Before the CALIFORNIA PUBLIC UTILITIES COMMISSION

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

West Virginia Broadband Enhance Council 2020 Annual Report

2020 West Virginia Broadband Enhancement Council 2020 ANNUAL REPORT TO THE WEST VIRGINIA LEGISLATURE Table of Contents 1. Executive Summary ............................................................................................................................... 1 2. Existing, Continuing and New Initiatives ............................................................................................... 2 3. Broadband Mapping ............................................................................................................................. 4 Key Components of the Interactive Mapping System .................................................................. 4 Broadband Advertised Speed Ranges Interactive Map ................................................................ 5 Broadband Development Hub ...................................................................................................... 6 Public Wi-Fi Map ........................................................................................................................... 6 Public Project Development ......................................................................................................... 7 Speed Tiers by County ................................................................................................................... 8 Speed Tiers Statewide ................................................................................................................... 8 Providers Statewide ..................................................................................................................... -

Brief of Amici Curiae of Access Now, Et Al. Case Nos. 2:18-Cv-02684, 2:18-Cv-02660 | I Case 2:18-Cv-02684-JAM-DB Document 68 Filed 09/30/20 Page 2 of 22

Case 2:18-cv-02684-JAM-DB Document 68 Filed 09/30/20 Page 1 of 22 1 Thomas H. Vidal (State Bar No. 204432) [email protected] 2 Benjamin S. Akley (State Bar No. 278506) [email protected] 3 PRYOR CASHMAN LLP 1801 Century Park East, 24th Floor 4 Los Angeles, California 90067-2302 Phone: (310) 556-9608 5 Fax: (310) 556-9670 6 Attorneys for Amici Curiae Access Now, Mozilla Corp, Public Knowledge, 7 New America's Open Technology Institute, and Free Press 8 9 UNITED STATES DISTRICT COURT 10 EASTERN DISTRICT OF CALIFORNIA 11 AMERICAN CABLE ASSOCIATION, CTIA Case No.: 2:18-cv-02684 12 THE WIRELESS ASSOCATION, NCTA – Case No.: 2:18-cv-02660 13 THE INTERNET & TELEVISION ASSOCIATION, and USTELECOM –THE BRIEF OF ACCESS NOW, MOZILLA 14 BROADBAND ASSOCIATION, CORP, PUBLIC KNOWLEDGE, NEW AMERICA'S OPEN TECHNOLOGY 15 Plaintiffs, INSTITUTE, AND FREE PRESS AS 16 AMICUS CURIAE IN OPPOSITION TO v. PLAINTIFFS’ RENEWED MOTIONS 17 FOR PRELIMINARY INJUNCTIONS XAVIER BECERRA, in his official capacity as 18 Attorney General of California, Judge: Hon. John A. Mendez 19 Defendant. 20 THE UNITED STATES OF AMERICA, 21 22 Plaintiff, 23 v. 24 THE STATE OF CALIFORNIA; GAVIN C. 25 NEWSOM, Governor of California, in his Official Capacity, and XAVIER BECERRA, 26 Attorney General of California, in his Official 27 Capacity, 28 Defendants. Brief of Amici Curiae of Access Now, et al. Case Nos. 2:18-cv-02684, 2:18-cv-02660 | i Case 2:18-cv-02684-JAM-DB Document 68 Filed 09/30/20 Page 2 of 22 1 TABLE OF CONTENTS 2 3 I. -

REPORT ABOUT FRONTIER Collection of Facts

10/28/2020 REPORT ABOUT FRONTIER Collection of Facts CALIFORNIA PUBLIC UTILITIES COMMISSION COMMUNICATIONS DIVISION REPORT ABOUT FRONTIER 10/28/2020 Contents Surcharge Reporting and Remittances for Public Purpose Programs................................................................................. 2 Payment of Fines related to General Order 133-D ............................................................................................................. 2 Payment of Annual Fees as a Video Franchise Holder ........................................................................................................ 2 Order Instituting Investigation 14-05-012 related to Intrastate Rural Call Completion ..................................................... 2 Order Instituting Investigation 19-12-009 related to Frontier’s Outages ........................................................................... 2 Complaints Received by the CPUC’s Consumer Affairs Branch .......................................................................................... 3 Complaint Category: Billing ............................................................................................................................................. 3 Complaint Category: Related to Internet or VoIP services ............................................................................................. 4 Complaint Category: Service ........................................................................................................................................... 4 -

