Automotive Communities Program Center for Automotive Research

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Opel GT: Opel Goes Roadster

January 2007 Opel GT: Opel Goes Roadster • Classic proportions: sleek silhouette, long hood, short overhangs • Archetypal roadster architecture with front-mounted engine and rear-wheel drive • High-tech turbo direct injection and twin A-arms • Roadster fun and performance at affordable price: 264 hp for 30,675 euros Rüsselsheim. The modern definition of an athletic two-seater finds its form in the new Opel GT. As a classic roadster, it has a powerful front-mounted engine, rear-wheel drive, a cockpit with sporty instruments and a tailor-made fabric roof. With a wide stance, sleek silhouette, long, front-hinged hood and short overhangs, the proportions are typical of this class. The Opel GT also brings new charm to this genre with its own unmistakable personality thanks to its exciting shape, which contrasts sharp edges with curved surfaces to create a dynamic look, and its configuration, which enables a refined driving experience, even on long journeys. The GT’ s pricing is also attractive. For 30,675 euros (recommended retail price in Germany incl. VAT), customers get no less than 264 hp from the high-tech turbo engine with gasoline direct injection. Acceleration from zero to 100 km/h takes less than six seconds. The new two-seater carries its legendary name because it continues the tradition of the first Opel GT (1968 – 1973) and, like the original, competes in one of the most exciting vehicle classes. The new Opel GT also showcases the brand’ s passion for dynamic cars, and the conviction that “ Opel was never as young as today” . This is underlined by niche models with a high fun factor, such as the Astra GTC with panorama windshield, the Tigra TwinTop Information concerning specifications and equipment applies to the models offered in iermany. -

2007 Saturn Aura

2007 SATURN AURA The Aura is a midsize car that replaces Saturn’s L series. The newcomer shares its platform with the Malibu, the Pontiac G6 and the Saab 9-3. For the time being, it is only available as a sedan; a station wagon should arrive in a year or two. The XE version gets a 3.5L V6, whereas in XR trim power to the front wheels comes courtesy of a 3.6L V6. A hybrid version will be added sometime in 2007, and a four cylinder should be available the following year. The Aura is similar in size to the Accord, Altima and Camry, give or take a few centimetres. Interior and trunk Because of the car’s relatively low stance, tall people may not find it all that easy to enter and exit the Aura. The doors open wide and are not easy to close once you’re seated. The front seats are very comfortable, but the controls to adjust them are hard to reach when the doors are closed. Headroom is a bit tight for tall individuals. Added to the difficulty accessing the front is the sharp rearward angle of the roof that makes it that much harder to get in and out of the back. The rear bench seats two adults comfortably. Headroom for tall people is rather limited. The seatback is split 60/40 but folds to reveal an opening lacking in both height and width. The trunk is roomy but has a small opening that won’t accept bulky items. There is no hand grip to help open the trunk lid. -

2009 Saturn Vue Warranty.Pdf

IMPORTANT: This booklet contains important information about the vehicle’s warranty coverage. It also explains owner assistance information and Saturn’s participation in the Mediation/Arbitration Program. Keep this booklet with your vehicle and make it available to a Saturn retailer if warranty work is needed. Be sure to keep it with your vehicle if you sell it so future owners will have the information. Owner’s Name: Street Address: City & State: Vehicle Identification Number (VIN): Date Vehicle First Delivered or Put In Use: Odometer Reading on Date Vehicle First Delivered or Put In Use: © 2008 Saturn Corporation U.S.A. All rights reserved. Printed in U.S.A. GENERAL MOTORS and GM are registered trademarks of General Motors Corporation. SATURN and the SATURN emblems are registered trademarks of Saturn Corporation. Part No. 15898479 B Second Printing 2009 Saturn Limited Warranty and Owner Assistance Information An Important Message to Owners... .....................1 After-Manufacture “Rustproofing” ........................12 Saturn’s Commitment to You ..............................1 Paint, Trim, and Appearance Items ....................12 Owner Assistance .............................................1 Vehicle Operation and Care ..............................13 GM Participation in an Alternative Dispute Maintenance and Warranty Service Records ........13 Resolution Program ........................................1 Chemical Paint Spotting ...................................13 Warranty Service – United States and Canada ......1 Warranty Coverage -

