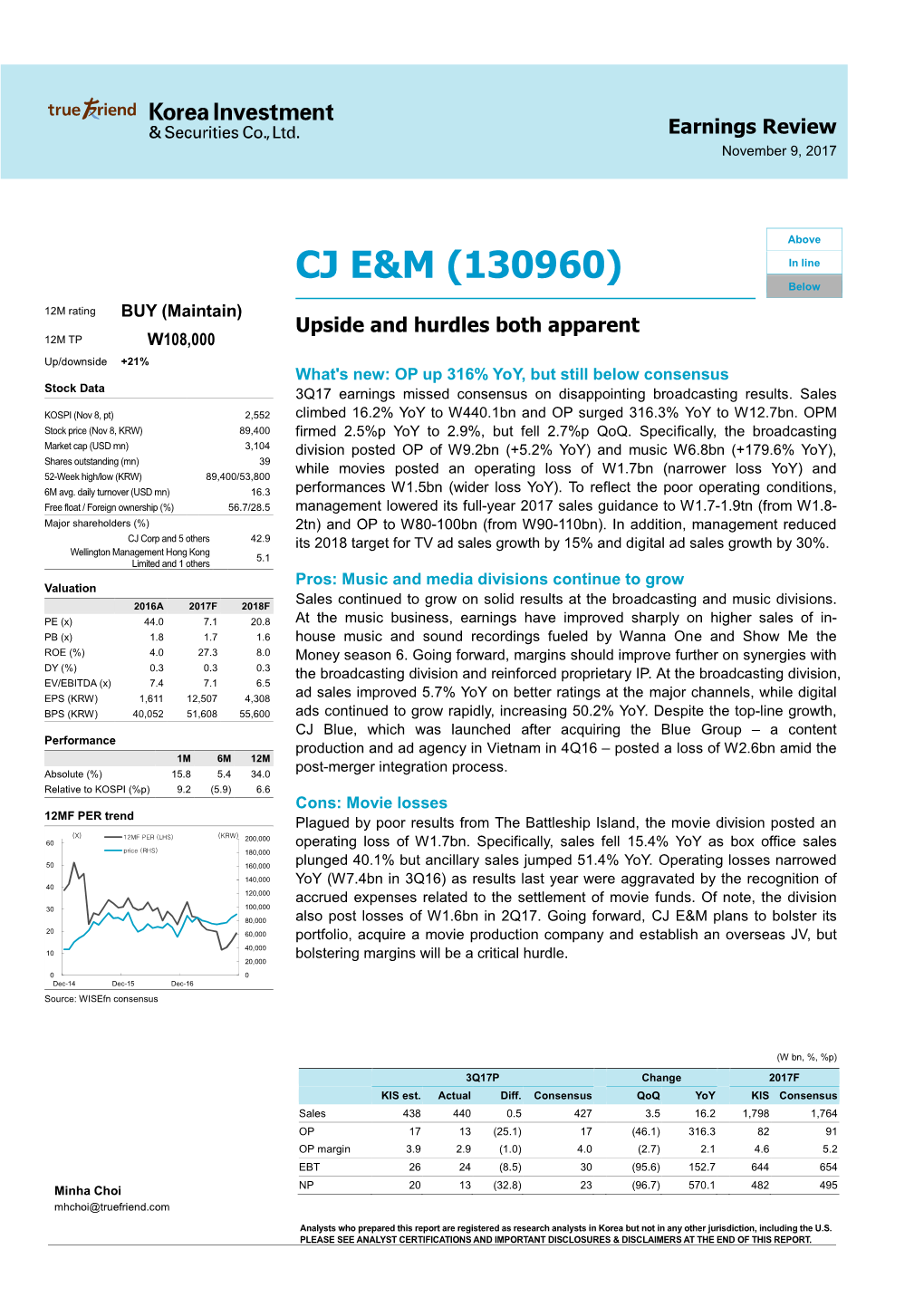

Cj E&M (130960)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

30, 1981 Evefy Thuridajr 26 Pages—25 Cents 11 Wwfcu.N.1

O O\ o oc- c< : <Q 2 m o - M a Q THE WESTFIELD LEADER o J The Leading and Most Widely Circulated Weekly Newspaper In Union County Publ[ih«d NINETY-FIRST YEAR, NO. 39 S^-ood Cbn PnUft PM WESTFIELD. NEW JERSEY,.THURSDAY, APRIL 30, 1981 Evefy Thuridajr 26 Pages—25 Cents 11 WWfcU.N.1. Y Official Balks at Town Another Sidewalk Battle Looms The battle of the Earl Lambert. project is needed to provide by the opponents is the Fairmont Ave., one of more sidewalks leading to Similar dissention oc- safe access for the walk to possibility of converting the than a dozen speakers at the Competition in Camp Market Washington School has been curred about a year ago Washington School and school system to a middle - public hearing on the or- revived—this year on the when council eventually opponents claiming their school concept which would dinance. "We don't need the Summer sports camps compete with the cost," he Jeremiah said he feared southeast side of St. Marks agreed to put sidewalks on own surveys do not warrant eliminate the two upper "Safety starts at home," Recreation Commission as a would emanate to make the said. the entrance of the Ave. between South South Chestnut St., and the the walks and subsequent grades in elementary replied Fred Gould of 716 St. competitor," William camps self-supporting and The Recreation Com- recreation' commission, or Chestnut and Sherman Sts. neighborhood was split on disruption to their schools and reduce Marks Ave. "Cost is not a Jeremiah toM Mayor Allen not dependent on tax mission proposes among its the "public factor," into a Originally scheduled for the issue. -

Kim Min Young Dating

Aug 02, · Park Min Young has shared her thoughts on her rumored romance with her “What’s Wrong with Secretary Kim” co-star Park Seo Joon. On August 1, . Feb 05, · Kim Ji-min’s Boyfriend. Kim Ji-min is single. She is not dating anyone currently. Kim had at least 1 relationship in the past. Kim Ji-min has not been previously engaged. She dated fellow comedian Yoo Sangmoo between and According to our records, she has no renuzap.podarokideal.ruality: South Korean. May 20, · kim ji won for park seo joon!!!!! their chemistry is super good and by the way i can see that many ppl in the comment section voted for pmy, well min young is . Hyun Young. Kim Jong-min and Hyun Young were in a relationship from until Hyun Young is a