Tcbn-2008-Eng.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Buryat Cumhuriyeti'nin Turizm Potansiyeli Ve Başlıca

SDÜ FEN-EDEBİYAT FAKÜLTESİ SOSYAL BİLİMLER DERGİSİ, AĞUSTOS 2021, SAYI: 53, SS. 136-179 SDU FACULTY OF ARTS AND SCIENCES JOURNAL OF SOCIAL SCIENCES, AUGUST 2021, No: 53, PP. 136-179 Makale Geliş | Received : 07.06.2021 Makale Kabul | Accepted : 31.08.2021 Emin ATASOY Bursa Uludağ Üniversitesi, Türkçe ve Sosyal Bilimler Eğitimi Bölümü [email protected] ORCID Numarası|ORCID Numbers: 0000-0002-6073-6461 Erol KAPLUHAN Burdur Mehmet Akif Ersoy Üniversitesi, Coğrafya Bölümü [email protected] ORCID Numarası|ORCID Numbers: 0000-0002-2500-1259 Yerbol PANGALİYEV [email protected] ORCID Numarası|ORCID Numbers: 0000-0002-2392-4180 Buryat Cumhuriyeti’nin Turizm Potansiyeli ve Başlıca Turizm Kaynakları Touristic Potential And Major Touristic Attractions Of Buryatia Republic Öz Rusya Federasyonu’nun Güney Sibirya Bölgesi’nde yer alan Buryat Cumhuriyeti, Saha Cumhuriyeti ve Komi Cumhuriyeti’nden sonra Rusya’nın en büyük yüzölçümüne sahip üçüncü özerk cumhuriyetidir. Siyasi yapılanma olarak Uzakdoğu Federal İdari Bölgesi, ekonomik yapılanma olarak ise Uzakdoğu İktisadi Bölge sınırları içinde yer alan Buryatya, Doğu Sibirya’nın güney kesimlerinde ve Moğolistan’ın kuzeyinde yer almaktadır. Araştırmada coğrafyanın temel araştırma metotları gözetilmiş, kaynak tarama yöntemi aracılığıyla ilgili kaynaklar ve yayınlar temin edilerek veri tabanı oluşturulmuştur. Elde edilen verilerin değerlendirilmesi için haritalar, şekiller ve tablolar oluşturulmuştur. Konunun net anlaşılması amacıyla Buryat Cumhuriyeti’nin lokasyon, Buryat Cumhuriyeti Kültürel Turizm Merkezleri, Buryat Cumhuriyeti’nin Doğal turizm alanları, Buryat Cumhuriyeti milli parkları ve doğa koruma alanları haritalarının yanı sıra ifadeleri güçlendirmek için konular arasındaki bağlantılar tablo ile vurgulanmıştır. Tüm bu coğrafi olumsuzluklara rağmen, Buryatya zengin doğal kaynaklarıyla, geniş Tayga ormanlarıyla, yüzlerce göl ve akarsu havzasıyla, yüzlerce sağlık, kültür ve inanç merkeziyle, çok sayıda kaplıca, müze ve doğa koruma alanıyla, Rusya’nın en zengin turizm kaynaklarına sahip cumhuriyetlerinden biridir. -

Research Article Lake Baikal Ecosystem Faces the Threat of Eutrophication

Hindawi Publishing Corporation International Journal of Ecology Volume 2016, Article ID 6058082, 7 pages http://dx.doi.org/10.1155/2016/6058082 Research Article Lake Baikal Ecosystem Faces the Threat of Eutrophication Galina I. Kobanova, Vadim V. Takhteev, Olga O. Rusanovskaya, and Maxim A. Timofeyev Institute of Biology at Irkutsk State University, Irkutsk State University, Irkutsk 664003, Russia Correspondence should be addressed to Maxim A. Timofeyev; [email protected] Received 18 October 2015; Revised 15 February 2016; Accepted 30 March 2016 Academic Editor: Ram Chander Sihag Copyright © 2016 Galina I. Kobanova et al. This is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited. Recently there have been reports about large accumulations of algae on the beaches of Lake Baikal, the oldest and deepest freshwater body on earth, near major population centers and in areas with large concentrations of tourists and tourism infrastructure. To evaluate the observations indicating the ongoing process of eutrophication of Lake Baikal, a field study in July 2012 in the two largest bays of Lake Baikal, Barguzinsky and Chivyrkuisky, was organized. The study of phytoplankton using the sedimentary method and quantitative records of accumulations of macrophytes in the surf zone was made. In Chivyrkuisky Bay, we found the massivegrowthofcolorlessflagellatesandcryptomonadsaswellastheaggregationsofElodea canadensis along the sandy shoreline 2 (up to 26 kg/m ). Barguzinsky Bay registered abundantly cyanobacterial Anabaena species, cryptomonads, and extremely high 3 biomass of Spirogyra species (up to 70 kg/m ). The results show the presence of local but significant eutrophication of investigated bays. -

Rebirth of the Great Silk Road: Myth Or Substance?

