Q4 2019 Heavy Oil Pricing Update – January 6, 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Water-In-Oil Emulsions Through Porous Media and the Effect

processes Brief Report Water-In-Oil Emulsions through Porous Media and the Effect of Surfactants: Theoretical Approaches Josue F. Perez-Sanchez 1,2 , Nancy P. Diaz-Zavala 1 , Susana Gonzalez-Santana 3, Elena F. Izquierdo-Kulich 3 and Edgardo J. Suarez-Dominguez 2,* 1 Centro de Investigación en Petroquímica, Instituto Tecnológico de Ciudad Madero-Tecnológico Nacional de México, Altamira, Tamaulipas 89600, Mexico; [email protected] (J.P.-S.); [email protected] (N.D.-Z.) 2 Facultad de Arquitectura, Diseño y Urbanismo, Universidad Autónoma de Tamaulipas, Tampico, Tamaulipas 89000, Mexico 3 Departamento de Química-Física, Facultad de Química, Universidad de la Habana, La Habana 10400, Cuba; [email protected] (S.G.-S.); [email protected] (E.I.-K.) * Correspondence: [email protected]; Tel.: +528332412000 (ext. 3586) Received: 14 August 2019; Accepted: 9 September 2019; Published: 12 September 2019 Abstract: The most complex components in heavy crude oils tend to form aggregates that constitute the dispersed phase in these fluids, showing the high viscosity values that characterize them. Water-in-oil (W/O) emulsions are affected by the presence and concentration of this phase in crude oil. In this paper, a theoretical study based on computational chemistry was carried out to determine the molecular interaction energies between paraffin–asphaltenes–water and four surfactant molecules to predict their effect in W/O emulsions and the theoretical influence on the pressure drop behavior for fluids that move through porous media. The mathematical model determined a typical behavior of the fluid when the parameters of the system are changed (pore size, particle size, dispersed phase fraction in the fluid, and stratified fluid) and the viscosity model determined that two of the surfactant molecules are suitable for applications in the destabilization of W/O emulsions. -

Athabasca Oil Corporation Takes Further Actions in Response to The

FOR IMMEDIATE RELEASE ‐ April 2, 2020 Athabasca Oil Corporation Takes Further Actions in Response to the Current Environment CALGARY – Athabasca Oil Corporation (TSX: ATH) (“Athabasca” or the “Company”) is taking further immediate actions in response to the significant decline in global oil prices to bolster balance sheet strength and corporate resiliency. Shut‐in of Hangingstone Asset Due to the significant decline in oil prices combined with the economic uncertainty associated to the ongoing COVID crisis, Athabasca has decided to suspend the Hangingstone SAGD operation. This suspension was initiated on April 2, 2020 and will involve shutting in the well pairs, halting steam injection to the reservoir, and taking measures to preserve the processing facility and pipelines in a safe manner so that it could be re‐started at a future date when the economy has recovered. The Hangingstone asset has an operating break‐even of approximately US$37.50 Western Canadian Select and this action is expected to significantly improve corporate resiliency in the current environment. As part of this action, Athabasca is reducing its corporate staff count by 15%. Hangingstone was Athabasca’s first operated oil sands project that began construction in 2013 and was commissioned in 2015. The Company would like to thank all staff that have worked hard over the years to bring this asset on stream. It is unfortunate that made‐in‐Alberta assets like Hangingstone cannot continue operations under current prices. Revised 2020 Guidance Annual corporate guidance is 30,000 – 31,500 boe/d and reflects a ~2,500 boe/d reduction related to the shut‐in. -