Filing Date (Enter W/Leading '): Holding Company: Filing Name

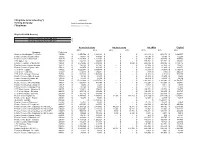

Filing Date (enter w/leading '): 6/16/2016 Holding Company: Frontier Communication Corporation Filing Name: 2016 Annual Access Tariff Filing Eligible ARC/ARM Recovery Holding Company Total CAF 2015 $ - Holding Company Total CAF 2016 $ - Access Reductions Net Recip Comp Net CMRS Eligible Recovery 2015 2016 2015 2016 2015 2016 2015 Company Study Area Southern New England Telephone 135200 $ 3,470,704 $ 5,129,118 $ - $ - $ 963,173 $ 963,173 $ 2,640,557 Frontier Comm.-Ausable Valley 150072 $ 140,671 $ 149,693 $ - $ - $ 48,580 $ 48,580 $ 112,208 Frontier Comm. of New York 150100 $ 1,092,747 $ 1,222,856 $ - $ - $ 197,979 $ 197,979 $ 777,798 CTC Ogden, Inc. 150110 $ 164,138 $ 204,606 $ - $ - $ 171,761 $ 171,761 $ 200,361 Frontier Telephone of Rochester 150121 $ 4,579,345 $ 5,189,398 $ - $ 8,692 $ 209,782 $ 209,782 $ 3,182,115 Frontier Comm.-Seneca Gorham 150122 $ 138,265 $ 151,362 $ - $ - $ 57,330 $ 57,330 $ 116,517 Frontier Comm. of Sylvan Lake 150128 $ 168,479 $ 188,115 $ - $ - $ 62,413 $ 62,413 $ 138,872 CTC of NY - Upstate 154532 $ 8,625,581 $ 9,164,844 $ - $ - $ (15,938) $ (15,938) $ 5,193,815 CTC of NY - Red Hook 154533 $ 541,863 $ 582,041 $ - $ - $ (798) $ (798) $ 320,578 CTC of NY - Western Counties 154534 $ 997,239 $ 1,003,080 $ - $ - $ (1,329) $ (1,329) $ 589,275 Frontier Comm. of Breezewood 170149 $ 32,126 $ 41,239 $ - $ - $ 21,410 $ 21,410 $ 31,488 Frontier Comm. of Canton, Inc. 170152 $ 37,533 $ 45,799 $ - $ - $ 28,669 $ 28,669 $ 38,760 Commonwealth of PA 170161 $ 17,612,066 $ 19,273,782 $ - $ - $ 2,346,892 $ 2,346,892 $ 13,706,537 Frontier Comm. -

Before the FEDERAL COMMUNICATIONS COMMISSION Washington, D.C. 20554 in the Matter of Frontier Communications Corporation, Transf

