GUIDANCE REPORT: Electric Trucks Where They Make Sense

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ELECTRIC VEHICLES MARKET IS POWERING up an Industry Snapshot

Investment and Company Research Opportunity Research INDUSTRY SNAPSHOT July 2, 2020 ELECTRIC VEHICLES MARKET IS POWERING UP An Industry Snapshot Featured Companies: Tesla (NASDAQ - TSLA); Nikola (NASDAQ – NKLA); Workhorse Group (NASDAQ – WKHS); Alternet Systems (OTC – ALYI) www.goldmanresearch.com Copyright © Goldman Small Cap Research, 2020 Page 1 of 8 Investment and Company Research Opportunity Research INDUSTRY SNAPSHOT OUR THESIS: As of this writing, shares of Tesla (NASDAQ – TSLA), the undisputed bellwether stock for the electric vehicle market trades at $1121 per share. At current prices, the market cap is over $207 billion, representing over 5 estimated 2021 sales and a whopping 98x next year’s EPS. In many investors’ minds, where Tesla goes, so goes the industry segment, especially as it relates to the capital markets. While TSLA is the industry’s most important company, it is the exact mid-point of 2020, not 2016, and therefore is not the only pubco in the space. In fact, some under the radar firms with exposure to the space offer major upside that may rival TSLA, with varying risk profiles and share prices. Instead of making the case for the industry and its constituents in the lithium, fuel cell, and other segments, we have elected to focus on the vehicle producers, where we believe the greatest attention and upside exist. THE EV MARKET: A BRIEF HISTORY We began writing about the EV market in 2015/2016 and while going over our old reports and blogs, we came across some striking information. In 2016, Bloomberg New Energy Finance (now billed as Bloomberg NEF) projected that by 2040, EV passenger sales will reach 41 million units. -

Advanced Technology Equipment Manufacturers*

Advanced Technology Equipment Manufacturers* Revised 04/21/2020 On-Road (Medium/Heavy Duty, Terminal Tractors) OEM Model Technology Vocations GVWR Type Altec Industries, Inc Altec 12E8 JEMS ePTO ePTO ePTO, Utility > 33,000, 26,001 - 33,000 New Altec Industries, Inc Altec JEMS 1820 and 18E20 ePTO ePTO ePTO, Utility > 33,000, 26,001 - 33,000 New Altec Industries, Inc Altec JEMS 4E4 with 3.6 kWh Battery ePTO ePTO, Utility 16,001-19,500, 19,501-26,000 New Altec Industries, Inc Altec JEMS 6E6 with 3.6 kWh Battery ePTO ePTO, Utility 16,001-19,500, 19,501-26,000 New Autocar Autocar 4x2 and 6x4 Xpeditor with Cummins-Westport ISX12N Engine Near-Zero Engine Truck > 33,001 New Autocar Autocar 4x2 and 6x4 Xpeditor with Cummins-Westport L9N Engine Near-Zero Engine Refuse > 33,001 New Blue Bird Blue Bird Electric Powered All American School Bus Zero Emission Bus, School Bus > 30,000 New Blue Bird Blue Bird Electric Powered Vision School Bus 4x2 Configuration Zero Emission Bus, School Bus > 30,000 New BYD Motors BYD 8Y Electric Yard Tractor Zero Emission Terminal Truck 81,000 New BYD Motors BYD C10 45' All-Electric Coach Bus Zero Emission Bus 49,604 New BYD Motors BYD C10MS 45' All-Electric Double-Decker Coach Bus Zero Emission Transit Bus 45' New BYD Motors BYD C6 23' All-Electric Coach Bus Zero Emission Bus 18,331 New BYD Motors BYD K11 60' Articulated All-Electric Transit Bus Zero Emission Bus 65,036 New BYD Motors BYD K7M 30' All-Electric Transit Bus Zero Emission Bus, Transit Bus 30' New BYD Motors BYD K9 40' All-Electric Transit Bus Zero Emission -