multi-talented celebrity, that has worked as a model, actress, MC, and even singer. Not much is known as to why they broke up, but was the year Kim was in the military, and Hyun Young was busy with her career. Sep 28, · “Heart Signal Season 1” car racer contestant Seo Joo Won will be tying the knot with model and television personality Kim Min Young. “Heart Signal” is a dating . Who is she dating right now? According to our records, Min-jung Kim is possibly single. Relationships. Min-jung Kim has been in a relationship with Dong-geon Lee ( - ).. About. Min-jung Kim is a 37 year old South Korean Actress born on 30th July, in Seoul, South Korea. Her zodiac sign is Leo. -

THE WESTFIELD LEADER the Leading and Most Widely Circulated Weekly Newspaper in Union County

THE WESTFIELD LEADER The Leading and Most Widely Circulated Weekly Newspaper In Union County Second Clau Po*l«* Published YEAR — NO. 35 »t WeitStliL N. J. WESTFIELD, NEW JERSEY, THURSDAY. APRIL 6, 1978 Every Thursday 24 Pajjes—15 Cents Pools, Courts On Agenda Donovan to Lead Fight Final action is expected at the8:3Op.m. public meeting Tuesday of the Town For Resource Room Funding Council on an ordinance establishing criteria for The Westfield Board of education," said Dr. Westfield, there are 289 which include child study pools and- tennis courts in Education, the Union Laurence F. Greene, students in 14 resource team personnel, general both residential and non- County Chapter of the Westfield's superintendent rqoms. Since resource medical examinations, residential areas in West- Council for Exceptional of schools. rooms will not receive state specific medical field. Children and the New Dr. Donovan will ask the aid for the 1977-78 school examinations such as Also anticipated is in- Jersey Association of Pupil legislators to put $8 million term,Westfield will lose psychiatric and troduction of ordinances to Personnel Administrators into the state budget to fund $311,643 in state aid. If neurological, the cost of amend the Community have sent a letter to the resource rooms for the legislation is passed to translating evaluations into Development Coperation Joint Appropriations handicapped. Although a provide state funds for the predominant language Agreement for 1978-79, to Committee of the New bill has been passed that resource rooms this year of the home, administrative prohibit parking in a section Jersey Legislature asking would provide these funds in Westfield: will receive that costs, secretariat costs, of Gallows Hiil Rd. -