Anatomy of the 10-Year Cycle in Crude Oil Prices Philip K. Verleger

Anatomy of the 10-Year Cycle in Crude Oil Prices Philip K. Verleger, Jr. David Mitchell/EnCana Professor of Strategy and International Management Haskayne School of Business University of Calgary, Calgary, Alberta, Canada March 2009 John Wiley & Sons published Twilight in the Desert in 2005. The book’s author, Mat- thew Simmons, contends the world will confront very high and rising oil prices shortly because the capacity of Saudi Arabia, the world’s largest oil producer, is insufficient to meet the future needs of oil consumers. In 448 pages, Simmons extensively discusses his views regarding Saudi Arabia’s future production levels. He asserts that the Saudis have refused to provide details about their reserves, insinuating at several points that the Kingdom’s leaders withhold information to keep the truth from the public. At its core, Simmons’ book is no more than a long exposition of the peak oil theory first espoused by King Hubbert in 1956. Hubbert, it may be recalled, studied the pattern of discovery of super giant oil fields. His review led him to conclude that world productive capacity would peak and then begin to decline. In 1974, Hubbert suggested the global zenith would occur around 1995. Simmons and other adherents to the “peak oil theory” enjoyed great prominence in the first half of 2008. Again and again, one read or heard that the oil price rise was occurring be- cause the flow from world oil reserves had reached or was approaching the maximum while de- mand was still growing. Here’s what one economist wrote just as prices peaked: Until this decade, the capacity to supply oil had been growing just as fast as de- mand, leaving plenty of room to expand production at the first sign of rising pric- es. -

U.S.-Canada Cross- Border Petroleum Trade

U.S.-Canada Cross- Border Petroleum Trade: An Assessment of Energy Security and Economic Benefits March 2021 Submitted to: American Petroleum Institute 200 Massachusetts Ave NW Suite 1100, Washington, DC 20001 Submitted by: Kevin DeCorla-Souza ICF Resources L.L.C. 9300 Lee Hwy Fairfax, VA 22031 U.S.-Canada Cross-Border Petroleum Trade: An Assessment of Energy Security and Economic Benefits This report was commissioned by the American Petroleum Institute (API) 2 U.S.-Canada Cross-Border Petroleum Trade: An Assessment of Energy Security and Economic Benefits Table of Contents I. Executive Summary ...................................................................................................... 4 II. Introduction ................................................................................................................... 6 III. Overview of U.S.-Canada Petroleum Trade ................................................................. 7 U.S.-Canada Petroleum Trade Volumes Have Surged ........................................................... 7 Petroleum Is a Major Component of Total U.S.-Canada Bilateral Trade ................................. 8 IV. North American Oil Production and Refining Markets Integration ...........................10 U.S.-Canada Oil Trade Reduces North American Dependence on Overseas Crude Oil Imports ..................................................................................................................................10 Cross-Border Pipelines Facilitate U.S.-Canada Oil Market Integration...................................14 -

Canadian Crude Oil and Natural Gas Production and Supply Costs Outlook (2016 – 2036)

Study No. 159 September 2016 CANADIAN CANADIAN CRUDE OIL AND NATURAL GAS ENERGY PRODUCTION AND SUPPLY COSTS OUTLOOK RESEARCH INSTITUTE (2016 – 2036) Canadian Energy Research Institute | Relevant • Independent • Objective CANADIAN CRUDE OIL AND NATURAL GAS PRODUCTION AND SUPPLY COSTS OUTLOOK (2016 – 2036) Canadian Crude Oil and Natural Gas Production and Supply Costs Outlook (2016 – 2036) Authors: Laura Johnson Paul Kralovic* Andrei Romaniuk ISBN 1-927037-43-0 Copyright © Canadian Energy Research Institute, 2016 Sections of this study may be reproduced in magazines and newspapers with acknowledgement to the Canadian Energy Research Institute September 2016 Printed in Canada Front photo courtesy of istockphoto.com Acknowledgements: The authors of this report would like to extend their thanks and sincere gratitude to all CERI staff involved in the production and editing of the material, including but not limited to Allan Fogwill, Dinara Millington and Megan Murphy. *Paul Kralovic is Director, Frontline Economics Inc. ABOUT THE CANADIAN ENERGY RESEARCH INSTITUTE The Canadian Energy Research Institute is an independent, not-for-profit research establishment created through a partnership of industry, academia, and government in 1975. Our mission is to provide relevant, independent, objective economic research in energy and environmental issues to benefit business, government, academia and the public. We strive to build bridges between scholarship and policy, combining the insights of scientific research, economic analysis, and practical experience. For more information about CERI, visit www.ceri.ca CANADIAN ENERGY RESEARCH INSTITUTE 150, 3512 – 33 Street NW Calgary, Alberta T2L 2A6 Email: [email protected] Phone: 403-282-1231 Canadian Crude Oil and Natural Gas Production and Supply Costs Outlook iii (2016 – 2036) Table of Contents LIST OF FIGURES ............................................................................................................ -

