT signal Telstra shows an average of -10,4 dB for NB-IoT signal Telstra shows an average of -15,5 dB for LTE-M signal net- network coverage (NRSRP) than Vodafone in 6 out of 8 network quality (NRSRQ) and is slightly worse (~1dB) than work quality (RSRQ) in all Australian regions. -

Reliance Industries and Reliance Communications Sign Telecom Tower Pact

Reliance Industries and Reliance Communications Sign Telecom Tower Pact The Ambani brothers have signed a mega deal to share mobile telecom towers. The agreement would permit Reliance Jio Infocomm, a subsidiary of Mukesh Ambani's, Reliance Industries Limited to rent 45000 telecom towers of Anil's Reliance Communications for a period of 15 years. Reliance Jio Infocomm will pay Rs. 12000 crores to Reliance Communication for this lease, which translates to around Rs. 14000-15000 per tower per month. The deal is a win-win for both the companies as it provides a regular income stream for Reliance Comunications and a quicker and economical network capability to Reliance Jio Infocomm when it rolls out its 4G services. Reliance Jio Infocomm could commence occupying some of the towers in the next six months. As per the market sources, Reliance Jio Infocomm did a hard bargain as the prevailing market rental value for a telecom tower ranges around Rs. 25000 - 30000 per month. Reliance Communication will use a large part of the proceeds to retire debt. It has an outstanding debt of around Rs 39,000 crores. This is the second telecom business deal between the two Ambani brothers. Earlier, in April this year these two companies had signed a Rs. 1200 crore pact to share the optic fibre network for carrying call traffic across the country. According to Gurdeep Singh - chief executive (mobility), Reliance Communications, it is possible that these two firms will sign more deals that are mutually beneficial. Synergies in telecom operations appear to have brought the two family factions together. -

PIPE Networks Submission to Senate Inquiry

Senate Standing Committee on Environment, Communications and the Arts Inquiry into the Telecommunications Legislation Amendment (Competition and Consumer Safeguards) Bill 2009 Submission of PIPE Networks Limited (Public version) 7 October 2009 1. Executive summary.......................................................................................................... 2 2. Scope............................................................................................................................... 2 3. About PIPE Networks ...................................................................................................... 2 4. Importance of facilities access......................................................................................... 3 4.1. PIPE’s fibre network................................................................................................. 3 4.2. ‘Facilities access’ vs ‘declared services’ .................................................................. 3 5. The proposed replacement for ‘negotiate-arbitrate’......................................................... 4 5.1. Current approach – arbitration prevails over agreed terms...................................... 4 5.2. New approach – agreed terms prevail over determinations .................................... 5 6. Telstra’s monetary incentive to delay............................................................................... 7 7. Amendments to Part XIB ................................................................................................ -

Before the FEDERAL COMMUNICATIONS COMMISSION Washington, D.C

Before the FEDERAL COMMUNICATIONS COMMISSION Washington, D.C. In the Matter of PIPE NETWORKS LIMITED, File No. SCL-T/C-2009-____________ Transferor, TPG TELECOM LIMITED, Transferee, PPC 1 LIMITED and PPC 1 (US) INC., Licensees, Application for Consent to Transfer Control of a Private Fiber-Optic Cable System Connecting Australia and Guam, THE PPC 1 SYSTEM JOINT APPLICATION FOR CONSENT TO TRANSFER CONTROL— STREAMLINED PROCESSING REQUESTED PIPE Networks Limited (“PIPE Networks,” FRN 0019313998) and TPG Telecom Limited (previously named SP Telemedia Limited1), an Australian corporation (“TPG Telecom,” FRN 0019355338, and together with PIPE Networks, “the Applicants”), hereby apply for consent to transfer control of the cable landing license for the PPC 1 undersea cable system (“PPC 1 System”), for which PPC 1 Limited (FRN 0017368408) and PPC 1 (US), Inc. (“PPC 1 US”), FRN 0017368432, and together with PPC 1 Limited, the “Licensees”) are joint licensees. 1 SP Telemedia Limited changed its name to TPG Telecom Limited on December 1, 2009. The PPC 1 System is a private fiber-optic undersea cable network connecting Sydney, Australia, with Piti, Guam. It entered into commercial service on October 1, 2009, providing much-needed competitive connectivity on the U.S.-Australia route. On November 11, 2009, PIPE Networks and TPG Telecom entered into an agreement in which TPG Telecom will acquire all of the outstanding shares of PIPE Networks (the “Proposed Transaction”), as described in further detail in part I below. The Applicants request streamlined processing pursuant to Section 1.767(k)(2) of the Commission’s rules, as TPG Telecom and its foreign affiliates lack market power in Australia, the destination market for the PPC 1 System. -

For Personal Use Only Use Personal For

ASX RELEASE 22 September 2009 PPC-1 successfully transmits IP packets between Australia and the USA via Guam PIPE Networks Limited (ASX: PWK) subsidiary, PIPE International (Australia) Pty Ltd today announced that PPC-1 has successfully completed another major milestone by transmitting Internet Protocol (IP) packets end to end between Australia and the USA via Guam. PIPE International in partnership with Australian internet innovator Internode Pty Ltd established IP connectivity from Sydney to San Jose via Guam with initial tests proving to be completely successful. “The PPC-1 project has been an extraordinary journey ‘full of firsts’, however we are delighted that this has been the ‘first’ that we are able to share with one of our foundation customers, Internode”, said Mr Slattery, CEO of PIPE Networks Ltd. Simon Hackett, Managing Director of Internode said that PPC-1 passed its first tests with flying colours. “PPC-1 has successfully demonstrated its performance by allowing Internode to send Internet Protocol (IP) packets end-to-end between Australia and the USA via Guam”, he said. “As the first customer to successfully trial PPC-1 ahead of its official launch on the 8th October 2009, Internode is completely confident in PPC-1’s readiness for official handover to foundation customers, including Internode on October 8”, Mr Hackett said. Since PPC-1 passed first light on 23 August 2009, the teams at PIPE International and Tyco have been undertaking a rigorous testing regime on the system including full capacity testing, commissioning and acceptance testing of the Submarine Line Terminal Equipment (SLTE) and Power Feed Equipment (PFE), and in the past week exhaustive confidence trials.