THEWESTFIELD LEADER 77Ie Leading and Most Widely Circulated Weekly Newspaper in Union County

THEWESTFIELD LEADER 77ie Leading and Most Widely Circulated Weekly Newspaper In Union County _1 H Jim a n C\J -• UHPS CS0020 flpconil ClnsH Pomapo Paid l'ullllnhflcl NINETIE J. 7 nt Wmtflclil, N. J. WESTF1ELD, NEW JERSEY, THURSDAY, SEPTEMBER 20,1979 Kvnry Thursday 20 Pngres—20 Cents Senior Citizen Housing Columbus, Elm St. Schools Waiting List Age Lowered Senior citizens may apply facility. However, with residents should be at the who have attained 58 should to be put on the Weslfield more than 60 Westfield youngest permitted age, 62, request a booklet and im- housing waiting list at age 58 residents already on the if possible. Accepting pre- mediately complete and To Go on Auction Block under a new policy adopted waiting list, not accepting applications at 58 will, in return the pre-application Columbus and Elm St. mendations that the two by Superintendent of Tamaques and Franklin — 'In the 'Catch 22' climate by the ' Westfield Senior applications until age G2 has time, make this occur. Also, printed in the booklet. They Schools will be auctioned at Citizens Housing Cor- buildings be declared Schools Laurence F. next fall. of New Jersey," Greene meant that "move-in" age this policy will permit will be put on the list as of a date as yet undecided by surplus and "no longer Greene, it was suggested Plans also are underway said, fewer students means poration, owner and of most residents of the retirement planning in the the date their request is the Board of Education operator of Westfield's 172- necessary or desirable for that school administrative to replace sheds on the lower state aid, higher local building will be in the mid to late '50s with some received, provided that the following its approval school use." and special services be Lincoln School property support, lower caps, higher unit complex on Boynton late COs. -

Viu Adds Korean Shows in July 2018

Beat: Arts Viu Adds Korean shows in July 2018 Vuclip Jeddah - Saudi Arabia, 16.07.2018, 23:12 Time USPA NEWS - Viu adds new Korean titles in the month of July, partnering with top content providers. The partnership will allow Viu to simulcast fresh episodes of some of the famous Korean TV shows every week during the same time as they are being aired in Korea. Additionally, Viu is also updating its library content with a new list of Korean shows which are now available for binge-watching. Simulcast shows for July include Lawless Lawyer, The Undateables, What´s Wrong with Secretary KIM and Wok of Love, and for library titles, the list includes Cheese in the Trap, Emergency Couple, Oh Hae Young Again, Reply 1988, Reply 1997 and Signal. Simulcast Titles Lawless Lawyer Synopsis: A former gangster turned lawyer uses both his fists and legal loopholes to fight against those with absolute power. He is driven by the desire to avenge his mother. To simulcast same time as Korea, one episode every Sunday and Monday, 8 AM Starring: Lee Joon-gi, Seo Ye-ji, Lee Hye-young, Choi Min-soo Episodes: 16 Genre: Drama, Thriller The Undateables Synopsis: The show is about two people who have struggled in love -- Hoon-Nam and Jung-Eum. The couple cross paths and fall into a romantic relationship with each other. To simulcast same time as Korea, two episodes every Thursday and Friday, 9 AM Starring: Namkoong Min, Hwang Jung-eum Episodes: 32 Genre: Romance, Comedy What´s Wrong with Secretary KIM Synopsis: This is the story of a narcissistic boss, Lee Young Joon, and his patient secretary, Kim Mi So, who has remained by his side and worked diligently for nine years. -

THE WESTFIELD LEADER the Leading and Mo$T Widely Circuited Weekly Nempaper in E/Iuen County

