Cebridge Telecom Wv, Llc, Cequel Communications

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

West Virginia Broadband Enhance Council 2020 Annual Report

2020 West Virginia Broadband Enhancement Council 2020 ANNUAL REPORT TO THE WEST VIRGINIA LEGISLATURE Table of Contents 1. Executive Summary ............................................................................................................................... 1 2. Existing, Continuing and New Initiatives ............................................................................................... 2 3. Broadband Mapping ............................................................................................................................. 4 Key Components of the Interactive Mapping System .................................................................. 4 Broadband Advertised Speed Ranges Interactive Map ................................................................ 5 Broadband Development Hub ...................................................................................................... 6 Public Wi-Fi Map ........................................................................................................................... 6 Public Project Development ......................................................................................................... 7 Speed Tiers by County ................................................................................................................... 8 Speed Tiers Statewide ................................................................................................................... 8 Providers Statewide ..................................................................................................................... -

Filing Date (Enter W/Leading '): Holding Company: Filing Name

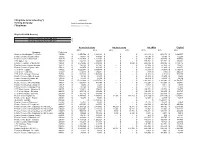

Filing Date (enter w/leading '): 6/16/2016 Holding Company: Frontier Communication Corporation Filing Name: 2016 Annual Access Tariff Filing Eligible ARC/ARM Recovery Holding Company Total CAF 2015 $ - Holding Company Total CAF 2016 $ - Access Reductions Net Recip Comp Net CMRS Eligible Recovery 2015 2016 2015 2016 2015 2016 2015 Company Study Area Southern New England Telephone 135200 $ 3,470,704 $ 5,129,118 $ - $ - $ 963,173 $ 963,173 $ 2,640,557 Frontier Comm.-Ausable Valley 150072 $ 140,671 $ 149,693 $ - $ - $ 48,580 $ 48,580 $ 112,208 Frontier Comm. of New York 150100 $ 1,092,747 $ 1,222,856 $ - $ - $ 197,979 $ 197,979 $ 777,798 CTC Ogden, Inc. 150110 $ 164,138 $ 204,606 $ - $ - $ 171,761 $ 171,761 $ 200,361 Frontier Telephone of Rochester 150121 $ 4,579,345 $ 5,189,398 $ - $ 8,692 $ 209,782 $ 209,782 $ 3,182,115 Frontier Comm.-Seneca Gorham 150122 $ 138,265 $ 151,362 $ - $ - $ 57,330 $ 57,330 $ 116,517 Frontier Comm. of Sylvan Lake 150128 $ 168,479 $ 188,115 $ - $ - $ 62,413 $ 62,413 $ 138,872 CTC of NY - Upstate 154532 $ 8,625,581 $ 9,164,844 $ - $ - $ (15,938) $ (15,938) $ 5,193,815 CTC of NY - Red Hook 154533 $ 541,863 $ 582,041 $ - $ - $ (798) $ (798) $ 320,578 CTC of NY - Western Counties 154534 $ 997,239 $ 1,003,080 $ - $ - $ (1,329) $ (1,329) $ 589,275 Frontier Comm. of Breezewood 170149 $ 32,126 $ 41,239 $ - $ - $ 21,410 $ 21,410 $ 31,488 Frontier Comm. of Canton, Inc. 170152 $ 37,533 $ 45,799 $ - $ - $ 28,669 $ 28,669 $ 38,760 Commonwealth of PA 170161 $ 17,612,066 $ 19,273,782 $ - $ - $ 2,346,892 $ 2,346,892 $ 13,706,537 Frontier Comm. -