Conflict Studies Research Centre S41 Table of Contents INTRODUCTION 3-5 “THE ANCIENT SILK ROAD” 6-9 TRACECA – THE MODERN SILK ROAD 10-25 Concept of the TRACECA Project 10 The TRACECA Route 11 TRACECA and the Establishment of Transport Corridors 13 First European Transport Conference – Prague 1991 13 Second European Transport Conference – Crete 1994 14 Third European Transport Conference – Helsinki 1995 14 St Petersburg Transport Conference – May 1998 15 Significance of European Transport Conferences in Russia 15 TRACECA Conference 7/8 September 1998 15 Russian Grievances 16 Underlying Factors in Economic Development 19 Natural Resources 21 Trans-Caspian Transport Trends and Developments 22 Creation of a Permanent Secretariat in Baku 22 Increase in Number of Ferries in the Caspian 22 Railway Developments and Proposals 24 Position of Russia, Iran and Armenia in Caucasus-Caspian Region 24 RUSSIAN CONCEPT OF A SUPER MAGISTRAL 26-28 The Baritko Proposal 26 THE PROBLEMS OF THE SUPER MAGISTRAL 29-35 The Problem of Siberia 29 Ravages of Climate compounded by Neglect 29 Financial and Strategic Contexts 30 Problems concerning the Baykal-Amur Magistral 33 CONCLUSIONS 36-38 TRACECA 36 European-Trans-Siberian Trunk Routes 37 APPENDIX 39-41 Text of Baku Declaration of 8 September 1998 1 S41 Tables Table 1 – Euro-Asiatic Trans-Continental Railway Trunk Routes Table 2 – TRACECA – The Modern Silk Road Table 3 – Three Transport Corridors Crossing into and over Russian Territory Table 4 – Trade Flows in the Transcaucasus Table 5 – Kazakhstan’s Railway Development -

DISCOVER URAL Ekaterinburg, 22 Vokzalnaya Irbit, 2 Proletarskaya Street Sysert, 51, Bykova St

Alapayevsk Kamyshlov Sysert Ski resort ‘Gora Belaya’ The history of Kamyshlov is an The only porcelain In winter ‘Gora Belaya’ becomes one of the best skiing Alapayevsk, one of the old town, interesting by works in the Urals, resort holidays in Russia – either in the quality of its ski oldest metallurgical its merchants’ houses, whose exclusive faience runs, the service quality or the variety of facilities on centres of the region, which are preserved until iconostases decorate offer. You can rent cross-country skis, you can skate or dozens of churches around where the most do snowtubing, you can visit a swimming-pool or do rope- honorable industrial nowadays. The main sight the world, is a most valid building of the Middle 26 of Kamyshlov is two-floored 35 reason to visit the town of 44 climbing park. In summer there is a range of active sports Urals stands today, is Pokrovsky cathedral Sysert. You can go to the to do – carting, bicycling and paintball. You can also take inseparably connected (1821), founded in honor works with an excursion and the lifter to the top of Belaya Mountain. with the names of many of victory over Napoleon’s try your hand at painting 180 km from Ekaterinburg, 1Р-352 Highway faience pieces. You can also extend your visit with memorial great people. The elegant Trinity Church was reconstructed army. Every august the jazz festival UralTerraJazz, one of the through the settlement of Uraletz by the direction by the renowned architect M.P. Malakhov, and its burial places of industrial history – the dam and the workshop 53 top-10 most popular open-air fests in Russia, takes place in sign ‘Gora Belaya’ + 7 (3435) 48-56-19, gorabelaya.ru vaults serve as a shelter for the Romanov Princes – the Kamyshlov. -

Download Article (PDF)

