BOLLINGER BANDS - the Methods As Explained by John Bollinger in His Book , Bollinger on Bollinger Bands

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

An Interview with John Bollinger

® AIQ Opening BellMonthly IN THIS ISSUE VOL. 6 ISSUE 2 FEBRUARY 1997 TRADING TECHNIQUES Feature John Bollinger discusses his Bollinger Bands .................. 1 AN INTERVIEW WITH JOHN BOLLINGER Se ctions account program, what percent of the By David Vomund investments are in equities and what is Price Volume Divergence your average holding period? Report .................................. 5 his month we are pleased to JB: We are primarily equity Market Review ..................... 8 present an interview with John investors. We dont buy any futures. Data Maintenance ............... 8 Bollinger, a keynote speaker at Our growth model is currently allo- Tour March seminar in Dallas. Mr. cated approximately 60% to the stock Bollinger is market, 20% to the president of bond market, and Bollinger Capital 20% to the interna- Management. He tional stock mar- provides money ket. We are management primarily interme- services and diate term traders. publishes the Our research tends Capital Growth to center on a Letter. He is best holding period of known for his three to six months Bollinger Bands, with most of the which is a feature emphasis on six in TradingExpert. months. However, For information on that doesnt Bollinger Capital preclude us from The Opening Bell Monthly Managements John Bollinger, CFA, CMT taking advantage is a publication of products and of short term AIQ Incorporated services, call 310-798-8855 or write to opportunities, for example when we see David Vomund, Chief Analyst P.O. Box 3358, Manhattan Beach, CA an attractive technical non-confirma- P.O. Box 7530 90266. Send e-mail to tion. Incline Village, Nevada 89452 [email protected]. -

Investing with Bollinger Bands

Investing with Bollinger Bands This article was written some years ago, but is very relevant to today. The charts used to illustrate the text are now somewhat dated, but still relevant for the present purpose of teaching a technique. As moving averages became more popular, some analysts noticed that when prices were moving upward, they had a tendency to rise only so far above the moving average. When prices were falling they tended to fall only so far below the moving average. How far they rose or fell seemed to vary from stock to stock and also from time to time. However, the tendency was so consistent that it could be useful to both traders and investors. These early analysts hit on the idea of drawing lines a certain percentage of the moving average above and below the moving average line. They selected the percentage stock-by-stock so that it seemed to catch most of the price action on the chart, typically 90% or more of the price action. GWT - GWA INTERNATIONAL > -2 to 291 D @ D 020103-070604 320 MOV AVS 22(0) 5 band 310 300 290 280 270 260 250 240 230 JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC JAN FEB MAR APR MAY JUN 03 04 Chart 1: Daily Line Chart of GWA International with a 22-day Moving Average and 5% Bands The result was something like Chart 1, where we have a daily line chart, on which is drawn a 22-day moving average, with 5% bands above and below it. -

Technical-Analysis-Bloomberg.Pdf

TECHNICAL ANALYSIS Handbook 2003 Bloomberg L.P. All rights reserved. 1 There are two principles of analysis used to forecast price movements in the financial markets -- fundamental analysis and technical analysis. Fundamental analysis, depending on the market being analyzed, can deal with economic factors that focus mainly on supply and demand (commodities) or valuing a company based upon its financial strength (equities). Fundamental analysis helps to determine what to buy or sell. Technical analysis is solely the study of market, or price action through the use of graphs and charts. Technical analysis helps to determine when to buy and sell. Technical analysis has been used for thousands of years and can be applied to any market, an advantage over fundamental analysis. Most advocates of technical analysis, also called technicians, believe it is very likely for an investor to overlook some piece of fundamental information that could substantially affect the market. This fact, the technician believes, discourages the sole use of fundamental analysis. Technicians believe that the study of market action will tell all; that each and every fundamental aspect will be revealed through market action. Market action includes three principal sources of information available to the technician -- price, volume, and open interest. Technical analysis is based upon three main premises; 1) Market action discounts everything; 2) Prices move in trends; and 3) History repeats itself. This manual was designed to help introduce the technical indicators that are available on The Bloomberg Professional Service. Each technical indicator is presented using the suggested settings developed by the creator, but can be altered to reflect the users’ preference. -