Frontier Communications Corp

Exhibit RWS-3 Page 1 of 114 FRONTIER COMMUNICATIONS CORP FORM 10-K (Annual Report) Filed 02/27/14 for the Period Ending 12/31/13 Address HIGH RIDGE PK BLDG 3 STAMFORD, CT 06905 Telephone 2036145600 CIK 0000020520 Symbol FTR SIC Code 4813 - Telephone Communications, Except Radiotelephone Industry Communications Services Sector Services Fiscal Year 12/31 http://www.edgar-online.com © Copyright 2014, EDGAR Online, Inc. All Rights Reserved. Distribution and use of this document restricted under EDGAR Online, Inc. Terms of Use. Exhibit RWS-3 Page 2 of 114 FRONTIER COMMUNICATIONS CORPORATION FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE YEAR ENDED DECEMBER 31, 2013 Exhibit RWS-3 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Page 3 of 114 WASHINGTON, D.C. 20549 FORM 10-K (Mark one) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2013 OR TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from _________ to ___________ Commission file number 001-11001 FRONTIER COMMUNICATIONS CORPORATION (Exact name of registrant as specified in its charter) Delaware 06-0619596 (State or other jurisdiction of (I.R.S. Employer Identification No.) incorporation or organization) 3 High Ridge Park Stamford, Connecticut 06905 (Address of principal executive offices) (Zip Code) Registrant's telephone number, including area code: (203) 614-5600 Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Common Stock, par value $.25 per share The NASDAQ Stock Market LLC Series A Participating Preferred Stock Purchase Rights The NASDAQ Stock Market LLC Securities registered pursuant to Section 12(g) of the Act: NONE Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. -

Before the CALIFORNIA PUBLIC UTILITIES COMMISSION

Before the CALIFORNIA PUBLIC UTILITIES COMMISSION In the Matter of the Joint Application of Frontier Communications Corporation, Frontier Communications of America, Inc. (U5429C), Verizon California, Inc. (U1002C), Verizon Long Application 15-03-005 Distance LLC (U5732C), and Newco West Holdings LLC for Approval of Transfer of Control Over Verizon California, Inc. and Related Approval of Transfer of Assets and Certifications. Reply Testimony of LEE L. SELWYN on behalf of the Office of Ratepayer Advocates of the California Public Utilities Commission July 28, 2015 REDACTED – FOR PUBLIC INSPECTION REPLY TESTIMONY OF LEE L. SELWYN TABLE OF CONTENTS EXECUTIVE SUMMARY v I. INTRODUCTION AND SUMMARY 1 Qualifications, background and experience 1 Assignment 4 Summary and Recommendation 5 II. GENERAL DESCRIPTION OF THE TRANSACTION AND SHAREHOLDER IMPACTS 13 A brief history of Verizon 15 A brief history of Frontier 20 The transaction 25 III. THE FINANCIAL ASPECTS OF “PROJECT GUAVA” – THE CA/TX/FL ACQUISITION 27 The transaction’s effect upon utility shareholders 27 The issuance of additional Frontier stock to finance the transaction. 31 Even under the worst case scenario that was considered by Frontier where none of the anticipated cost savings materialize, the transaction appears to have been reasonably priced on an Enterprise Value/EBITDA basis. 36 Frontier’s evaluation of the deal conservatively contemplates continued subscriber losses in the legacy wireline business. 37 Even under what Frontier considers to be its “worst case” conditions, the transaction appears to be at least fair, if not beneficial, to Frontier shareholders. 39 i ECONOMICS AND REDACTED – FOR PUBLIC INSPECTION TECHNOLOGY, INC. TABLE OF CONTENTS (continued) IV. -