SN. Market Make Model Year Range Feature Model Code OBD

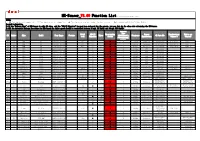

MX-Sensor_V3.09 Function List(Note:For reference only) NOTES: ● This function is supported. ○ This function is not supported. ▲ This function is a new feature in this version. Mark explaining(Red:New,Yellow:Modify) Special Declaration: 1).If the "Relearn Type" of MX-Sensor is only OBD type, and the "OBD-II Function" has not been released for the moment, you can just do the clone for relearning the MX-Sensor. 2).All the Automatic Relearn Procedure for MX-Sensor,the drive speed should be controlled between 16 mph (25 km/h) and 64 mph (100 km/h). Relearn Type Model OBD-II Programming Sensor Manufacturer Number on SN. Market Make Model Year Range Feature Tires (A=Automatic, Frequency OE Part NO. code Function Status Manufactuer Sensor # Sensor# S=Stationary, O=OBD) 103 EU BMW M5 2014/03-2016/06 F10 ○ 4 ● A 433Mhz Huf/Beru 36106798872 0532207017 RDE017 104 EU BMW M6 2014/03-2016/06 F12 ○ 4 ● A 433Mhz Huf/Beru 36106798872 0532207017 RDE017 105 EU BMW M7 2014/03-2016/06 F01 ○ 4 ● A 433Mhz Huf/Beru 36106798872 0532207017 RDE017 2906 EU BYD G5 2014/01-2015/12 ○ 4 ● S 433Mhz BYD 6B3609200 2907 EU BYD G6 2013/01-2015/12 ○ 4 ● S 433Mhz BYD 6B3609200 2903 EU BYD S7 2015/01-2015/12 ○ 4 ● S 433Mhz BYD 6B3609200 2909 EU BYD Sirui 2015/01-2015/12 ○ 4 ● S 433Mhz BYD 6B3609200 2904 EU BYD Song 2016/1-2016/12 ○ 4 ● S 433Mhz BYD 6B3609200 2908 EU BYD Surui 2015/01-2015/12 ○ 4 ● S 433Mhz BYD 6B3609200 2905 EU BYD Tang 2015/01-2015/12 ○ 4 ● S 433Mhz BYD 6B3609200 2939 EU Cadillac ATS-V 2016/01-2016/12 ○ 4 ● 433Mhz Schrader 20925925 60518416 20925925 2940 EU -

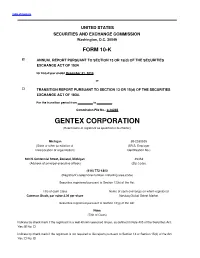

GENTEX CORPORATION (Exact Name of Registrant As Specified in Its Charter)

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 for fiscal year ended December 31, 2010, or o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. For the transition period from to . Commission File No.: 0-10235 GENTEX CORPORATION (Exact name of registrant as specified in its charter) Michigan 38-2030505 (State or other jurisdiction of (I.R.S. Employer Incorporation of organization) Identification No.) 600 N. Centennial Street, Zeeland, Michigan 49464 (Address of principal executive offices) (Zip Code) (616) 772-1800 (Registrant’s telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: Title of each Class Name of each exchange on which registered Common Stock, par value $.06 per share Nasdaq Global Select Market Securities registered pursuant to Section 12(g) of the Act: None (Title of Class) Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes: No: o Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes: o No: Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

2009 Saturn AURA Owner Manual M

2009 Saturn AURA Owner Manual M Seats and Restraint System ............................. 1-1 Driving Your Vehicle ....................................... 4-1 Front Seats ............................................... 1-2 Your Driving, the Road, and the Vehicle ....... 4-2 Rear Seats ............................................... 1-8 Towing ................................................... 4-26 Safety Belts ............................................. 1-10 Service and Appearance Care .......................... 5-1 Child Restraints ....................................... 1-30 Service ..................................................... 5-3 Airbag System ......................................... 1-56 Fuel ......................................................... 5-5 Restraint System Check ............................ 1-72 Checking Things Under the Hood ............... 5-10 Features and Controls ..................................... 2-1 Headlamp Aiming ..................................... 5-41 Keys ........................................................ 2-3 Bulb Replacement .................................... 5-41 Doors and Locks ...................................... 2-10 Windshield Wiper Blade Replacement ......... 5-44 Windows ................................................. 2-15 Tires ...................................................... 5-45 Theft-Deterrent Systems ............................ 2-18 Appearance Care ..................................... 5-81 Starting and Operating Your Vehicle ........... 2-21 Vehicle Identification -

Healthycar.Org 2006-2009 Model Vehicle Rankings Lead Bromine Market Chlorine Overall Rating

