E2v Annual Report 2010

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

제15권 제2호 2017년 12월 1일

제15권 제2호 2017년 12월 1일 제15권 제2호 1. 틸트 항공기 개발의 역사적 교훈 및 고성능 수직이착륙 무인기 개발 방향 · ···························· 3 한국항공우주연구원, 항공연구본부, 비행체계연구팀 김재무 2. 위성보험 시장 특성 및 동향 분석 · ························································································ 11 한국항공우주연구원,·위성연구본부·정지궤도복합위성사업단 박응식, 이상률 한국항공우주연구원,·경영본부·인프라관리부 이원석, 조정남 3. 중국 발사장 기술 동향 ·········································································································· 21 한국항공우주연구원,·한국형발사체개발사업본부·발사대팀 강선일, 오화영 4. 러시아 로켓엔진산업 구조개편과 엔진개발 동향 · ································································· 31 한국항공우주연구원,·한국형발사체개발사업본부·발사체엔진팀 김철웅, 정은환 5. 2016년 세계 정부 우주개발의 국가별 . 분야별 동향 분석 · ·················································· 41 한국항공우주연구원,·미래전략본부·정책협력부·우주정책팀 이준, 정서영, 임창호, 임종빈, 박정호, 김은정, 신상우 6. 지상기지 현황 및 항우연/독일 지상기지 개발 · ····································································· 66 한국항공우주연구원, 국가위성정보활용지원센터 지상체계개발팀 정대원 1. 민간 무인기 운항안전을 위한 주요국의 UTM 개발 동향 ······················································· 78 한국항공우주연구원, 항공연구본부 항공기획팀 오경륜 한국항공우주연구원, 항공연구본부 비행체계팀 구삼옥 제15권 제2호 2. 재난치안용 멀티콥터 무인기 운용 개념-임무 시나리오를 중심으로 ·································· 84 한국항공우주연구원·항공연구본부·재난치안용무인기개발사업단 김근택, 박민순, 박상욱, 박상현 3. 헬리콥터 주로터 블레이드 동적밸런싱시험의 기술 동향 · ·················································· 97 한국항공우주연구원,·항공연구본부·항공기술연구단·회전익기연구팀 송근웅, 김덕관 4. 우주용 방사차폐 구조 국내 연구 동향 · ·············································································· 109 한국과학기술원,·인공위성연구센터 장태성 한국항공우주연구원,·위성연구본부,·위성사업개발팀 이주훈 5. 심우주 기후관측 위성(DSCOVR)의 특징 · ·········································································· -

HAR5018 Space Bro V2 AW Visual.Indd

HARWELL SPACE MultidisciplinaryCLUSTER Innovation CONTENTS HARWELL FOREWORD CAMPUS 2 Harwell Campus 4 Success of the Harwell Space Cluster 6 Multidisciplinary Innovation 5,500people 8 Building the Harwell Space Cluster 9 Vision for the Future Harwell Campus is an exciting place to be, with cutting edge 10 UK Space Industry science facilities, major organisations and a great mix of companies from start-ups to multinationals. The Campus was quick to realise 12 Stakeholder Organisations £2+bnfacilities that it needed a mechanism to encourage collaboration, knowledge 20 Companies Driving Innovation at Harwell sharing and drive innovation, which led to the development of 40 Life at Harwell thematic Clusters. It started with the Harwell Space Cluster and now includes the HealthTec and EnergyTec Clusters. 42 Harwell Tomorrow 45 Contact I have watched Harwell Campus flourish over the last seven years, including the Harwell Space Cluster, which has grown to 80 organisations employing 800 people. I don’t expect there to be any let up in this growth and I look forward to the Campus changing, literally before my very eyes. SPACE I am really excited about the opportunities at the intersections between these Clusters, such as between the Space and HealthTec Clusters. Harwell CLUSTER Campus is able to demonstrate multidisciplinary innovation every day. There is no better way to really understand what is happening than to visit. I hope that you will do just that and that you will become part of the exciting future of the Harwell Space Cluster and help the UK reach organisations80 its goal of taking 10% of the global space market by 2030. -