Filing Date (Enter W/Leading '): Holding Company: Filing Name

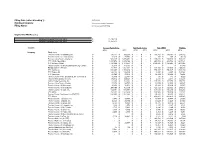

Filing Date (enter w/leading '): 6/17/2013 Holding Company: Frontier Communication Corporation Filing Name: 2013 Annual Access Tariff Filing Eligible ARC/ARM Recovery Holding Company Total CAF 2012 $ 11,710,119 Holding Company Total CAF 2013 $ 14,464,517 7/2/2013 Access Reductions Net Recip Comp Net CMRS Eligible Recovery 2012 2013 2012 2013 2012 2013 2012 Company Study Area Frontier Comm. of Alabama, Inc. $ 175,147 $ 350,293 $ - $ - $ 149,707 $ 149,707 $ 263,132 Frontier Comm. of Lamar County $ 12,645 $ 71,748 $ - $ - $ 259 $ 259 $ (5,129) Frontier of the South - Alabama $ 538,225 $ 1,076,452 $ - $ - $ 160,816 $ 160,816 $ 566,223 CTC White Mountains $ 1,837,072 $ 3,674,144 $ - $ - $ 245,794 $ 245,794 $ 1,687,121 CTC Mohave (Rural) $ 1,186,629 $ 2,373,257 $ - $ - $ 1,199,895 $ 1,199,895 $ 1,933,085 Frontier Comm. of the Southwest, Inc (AZ-Contel) $ 75,778 $ 151,555 $ - $ - $ - $ - $ 61,380 Navajo Comm - Arizona $ 781,431 $ 1,562,862 $ - $ - $ 194,880 $ 194,880 $ 790,959 CTC California $ 684,005 $ 1,368,010 $ - $ - $ 750,847 $ 750,847 $ 1,162,230 CTC Golden St $ 143,192 $ 286,385 $ - $ - $ 8,657 $ 8,657 $ 123,062 CTC Tuolomne $ 42,506 $ 85,013 $ - $ - $ 54,299 $ 54,299 $ 78,464 Frontier Comm of the Southwest, Inc (CA-Contel) $ 11,330 $ 22,661 $ - $ - $ 175 $ 175 $ 9,320 Frontier West Coast, Inc (CA) $ 139,972 $ 459,326 $ - $ - $ 2,344 $ 2,344 $ 115,276 Global Valley Networks, Inc. $ 81,696 $ 163,392 $ - $ - $ 107,379 $ 107,379 $ 153,151 Frontier of the South - Florida $ 27,376 $ 54,751 $ - $ - $ 32,535 $ 32,535 $ 48,527 Frontier Comm. -

COSA Code Table December 2013 Page 1 of 4 AT&T Inc. Verizon

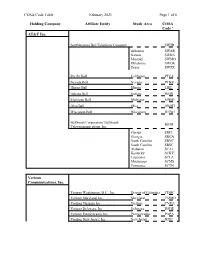

COSA Code Table December 2013 Page 1 of 4 AT&T Inc. Southwestern Bell SWTR Telephone Company Pacific Telesis Group PTTR Pacific Bell California PTCA Nevada Bell Nevada PTNV Southern New England Telecommunications Corp. Southern New England Telephone Connecticut SNCT Ameritech Corporation AMTR Illinois Bell Illinois LBIL Indiana Bell Indiana NBIN Michigan Bell Michigan MBMI Ohio Bell Ohio OBOH Wisconsin Bell Wisconsin WTWI BellSouth Corporation BellSouth Telecommunications, Inc. BSTR Verizon Communications, Inc. Verizon Bell Atlantic BNTR Verizon Washington, D.C., Inc. District of Columbia CDDC Verizon Maryland, Inc. Maryland CMMD Verizon Virginia, Inc. Virginia CVVA Verizon Delaware, Inc. Delaware DSDE Verizon Pennsylvania, Inc. Pennsylvania PAPA Verizon New Jersey, Inc. New Jersey NJNJ Verizon New England NETC Verizon New York Telephone New York NYNY Verizon GTE GTTC Verizon California California GTGC Verizon Florida Florida GTFL Verizon Communications, Inc. (Cont’d.) COSA Code Table December 2013 Page 2 of 4 Verizon North GTMW Verizon South GTSO GTE Southwest dba Verizon Southwest GTSW Total Large ILECs TBOC America Movil Telecommunications of Puerto Rico PRTC Puerto Rico Telephone Company PRPR Puerto Rico PRSA Puerto Rico Central PRCC Cincinnati Bell, Inc. Cincinnati Bell Telephone CBTC Ohio CBOH Kentucky CBKY Frontier Communications Corp. Citizens Companies CTTC Citizens Telecom. Co. of New York CTNY Upstate New York CTUP Red Hook New York CTRH Western Counties New York CTWC Frontier Companies RTTC Rochester Telephone Corp. New York RTNY Commonwealth Telephone Enterprises, Inc. Commonwealth Telephone Co. Pennsylvania CWTC Verizon Companies FVTC Frontier Communications of the Carolinas FVSO Frontier North Inc. FVNO Frontier West Virginia Inc. FVWV Frontier Communications of the Northwest Inc. -