.*," THE WESTFIELD LEADER The Leading and Mo$t Widely Circuited Weekly Nempaper In E/iuen County Publish** Seconnd Clan PoitPoiUi f e PaiI i 24 Pages—15 Cento EIGHTY-FOURTH YEAR — No. 45 at w»tf leld, N J. WESTFIELD, NEW JERSEY, THURSDAY, JUNE 20, 1974 Every Thuridty WE A Claims 4.2% Fears Ward 4 "Dumping Place," Asks Pilot Project Five with Perfect Averages Board Offer On Curbside Collection Fourth Ward Councilman periment proved to be in- In Graduating Class of 583 "Unrealistic" Lawrence Weiss- today conclusive," Weiss said, "so called for a pilot program in it is now logical that we Although five Westfield the New Jersey Junior A Westfield Board of comparable communities in the third and fourth wards to move to test the other form High School seniors Classical League award far Education wage offer of a the state. test the acceptability of of effective attic waste achieved perfect 4.0 excellence in the study «f 4,2 percent increase, was Beverly Geddis, WEA curbside collection of attic collection: curbside pickup. averages and tied as first five years of Latin and called "unrealistic" at a president and chief waste in selected areas in "When I campaigned place honor students at outstanding contribution to meeting of the Westfield negotiator commented, Westfield. throughout the fourth ward graduation ceremonies latt Latin department activities Education Association "The latest board proposal Weiss coupled the an-two years ago, a large night, Karim Valjl was - Kathleen Ungford aod Monday afternoon. The in unrealistic in light of the nouncement of his intention majority of residents said recognized as the top honor Lucy Potter. -

J-Rockers * K-Poppers * C-Poppers Comunicação, Mídia, Cultura E Jovens

J-Rockers * K-Poppers * C-Poppers Comunicação, mídia, cultura e jovens Talita de Cássia Mota J-Rockers * K-Poppers * C-Poppers Comunicação, mídia, cultura e jovens Universidade Estadual Paulista “Júlio de Mesquita Filho” Campus Bauru Bauru 2009 Mota, Talita de Cássia. J-Rockers K-Poppers C-Poppers – Comunicação, mídia, cultura e jovens. / Talita de Cássia Mota, 2009. 97 f. : il. Orientador: Cláudio Bertolli Filho Monografia (Graduação)–Universidade Estadual Paulista “Júlio de Mesquita Filho”. Faculdade de Arquitetura, Artes e Comunicação, Bauru, 2009 1. Neotribalismo. 2. Cultura pop. 3. Iden- tidade. 4.Comunicação. 5.Mídia I. Universidade Estadual Paulista “Júlio de Mesquita Filho”, Faculdade de Arquitetura, Artes e Comunicação II. Título.Comunicação, mídia, cultura e jovens. Dedicado à minha avó Dagmar. [in memoria] Sumário Introdução 11 Parte 1 – A comunicação como instrumento de 13 estruturação social e cultural 1. Eu, eles e nós: um pouco de identificação 15 2. Influências Culturais 21 2.1 Imigração e cultura japonesa no Bra- 21 sil 2.2 A imigração coreana 25 2.3 Imigração chinesa 27 3. Comunicação, mídia e potência asiática no 29 Brasil 4. Comunicação e Cibercultura 39 5. Culturas pop e seus fãs: diferentes e genera- 45 lizados Parte 2 – Você já ouviu esse som? 53 1.Rock & Pop: música é fenômeno global 55 2.J-Music: introdução à música japonesa 59 2.1 J-rock e Visual kei: um histórico das 66 muitas variantes do rock japonês 3.K-pop, a qual geração você pertence? 91 4.C-pop, o som made in China 105 Parte 3 – Nesse nosso mundo paralelo 111 1.Neotribalismo: a cultura na pós-moderni- 113 dade 2.O Japão e o Grupo: a difícil sobrevivência da 119 individualidade 3.“Ei, seu otaku!” 125 3.1 “Vamos Fugir?” 127 4.Eles estão aqui 133 5.Considerações Finais 139 Glossário 141 Para acessar 171 Referências Bibliográficas 181 Lista de Imagens 189 8 Agradeço ao grupão querido, Marisa, Rafael, Bianca, Dani, Natália, Luana, Fouad, Aline, Lucas, Carla e Fábio e aos agregados Pátria, Neto e Tácia pelo apoio. -