2019 09 23 TIAD Space Science 11X17 Size.Indd

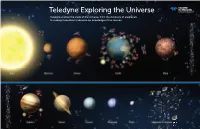

Teledyne Exploring the Universe Teledyne enables the study of the universe, from the discovery of exoplanets to making it possible to advance our knowledge of the cosmos. MISSION HINODE SOLARB MISSION HAYABUSA2 MISSION JUICE 14 SPACE AGENCY JAXA / NASA 28 SPACE AGENCY JAXA 42 SPACE AGENCY ESA DESCRIPTION Studying the impact of the Sun on the Earth DESCRIPTION Asteroid exploration mission DESCRIPTION Studying Jupiter’s icy moons Mission Index LAUNCH YEAR 2006 LAUNCH YEAR 2014 LAUNCH YEAR 2022 COMPANY e2v COMPANY e2v, Reynolds COMPANY e2v, Reynolds, TIS, TES PRODUCTS CCD42-20, CCD42-40 PRODUCTS CCD47-20, CCD47-20, Cables/Connectors PRODUCTS CIS115, H1RG, SIDECAR ASIC, †, Cables/Connectors MISSION NEW HORIZONS MISSION EXOMARS ORBITER MISSION PUNCH MISSION HUBBLE SPACE TELESCOPE HST 15 SPACE AGENCY NASA 29 SPACE AGENCY ESA / ROSCOSMOS 43 SPACE AGENCY NASA 1 SPACE AGENCY ESA/NASA DESCRIPTION Mission to Pluto and the Kuiper Belt DESCRIPTION Investigate trace gases in the Martian DESCRIPTION Focus on the Sun’s corona, and how it generates DESCRIPTION Revolutionised modern astronomy LAUNCH YEAR 2006 atmosphere the solar wind LAUNCH YEAR 1990 COMPANY e2v, TIS, Reynolds LAUNCH YEAR 2016 LAUNCH YEAR 2022 COMPANY e2v, Reynolds, TIS PRODUCTS CCD47-20, CCD96, H1R, Cables/Connectors COMPANY e2v, Reynolds COMPANY e2v PRODUCTS CCD43-82, H1R, SIDECAR ASIC, PRODUCTS CCD30-11, Cables/Connectors PRODUCTS CCD230-82 Cables/Connectors MISSION STEREO A+B 16 SPACE AGENCY NASA MISSION OSIRIS-REx MISSION SPHEREx MISSION SOHO DESCRIPTION Revolutionary view of the -

Spaziali" Dell'inaf Nei Campi Della Fisica Del Sistema Solare, Dell'astrofisica E Della Cosmologia

Number 24 Publication Year 2020 Acceptance in 2020-05-21T09:43:33Z OA@INAF Title Attività "spaziali" dell'INAF nei campi della Fisica del Sistema Solare, dell'Astrofisica e della Cosmologia Authors DELLA CECA, Roberto; SANTORO, MARCO; ARGAN, ANDREA; SPINELLA, LAURA Affiliation of first O.A. Brera author Handle http://hdl.handle.net/20.500.12386/25036 Attività “spaziali” dell’INAF nei campi della Fisica del Sistema Solare, dell’Astrofisica e della Cosmologia In copertina: Illustrazione artistica presa da https://science.jpl.nasa.gov/Astrophysics/index.cfm (Courtesy of NASA/JPL-Caltech). 2 Razionale del presente documento L’Italia può vantare una lunghissima tradizione in campo spaziale essendo stata, nel lontano 1964, la terza nazione a mettere in orbita, con proprio personale, un satellite nazionale dopo USA ed Unione Sovietica. Da allora la comunità internazionale ha segnato enormi progressi in tutti i campi del settore spaziale, dalle telecomunicazioni all’osservazione della Terra, dall’esplorazione robotica del Sistema Solare all’osservazione dell’Universo lontano. Il nostro Paese, grazie al contributo della nostra Agenzia Spaziale, degli Istituti di Ricerca e delle Università italiane, ha mantenuto e consolidato nel tempo la sua posizione di primissimo ordine nelle missioni scientifiche a livello Europeo e mondiale, spesso ricoprendo posizioni di leadership riconosciute a livello internazionale. Guardando al futuro, lo spazio si presenta come una frontiera quanto mai irrinunciabile per la nuova generazione di imprese scientifiche di -