Advances in Economics, Business and Management Research, volume 139 International Conference on Economics, Management and Technologies 2020 (ICEMT 2020) Regional Differences in Income and Involvement in the Use of DFS as Factors of Influence on the Population Financial Literacy Elena Razumovskaya1,2,* Denis Razumovskiy1,2 1Department of Finance, Money Circulation and Credit, Ural Federal University named after B.N. Yeltsin, Yekaterinburg, Russia 2Department of Finance, Money Circulation and Credit, Ural State University of Economics, Yekaterinburg, Russia *Corresponding author. Email: [email protected] ABSTRACT The article attempts to analyze the impact of regional differences in income and activity of using digital financial services (DFS) on the financial literacy of the population. The authors proceeded from the hypothesis that the effect of concentration of financial activity in large federal centers of the Russian Federation on other territories, in particular, the Sverdlovsk region, is approximated. The main research hypothesis is that the regular and active use of digital financial services is more inherent with people living in large settlements and having a relatively higher income; these two factors have a decisive influence on the level of financial literacy. The use of constantly developing digital financial services in everyday life allows people to visualize the dynamics of their financial capabilities, analyze and adjust the structure of financial resources, which increases financial knowledge and strengthens -

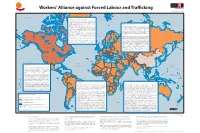

Workers' Alliance Against Forced Labour and Trafficking

165˚W 150˚W 135˚W 120˚W 105˚W 90˚W 75˚W 60˚W 45˚W 30˚W 15˚W 0˚ 15˚E 30˚E 45˚E 60˚E 75˚E 90˚E 105˚E 120˚E 135˚E 150˚E 165˚E Workers' Alliance against Forced Labour and Tracking Chelyuskin Mould Bay Grise Dudas Fiord Severnaya Zemlya 75˚N Arctic Ocean Arctic Ocean 75˚N Resolute Industrialised Countries and Transition Economies Queen Elizabeth Islands Greenland Sea Svalbard Dickson Human tracking is an important issue in industrialised countries (including North Arctic Bay America, Australia, Japan and Western Europe) with 270,000 victims, which means three Novosibirskiye Ostrova Pond LeptevStarorybnoye Sea Inlet quarters of the total number of forced labourers. In transition economies, more than half Novaya Zemlya Yukagir Sachs Harbour Upernavikof the Kujalleo total number of forced labourers - 200,000 persons - has been tracked. Victims are Tiksi Barrow mainly women, often tracked intoGreenland prostitution. Workers are mainly forced to work in agriculture, construction and domestic servitude. Middle East and North Africa Wainwright Hammerfest Ittoqqortoormiit Prudhoe Kaktovik Cape Parry According to the ILO estimate, there are 260,000 people in forced labour in this region, out Bay The “Red Gold, from ction to reality” campaign of the Italian Federation of Agriculture and Siktyakh Baffin Bay Tromso Pevek Cambridge Zapolyarnyy of which 88 percent for labour exploitation. Migrant workers from poor Asian countriesT alnakh Nikel' Khabarovo Dudinka Val'kumey Beaufort Sea Bay Taloyoak Food Workers (FLAI) intervenes directly in tomato production farms in the south of Italy. Severomorsk Lena Tuktoyaktuk Murmansk became victims of unscrupulous recruitment agencies and brokers that promise YeniseyhighN oril'sk Great Bear L. -

Investment Activities

About the company Strategic report Performance overview Investment activities Investment programme approaches The Company’s investment programme The projects’ commercial efficiency Budget efficiency for projects is assessed is designed to: is assessed based on the net cash flow based on comparison of cash inflows (tax, • ensure uninterrupted transportation from investing and operating activities, customs and insurance payments) resulting service; with the resulting estimates taking into from railway infrastructure development • embrace the most promising projects consideration the financial aftermaths vs government-financed investments. in terms of both commercial and budget for the investment project owner assuming efficiency; that such owner fully covers the project • minimise federal government spending costs and reaps all of its benefits. on investment projects. Russian Railways has uniform guidelines in place to assess the efficiency All the investment projects have of investment projects1. With a payback commercial and budget efficiency period of up to 20 years and an IRR estimates in place and are ranked using of at least 10%, an investment project the cost/benefit analysis. is deemed to be sufficiently efficient. 1. In accordance with the Russian Government’s Order No. 2991-r dated 29 December 2017. 76 Russian Railways Sustainable development Corporate governance Appendices Investment highlights in 2019 As adjusted by the Board of Directors PROJECTS INCLUDED the target was met with 115.8 mt of cargo of Russian Railways, the Company’s -