PUBLIC SERVICE COMMISSION of WEST VIRGINIA CHARLESTON At

PUBLIC SERVICE COMMISSION OF WEST VIRGINIA CHARLESTON At a session of the PUBLIC SERVICE COMMISSION OF WEST VIRGINIA in the City of Charleston on the 7" day of January 2015. GENERAL ORDER NO. 187.44 In the matter of proposed amendments to the Rules and Regulations for the Government of Telephone Utilities, 150 C.S.R. Series 6. COMMISSION ORDER The Commission promulgates a proposed amendment to Rule 2.6 of the Rules and Regulations for the Government of Telephone Utilities, 150 C.S.R. Series 6 (Telephone m)for comment. BACKGROUND On September 11, 2013, the Commission opened a general investigation into the continuing need for local exchange carriers (LECs) to annually distribute printed telephone directories to customers as required under Teleuhone Rule 2.6.a. The Commission opened that proceeding after a request from Frontier West Virginia Inc., and Citizens Telecommunications Company of West Virginia dba Frontier Communications of West Virginia (together Frontier) seeking Commission consent for an opt-in directory distribution program. Instead of proceeding with the Frontier request, the Commission invited interested parties to submit comments and directed the Executive Secretary to publish notice of this matter statewide. The Executive Secretary also provided notice to all incumbent and competitive carriers of this proceeding. Beginning on September 23, 2013, the Commission began receiving letters from the public regarding the Frontier proposal. The letters, often from senior citizens, stated that they continue to use printed telephone directories and argued for ongoing directory printing and distribution. One customer, however, wrote in support of ending the requirement to distribute printed directories, concluding that eliminating the requirement will reduce waste and cut costs. -

P.S.C.-W.Va.-No. 217 Frontier West Virginia Inc. Original Title Page

P.S.C.-W.Va.-No. 217 Cancels P.S.C. – W.Va. – No. 217 of Verizon West Virginia Inc. Frontier West Virginia Inc. Original Title Page ACCESS SERVICE TARIFF Containing Regulations, Rates and Charges applying to the provision of Access Services within a Local Access and Transport Area (LATA) for connection to intrastate communications facilities for customers in the State of West Virginia by Frontier West Virginia Inc. The name Verizon West Virginia Inc. and Bell Atlantic – West Virginia, Inc. have been changed to Frontier West Virginia Inc. All references throughout this Tariff to Verizon West Virginia Inc. and Bell Atlantic – West Virginia, Inc., “the telephone company” or “the company” shall be read as Frontier West Virginia Inc. Issued by authority of an Order of the Public Service Commission of West Virginia in Case No. 09-0871-T-PC Dated May 13, 2010. Issued: July 1, 2010…… Effective: July 1, 2010 ACCESS SERVICE TARIFF P.S.C.-W.Va.-No. 217 Frontier West Virginia Inc. Contents Original Page 1 TABLE OF CONTENTS Section Page APPLICATION OF TARIFF 1 A. General 1 B. Regulations .................................................... 1 1. Explanation of Symbols ..................................... 1 2. Explanation of Abbreviations ............................... 1 3. Provision of Services ...................................... 3 4. Regulations, Rates and Charges Contained Herein ............ 3 5. Reference to Other Tariffs ................................. 3 GENERAL REGULATIONS 2 2.1 Undertaking of the Telephone Company ........................... 1 2.1.1 Scope.................................................. 1 2.1.2 Limitations............................................ 1 2.1.3 Liability.............................................. 2 2.1.4 Provision of Services.................................. 4 2.1.5 Installation and Termination of Services............... 5 2.1.6 Maintenance of Services............................... -