Before the FEDERAL COMMUNICATIONS COMMISSION Washington, D.C. 20554 In the Matter of ) ) Frontier Communications Corporation, ) Transferor ) ) and ) WC Docket No. 19-_____________ ) Northwest Fiber, LLC, ) IB File No. ITC-T/C-2019________ Transferee ) ) Application for Consent to Partially Assign ) and Transfer Control of Domestic and ) International Authorizations Pursuant to ) Section 214 of the Communications Act of ) 1934, As Amended, and Sections 63.04, 63.18 ) and 63.24 of the Commission’s Rules. ) CONSOLIDATED APPLICATION FOR THE PARTIAL ASSIGNMENT AND TRANSFER OF CONTROL OF DOMESTIC AND INTERNATIONAL SECTION 214 AUTHORIZATIONS Pursuant to Section 214 of the Communications Act of 1934, as amended (“the Act”),1 and Sections 63.04, 63.18 and 63.24 of the Commission’s rules,2 Frontier Communications Corporation (“Frontier” or “Transferor”) and Northwest Fiber, LLC (“Northwest Fiber” or “Transferee”) (collectively, the “Applicants”) request Commission consent to: (1) transfer control of certain domestic and international Section 214 authorizations held by Frontier’s wholly owned subsidiaries (i) Citizens Telecommunications Company of Idaho (“Frontier Idaho”), (ii) Citizens Telecommunications Company of Montana (“Frontier Montana”), 1 47 U.S.C. § 214. 2 47 C.F.R. §§ 63.04, 63.18 and 63.24. (iii) Citizens Telecommunications Company of Oregon (“Frontier Oregon”) and (iv) Frontier Communications Northwest Inc. (“Frontier Northwest”) ((i) through (iv) collectively, the “Transferring Companies”) from Frontier to Northwest Fiber; and (2) assign certain long distance customer relationships from Frontier Communications of America, Inc. (“Frontier America”) and Frontier Communications Online and Long Distance Inc. (“Frontier LD”) to Northwest Fiber. The transaction represents the sale to Northwest Fiber of Frontier’s entire operations across four states—Idaho, Montana, Oregon and Washington (collectively, the “Territory”). -

2018/034 – 2018 Listing of State Assessees

STATE OF CALIFORNIA SEN. GEORGE RUNNER (RET.) STATE BOARD OF EQUALIZATION First District, Lancaster PROPERTY TAX DEPARTMENT FIONA MA, CPA 450 N STREET, SACRAMENTO, CALIFORNIA Second District, San Francisco PO BOX 942879, SACRAMENTO, CALIFORNIA 94279-0061 JEROME E. HORTON 1-916-274-3270 FAX 1-916-285-0132 Third District, Los Angeles County www.boe.ca.gov DIANE L. HARKEY Fourth District, Orange County July 25, 2018 BETTY T. YEE State Controller _______ DEAN R. KINNEE Executive Director No. 2018/034 TO COUNTY ASSESSORS AND COUNTY AUDITOR–CONTROLLERS: LISTING OF STATE ASSESSEES Enclosed are two listings of 680 companies whose property is subject to ad valorem tax assessment by the Board of Equalization (Board) for the lien date 2018. The first list is alphabetical by assessee name. The second list is numerical by assessee SBE number. These listings are current as of July 24, 2018. The State-Assessed Properties Division groups the assessees numerically by industry as follows: Industry SBE No. Gas, Electric, Water and Gas Transmission 100 - 199 Local Exchange Telephone Companies 200 - 399 Pipeline Companies 400 - 499 Railcar Maintenance Facilities 500 - 699 Railroad Companies 800 - 899 Electric Generation Facilities 1100 - 1199 Long Distance Telephone Companies 2000 - 2499 Wireless Telephone Companies 2500 - 3999 Long Distance Telephone Companies 7500 - 8999 Wireless Telephone Companies D001 - D999 Electric Generation Facilities E001 - E999 Long Distance Telephone Companies P001 - P999 Long Distance Telephone Companies Q001 - Q999 Long Distance Telephone Companies R001 - R999 The property of these companies is subject to state assessment pursuant to section 19 of Article XIII of the California Constitution and sections 721 and 721.5 of the Revenue and Taxation Code. -