11 Electric Vehicle Stocks to Buy for 2021

INVESTOR PLACE 11 ELECTRIC VEHICLE STOCKS TO BUY FOR 2021 LUKE LANGO How to turn the electric disruption of transportation into your million-dollar opportunity When it comes to identifying next-generation breakthrough investments that could rise 100%, 200%, 500%, or more, I always come back to one saying. Where there’s disruption, there’s opportunity. Case-in-point: The internet. Throughout the 1990s, the emergence of the internet rapidly disrupted how people across the globe worked, communicated, and played. For many, it was a scary time. Change is never easy. For many more, it was an exciting time, as the internet was unlocking a new world of possibilities. But… for investors… it was an opportunity. Specifically, it was a once-in-a-decade opportunity to invest early in emerging titans of the internet industry. Like Amazon (AMZN)… when it was a $438 million company in 1997… It’s a $1.6 TRILLION company today – representing a whopping 365,000% return. That means a mere $1,000 investment in Amazon in 1997 would be worth more than $3.6 million today. 2 Luke Lango’s Hypergrowth Investing Need I say more? Where there’s disruption, there’s opportunity – and the bigger the disruption, the bigger the opportunity. Right now, we are on the cusp of an enormous disruption. This disruption will fundamentally and entirely change the world’s multi-trillion-dollar transportation work. In its wake, it will create new hundred-billion-dollar titans of the auto industry – most of whom are just tiny companies today. What disruption am I talking about specifically? The shift toward electric vehicles. -

GM Sells Shuttered Ohio Assembly Plant to Electric Vehicle Startup by David Welch November 7, 2019, 3:10 PM EST

Hyperdrive GM Sells Shuttered Ohio Assembly Plant to Electric Vehicle Startup By David Welch November 7, 2019, 3:10 PM EST Lordstown Motors is still raising money for its plug-in pickup CEO Steve Burns says he hopes to start production in late 2020 rally-goers from selling their homes because of all the jobs he would bring back to the area. Democrats seized on the development as a symbol of unfulfilled promises made to voters in a key battleground state. Trump was so eager to endorse GM’s discussions to sell the Lordstown plant that he preempted the announcement of the talks in May by the largest U.S. automaker and Workhorse. But both companies are on shaky financial footing, with Workhorse totaling just $6,000 of revenue during its latest quarter. American flags fly in front of the GM plant in Lordstown, Ohio, in March. The automaker has sold the factory to Lordstown Motors. Lordstown Motors Corp., the electric-truck startup formed specifically to save a shuttered Ohio car factory, has acquired the highly politicized plant from General Motors Co. The acquisition that the two companies announced Thursday ends an era that began when GM opened the complex in 1966. The factory’s fate was largely sealed when the United Auto Workers union was unable to convince GM to keep it in the fold as part of a new labor contact ratified late last month. With the plant acquisition out of the way, Steve Burns, who Terms of the deal aren’t being disclosed. Workhorse Group used to lead Workhorse and is now chief executive officer Inc., which is affiliated with Lordstown Motors but doesn’t of Lordstown Motors, is turning his attention to phase two: share any ownership, soared 27% to close at $3.13 in New seeking cash to convert the Lordstown plant from making York trading. -

Strategic Design for Delivery with Trucks and Drones

Strategic Design for Delivery with Trucks and Drones James F. Campbell*, Donald C. Sweeney II, Juan Zhang College of Business Administration University of Missouri – St. Louis One University Blvd St. Louis, MO USA Email: [email protected]; [email protected]; [email protected] April 17, 2017 Supply Chain & Analytics Report SCMA-2017-0201 College of Business Administration University of Missouri-St. Louis St. Louis, MO 63121 * Corresponding author Strategic Design for Delivery with Trucks and Drones Abstract Home delivery by drones as an alternative or complement to traditional delivery by trucks is attracting considerable attention from major retailers and service providers (Amazon, UPS, Google, DHL, Wal- mart, etc.), as well as several startups. While drone delivery may offer considerable economic savings, the fundamental issues of how best to deploy drones for home delivery are not well understood. Our research provides a strategic analysis for the design of hybrid truck-drone delivery systems using continuous approximation modeling techniques to derive general insights. We formulate and optimize models of hybrid truck-drone delivery, where truck-based drones make deliveries simultaneously with trucks, and compare their performance to truck-only delivery. Our results suggest that truck-drone delivery can be very advantageous economically in many settings, especially with multiple drones per truck, but that the benefits depend strongly on the relative operating costs and marginal stop costs. 1. Introduction Home delivery by drones is being promoted and researched by a growing number of firms, including Amazon, UPS, Google DHL and Wal-mart, as a possible alternative or complement to traditional delivery by trucks. -