ENGE 2012 Program Book.Pdf

CONTENTS 02 Welcome Message 03 Committee 05 Venue Layout 06 Conference Information Registration Internet Lounge Speaker’s Room Announcement & Message Board Secretariat Office Coffee Break Lunch Social Programs 08 Technical Program Session Timetable Plenary Speakers Presentation Guidelines Oral Presentation 14 • Sep. 17 (Mon.) 21 • Sep. 18 (Tue.) 30 • Sep. 19 (Wed.) Poster Presentation 39 • Sep. 17 (Mon.) 52 • Sep. 18 (Tue.) 76 • Sep. 19 (Wed.) 93 Author Index Welcome Message PROGRAM Dear Electronic Materials Researchers, On behalf of staff members of ENGE preparation committee, it is my great pleasure to cordially welcome PRESENTATION you to ENGE 2012. SEP. 17 (MON.) ORAL Following the first ENGE in 2010, where about 500 technical papers were presented, we are to meet about 900 papers at this second ENGE international conference contributed by delegates from 12 countries around the world. Especially, we proudly announce 10 topical symposiums at ENGE 2012, where more than 10 prominent researchers for each symposium are invited for an oral presentation of their new PRESENTATION SEP. 18 (TUE.) findings on the electronic materials. ORAL History of a mankind has been grouped depending on the materials governed the corresponding era such as Stone age - New Stone age - Bronze age - Iron age and now it can be said we are living in Electronic materials age. The cutting edge technologies in electronic materials are advancing so fast that in the year PRESENTATION of 2010, a certain number of professors in Korea felt it essential to build a ground, where new findings can SEP. 19 (WED.) be disclosed and exchanged among the researchers. ORAL Research on electronic materials is so interdisciplinary that ENGE is not belonging to any specific academic society. -

Evaluation of U.S. and European Concrete Pavement Noise Reduction Methods July 2006

Evaluation of U.S. and European Concrete Pavement Noise Reduction Methods July 2006 Sponsored by Federal Highway Administration Cooperative Agreement DTFH61-01-X-00042 (Project 15) Part 1, Task 2, of the ISU-FHWA-ACPA Concrete Pavement Surface Characteristics Project National Concrete Pavement Technology Center 2711 South Loop Drive, Suite 4700 Ames, IA 50010 Evaluation of U.S. and European Concrete Pavement Noise Reduction Methods Sponsored by the Federal Highway Administration under Cooperative Agreement DTFH61-01-X-00042 (Project 15) Part 1, Task 2, of the ISU-FHWA Concrete Pavement Surface Characteristics Project Principal Investigator E. Thomas Cackler Director, National Concrete Pavement Technology Center, Iowa State University Co-Principal Investigators Theodore Ferragut Dale S. Harrington President, TDC Partners, Ltd. Principal Senior Engineer, Snyder & Associates Principal Project Engineer Robert Otto Rasmussen, Ph.D. Vice President and Chief Engineer, the Transtec Group, Inc. Project Manager Paul Wiegand Research Engineer, National Concrete Pavement Technology Center, Iowa State University Research Associates Robert Bernhard, Ph.D., Institute for Safe, Quiet and Durable Highways, Purdue University James Cable, Ph.D., Iowa State University George K. Chang, Ph.D., the Transtec Group, Inc. Gary Fick, Trinity Construction Management Services Steven Karamihas, Ph.D., Transportation Research Institute, University of Michigan Eric Mun, the Transtec Group, Inc. Robert Prisby, American Concrete Pavement Association Pennsylvania Chapter -

Using Genattack to Deceive Amazon's and Naver's Celebrity Recognition

When George Clooney Is Not George Clooney: Using GenAttack to Deceive Amazon’s and Naver’s Celebrity Recognition APIs Keeyoung Kim, Simon Woo To cite this version: Keeyoung Kim, Simon Woo. When George Clooney Is Not George Clooney: Using GenAttack to De- ceive Amazon’s and Naver’s Celebrity Recognition APIs. 33th IFIP International Conference on ICT Systems Security and Privacy Protection (SEC), Sep 2018, Poznan, Poland. pp.355-369, 10.1007/978- 3-319-99828-2_25. hal-02023746 HAL Id: hal-02023746 https://hal.inria.fr/hal-02023746 Submitted on 21 Feb 2019 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. Distributed under a Creative Commons Attribution| 4.0 International License When George Clooney is not George Clooney: Using GenAttack to Deceive Amazon's and Naver's Celebrity Recognition APIs Keeyoung Kim1;2;3 and Simon S. Woo1;2 ? 1 The State University of New York, Korea (SUNY-Korea), Incheon, S. Korea 2 Stony Brook University, Stony Brook, NY, USA 3 Artificial Intelligence Research Institute (AIRI), Seongnam, S. Korea {kykim;simon:woo}@sunykorea:ac:kr Abstract. In recent years, significant advancements have been made in detecting and recognizing contents of images using Deep Neural Net- works (DNNs). -