Timeframeset

QuantShare Programming Language Table of contents 1. QuantShare Language 1.1 Application Info 1.1.1 NbGroups 1.1.2 NbIndexes 1.1.3 NbIndustries 1.1.4 NbInGroup 1.1.5 NbInIndex 1.1.6 NbInIndustry 1.1.7 NbInMarket 1.1.8 NbInSector 1.1.9 NbMarkets 1.1.10 NbSectors 1.2 Candlestick Pattern 1.2.1 Cdl2crows (0) 1.2.2 Cdl2crows (1) 1.2.3 Cdl3blackcrows (0) 1.2.4 Cdl3blackcrows (1) 1.2.5 Cdl3inside (0) 1.2.6 Cdl3inside (1) 1.2.7 Cdl3linestrike (0) 1.2.8 Cdl3linestrike (1) 1.2.9 Cdl3outside (0) 1.2.10 Cdl3outside (1) 1.2.11 Cdl3staRsinsouth (0) 1.2.12 Cdl3staRsinsouth (1) 1.2.13 Cdl3whitesoldiers (0) 1.2.14 Cdl3whitesoldiers (1) 1.2.15 CdlAbandonedbaby (0) 1.2.16 CdlAbandonedbaby (1) 1.2.17 CdlAdvanceblock (0) 1.2.18 CdlAdvanceblock (1) 1.2.19 CdlBelthold (0) 1.2.20 CdlBelthold (1) 1.2.21 CdlBreakaway (0) 1.2.22 CdlBreakaway (1) 1.2.23 CdlClosingmarubozu (0) 1.2.24 CdlClosingmarubozu (1) 1.2.25 CdlConcealbabyswall (0) 1.2.26 CdlConcealbabyswall (1) 1.2.27 CdlCounterattack (0) 1.2.28 CdlCounterattack (1) 1.2.29 CdlDarkcloudcover (0) 1.2.30 CdlDarkcloudcover (1) 1.2.31 CdlDoji (0) 1.2.32 CdlDoji (1) 1.2.33 CdlDojistar (0) 1.2.34 CdlDojistar (1) 1.2.35 CdlDragonflydoji (0) 1.2.36 CdlDragonflydoji (1) 1.2.37 CdlEngulfing (0) 1.2.38 CdlEngulfing (1) 1.2.39 CdlEveningdojistar (0) 1.2.40 CdlEveningdojistar (1) 1.2.41 CdlEveningstar (0) 1.2.42 CdlEveningstar (1) 1.2.43 CdlGapsidesidewhite (0) 1.2.44 CdlGapsidesidewhite (1) 1.2.45 CdlGravestonedoji (0) 1.2.46 CdlGravestonedoji (1) 1.2.47 CdlHammer (0) 1.2.48 CdlHammer (1) 1.2.49 CdlHangingman (0) 1.2.50 -

Index.Pdf (69.91KB)