Trans-Baykal (Rusya) Bölgesi'nin Coğrafyasi

International Journal of Geography and Geography Education (IGGE) To Cite This Article: Can, R. R. (2021). Geography of the Trans-Baykal (Russia) region. International Journal of Geography and Geography Education (IGGE), 43, 365-385. Submitted: October 07, 2020 Revised: November 01, 2020 Accepted: November 16, 2020 GEOGRAPHY OF THE TRANS-BAYKAL (RUSSIA) REGION Trans-Baykal (Rusya) Bölgesi’nin Coğrafyası Reyhan Rafet CAN1 Öz Zabaykalskiy Kray (Bölge) olarak isimlendirilen saha adını Rus kâşiflerin ilk kez 1640’ta karşılaştıkları Daur halkından alır. Rusçada Zabaykalye, Balkal Gölü’nün doğusu anlamına gelir. Trans-Baykal Bölgesi, Sibirya'nın en güneydoğusunda, doğu Trans-Baykal'ın neredeyse tüm bölgesini işgal eder. Bölge şiddetli iklim koşulları; birçok mineral ve hammadde kaynağı; ormanların ve tarım arazilerinin varlığı ile karakterize edilir. Rusya Federasyonu'nun Uzakdoğu Federal Bölgesi’nin bir parçası olan on bir kurucu kuruluşu arasında bölge, alan açısından altıncı, nüfus açısından dördüncü, bölgesel ürün üretimi açısından (GRP) altıncı sıradadır. Bölge topraklarından geçen Trans-Sibirya Demiryolu yalnızca Uzak Doğu ile Rusya'nın batı bölgeleri arasında bir ulaşım bağlantısı değil, aynı zamanda Avrasya geçişini sağlayan küresel altyapının da bir parçasıdır. Bölgenin üretim yapısında sanayi, tarım ve ulaşım yüksek bir paya sahiptir. Bu çalışmada Trans-Baykal Bölgesi’nin fiziki, beşeri ve ekonomik coğrafya özellikleri ele alınmıştır. Trans-Baykal Bölgesinin coğrafi özelliklerinin yanı sıra, ekonomik ve kültürel yapısını incelenmiştir. Bu kapsamda konu ile ilgili kurumsal raporlardan ve alan araştırmalarından yararlanılmıştır. Bu çalışma sonucunda 350 yıldan beri Rus gelenek, kültür ve yaşam tarzının devam ettiği, farklı etnik grupların toplumsal birliği sağladığı, yer altı kaynaklarının bölge ekonomisi için yüzyıllardır olduğu gibi günümüzde de önem arz ettiği, coğrafyasının halkın yaşam şeklini belirdiği sonucuna varılmıştır. -

Systemic Criteria for the Evaluation of the Role of Monofunctional Towns in the Formation of Local Urban Agglomerations

ISSN 2007-9737 Systemic Criteria for the Evaluation of the Role of Monofunctional Towns in the Formation of Local Urban Agglomerations Pavel P. Makagonov1, Lyudmila V. Tokun2, Liliana Chanona Hernández3, Edith Adriana Jiménez Contreras4 1 Russian Presidential Academy of National Economy and Public Administration, Russia 2 State University of Management, Finance and Credit Department, Russia 3 Instituto Politécnico Nacional, Escuela Superior de Ingeniería Mecánica y Eléctrica, Mexico 4 Instituto Politécnico Nacional, Escuela Superior de Cómputo, Mexico [email protected], [email protected], [email protected] Abstract. There exist various federal and regional monotowns do not possess any distinguishing self- programs aimed at solving the problem of organization peculiarities in comparison to other monofunctional towns in the periods of economic small towns. stagnation and structural unemployment occurrence. Nevertheless, people living in such towns can find Keywords. Systemic analysis, labor migration, labor solutions to the existing problems with the help of self- market, agglomeration process criterion, self- organization including diurnal labor commuting migration organization of monotown population. to the nearest towns with a more stable economic situation. This accounts for the initial reason for agglomeration processes in regions with a large number 1 Introduction of monotowns. Experimental models of the rank distribution of towns in a system (region) and evolution In this paper, we discuss the problems of criteria of such systems from basic ones to agglomerations are explored in order to assess the monotown population using as an example several intensity of agglomeration processes in the systems of monotowns located in Siberia (Russia). In 2014 the towns in the Middle and Southern Urals (the Sverdlovsk Government of the Russian Federation issued two and Chelyabinsk regions of Russia). -