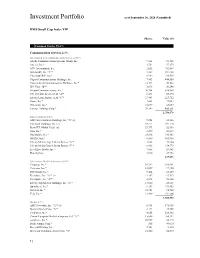

DWS Small Cap Index VIP

Investment Portfolio as of September 30, 2020 (Unaudited) DWS Small Cap Index VIP ______________________Shares Value ($) Common Stocks 98.6% Communication Services 2.3% Diversified Telecommunication Services 0.8% Alaska Communications Systems Group, Inc. 9,664 19,328 Anterix, Inc.* 1,751 57,275 ATN International, Inc. 2,052 102,887 Bandwidth, Inc. "A"* 3,387 591,268 Cincinnati Bell, Inc.* 8,969 134,535 Cogent Communications Holdings, Inc. 7,403 444,550 Consolidated Communications Holdings, Inc.* 12,394 70,522 IDT Corp. "B"* 3,076 20,240 Iridium Communications, Inc.* 20,284 518,865 Liberty Latin America Ltd. "A"* 8,472 69,894 Liberty Latin America Ltd. "C"* 27,483 223,712 Ooma, Inc.* 3,608 47,084 Orbcomm, Inc.* 12,899 43,857 Vonage Holdings Corp.* 39,742 _________406,561 2,750,578 Entertainment 0.2% AMC Entertainment Holdings, Inc. "A" (a) 9,254 43,586 Cinemark Holdings, Inc. (a) 19,171 191,710 Eros STX Global Corp* (a) 23,773 52,538 Gaia, Inc.* 2,099 20,633 Glu Mobile, Inc.* 24,816 190,463 IMAX Corp.* 8,860 105,966 Liberty Media Corp.-Liberty Braves "A"* 1,868 39,004 Liberty Media Corp.-Liberty Braves "C"* 6,415 134,779 LiveXLive Media, Inc.* 7,885 20,462 Marcus Corp. 3,616 _________27,952 827,093 Interactive Media & Services 0.4% Cargurus, Inc.* 14,792 319,951 Cars.com, Inc.* 12,057 97,420 DHI Group, Inc.* 9,464 21,389 Eventbrite, Inc. "A"* (a) 11,367 123,332 EverQuote, Inc. "A"* 2,494 96,368 Liberty TripAdvisor Holdings, Inc. -

What Truck Stop Operators Need to Know About Diesel Exhaust Fluid (DEF) by Chad Johnson, [email protected]

What Truck Stop Operators Need to Know about Diesel Exhaust Fluid (DEF) By Chad Johnson, [email protected] © December 2012 by Gilbarco Inc. SP-3335C Overview Since January 1, 2010, the US Environmental Protection Agency (EPA) has required diesel vehicles to reduce nitrogen oxide emissions significantly. Because of the stringent requirement, most trucks have committed to using Selective Catalytic Reduction system (SCR). SCR reduces nitrogen oxide emissions by converting it into harmless nitrogen through the use of a special catalytic converter and a non-explosive, non-toxic, non-flammable, water-based urea solution called Diesel Exhaust Fluid (DEF). As a result of the new EPA regulation, all truck OEMs have been using a form of NOx emission reduction for their fleets since 2010. Two methods have been deployed to meet the stringent requirements: Exhaust Gas Recirculation (EGR) and Selective Catalytic Reduction (SCR) – with SCR having been the most widely used application. Selective Catalytic Reduction (SCR) SCR reduces tailpipe nitrogen oxide emissions by treating the exhaust stream with a spray of DEF, along with a catalyst that converts NOx into nitrogen and water, which are harmless and present in the air. To reduce NOx, a small amount of DEF is injected directly into the exhaust upstream of a catalytic converter. The DEF vaporizes and decomposes to form ammonia (NH3), which in conjunction with the SCR catalyst reacts with NOx to convert the pollutant into nitrogen (N2) and water (H2O). Exhaust Gas Recirculation (EGR) NOx formation is a function of the high combustion temperature in diesel engines. The hotter the combustion temperature, exponentially more NOx is created from oxygen and nitrogen molecules. -