Frontier Communications Corp

Exhibit RWS-3 Page 1 of 114 FRONTIER COMMUNICATIONS CORP FORM 10-K (Annual Report) Filed 02/27/14 for the Period Ending 12/31/13 Address HIGH RIDGE PK BLDG 3 STAMFORD, CT 06905 Telephone 2036145600 CIK 0000020520 Symbol FTR SIC Code 4813 - Telephone Communications, Except Radiotelephone Industry Communications Services Sector Services Fiscal Year 12/31 http://www.edgar-online.com © Copyright 2014, EDGAR Online, Inc. All Rights Reserved. Distribution and use of this document restricted under EDGAR Online, Inc. Terms of Use. Exhibit RWS-3 Page 2 of 114 FRONTIER COMMUNICATIONS CORPORATION FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE YEAR ENDED DECEMBER 31, 2013 Exhibit RWS-3 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Page 3 of 114 WASHINGTON, D.C. 20549 FORM 10-K (Mark one) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2013 OR TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from _________ to ___________ Commission file number 001-11001 FRONTIER COMMUNICATIONS CORPORATION (Exact name of registrant as specified in its charter) Delaware 06-0619596 (State or other jurisdiction of (I.R.S. Employer Identification No.) incorporation or organization) 3 High Ridge Park Stamford, Connecticut 06905 (Address of principal executive offices) (Zip Code) Registrant's telephone number, including area code: (203) 614-5600 Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Common Stock, par value $.25 per share The NASDAQ Stock Market LLC Series A Participating Preferred Stock Purchase Rights The NASDAQ Stock Market LLC Securities registered pursuant to Section 12(g) of the Act: NONE Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. -

Public Notice

PUBLIC NOTICE Federal Communications Commission News Media Information 202 / 418-0500 445 12th St., S.W. Internet: http://www.fcc.gov Washington, D.C. 20554 TTY: 1-888-835-5322 Report Number: 15774 Date of Report: 03/24/2021 Wireless Telecommunications Bureau Site-By-Site Action Below is a listing of applications that have been acted upon by the Commission. AF - Aeronautical and Fixed File Number Action Date Call Sign Applicant Name Purpose Action 0009104979 03/19/2021 KAI7 Aviation Spectrum Resources Inc AM G 0009460053 03/19/2021 WRAW404 CAE Oxford Aviation Academy Phoenix CA G 0009371227 03/17/2021 WRMB754 Aviation Spectrum Resources Inc NE G 0009374627 03/17/2021 WRMB755 Aviation Spectrum Resources Inc NE G 0009374630 03/17/2021 WRMB756 Aviation Spectrum Resources Inc NE G 0009374644 03/17/2021 WRMB757 Aviation Spectrum Resources Inc NE G 0009447170 03/18/2021 SUN 'n FUN Fly-In, Inc. NE D 0009376660 03/17/2021 WQNK780 Aviation Spectrum Resources Inc RM G 0009376662 03/17/2021 WQNM373 Aviation Spectrum Resources Inc RM G 0009376663 03/17/2021 WQNK782 Aviation Spectrum Resources Inc RM G 0009447153 03/19/2021 WQEV848 Textron Aviation, Inc. RM G 0009358046 03/17/2021 Aviation Spectrum Resources Inc WD W Page 1 AR - Aviation Radionavigation File Number Action Date Call Sign Applicant Name Purpose Action 0009315345 03/18/2021 WQOR529 The Boeing Company AM G AS - Aural Studio Transmitter Link File Number Action Date Call Sign Applicant Name Purpose Action 0009318964 03/18/2021 WQTJ537 EAGLE COMMUNICATIONS, INC. MD G 0009318979 03/18/2021 WLG829 EAGLE COMMUNICATIONS, INC. -