Housing Russia

Housing Russia Danske Bank Markets – Russia Seminar Teemu Helppolainen | St. Petersburg March 12, 2014 YIT operations in 7 countries CEE = Baltic countries and Russia 92% Central Eastern Europe (Estonia, Latvia, Lithuania, (900,000) The Czech Republic, Slovakia) Finland 66% (1,215) Finland 57 % (3,515) Russia 27% Russia 32% (497) (1,968) CEE 5% (45,900) CEE 7% CEE 11% (689) (124) Finland 3% (26,200) Revenue (EUR million) Residential market size Personnel in 2013 in 2013 (commissioned) in 2013 YIT | 2 | Housing Russia YIT’s key figures EUR million 10–12/13 10–12/12 Change 1–12/13 1–12/12 Change • Revenue 521 555 -6% 1,859 1,959 -5% • Operating profit 41.2 68.0 -39% 152.8 201.1 -24% % of revenue 7.9 12.2 - 8.2 10.3 - • Operating profit, excluding non-recurring items* 42.4 68.0 -38% 154.0 194.1 -21% % of revenue, excluding non-recurring items* 8.1 12.2 - 8.3 9.9 - • Order backlog 2,714 2,765 -2% 2,714 2,765 -2% • Profit before taxes 32.5 59.1 -45% 122.8 169.6 -28% • Profit for the review period1) 24.3 43.8 -45% 93.9 130.7 -28% • Earnings per share, EUR 0.19 0.35 -46% 0.75 1.04 -28% • Operating cash flow after investments 76.3 8.0 - -87.9 49.9 - • Cash at the end of the period 76.3 74.9 2% 76.3 74.9 2% • Personnel at the end of the period 6,172 6,691 -8% 6,172 6,691 -8% • Dividend, EUR* 0.38 n/a 1) Attributable to equity holders of the parent company Note: A EUR 10.0 million cost provision covering costs related to the ammonia case in St. -

International Winter Schools in Russia

International winter schools in Russia COUNTRY OVERVIEW Geography Russia spans from the eastern plains of Europe to the Pacific Ocean in Asia, making it the largest country in the world. The coasts of Russia are washed by 12 seas and three oceans. There is hardly any country in the world where such a variety of scenery and vegetation can be found: steppes in the south, plains and forests in the midlands, tundra and taiga in the north, highlands and deserts in the east. There are 11 time zones in Russia, which is more than in any other country in the world. Climate Due to its vast territory, Russia is a country of natural contrasts. The northern part of the country is located in arctic and subarctic climate zones, while the southern regions have a subtropical climate. Normally Moscow, St. Petersburg and Kazan have very warm summers and fairly cold winters, while Tomsk in Siberia often has temperatures of -40 C or colder in winter. Culture Despite its vast area the population is 146 million people, less than the United States, Brazil or Pakistan. However, it is extremely diverse culturally. There are about 185 ethnic groups, whereas Slavs (the first inhabitants of Russia, Ukraine and Belarus) comprise the major ethnicity. Russian is the only official language across the country, but there are more than 25 different languages that are considered official in certain regions. Economy Russia is the biggest gas and second biggest oil exporter in the world and also has vast stocks of precious metals. Other important sectors include information technology, defense, agriculture and aerospace. -

Subject of the Russian Federation)

How to use the Atlas The Atlas has two map sections The Main Section shows the location of Russia’s intact forest landscapes. The Thematic Section shows their tree species composition in two different ways. The legend is placed at the beginning of each set of maps. If you are looking for an area near a town or village Go to the Index on page 153 and find the alphabetical list of settlements by English name. The Cyrillic name is also given along with the map page number and coordinates (latitude and longitude) where it can be found. Capitals of regions and districts (raiony) are listed along with many other settlements, but only in the vicinity of intact forest landscapes. The reader should not expect to see a city like Moscow listed. Villages that are insufficiently known or very small are not listed and appear on the map only as nameless dots. If you are looking for an administrative region Go to the Index on page 185 and find the list of administrative regions. The numbers refer to the map on the inside back cover. Having found the region on this map, the reader will know which index map to use to search further. If you are looking for the big picture Go to the overview map on page 35. This map shows all of Russia’s Intact Forest Landscapes, along with the borders and Roman numerals of the five index maps. If you are looking for a certain part of Russia Find the appropriate index map. These show the borders of the detailed maps for different parts of the country.