HOW the NEW REGULATIONS AFFECT YOU United States and Canada

IDLE TALK: HOW THE NEW REGULATIONS AFFECT YOU United States and Canada Updated: March, 2007 ntil recently, diesel truck idling has been standard operating procedure. But stricter idling regulations are Ubecoming more common in many regions, and more rules are guaranteed. This guide explains the situation and offers a summary of current idling regulations so you and your drivers won’t be caught off-guard. A U.S. state-by-state overview of regulations starts on page 5 of this guide, and a list of Canadian regulations on page 11. For background information on truck idling, emerging regulations and what you can do to comply, read on: NEW INFORMATION, LEGISLATION AND BETTER ALTERNATIVES Engine wear and tear. Fleet owners who track idling time discover that engines designed for moving heavy loads at highway speeds often spend around 50% of their life running systems that require a small fraction of their muscle. Idling a heavy- duty diesel engine to operate lights and an air conditioner drives higher fuel and maintenance costs. Fuel costs. High-priced diesel fuel makes extended idling a high-cost activity worth reducing. A large idling diesel engine can consume up to 1.5 gallons per hour. Regulation. Some people are sensitive to the exhaust that idling diesel engines can produce. Large engines at idle also make a low-frequency rumbling sound that many find objectionable. Under certain conditions, these residual effects of idling could be considered public nuisances making further regulation inevitable. Alternatives. Auxiliary power units (APUs), such as the Cummins ComfortGuard™ APU System, can provide a far less expensive, dependable source of energy for equipment used by a resting or parked trucker, thereby virtually eliminating the need for idling. -

Usef-I Q2 2021

Units Cost Market Value U.S. EQUITY FUND-I U.S. Equities 88.35% Domestic Common Stocks 10X GENOMICS INC 5,585 868,056 1,093,655 1ST SOURCE CORP 249 9,322 11,569 2U INC 301 10,632 12,543 3D SYSTEMS CORP 128 1,079 5,116 3M CO 11,516 2,040,779 2,287,423 A O SMITH CORP 6,897 407,294 496,998 AARON'S CO INC/THE 472 8,022 15,099 ABBOTT LABORATORIES 24,799 2,007,619 2,874,948 ABBVIE INC 17,604 1,588,697 1,982,915 ABERCROMBIE & FITCH CO 1,021 19,690 47,405 ABIOMED INC 9,158 2,800,138 2,858,303 ABM INDUSTRIES INC 1,126 40,076 49,938 ACACIA RESEARCH CORP 1,223 7,498 8,267 ACADEMY SPORTS & OUTDOORS INC 1,036 35,982 42,725 ACADIA HEALTHCARE CO INC 2,181 67,154 136,858 ACADIA REALTY TRUST 1,390 24,572 30,524 ACCO BRANDS CORP 1,709 11,329 14,749 ACI WORLDWIDE INC 6,138 169,838 227,965 ACTIVISION BLIZZARD INC 13,175 839,968 1,257,422 ACUITY BRANDS INC 1,404 132,535 262,590 ACUSHNET HOLDINGS CORP 466 15,677 23,020 ADAPTHEALTH CORP 1,320 39,475 36,181 ADAPTIVE BIOTECHNOLOGIES CORP 18,687 644,897 763,551 ADDUS HOMECARE CORP 148 13,034 12,912 ADOBE INC 5,047 1,447,216 2,955,725 ADT INC 3,049 22,268 32,899 ADTALEM GLOBAL EDUCATION INC 846 31,161 30,151 ADTRAN INC 892 10,257 18,420 ADVANCE AUTO PARTS INC 216 34,544 44,310 ADVANCED DRAINAGE SYSTEMS INC 12,295 298,154 1,433,228 ADVANCED MICRO DEVICES INC 14,280 895,664 1,341,320 ADVANSIX INC 674 15,459 20,126 ADVANTAGE SOLUTIONS INC 1,279 14,497 13,800 ADVERUM BIOTECHNOLOGIES INC 1,840 7,030 6,440 AECOM 5,145 227,453 325,781 AEGLEA BIOTHERAPEUTICS INC 287 1,770 1,998 AEMETIS INC 498 6,023 5,563 AERSALE CORP -