HealthyCar.org 2006-2009 Model Vehicle Rankings Lead Bromine Market Chlorine Overall Rating 2006 Model Year Class MPG–Combined Honda Odyssey (2006) Minivan 0.8 0.4 0.0 0.0 20 Chrysler PT Cruiser (2006) SUV 0.8 0.1 0.9 0.0 22 Suzuki Aerio (2006) Station Wagon 0.8 0.4 0.3 0.0 24 Toyota Matrix (2006) Station Wagon 0.9 0.7 0.0 0.0 29 BMW X3 (2006) SUV 0.9 0.5 0.0 0.0 18 Nissan Frontier (2006) Pickup Truck 1.0 0.3 0.6 0.0 21 Honda CRV (2006) SUV 1.0 0.4 0.3 1.4 22 Chevy Colorado 2WD (2006) Pickup Truck 1.2 0.2 0.6 0.0 21 Subaru Tribeca (2006) SUV 1.2 0.5 0.0 0.6 18 Nissan Titan (2006) Pickup Truck 1.3 0.4 0.6 1.7 14 Toyota Tacoma (2006) Pickup Truck 1.3 0.6 0.3 0.0 20 BMW Z4 3.0 (2006) Sport/sporty Car 1.3 0.5 0.3 0.0 21 Acura TSX (2006) Upscale Sedan 1.3 0.6 0.0 0.0 23 Acura RL (2006) Luxury Sedan 1.3 1.2 0.0 0.0 19 Cadillac STS Lux (2006) Upscale Sedan 1.3 0.4 0.6 0.3 19 Mazda MX-5 Miata (2006) Sport/sporty Car 1.4 0.5 0.6 0.0 24 Ford F150 (2006) Pickup Truck 1.4 0.6 0.9 0.3 15 Ford Explorer (2006) SUV 1.4 0.4 0.9 0.0 16 Nissan XTerra (2006) SUV 1.4 0.3 1.2 0.0 17 Suzuki XL7 (2006) SUV 1.4 0.6 0.6 0.6 18 Chevy Equinox (2006) SUV 1.4 0.3 0.6 0.0 18 Ford Freestar (2006) Minivan 1.5 0.5 0.9 0.0 18 BMW M3 Convertible (2006) Convertible 1.5 0.5 0.0 1.9 17 BMW 330 i (2006) Upscale Sedan 1.5 0.9 0.0 1.7 21 Honda Pilot (2006) SUV 1.6 1.0 0.3 0.0 17 Infiniti FX35 (2006) SUV 1.6 0.7 0.6 1.1 18 Acura TL (2006) Upscale Sedan 1.6 0.9 0.9 0.0 21 BMW 335i Coupe (2006) Upscale Sedan 1.6 0.5 0.6 1.4 Toyota 4 Runner (2006) SUV 1.7 0.5 1.2 0.0 18 Saab 9-3 2.0T -

MOTORES CODIGOS 7E

CODIGO MAESTRO DE MOTORES Y TRANSMISIONES CREADO POR: ING. FERNER A. MORALES ABREU AGOSTO 2007-JUNIO 2017 MODEL AÑO CODIGO PETROL ENGINE DIESEL ENGINE TRANSMISION MARCA ACURA 2.5TL 95-98 UA1 2.5L G25A4 B7XA 99-03 UA4 2.5L J25A B7WA / MPYA 2004-2008 UA6 3.2L J32A3 BDGA 2009-present UA8 3.5L J35Z6 BK3A / BK4A CDX 2016-PRESENT 1.5L T 8 speed dual clutch CL 97-99 YA1 3.0L J30A1 / 2.2L F22B1 / 2.3L F23A1 A6VA / B6VA 2001-2003 YA4 3.2L J32A1 / J32A2 (type-s) MGFA CSX 2006-2011 CSX 2.0L K20Z2 / 2.0L D20Z3 (Type-S) MPMA (06-09) / SPCA (10-11) B4RA (97-00) / M4RA (97-98) / S4RA EL 97-00 MB4 1.6L D16Y8 (98-00) BDRA (99-00) 2001-2005 MB5 1.7L D17A2 B46A 1.5L LDA/LEA (hybrid) / 2.0L R20A (auto) M9DA 5 Speed (13-15) / S9FA 5 ILX 2013-Present DE1 / 2.4L K24Z7 (manual) / 2.4L K24W7 (16- speed CVT / M4JA 8 speed (16-) ) INTEGRA 86-89 DA1 1.6L D16A1 CA / P1 1.6L B16A / 1.8L B18A1 / 1.7L B17A1 90-93 DB1 RO / MPRA GS-R / 1.8L B18B1 1.8L B18B1 / 1.8L B18C5 TYPE R / 1.8L 94-99 DB7 B18C VTEC / 1.8L B18C1 / 1.8L B18C3 / MP7A / S4XA 1.8L B18C5 (USA) 2000-2001 DB8 1.8L B18B1 SKWA LEGEND 86-90 KA6 2.5L C25A / 2.7L C27A G4 / L5 / PL5X 92-95 KA8 3.2L C32A MPYA MDX 2001-2006 YD1 J35A3 / J35A5 (04-06) MDKA 2007-2012 YD2 3.7L J37A1 BDKA 2013-Present YD3 3.5L J35Y5 9HP48 (2016-) J4A4 Standard 5 Spd Honda (90-94) / NSX 1990-2005 NSX 3.0L V6 / 3.5L Twin-turbo hybrid SR8M Standard 5 Spd Honda RDX 2007-2012 TB1 2.3L K23A1 Turbo BWEA / BT3A 3.0L J30Y1 (china) / 3.5L J35Y / J35Z2 B8CA (AWD) 6 speed / B8BA 2013- TB2 (2013-2015) FWD 6speed RL 96-98 KA9 3.5L C35A M5DA 99-2004 -