June 17,2019 Electronic Service Only Joshua A. Johnson, Esq. Counsel

201 Brooks Street, P.O. Box 812 Phone: (304) 340-0300 Charleston, West Virginia 25323 Fax: (304) 340-0325 June 17,2019 Electronic Service Only Joshua A. Johnson, Esq. Counsel, Frontier Communications Frontier West Virginia Inc. 1500 MacCorkle Ave., S.E. Charleston, WV 25396 RE: Case No. 19-0502-T-PC Citizens Telecommunications of West Virginia dba Frontier Communications of West Virginia and Frontier West Virginia Inc. Dear Mr. Johnson: The Staff Memorandum issued today was served via email on the above-listed parties. Any responses must be submitted to the Executive Secretary’s Office in writing within 10 days of this date, unless directed otherwise. You will not receive a copy of the Staff Memorandum by regular mail. Your failure to respond in writing to the utility’s answer, Staffs recommendations, or other documents may result in a decision in your case based on your original filing and the other documents in the case file, without further hearing or notice. When you provide an email address, you will automatically receive electronic docket notifications as documents are filed in this proceeding. The email notifications allow recipients to view a document within an hour from the time the filing is processed. Please note - the Public Service Commission does not accept electronic filings. Sincerely, IF/tg Ingrid Fdell, Director Enc. - Memo Executive Secretary Division FINAL JOINT STAFF MEMORANDUM TO: INGRID FERRELL DATE: June 17,2019 Executive Secretary FROM: LISA L. WANSLEY Staff Attorney RE: 19-0502-T-PC CITIZENS TELECOMMUNICATIONS OF WEST VIRGINIA INC. DBA FRONTIER COMMUNICATIONS OF WEST VIRGINIA AND FRONTIER WEST VIRGINIA INC. -

Annual Statistical Report for 2017

ANNUAL STATISTICAL REPORT Statistical Data on Public Utilities in West Virginia Source: Annual Reports Submitted To The Public Service Commission Of West Virginia ______________________________ Condition at the Close of Year Ended December 31, 2017 or as Otherwise Noted Compiled by: Kathryn Stalnaker, Executive Secretary Division Annual Reports Section – 11/15/2018 WEST VIRGINIA PUBLIC SERVICE COMMISSION 2017 ANNUAL REPORT STATISTICS FISCAL YEAR 07/01/16 - 06/30/17 CALENDAR YEAR 01/01/17 - 12/31/17 NAME AND PRINCIPAL OFFICE OF CORPORATE AND INDIVIDUAL UTILITIES UNDER THE JURISDICTION OF THE PUBLIC SERVICE COMMISSION OF WEST VIRGINIA YEAR ENDED DECEMBER 31, 2017 TABLE OF CONTENTS Page Number List of Utilities ............................................................................................5 – 25 Utilities Summary ............................................................................................26 - - - - - - - - - - - - - - - - - - -- - - - Type of Utilities - - - - - - - - - - - - - - - - - - - - - - - - Telephone Companies ....................................................................... 27 - 29 Electric Companies ............................................................................ 30 - 36 Gas Companies .................................................................................. 37- 39 Water Utilities: Privately Owned ...................................................................................40 Publicly Owned - Municipals ......................................................... 41 - 45 -