Generic Company

Nikola Corporation Nikola Corporation Q1 2021 Earnings Conference Call May 7th, 2021 Presenters Britton Worthen, Chief Legal Officer Mark Russell, Chief Executive Officer Kim Brady, Chief Financial Officer Q&A Participants Paul Coster – JP Morgan Jeff Osborne – Cowen & Company Jeff Kaufman – Vertical Research Partners Chris McNally - Evercore ISI Joseph Spak - RBC Capital Markets Michael Shlisky - Colliers Securities Daniel Ives - Wedbush Securities Operator Good morning and welcome to Nikola Corporation's first quarter 2021 earnings call. At this time, all participants are in a listen-only mode. We begin today's call with a short video presentation followed by management's prepared remarks. A brief question and answer session will follow the formal prepared remarks. If anyone should require operator assistance during the conference, please press *0 on your telephone keypad. As a reminder, this conference is being recorded. We will now begin the video presentation. Video Presentation Thank you. It is my pleasure to now introduce Nikola's Chief Legal Officer, Britton Worthen. Thank you, Britton, you may begin. Britton Worthen Page 1 of 21 Thank you, and good morning, everyone. Welcome to Nikola Corporation's first quarter 2021 Earnings Call. With me today is Mark Russell, Chief Executive Officer of Nikola, and Kim Brady, Chief Financial Officer. During today’s call, we will share our views on the business environment and our financial results for the March 2021 quarter and our outlook for the June 2021 quarter and the full-year 2021. The press release detailing our financial results was distributed a little after 6 am Pacific Time earlier this morning. -

4/7/2017 the Future of Trucks; Implications for Energy and The

The Future of Trucks Implications for energy and the environment The views expressed in this report do not necessarily reflect the views or policy of the International Energy Agency (IEA) Secretariat or of its individual member countries. The paper does not constitute advice on any specific issue or situation. The IEA makes no representation or warranty, express or implied, in respect of the paper’s content (including its completeness or accuracy) and shall not be responsible for any use of, or reliance on, the paper. Comments are welcome, directed to [email protected]. INTERNATIONAL ENERGY AGENCY INTERNATIONAL INSIGHTS SERIES 2O17 SERIES INSIGHTS The Future of Trucks Implications for energy and the environment INTERNATIONAL ENERGY AGENCY INTERNATIONAL INSIGHTS SERIES 2O17 SERIES INSIGHTS INTERNATIONAL ENERGY AGENCY The International Energy Agency (IEA), an autonomous agency, was established in November 1974. Its primary mandate was – and is – two-fold: to promote energy security amongst its member countries through collective response to physical disruptions in oil supply, and provide authoritative research and analysis on ways to ensure reliable, affordable and clean energy for its 29 member countries and beyond. The IEA carries out a comprehensive programme of energy co-operation among its member countries, each of which is obliged to hold oil stocks equivalent to 90 days of its net imports. The Agency’s aims include the following objectives: n Secure member countries’ access to reliable and ample supplies of all forms of energy; in particular, through maintaining effective emergency response capabilities in case of oil supply disruptions. n Promote sustainable energy policies that spur economic growth and environmental protection in a global context – particularly in terms of reducing greenhouse-gas emissions that contribute to climate change. -

Workhorse Group, INC--The Small Cincinnati Company “Delivering” in the Electric Vehicle Race

June 2020 Will Brown Adam Eagleston CEO and Managing Partner CIO Workhorse Group, INC--The Small Cincinnati Company “Delivering” in the Electric Vehicle Race It is rare to find a company at the intersection of two major trends; it’s even more unusual that it is in your hometown. However, that is the case with the aptly named Workhorse Group, Inc. (ticker: WKHS) headquartered in Loveland, OH. Formidable Asset Management (“FAM”) recently established a position; following are the key pieces of our investment thesis: • Established technology and infrastructure • Marquee customers • Undervalued investments Overview Workhorse manufactures electric vehicles (both land-based and aerial), predominantly for use in deliveries (think Amazon, UPS, or the U.S. Postal Service). Despite its presence in this attractive niche, valuable intellectual property, and potentially transformative strategic partnerships, the company trades at a significant discount to our estimate of its intrinsic value. Established technology and infrastructure The company builds more than electric vehicles; it has developed an integrated platform to offer clients a holistic delivery solution that includes cost efficient ground vehicles, telematics to optimize deliveries, and unmanned aerial systems (UASs) for last mile delivery. In the company’s opinion, it is a first mover with a two-to-three year head start over its competitors, which is critically important. Once established, it is very difficult to displace an incumbent within the context of a vehicle fleet, especially one that is integrated. The company has seven (7) granted and four (4) pending patents. As we’ll see later, some of Workhorse’s core electric vehicle intellectual property is currently being licensed.