2019 Annual Report

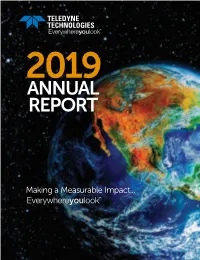

ANNUAL REPORT Making a Measurable Impact... GAAP EPS (a) Sales $3,500 $12 $ In Millions $3,164 $10.73 $ Per Share $3,000 $2,902 $2,604 $10 $9.01 $2,394 $2,500 $2,339 $2,298 $2,127 $2,150 $8 $1,942 $6.26 $2,000 $5.75 $1,644 $6 $5.44 $5.37 $4.87 $1,500 $4.33 $3.81 $ Per$ Share $4 $3.25 $ In Millions $1,000 $2 $500 $0 $0 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 Year Year (a) Represents total GAAP earnings per diluted share for 2013 through 2019 and GAAP EPS from continuing operations for 2010 through 2012. Financial Highlights Selected Consolidated Financial Data (In millions, except per share data) Summary Financial Information 2019 2018 2017 2016 2015 Sales $3,163.6 $2,901.8 $2,603.8 $2,149.9 $2,298.1 Net income attributable 402.3 333.8 227.2 190.9 195.8 to Teledyne Diluted earnings per 10.73 9.01 6.26 5.37 5.44 common share Weighted average diluted 37.5 37.0 36.3 35.5 36.0 common shares outstanding Summary Balance Sheet Data 2019 2018 2017 2016 2015 Cash and cash equivalents $199.5 $142.5 $70.9 $98.6 $85.1 Total assets 4,579.8 3,809.3 3,846.4 2,774.4 2,717.1 Long-term debt 750.0 610.1 1,063.9 509.7 754.1 Total equity 2,714.7 2,229.7 1,947.3 1,554.4 1,344.1 See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the “Notes to Consolidated Financial Statements” in the 2019 Form 10-K for additional information regarding Teledyne Technologies Incorporated’s financial data. -

E2v Annual Report 2011

Financial Highlights 01 l Key Performance Indicators (KPIs) 02 l e2v technologies plc Chairman’s & Chief Executive’s Annual Report and Financial Statements 2011 Statement 03 l Business Review 05 l Five Year Financial Summary 13 l Board of Directors 14 l Corporate Responsibility Review 16 l Directors’ Report 20 l Corporate Governance Report 24 l Directors’ Remuneration Report 27 l Consolidated Financial Statements 33 l Company Financial Statement 74 l Notice of Annual General Meeting (AGM) 84 l Explanation of AGM Business 87 l k l Financial Highlights 01 l Key Performance Indicators (KPIs) Contents 02 l Financial Highlights 01 e2v delivers technology solutions Chairman’s & Chief Key Performance Indicators (KPIs) 02 Executive’s Chairman’s & Chief Executive’s for high performance systems Statement Statement 03 and equipment at a component, 03 l Business Review 05 sub-system and service level. Five Year Financial Summary 13 Business Review Board of Directors 14 05 l Corporate Responsibility Review 16 Directors’ Report 20 Five Year Financial Corporate Governance Report 24 Summary Directors’ Remuneration Report 27 13 l Consolidated Financial Statements 33 Board of Directors Company Financial Statement 74 Notice of Annual General Meeting 14 l (AGM) 84 Explanation of AGM Business 87 Corporate Responsibility Review 16 l Directors’ Report 20 l Corporate Governance Report First half 24 l Second half 233.2 38.2 228.6 Directors’ 21.8 204.6 126.2 123.2 Remuneration Report 201.2 108.7 105.0 29.1 27 l 173.9 27.4 24.7 18.6 106.1 15.8 Consolidated Financial -

Delivering 'Our Vision, Our Future'

Delivering ‘Our vision, our future’ Chelmsford Site Visit - August 2016 Summary of e2v e2v partners with its customers to improve, save and protect people’s lives 1750 employees in 9 engineering locations and 6 sales offices across UK, Europe, US and Asia Pacific Geographic revenue split of: 33% N. America, 27% Europe, 24% Asia, 14% UK, 2% rest of world Asia Pacific revenue growth of 20% 3 divisions with revenue split of: 44% Imaging, 34% RF Power, 22% Semiconductors Revenue driven growth, trusted expert partner, resilient financial profile 2 Business model 3 divisions Strategic drivers Investment proposition In all that we do: “Does this drive growth?” 3 Platform for growth Achieving growth through: - Taking market with innovation/service - Making new markets through product introductions - Focused R&D in growth areas (Industrial Vision, Space, Radiotherapy, Modules & ADC, IP partners, distributors) - Operational improvements and self help - Continuing culture change - Increased focus on acquisitions (2 completed in Industrial Vision and Semiconductors) Medium term growth potential in e2v end markets: - HIGH in automation/healthcare/environment - MEDIUM in communications/discovery 4 Structure and value proposition Imaging - Professional Imaging RF Power Semiconductors High performance image sensors and Components and subsystems that High reliability semiconductors and camera solutions. deliver high performance and high board-level solutions and specialist reliability radio frequency power applications expertise to meet the Fact: -