MNC Play Kembali Siarkan Premier League Pertandingan Klub Favorit Kini Dalam Genggaman

For internal distribution only Let’s Play • 2 memo Chief Executive Ade Tjendra Vera Tanamihardja Editor in Chief Aditya Haikal Managing Editor MAGAZINE Nilasari Yani Dirgahayu Indonesia yang Editor Dina Adriandini ke-72! Octaviniant Aspary Bulan ini, Let’s Play hadir Contributor dengan ulasan spesial Michael Kristanto akan Hari Kemerdekaan Diana Rafikasar Tiara Putri Indonesia yang jatuh pada Devi Setya Lestari tanggal 17 Agustus. Andik Sismanto Untuk menyemarakkan Layout and Design peringatan istimewa Muhammad Ali Mu’awiyah Nasution Yustiawan ini, Let’s Play akan Androgama Jaya Pranata menunjukkan berbagai alasan mengapa Indonesia tidak kalah keren dari negara lainnya dan patut untuk kita puja! Photographer Victor Sasongko Agar semakin mengenal dan mencintai tanah air kita ini, Bayu Aji Saputra Fadil Kalimuda Siregar Let’s Play juga menyajikan ulasan mengenai berbagai program acara kuliner dan traveling khas Indonesia secara eksklusif dari saluran Food & Travel. Tak ketinggalan, wawancara yang inspiratif bersama Runner Up Miss World 2016 asal Indonesia Natasha Publisher Mannuela yang banyak memiliki segudang prestasi untuk mengharumkan nama Indonesia namun tidak berhenti berkarya untuk Indonesia. Ada pula kejutan dari beragam saluran berkualitas MNC Play seperti HBO, CinemaWorld, Zee, TVN, hingga BabyTV Office yang hadir dengan program-program khusus untuk MNC Tower, Lantai 10, 11, 12A, 25, bulan ini. Jl. Kebon Sirih No. 17-19, Gondangdia, Jakarta Pusat Selamat menikmati, Players! Phone : (+62-21) 392 6933 Ext. 1035, Merdeka! Fax : (+62-21) -

Cha Jin Wook Dating

My Secret Romance (Korean: 애타는 로맨스; RR: Aetaneun Romaenseu) is a South Korean television series starring Sung Hoon and Song renuzap.podarokideal.ru aired on cable network OCN at every Monday and Tuesday, from April 17 to May 30, for 14 renuzap.podarokideal.ru was also released on SK Telecom's "oksusu" mobile app.. My Secret Romance was selected in the Top Creator Audition Original network: OCN. Who is he dating right now? According to our records, Jin-wook Lee is possibly single. Relationships. Jin-wook Lee has been in relationships with Hyo-Jin Kong () and Ji-woo Choi ( - ).. About. Jin-wook Lee is a 38 year old South Korean Actor. Born on 16th September, in South Korea, he is famous for Panasonic print ad model in a career that spans –present. He then bagged the leading role of Cha Jin-wook in the South Korean television series ‘My Secret Romance’. It aired on OCN for 13 episodes starting from April 17, , to May 30, , marking the first romantic drama by the cable network. Dec 13, · ASTRO's Cha Eun Woo opened up about his dating experience.. On December 13, Cha Eun Woo joined KBS2's 'Happy Together 4' as the special renuzap.podarokideal.ru handsome idol star, who is rumored to be a motae solo. Cha Jin-Wook is a son from a wealthy family. His family runs a large company. Cha Jin- Wook only pursues short term love. He meets Lee Yoo-Mi (Song Ji-Eun) and changes. Lee Yoo-Mi has never had a boyfriend before. Notes.