Annual Report on Form 20-F ANNUAL REPORT /2012 Annual Report on Form 20-F

ANNUAL REPORT /2012 Annual Report on Form 20-F ANNUAL REPORT /2012 Annual Report on Form 20-F The Annual Report on Form 20-F is our SEC filing for the fiscal year ended December 31, 2012, as submitted to the US Securities and Exchange Commission. The complete edition of our Annual Report is available online at www.statoil.com/2012 © Statoil 2013 STATOIL ASA BOX 8500 NO-4035 STAVANGER NORWAY TELEPHONE: +47 51 99 00 00 www.statoil.com Cover photo: Ole Jørgen Bratland Annual report on Form 20-F Cover Page 1 1 Introduction 3 1.1 About the report 3 1.2 Key figures and highlights 4 2 Strategy and market overview 5 2.1 Our business environment 5 2.1.1 Market overview 5 2.1.2 Oil prices and refining margins 6 2.1.3 Natural gas prices 6 2.2 Our corporate strategy 7 2.3 Our technology 9 2.4 Group outlook 10 3 Business overview 11 3.1 Our history 11 3.2 Our business 12 3.3 Our competitive position 12 3.4 Corporate structure 13 3.5 Development and Production Norway (DPN) 14 3.5.1 DPN overview 14 3.5.2 Fields in production on the NCS 15 3.5.2.1 Operations North 17 3.5.2.2 Operations North Sea West 18 3.5.2.3 Operations North Sea East 19 3.5.2.4 Operations South 19 3.5.2.5 Partner-operated fields 20 3.5.3 Exploration on the NCS 20 3.5.4 Fields under development on the NCS 22 3.5.5 Decommissioning on the NCS 23 3.6 Development and Production International (DPI) 24 3.6.1 DPI overview 24 3.6.2 International production 25 3.6.2.1 North America 27 3.6.2.2 South America and sub-Saharan Africa 28 3.6.2.3 Middle East and North Africa 29 3.6.2.4 Europe and Asia -