Teledyne Technologies Incorporated 2020 Annual Report

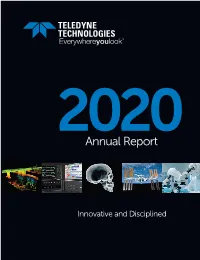

2020 Annual Report Innovative and Disciplined GAAP EPS (a) Sales $3,500 $12 $ In Millions $3,164 $3,086 $10.73 $10.62 $ Per Share $3,000 $2,902 $10 $2,604 $9.01 $2,394 $2,500 $2,339 $2,298 $2,127 $2,150 $8 $1,942 $6.26 $2,000 $5.75 $6 $5.44 $5.37 $4.87 $1,500 $4.33 $3.81 $4 $1,000 $2 $500 $0 $0 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 (a) Represents total GAAP earnings per diluted share for 2013 through 2020 and GAAP EPS from continuing operations for 2011 and 2012. Financial Highlights Selected Consolidated Financial Data (In millions, except per share data) Summary Financial Information 2020 2019 2018 2017 2016 Sales $3,086.2 $3,163.6 $2,901.8 $2,603.8 $2,149.9 Net income 401.9 402.3 333.8 227.2 190.9 Diluted earnings per 10.62 10.73 9.01 6.26 5.37 common share Weighted average diluted 37.9 37.5 37.0 36.3 35.5 common shares outstanding Summary Balance Sheet Data 2020 2019 2018 2017 2016 Cash and cash equivalents $673.1 $199.5 $142.5 $70.9 $98.6 Total assets 5,084.8 4,579.8 3,809.3 3,846.4 2,774.4 Long-term debt 680.9 750.0 610.1 1,063.9 509.7 Total equity 3,228.6 2,714.7 2,229.7 1,947.3 1,554.4 See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the “Notes to Consolidated Financial Statements” in the 2020 Form 10-K for additional information regarding Teledyne Technologies Incorporated’s financial data. -

Next Generation EOS Wind Speed LIDAR Sensor: Hot Pixel Generation and Clock Induced Charge in Te2v EM Ccds

Next generation EOS wind speed LIDAR sensor: Hot Pixel Generation and Clock Induced Charge in Te2v EM CCDs Supervision team: David Hall, Ben Dryer, Andrew Holland External supervisors: Doug Jordan and Paul Jerram, Te2v Lead contact: David Hall ([email protected]) Description: Launched in August 2018, Aeolus is the first satellite that is able to acquire profiles of the Earth’s wind at a global scale. Near-real time observations from the mission are helping to dramatically improve the accuracy of weather and climate prediction, advancing our understanding of climate variability and tropical dynamics. In recent months, with the current global pandemic bringing a sharp decline in weather-related measurements, data from Aeolus has proved even more important to provide accurate forecasting across Europe. The Aeolus mission, the fifth in the family of ESA’s Earth Explorer missions addressing key scientific challenges using breakthrough technology, is collecting these vital data using laser technology. Traditional methods used to gather this type of data involve deploying weather balloons, cloud tracking, and monitoring temperature and surface winds. Instead, the Aeolus satellite employs a very powerful laser in an instrument known as ALADIN. Teledyne e2v, in collaboration with Airbus Defence & Space and ESA, developed an innovative new detector that simultaneously measures the distance of a returned ultraviolet laser pulse to resolve the altitude of aerosols in the atmosphere, and the Doppler shift that equates to the wind speed at each altitude. Teledyne e2v’s detector consists of a 16 x 16 pixel CCD with a novel storage region that accumulates the signal from several successive laser pulses. -

Defence and Security Innovation

DefenceDefence and andSecurity Security RF POWERRF POWER Defence and Security Innovation Providing the power to detect, Page 1 deceive,teledyne-e2v.com defend,/RF Page 1 defeat Defence and Security RF POWER Introduction ABOUT US Founded in 1947, Teledyne e2v first developed Radio Our legacy Frequency sources (magnetrons) for use in air and land We provide the defences. power to detect, deceive, defend and Teledyne e2v’s RF Power division pioneers industry defeat for defence leading innovation and technology around the primes worldwide world, with expertise spanning across life sciences, healthcare, industrial, transportation and defence and security markets. With over 65 years’ experience in the design and manufacture of high performance RF Power technologies, we offer both standard and bespoke Our expertise engineering capabilities to design solutions to exacting In the defence and requirements. security market, our expertise ranges from design and integration right through to support of existing platforms teledyne-e2v.com/RF Introduction Page 2 Defence and Security RF POWER Supporting defence primes for over 60 years Our innovative approach across defence and security technologies supports governments, armed forces, industry and security services around the world Page 2 teledyne-e2v.com/RF Page 3 Defence and Security RF POWER Innovative research, cutting edge development and manufacture Our capabilities We meet the complex requirements of projects and provide innovative, ITAR free solutions across the defence and security spectrum teledyne-e2v.com/RF Page 4 Defence and Security RF POWER High Profile Projects + Projects we are involved in + Bespoke and off-the-shelf solutions Image: Aircraft carrier Eurofighter Typhoon Anti-Piracy at Sea Eurofighter Typhoon is the world’s Piracy at sea undermines humanitarian most advanced swing-role combat efforts as well as impedes safety on aircraft, offering agile performance, maritime routes around the world. -