Filing Date (Enter W/Leading '): Holding Company: Filing Name

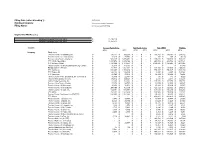

Filing Date (enter w/leading '): 6/17/2013 Holding Company: Frontier Communication Corporation Filing Name: 2013 Annual Access Tariff Filing Eligible ARC/ARM Recovery Holding Company Total CAF 2012 $ 11,710,119 Holding Company Total CAF 2013 $ 14,464,517 7/2/2013 Access Reductions Net Recip Comp Net CMRS Eligible Recovery 2012 2013 2012 2013 2012 2013 2012 Company Study Area Frontier Comm. of Alabama, Inc. $ 175,147 $ 350,293 $ - $ - $ 149,707 $ 149,707 $ 263,132 Frontier Comm. of Lamar County $ 12,645 $ 71,748 $ - $ - $ 259 $ 259 $ (5,129) Frontier of the South - Alabama $ 538,225 $ 1,076,452 $ - $ - $ 160,816 $ 160,816 $ 566,223 CTC White Mountains $ 1,837,072 $ 3,674,144 $ - $ - $ 245,794 $ 245,794 $ 1,687,121 CTC Mohave (Rural) $ 1,186,629 $ 2,373,257 $ - $ - $ 1,199,895 $ 1,199,895 $ 1,933,085 Frontier Comm. of the Southwest, Inc (AZ-Contel) $ 75,778 $ 151,555 $ - $ - $ - $ - $ 61,380 Navajo Comm - Arizona $ 781,431 $ 1,562,862 $ - $ - $ 194,880 $ 194,880 $ 790,959 CTC California $ 684,005 $ 1,368,010 $ - $ - $ 750,847 $ 750,847 $ 1,162,230 CTC Golden St $ 143,192 $ 286,385 $ - $ - $ 8,657 $ 8,657 $ 123,062 CTC Tuolomne $ 42,506 $ 85,013 $ - $ - $ 54,299 $ 54,299 $ 78,464 Frontier Comm of the Southwest, Inc (CA-Contel) $ 11,330 $ 22,661 $ - $ - $ 175 $ 175 $ 9,320 Frontier West Coast, Inc (CA) $ 139,972 $ 459,326 $ - $ - $ 2,344 $ 2,344 $ 115,276 Global Valley Networks, Inc. $ 81,696 $ 163,392 $ - $ - $ 107,379 $ 107,379 $ 153,151 Frontier of the South - Florida $ 27,376 $ 54,751 $ - $ - $ 32,535 $ 32,535 $ 48,527 Frontier Comm. -

FCC Access Tariff

MCC Telephony, LLC FCC Tariff No. 1 3rd Revised Title Page Cancels 2nd Revised Title Page ACCESS SERVICES This tariff sets forth the service descriptions, regulations and rates applicable to the provision of telecommunications access service within the operating territories of MCC Telephony, LLC and its subsidiary companies: MCC Telephony of Florida, LLC MCC Telephony of Georgia, LLC MCC Telephony of Iowa, LLC MCC Telephony of the Mid-Atlantic, LLC MCC Telephony of the Midwest, LLC MCC Telephony of Minnesota, LLC MCC Telephony of Missouri, LLC MCC Telephony of the South, LLC MCC Telephony of the West, LLC Mediacom Telephony of Illinois, LLC __________________________ Original tariff effective May 18, 2010 Issued: July 15, 2014 Effective: July 16, 2014 Transmittal No. 8 Mr. Dan Templin, President One Mediacom Way, Mediacom Park, NY 10918 MCC Telephony, LLC FCC Tariff No. 1 10th Revised Page 1 Cancels 9th Revised Page 1 CHECK SHEET The Title Page and pages 1 – 91, inclusive, of this tariff are effective as of the date shown. The original and revised pages named below contain all changes from the original tariff that are in effect on the date shown Page Page Page Page Revision Revision Revision Revision No. No. No. No. Title 3rd Rev 26 3rd Rev 52 9th Rev * 78 3rd Rev 1 10th Rev * 27 2nd Rev 53 6th Rev 79 3rd Rev 2 2nd Rev 28 3rd Rev 54 8th Rev * 80 3rd Rev 3 4th Rev 29 3rd Rev 55 8th Rev * 81 3rd Rev 4 2nd Rev 30 3rd Rev 56 8th Rev * 82 3rd Rev 5 3rd Rev 31 2nd Rev 57 5th Rev 83 2nd Rev 6 3rd Rev 32 3rd Rev 58 5th Rev 84 2nd Rev 7 3rd Rev -