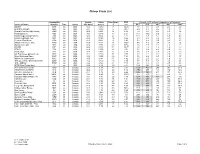

Chicap-Crude-List-7-15-2020.Pdf

Chicap Crude List Commodity Gravity Sulfur Pour Point RVP Viscosity (cST) at listed temperature in Fahrenheit Crude Oil Name Identifier Type Origin °API @60°F mass% °F psi 40°F 50°F 68°F 86°F 104°F Bakken BAK sw USA 42.5 0.080 -71 10.21 4.1 3.6 2.9 2.5 2.0 Grand Mesa Light GML sw USA 48.7 0.060 5 10.67 2.9 2.7 2.2 1.9 1.6 Grand Mesa Sweet@Cushing GMS sw USA 40.2 0.206 32 8.26 7.2 6.0 4.6 3.6 3.0 Mississippi Lime MSL sw USA 34.3 0.519 -11 6.27 16.1 13.2 9.6 7.2 6 Niobrara @Cushing Pony PL NIB sw USA 37.5 0.402 27 8.11 11.1 8.8 6.7 5.1 4.0 Niobrara @Saddlehorn SSC sw USA 43.2 0.144 -38 9.55 5.3 4.5 3.5 2.8 2.3 Permian Sour Blend PRM sw USA 41.9 0.281 -6 8.03 5.1 4.4 3.5 2.8 2.3 Saddlehorn Intermediate SHM sw USA 42.5 0.137 21 10.67 5.6 4.9 3.8 3.1 2.6 Saddlehorn Light SHL sw USA 48.4 0.058 -33 10.54 2.8 2.5 2.1 1.8 1.6 SCOOP SCP sw USA 54.4 0.015 -71 10.77 2.0 1.8 1.6 1.4 1.2 STACK STK sw USA 41.9 0.079 -22 9.71 7.1 6.4 4.9 4.0 3.2 Stack Light STL sw USA 47.4 0.022 5 8.17 3.6 3.3 2.7 2.3 2.0 US High Sweet @Clearbrook UHC sw USA 42.1 0.120 -71 9.78 4.7 4.1 3.2 2.6 2.2 West Oklahoma Sweet WOS sw USA 49.0 0.025 -38 7.84 3.1 2.8 2.3 1.9 1.7 Whitecliffs Condensate WCC sw USA 48.5 0.141 -71 8.82 2.5 2.5 2.1 1.9 1.6 WTI @Cushing - Domestic Sweet DSW sw USA 41.2 0.400 -38 7.69 6.7 5.7 4.4 3.5 2.8 WTI - Midland WTM sw USA 43.6 0.163 -11 7.13 5.3 4.5 3.4 2.7 2.3 WTS (West Texas Sour) C so USA 32.9 1.64 -23 5.67 18.0 14.3 9.9 7.2 5.5 Access Western Blend AWB H Canada 21.6 3.79 -46 6.67 672 457 248 145 91.0 Albian Heavy Synthetic AHS H Canada 20.0 -

2018 ANNUAL INFORMATION FORM Suncor Energy Inc

11FEB201917213713 ANNUAL INFORMATION FORM Dated February 28, 2019 Suncor Energy Inc. 19FEB201920364295 ANNUAL INFORMATION FORM DATED FEBRUARY 28, 2019 TABLE OF CONTENTS 1 Advisories 2 Glossary of Terms and Abbreviations 2 Common Industry Terms 4 Common Abbreviations 4 Conversion Table 5 Corporate Structure 5 Name, Address and Incorporation 5 Intercorporate Relationships 6 General Development of the Business 6 Overview 7 Three-Year History 10 Narrative Description of Suncor’s Businesses 10 Oil Sands 15 Exploration and Production 19 Refining and Marketing 23 Other Suncor Businesses 24 Suncor Employees 24 Ethics, Social and Environmental Policies 26 Statement of Reserves Data and Other Oil and Gas Information 28 Oil and Gas Reserves Tables and Notes 33 Future Net Revenues Tables and Notes 39 Additional Information Relating to Reserves Data 51 Industry Conditions 58 Risk Factors 68 Dividends 69 Description of Capital Structure 71 Market for Securities 72 Directors and Executive Officers 78 Audit Committee Information 80 Legal Proceedings and Regulatory Actions 80 Interests of Management and Others in Material Transactions 80 Transfer Agent and Registrar 80 Material Contracts 80 Interests of Experts 81 Disclosure Pursuant to the Requirements of the NYSE 81 Additional Information 82 Advisory – Forward-Looking Information and Non-GAAP Financial Measures Schedules A-1 SCHEDULE ‘‘A’’ – AUDIT COMMITTEE MANDATE B-1 SCHEDULE ‘‘B’’ – SUNCOR ENERGY INC. POLICY AND PROCEDURES FOR PRE-APPROVAL OF AUDIT AND NON-AUDIT SERVICES C-1 SCHEDULE ‘‘C’’ – FORM 51-101F2 REPORT ON RESERVES DATA BY INDEPENDENT QUALIFIED RESERVES EVALUATOR OR AUDITOR D-1 SCHEDULE ‘‘D’’ – FORM 51-101F2 REPORT ON RESERVES DATA BY INDEPENDENT QUALIFIED RESERVES EVALUATOR OR AUDITOR E-1 SCHEDULE ‘‘E’’ – FORM 51-101F3 REPORT OF MANAGEMENT AND DIRECTORS ON RESERVES DATA AND OTHER INFORMATION ADVISORIES In this Annual Information Form (AIF), references to ‘‘Suncor’’ each year in the two-year period ended December 31, 2018. -