26_178089 bindex.qxp 2/27/08 9:38 PM Page 329 Index • Symbols & • B • Numerics • bar charts candlestick chart, compared to, 19, 20, %K (fast) stochastic oscillators, 263 317–319 %D (slow) stochastic oscillators, 263 defined, 10, 27–28 5-day moving average, 253–254, 256, 257, single line, 28 258–260 on Web sites, 53 10-day moving average, 259–260 BEA Systems, 220 20-day moving average, 255, 256, 258–260 bear market, defined, 22 24-hour electronic trading Bear Stearns Companies, Inc., 147 high and low prices, futures, 36–37 bearish state volume, relationship to, 25 candlestick charting and patterns, 20–22, 30-minute chart, 74–75 279–290 200-day moving average, 253 closing price as body of candlestick, 38 defined, 96 double-stick patterns • A • dark cloud cover, 172–174 abandoned baby doji star, 167–168 bearish, 229–231 engulfing pattern, 156–158 bullish, 199–201 harami, 159–161 affordability and trading choices, 15 harami cross, 161–164 after-hours trading inverted hammer, 164–167 high and low prices, futures, 36–37 meeting line, 168–172 volume, relationship to, 25 neck lines, 180–183 Alcoa, 170, 171 piercing line, 172–174 Altera Corp., 304 separating lines, 178–180 Amazon.com, 269 thrusting lines, 175–177 American Express, 310–311 sell indicators, 279–290 American Stock Exchange (AMEX), 33, 68 single-stick pattern Amgen, Inc., 151–152 belt hold, 113 Analog Devices Inc., 206–207 doji, 90–94 Apple Computer, 93–94, 168, 169, 276, gravestone doji, 90–94 292–293 long black candle, 84–90 Applebee’s International, 221–222 long marubozus, 86–88 -

Trapped Ions and Laser Cooling III : Selected Publications of the Ion Storage Group of the Time and Frequency Division, NIST, Bo

NATL INST Of STAND & TECH R.IC, A111D3 TSbMfiO NIST Technical Note 1353 NIST jpUBllCATlONS*;:; U.S. DEPARTMENT OF COMMERCE / National Institute of Standards and Technology Selected publications of the Edited by: James C. Bergquist Storage Group John J. Bollinger e and Frequency Division Wayne M. Itano J, Boulder, Colorado David J. Wineland /S & 3 '^1 Trapped Ions and Laser Cooling Selected publications of the Ion Storage Group of the Time and Frequency Division Edited by James C. Bergquist John J. Bollinger / ^ Wayne M. Itano , David J. Wineland"^ Time and Frequency Division Physics Laboratory National Institute of Standards and Technology Boulder, Colorado 80303-3328 Supported in part by U.S. Office of Naval Research 800 North Quincy Arlington, Virginia 22217 April 1992 *" *^TE3 o* U.S. DEPARTMENT OF COMMERCE, Barbara Hackman Franklin, Secretary TECHNOLOGY ADMINISTRATION, Robert M. White, Under Secretary for Technology NATIONAL INSTITUTE OF STANDARDS AND TECHNOLOGY, John W. Lyons, Director National Institute of Standards and Technology Technical Note Natl. Inst. Stand. Technol., Tech. Note 1353, 204 pages (April 1992) CODEN:NTNOEF U.S. GOVERNMENT PRINTING OFFICE WASHINGTON: 1992 For sale by the Superintendent of Documents, U.S. Government Printing Office, Washington, DC 20402-9325 PREFACE This collection of papers represents the work of the Ion Storage Group, Time and Frequency Division, National Institute of Standards and Technology from October 1988 to February 1992. It follows the collections of papers contained in NBS Technical Note 1086, Trapped Ions and Laser Cooling (June 1985) and NIST Technical Note 1324 Trapped Ions and Laser Cooling II (September 1988). Although the primary goal of this work has been the development of techniques necessary for achieving high resolution spectroscopy, we have also been able to investigate related areas of research. -