EMCCD Detector Development for Space Applications: from the Nancy Grace Roman Space Telescope to Future Mission Opportunities

EMCCD detector development for space applications: from the Nancy Grace Roman Space Telescope to future mission opportunities Supervision team: Dr David Hall, Dr Jesper Skottfelt and Prof. Andrew Holland External supervisors: Doug Jordan and David Barry, Te2v Lead contact: David Hall ([email protected]) Description: The Charge-Coupled Device (CCD) has been the detector of choice for space telescopes for visible and X-ray astronomy for several decades, with key successes on the Hubble Space Telescope, XMM-Newton and Gaia to name but a few. However, to push forwards with new discoveries and to better understand the universe we need to observe ever fainter signals. The Centre for Electronic Imaging (CEI) at the Open University (OU) has been involved in Electron-Multiplying (EM) CCD development since 2004. The EMCCD was developed for low- light-level imaging with applications such as night vision. It was later developed further for use in bio imaging and life sciences, observing faint fluorescence from biological samples. The technology works in much the same way as the standard CCD, but includes an additional register in the silicon that allows the application of higher voltages (approximately 5 times higher than those used as standard in a CCD) to employ impact ionisation, multiplying the signal before it leaves the device and therefore before any additional noise is added. In this way, an EMCCD can be operated with much higher frame rates and with sub-electron noise. Despite the new applications that the EMCCD has found on the ground, it is yet to be employed in a large space mission. -

Airbus-Approved-Suppliers-List.Pdf

AIRBUS APPROVAL SUPPLIERS LIST 01 September 2021 AIRBUS APPROVAL SUPPLIERS LIST 01 September 2021 Country CAGE / Company Name code Street City Region Product Group 276086 2MATECH # 19 AVENUE BLAISE PASCAL AUBIERE France AFM-003-4 TEST LAB 305864 3A COMPOSITES GMBH # ALUSINGENPLATZ 1 SINGEN Germany AFM-002-2 MATERIAL PART MANUFACTURING 299679 3D ICOM GMBH & CO KG D3402 GEORG-HEYKEN-STR. 6 HAMBURG Germany AFM-001-2 AEROSTRUCTURE BUILD TO PRINT 309633 3D ICOM GMBH & CO KG # ZUM FLIEGERHORST 11 GROSSENHAIN Germany AFM-001-2 AEROSTRUCTURE BUILD TO PRINT 271379 3M ASD DIVISON PLANT # 801 NO MARQUETTE PRAIRIE DU CHIEN USA AFM-002-2 MATERIAL PART MANUFACTURING 285419 3M CO 8M369 610 N COUNTY RD 19 ABERDEEN USA AFM-002-2 MATERIAL PART MANUFACTURING 133367 3M COMPANY 6A670 3211 EAST CHESTNUT EXPRESS WAY SPRINGFIELD USA AFM-002-2 MATERIAL PART MANUFACTURING 305720 3M COMPANY 68293 2120 E AUSTIN BLVD NEVADA USA AFM-002-2 MATERIAL PART MANUFACTURING 133370 3M DEUTSCHLAND GMBH DL851 DUESSELDORFER STR. 121-125 HILDEN Germany AFM-002-2 MATERIAL PART MANUFACTURING 230295 3M DEUTSCHLAND GMBH D2607 CARL SCHURZ STR. 1 NEUSS Germany AFM-002-1 MATERIAL DISTRIBUTION 133374 3M ESPANA SL 0211B CL JUAN IGNACIO LUCA DE TENA 19-25 MADRID Spain AFM-002-2 MATERIAL PART MANUFACTURING 311744 3M FAIRMONT 5K231 710 N STATE STREET FAIRMONT USA AFM-002-2 MATERIAL PART MANUFACTURING 133379 3M FRANCE F0347 ROUTE DE SANCOURT TILLOY LEZ CAMBRAI France AFM-002-2 MATERIAL PART MANUFACTURING 308272 3M FRANCE # AVENUE BOULE BEAUCHAMP France AFM-003-4 TEST LAB 133376 3M FRANCE SA