COSA Code Table February 2021 Page 1 of 6 Holding Company

COSA Code Table February 2021 Page 1 of 6 Holding Company Affiliate Entity Study Area COSA Code 1 AT&T Inc. Southwestern Bell Telephone Company SWTR Arkansas SWAR Kansas SWKS Missouri SWMO Oklahoma SWOK Texas SWTX Pacific Bell California PTCA Nevada Bell Nevada PTNV Illinois Bell Illinois LBIL Indiana Bell Indiana NBIN Michigan Bell Michigan MBMI Ohio Bell Ohio OBOH Wisconsin Bell Wisconsin WTWI BellSouth Corporation/ BellSouth BSTR Telecommunications, Inc. Florida SBFL Georgia SBGA North Carolina SBNC South Carolina SBSC Alabama SCAL Kentucky SCKY Louisiana SCLA Mississippi SCMS Tennessee SCTN Verizon Communications, Inc. Verizon Washington, D.C., Inc. District of Columbia CDDC Verizon Maryland, Inc. Maryland CMMD Verizon Virginia, Inc. Virginia CVVA Verizon Delaware, Inc. Delaware DSDE Verizon Pennsylvania, Inc. Pennsylvania PAPA Verizon New Jersey, Inc. New Jersey NJNJ COSA Code Table February 2021 Page 2 of 6 Holding Company Affiliate Entity Study Area COSA Code 1 Verizon Communications, Inc. (Cont’d.) Verizon New England NETC Massachusetts NEMA Rhode Island NERI Verizon New York Telephone New York NYNY Verizon North GTMW Pennsylvania GTPA Contel Pennsylvania COPA Contel Quaker State COQS General Offices GTGO Verizon South GTSO Virginia GTVA Contel Virginia COVA America Movil/ Telecommunications of Puerto Rico Puerto Rico Telephone Company PRPR Puerto Rico PRSA Puerto Rico Central PRCC Cincinnati Bell, Inc. Cincinnati Bell Telephone CBTC Ohio CBOH Kentucky CBKY COSA Code Table February 2021 Page 3 of 6 Holding Company Affiliate Entity Study Area COSA Code 1 Frontier Communications Corp. Citizens Telecom. Co. of New York CTNY Upstate New York CTUP Red Hook New York CTRH Western Counties New York CTWC Rochester Telephone Corp. -

The Law Office of Vincent Trivelli, PLLC

The Law Office of Vincent Trivelli, PLLC 178 Chancery Row Morgantown, West Virginia 26505 Phone (304) 291-5223 Toll Free 1-866-266-5948 November 16,2009 Fax (304) 291-2240 E-mail: [email protected] (Via Hand Delivery) Ms. Sandra Squire, Executive Secretary Public Service Commission of West Virginia P. 0. Box 812 201 Brooks Street Charleston, WV 25323 RE: Citizens Telecommunications Company of West Virginia, dba Frontier Communications of West Virginia and Verizon West Virginia, Inc. Case No.09-0871-T-PC Dear Ms. Squire: Enclosed for filing in the above-styled and numbered case, please find the original and twelve (12) copies of the following: 1. Public (Redacted) Version of the Direct Testimony of Randy Barber on Behalf of the Communications Workers of America, AFL-CIO; 3. Public (Redacted) Version of the Direct Testimony of Susan M. Baldwin on Behalf of the Communications Workers of America, AFL-CIO; and 2. Direct Testimony of John Pusloskie on Behalf of the Communications Workers of America, AFL-CIO. Copies have been served this date upon the parties of record via U. S. mail as indicated by the Certificates of Service. Also enclosed is one copy each of the PROPRIETARY VERSIONS of the Direct Testimony of Randy Barber on Behalf of the Communications Workers of America, AFL- CIO and Direct Testimony of Susan M. Baldwin on Behalf of the Communications Workers of America, AFL-CIO which are being filed under seal in this case. Copies of these Proprietary versions will be sent to parties of record who have executed a Protective Agreement in this matter.