Analysis of the Product Development Process for Geographically Distant Teams in Vehicle Tophat Design Phases By

Analysis of the Product Development Process for Geographically Distant Teams in Vehicle Tophat Design Phases by Antonio Del Puerto Valdez B.S. Mechanical and Electrical Engineering (2001) Instituto Tecnol6gico y de Estudios Superiores de Monterrey Submitted to the System Design and Management Program in Partial Fulfillment of the Requirements for the Degree of Master of Science in Engineering and Management ARCHIES at the SSACHUSETTS INSTITUTE MA~ Massachusetts Institute of Technology OF TECHNOLOGY February 2010 JUN 16 2010 C 2010 Antonio Del Puerto Valdez All rights reserved LIBRARIES The author hereby grants to MIT permission to reproduce and to distribute publicly paper and electronic copies of this thesis document in whole or in part in any medium now known or hereafter created. Signature of Au or Antonio Del Puerto Valdez System Design and Management Program February 2010 Certified L/ Christopher L. Magee Thesis Supervisor Professor of the Practice of Mechanical Engineering and Engineering Systems Co-Director Nineering Design and A nced Manufacturing (EDAM). MIT-Portugal Program -0 n e-7i ( Y Certified by N...J \v~ Patrick Hale Director System Design & Management Program THIS PAGE IS INTENTIONALLY LEFT BLANK To my mother. A paragonof courage and hard work Muchas gracias. THIS PAGE IS INTENTIONALLY LEFT BLANK Analysis of the Product Development Process for Geographically Distant Teams in Vehicle Tophat Design Phases by Antonio Del Puerto Valdez Submitted to the System Design and Management Program in Partial Fulfillment of the Requirements for the Degree of Master of Science in Engineering and Management ABSTRACT The current global economic recession is putting pressure to increase model variation on the carmakers, while at the same time leveraging highly efficient and proven platforms and product development assets globally is becoming critical. -