Frontier TV Terms of Service

Frontier.com FRONTIER TV TERMS OF SERVICE THESE TERMS AND CONDITIONS STATE IMPORTANT REQUIREMENTS REGARDING YOUR USE OF FRONTIER TV PROVIDED BY FRONTIER® AND YOUR RELATIONSHIP WITH FRONTIER COMMUNICATIONS AND ITS AFFILIATES PROVIDING FRONTIER TV SERVICE1, INCLUDING THE REQUIREMENT THAT ANY DISPUTE BE RESOLVED BY BINDING ARBITRATION ON AN INDIVIDUAL BASIS RATHER THAN LAWSUITS, JURY TRIALS, OR CLASS ACTIONS, AS EXPLAINED MORE FULLY BELOW. This Agreement sets forth the terms and conditions under which you the subscriber ("you," "your" or "Subscriber") agree to use Frontier TV (including Equipment and Programming) (“Frontier TV Service” or “Service”) and under which Frontier affiliates ("Frontier," "us " or "we") agree to provide Service to you. References to “Frontier,” “you,” and “us” include our respective subsidiaries, affiliates, agents, employees, predecessors in interest, successors, and assigns, as well as all authorized or unauthorized users or beneficiaries of Frontier TV Service under this or prior agreements between us or our predecessors in interest. THIS IS A CONTRACT. PLEASE READ THESE TERMS CAREFULLY AS THEY CONTAIN IMPORTANT INFORMATION REGARDING YOUR RIGHTS AND OBLIGATIONS, AND OURS. IF YOU DO NOT AGREE TO THESE TERMS, DO NOT USE THE SERVICE AND CONTACT US IMMEDIATELY TO TERMINATE IT. 1. ACCEPTANCE OF AGREEMENT; AGREEMENT TERMS GENERALLY INCLUDED. This Agreement starts when you accept it. By accepting this Agreement, you and any other users of Frontier TV Service within your Premises are bound by its conditions. Your acceptance of this Agreement occurs upon the earlier of your use of or payment for the Service. This Agreement will end when you or we terminate this Agreement as permitted below. -

FRONTIER CALIFORNIA INC. SCHEDULE Cal. P.U.C. No. C-1 9260 E

FRONTIER CALIFORNIA INC. SCHEDULE Cal. P.U.C. No. C-1 9260 E. Stockton Blvd., Elk Grove, CA 95624 6th Revised Check Sheet 1 U-1002-C Canceling 5th Revised Check Sheet 1 FACILITIES FOR INTRASTATE ACCESS List of Effective Sheets Sheet A through 375 of the schedule are effective as of the date shown on each sheet. Original or revised sheets contain all material including changes from the original schedule that are in effect on the date hereof. Number of Number of Number of Revision Except Revision Except Revision Except Sheet No. As Indicated Sheet No. As Indicated Sheet No. As Indicated Check Sheet 1 6th Revised* 11 Original 46 Original Check Sheet 2 5th Revised* 12 Original 47 Original Check Sheet 3 3rd Revised* 13 Original 48 Original Check Sheet 4 Original 14 Original 49 Original Title Sheet 1 Original 15 Original 50 Original TOC 1 Original 16 Original 51 Original TOC 2 Original 17 Original 52 Original TOC 3 Original 18 Original 53 Original TOC 4 Original 19 Original 54 Original TOC 5 Original 20 Original 55 Original TOC 6 Original 21 Original 56 Original TOC 7 1st Revised 22 Original 57 Original TOC 8 Original 23 Original 58 Original TOC 9 Original 24 Original 59 Original TOC 10 Original 25 Original 60 1st Revised TOC 11 Original 26 Original 61 1st Revised TOC 12 Original 27 Original 61.1 Original TOC 13 Original 28 Original 61.2 Original TOC 14 Original 29 Original 61.3 Original TOC 15 Original 30 Original 61.4 Original TOC 16 Original 31 Original 62 Original TOC 17 Original 32 Original 63 Original TOC 18 Original 33 Original 64 Original TOC 19 Original 34 Original 65 Original TOC 20 Original 35 Original 66 Original 1 Original 36 Original 67 Original 2 Original 37 Original 68 Original 3 Original 38 Original 69 Original 4 Original 39 Original 70 Original 5 Original 40 Original 71 Original 6 Original 41 Original 72 Original 7 Original 42 Original 8 Original 43 Original 9 Original 44 Original 10 Original 45 Original * New or Revised Continued Advice Letter No.