Download Download

https://doi.org/10.3311/PPch.17236 462|Creative Commons Attribution b Periodica Polytechnica Chemical Engineering, 65(4), pp. 462–475, 2021 Recent Approaches, Catalysts and Formulations for Enhanced Recovery of Heavy Crude Oils Umar Gaya1,2* 1 Department of Pure and Industrial Chemistry, Faculty of Physical Sciences, Bayero University, 700241 Kano, 1 Gwarzo Road, Nigeria 2 Directorate of Science and Engineering Infrastructure, National Agency for Science and Engineering Infrastructure (NASENI), Idu Industrial Layout, 900104 Garki, Abuja, Nigeria * Corresponding author, e-mail: [email protected] Received: 20 September 2020, Accepted: 04 December 2020, Published online: 16 August 2021 Abstract Crude oil deposits as light/heavy form all over the world. With the continued depletion of the conventional crude and reserves trending heavier, the interest to maximise heavy oil recovery continues to emerge in importance. Ordinarily, the traditional oil recovery stages leave behind a large amount of heavy oil trapped in porous reservoir structure, making the imperative of additional or enhanced oil recovery (EOR) technologies. Besides, the integration of downhole in-situ upgrading along with oil recovery techniques not only improves the efficiency of production but also the quality of the produced oil, avoiding several surface handling costs and processing challenges. In this review, we present an outline of chemical agents underpinning these enabling technologies with a focus on the current approaches, new formulations and future directions. Keywords in-situ upgrading, enhanced oil recovery, aquathermolysis, heavy oil, catalyst 1 Introduction The world is caught up in the ever-increasing need for Table 1 Selected definitions of heavy crude oil at 15 °C. -

Crudemonitor.Ca Western Canadian Select (WCS)

CrudeMonitor.ca - Canadian Crude Quality Monitoring Program Page 1 of 2 crudemonitor.ca Home Monthly Reports Tools Library Industry Resources Contact Us Western Canadian Select (WCS) What is Western Canadian Select crude? Western Canadian Select is a Hardisty based blend Canada of conventional and oilsands production managed by Liberia Canadian Natural Resources, Cenovus Energy, Manilol Suncor Energy, and Talisman Energy. Argus has sti. launched daily volume-weighted average price ibia Saskalchewan Edmon-i t indexes for Western Canadian Select (WCS) and will publish this index in the daily Argus Crude and Argus Americas Crude publications. Calgary Winnipt Map data ©2013 Google Most Recent Sample Comments: Light Ends Summary Last 6 Samples WCS-807, Sep 17, 2013 Most Property 6 Month 1 Year 5 Year Recent The September 17th sample of Western Canadian ( vol% ) Average Average Average Select contained slightly elevated density, Sample sulphur, MCR, BTEX and C7 x C10 concentrations, C3- 0.04 0.05 0.06 0.06 while butanes and pentanes were slightly Butanes 1.04 1.68 1.82 2.02 decreased. Simulated distillation results indicate Pentanes 3.56 4.76 4.87 4.44 an increase in the residue fraction. Hexanes 3.86 4.10 4.21 3.94 Monthly Reports Heptanes 3.70 3.00 2.96 2.82 Octanes 3.08 2.27 2.14 2.12 Basic Analysis Nonanes 2.36 1.72 1.57 1.50 Decanes 1.27 0.89 0.82 0.72 Most 6 Month 1 Year 5 Year Property Recent Average Average Average Sample BTEX H Density (kg/m3) 934.5 929.6 928.3 929.2 Most 6 Gravity (oAPI) 19.8 20.6 20.8 20.7 Property 1 Year 5 Year Recent Month 0 (vol%) Average Average Sulphur ( wt o) 3.71 3.53 3.51 3.52 Sample Average MCR (wt%) 10.20 10.02 9.84 9.71 Benzene 0.18 0.17 0.18 0.16 Sediment (ppmw) 305 302 296 329 Toluene 0.41 0.33 0.32 0.30 TAN (mgKOH/g) 0.94 0.91 0.93 0.94 • Ethyl Benzene 0.09 0.07 0.06 0.06 Salt (ptb) 28.0 30.9 46.4 Xyl enes 0.45 0.33 0.30 0.29 Nickel (mg/L) 62.7 60.7 59.0 Vanadium (mg/L) 147.0 143.7 141.8 Olefins (wt%) ND ND Distillation *ND indicates a tested value below the instrument threshold. -