John Bollinger's Market Timing Chart Pack

John Bollinger's Market-Timing Chart Pack Data as of 30 November 2018 A collection of stock-market forecasting tools. This chart pack is part of your Bollinger Bands Letter subscription. While re-distributing the Bollinger Bands Letter is not allowed, you may feel free to share this chart pack with others. Good trading, John Bollinger Copyright 2018 Bollinger Capital Management John Bollinger's Market-Timing Chart Pack 1. Bollinger Bands with %b 2. Bollinger Bands with BandWidth 3. BBTrend 4. Volatility Index (VIX) 5. Volatility Premium: Spot vs. 3-month (VXV/VIX) 6. S&P 500 with 21-, 63- & 126-day Averages and S&P/Value Line Ratio 7. S&P 500 & S&P 600, Percent above 50-day Averages 8. NYSE Advance-Decline Line 9. NYSE Breadth Thrust & 10-day AD Osc 10. NYSE Advance-Decline Oscillator 11. NYSE Up-Down Volume Oscillator 12. NYSE New 52-week Highs and Lows with Titanic Markers Copyright 2018 Bollinger Capital Management John Bollinger's Market-Timing Chart Pack 13. High-Low Index 14. High Low Logic Index with Hindenburg Omen Markers (exp) 15. 10-day Open Arms Index 16. AAII Sentiment Survey 17. Investors Intelligence Advisor Sentiment 18. Russell 1000 & Advance-Decline Line 19. Russell 2000 & Advance-Decline Line 20. Russell 3000 & Advance-Decline Line 21. Sector Grid 22. Commodities 23. Theoretical Dow with Intraday Intensity 24. Deviation from Average 25. Interest Rates 26. World Stock Markets Copyright 2018 Bollinger Capital Management 3000 Courtesy www.BollingerBands.comChart 1: Bollinger Bands with %b 2900 2800 S&P 500 2700 2600 1.0 -

Trade on Reversals: RSI and Bollinger Bands

Trade on Reversals: RSI and Bollinger Bands Many researchers in the academic world have shown that momentum port- folios, which consist in buying the best-performing assets and selling the worst- performing assets, can be followed by reversals or negative returns immediately after the observation period (usually 12 months for equities). In the FX market, two popular technical indicators that are closely watch by market participants to observe a potential overbought or oversold currency are the Relative Strength Index (RSI) and the Bollinger Bands. 1 Relative Strength Index (RSI) The RSI was developed by J. Welles Wilder in 1978, and inform investors when a particular currency (or other asset) is oversold or overbought based on the past observations. There are several ways of computing the RSI: here is the most simple one that I used in my Excel File. 1.1 A Simple RSI We first have to select the number of periods, which is usually 14 days for traditional RSI users. We add all upward movements (Ups) and downward movements (Downs) in [closing] price during that time frame, and then compute the ratio of the two variables: Ups RS = (1) t Downs We can eventually calculate the [simple] RSI by using the following formula: 100 RSIt = 100 − (2) 1 + RSt We then get a number that stands between 0 and 100 (Note that if we had only negative sessions, the RSI would be equal to 0 and in case of only positive sessions, the RSI should be set at 100 as Downs would be equal to zero). Then, we have to set our two thresholds to determine when our RSI indica- tor is signalling an overbought or oversold currency. -

Battle of the Bands Putting Various Bollinger Band Strategies to the Test in Stock Indices Since 1999

TRADING STRATEGIES Battle of the bands Putting various Bollinger Band strategies to the test in stock indices since 1999. BY CAMILLO LENTO ollinger Bands are price past 10 years. It then focuses on two dis- According to standard interpretations, boundaries that are typically tinct periods — the technology bubble’s when price touches or exceeds one of the placed two standard devia- arc from 1999 to 2002 and the recent trading bands, the market is overextend- B tions (SD) above and below financial meltdown from late 2007 to ed. The essence of the traditional a simple moving average (SMA). The early 2009. In such crisis periods, one approach is to sell into strength and buy indicator shows whether volatility is high Bollinger Band approach worked better into weakness on the premise that or low as the width between the bands than the other. strength or weakness is overdone. A buy widens or narrows; it also shows where signal triggers if price drops below the the market is relative to past prices and Take the traditional lower band. In this case, the market within the bands themselves. (countertrend) view … could be oversold. A sell signal triggers if Most price action occurs within the The debate over how to interpret situa- price breaks above the upper band. In upper and lower bands, so when price tions in which price hits or exceeds the this case, the market could be over- hits either line, the market is reaching an upper or lower Bollinger Bands boils bought. extreme. As with most technical indica- down to one question: Fade or trade? In However, this method doesn’t work tors, Bollinger Bands are interpreted in other words, is the market poised to during strong trends. -