TEQ® Correct Professional Brake Pads

Most Popular Numbers ‐ TEQ® Correct Professional Brake Pads Line Rank Part # Vehicle Applications Code •Cadillac - Escalade (2002-2006) Front, Escalade ESV (2003-2006) Front, Escalade EXT (2002-2006) Front•Chevrolet - Astro (2003-2005) Front, Avalanche 1500 (2002-2006) Front, Avalanche 2500 (2002-2006) Rear, Express Vans (2003-2008) Front, Silverado Pickups (1999-2007) Front, Silverado Pickups (1999-2010) Rear, Silverado Pickups V8 5.3 (2005-2007) Front, Suburbans (2000-2006) Front, Suburbans (2000-2013) Rear, Tahoe (2000-2006) Front•GMC - C-Series Pickups 1 PDP PXD785H (2000) Rear, C/K Series Pickups (2000) Rear, Safari (2003-2005) Front, Savana Vans (2003-2008) Front, Sierra Pickups (1999-2007) Front, Sierra Pickups (1999-2010) Rear, Sierra Pickups V8 6.6 (2001-2002) Front, Sierra Pickups V8 8.1 (2002) Front, Sierra Pickups V8 6.0 (2005) Front, Sierra Pickups V8 6.0 (2005) Rear, Sierra Pickups V8 6.6 (2005) Rear, Yukons (2000-2006) Front, Yukons (2000-2013) Rear•Hummer - H2 (2003-2009) Rear •Cadillac - Escalade (2008-2014) Front, Escalade ESV (2008-2014) Front, Escalade EXT (2008-2013) Front, XTS (2013) Front•Chevrolet - Avalanche (2008-2013) Front, Express Vans (2009-2014) Front, Silverado Pickups (2005-2013) Front, Silverado Pickups V6 4.3 (2005-2007) Front, Silverado Pickups V8 4.8 (2005-2007) Front, Silverado Pickups V8 5.3 (2005- 2 PDP PXD1363H 2007) Front, Silverado Pickups V8 6.0 (2007) Front, Suburbans (2007-2014) Front, Tahoe (2008-2014) Front, Tahoe V8 4.8 (2008) Front, Tahoe V8 5.3 (2008) Front•GMC - Savana Vans (2009-2013) -

TRB 05-1960 15 Nov 2004

Automotive CO2 Emissions Characterization by U.S. Light-Duty Vehicle Platform Revised Manuscript for TRB, 15 November 2004 Feng An,1 John DeCicco,2* and Huiming Gong1 1Energy and Transportation Technologies, LLC 42977 Ashbury Drive Novi, MI 48375 248-347-9004 [email protected] [email protected] 2Environmental Defense 6327 Todds Lane Dexter, MI 48130 734-424-3742 [email protected] *corresponding author C:\Documents\Active\CarBur\Platforms\An, DeCicco, Gong -- TRB 05-1960 (15 Nov 2004).doc An, DeCicco, and Gong -- TRB 05-1960 2 ABSTRACT Raising the fuel economy of automobiles to lower carbon dioxide (CO2) emissions affects many aspects of vehicle design. Automakers organize their production using platforms, representing shared engineering across different models. A platform level of aggregation is therefore useful when examining the opportunities for and impacts of redesign. This paper explores the CO2 emissions-related characteristics of major platforms in the U.S. market, using data for model year 2002. The top 30 platforms were found to hold 69% of sales and emit 72% of the annualized CO2 contribution of the model year 2002 new light vehicle fleet. Variations of up to 35% in vehicle weight were observed for models within a given platform. The within-platform variation of CO2 emissions rate ranged up to 45% for all platforms among the top 30, except a platform including diesel engines, which had a 67% variation. Across major platforms, average CO2 emissions rates varied by a factor of 2.3 from lowest to highest. Powertrain efficiency, as indicated by ton-miles per gallon, varied by 40% across platforms, with both the lowest and highest values being seen in truck platforms. -

From Turnaround to Transformation

General Motors Corporation 2006 Annual Report From turnaround to transformation Contents 3 Letter to Stockholders 44 Management’s Discussion and Analysis 76 Notes to Consolidated Financial Statements 4 Financial Highlights 67 Disclosure Controls and Procedures 125 Selected Financial Data 10 Design Transformation 68 Management’s Report on Internal Control 126 Board of Directors and Committees 22 Global Transformation over Financial Reporting 128 Senior Leadership Group 28 Technology Transformation 70 Report of Independent Registered Inside Back Cover 36 People Transformation Public Accounting Firm General Information 42 At a Glance 72 Consolidated Financial Statements Front cover: 2007 Opel Astra TwinTop There’s a major turnaround under way at GM. We made broad and signifi cant progress in 2006. We accomplished more than people expected, and in many cases, we even surpassed our goals, on or ahead of schedule. We’re not fi nished. There’s much more to do. But our growing confi dence and excitement is rooted in the fact that we’re not just fi xing problems. We’re transforming GM for fundamental, sustainable, long-term success. General Motors Corporation 1 A full-scale production clay model of the 2009 Chevrolet Camaro starts to take shape at GM’s Warren, Michigan, Design Center, Rear Wheel Drive Performance Studio. Bob Lutz Rick Wagoner Fritz Henderson Vice Chairman, Chairman and Vice Chairman and Global Product Development Chief Executive Offi cer Chief Financial Offi cer 2 General Motors Corporation Dear Stockholders: Our company is in a crucial period in its nearly 100-year history. goals of steady growth, solid profi tability and positive cash I’m pleased to report that, in 2006, the entire GM team rose up generation.