Quality and Chemistry of Crude Oils

Journal of Petroleum Technology and Alternative Fuels Vol. 4(3), pp. 53-63, March 2013 Available online at http://www.academicjournals.org/JPTAF DOI:10.5897/JPTAF12.025 ©2013 Academic Journals Full Length Research Paper Quality and chemistry of crude oils Ghulam Yasin1*, Muhammad Iqbal Bhanger2, Tariq Mahmood Ansari1, Syed Muhammad Sibtain Raza Naqvi3, Muhammad Ashraf1, Khizar1 Ahmad and Farah Naz Talpur2 1Department of Chemistry Bahauddin Zakariya University, Multan 60800, Pakistan. 2National Centre of Excellence in Analytical Chemistry, University of Sindh, Jamshoro 76080, Pakistan. 3HDIP Petroleum Testing Laboratory, Multan, Pakistan. Accepted 25 January, 2013 Physico-chemical characteristics such as API (American Petroleum Institute gravity) specific gravity, pour point, Calorific value, Kinematic viscosities, Reid vapour pressure, Copper corrosion, Water and sediments, Total Sulphur, Distillation range (I.B.P.F.B.P., Total recovery), residue and hydrocarbon contents (saturates, aromatics and polar) of crude oils collected from different oil fields of North (Punjab) and South (Sindh) regions of Pakistan have been evaluated using standard ASTM (American Society for Testing and Material) procedures. The results of North Region (Punjab) and South Region (Sindh) crude oils have been compared with each other. Punjab crude oils are better than Sindh crude oils because these have low specific gravity, low sulphur contents, low viscosity and low pour point. All the tested samples are of sweet type on the basis of total sulfur contents except three (L, N, O) samples of south (Sindh) region which are of sour type. All the tested samples belongs to the class light crude oil on the basis of API gravity except one (N) sample which belongs to the medium class. -

Faces of the Future: Conocophillips and Phillips 66 Emerge Spirit Magazine First Quarter 2012 “Energy Production Creates Jobs.”

CONOCOPHILLIPS ConocoPhillips First Quarter 2012 Faces of the Future: ConocoPhillips and Phillips 66 emerge spirit Magazine First Quarter 2012 “Energy production creates jobs.” “We need to protect the environment.” Each wants the best for our country. So how can we satisfy both — right now? At ConocoPhillips, we’re helping to power America’s economy with cleaner, affordable natural gas. And the jobs, revenue and safer energy it provides. Which helps answer both their concerns. In real time. To find out why natural gas is the right answer, visit PowerInCooperation.com © ConocoPhillips Company. 2011. All rights reserved. Sharing Insights Five years ago, I wrote the first Sharing Insights letter for the new spirit Magazine. Since then, the magazine has documented a pivotal time in our company’s history, consistently delivering news and information to a wide-ranging audience. More than 7,000 employees have appeared in its pages. Remarkably, as the magazine grew, so did the number of employees who volunteered to contribute content. When your audience is engaged enough to do that, you know you are making a difference. Now, as we approach the completion of our repositioning effort, I am writing in what will be the final issue of spirit Magazine for Jim Mulva Chairman and CEO the integrated company. I have little doubt that both ConocoPhillips and Phillips 66 will continue to offer robust and engaging internal communications. But it seems fitting that this final issue includes a variety of feature articles, news stories and people profiles that reflect the broad scope of our work across upstream and downstream and the rich heritage of our history.