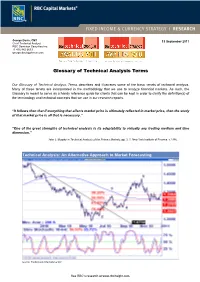

Glossary of Technical Analysis Terms

George Davis, CMT 13 September 2011 Chief Technical Analyst RBC Dominion Securities Inc. +1 416 842 6633 [email protected] Glossary of Technical Analysis Terms Our Glossary of Technical Analysis Terms describes and illustrates some of the basic tenets of technical analysis. Many of these tenets are incorporated in the methodology that we use to analyze financial markets. As such, the Glossary is meant to serve as a handy reference guide for clients that can be kept in order to clarify the definition(s) of the terminology and technical concepts that we use in our research reports. “It follows then that if everything that affects market price is ultimately reflected in market price, then the study of that market price is all that is necessary.” “One of the great strengths of technical analysis is its adaptability to virtually any trading medium and time dimension.” John J. Murphy in Technical Analysis of the Futures Markets, pp. 3, 7, New York Institute of Finance, c.1986. Technical Analysis: An Alternative Approach to Market Forecasting Source: Tradermade International Ltd. See RBC’s research at www.rbcinsight.com. 13 September 2011 Glossary of Technical Analysis Terms Table of Contents Glossary of Technical Analysis Terms............................................. 1 Table of Contents ............................................................................... 2 Introduction ........................................................................................ 3 Types of Charts ................................................................................. -

Empirical Optimization of Bollinger Bands for Profitability

EMPIRICAL OPTIMIZATION OF BOLLINGER BANDS FOR PROFITABILITY Oliver Douglas Williams Bachelor of Arts, The University of Western Ontario PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF ARTS In the Faculty of Business Administration Financial Risk Management Program O Oliver Williams, 2006 SIMON FRASER UNIVERSITY Summer 2006 All rights reserved. This work may not be reproduced in whole or in part, by photocopy or other means, without permission of the author. APPROVAL Name: Oliver Douglas Williams Degree: Master of Arts Title of Project: Empirical Optimization of Bollinger Bands for Profitability Supervisory Committee: Dr. Geoffrey Poitras Senior Supervisor Professor of Finance Dr. Chris Veld Second Reader Associate Professor of Finance Date Approved: SIMON FRASER UMWERS~I.brary DECLARATION OF PARTIAL COPYRIGHT LICENCE The author, whose copyright is declared on the title page of this work, has granted to Simon Fraser University the right to lend this thesis, project or extended essay to users of the Simon Fraser University Library, and to make partial or single copies only for such users or in response to a request from the library of any other university, or other educational institution, on its own behalf or for one of its users. The author has further granted permission to Simon Fraser University to keep or make a digital copy for use in its circulating collection, and, without changing the content, to translate the thesislproject or extended essays, if technically possible, to any medium or format for the purpose of preservation of the digital work. The author has further agreed that permission for multiple copying of this work for scholarly purposes may be granted by either the author or the Dean of Graduate Studies. -

Forecasting a Volatility Tsunami

Forecasting a Volatility Tsunami Andrew Thrasher Introduction Great importance is found in the study of Financial Enhancement Group market volatility due to the historically negative According to the United Kingdom’s National correlation the Volatility Index has had to U.S. Oceanography Centre, tsunami waves can be as equities. By knowing the warning signs of a much as 125 miles in length and have resulted tsunami wave of volatility, professional and non- in some of the deadliest natural disasters in professional traders can better prepare their history. Fortunately, scientists have discovered portfolios for potential downside risks as well as warning signs of these massive waves, which have the opportunity to profit from advances in are believed to be caused by shifts in the earth’s volatility and/or declines in equities. tectonic plates. One of the visible signs of a forthcoming tsunami is the receding of water The popularity of volatility trading has seen from a coast line, exposing the ocean floor. steady growth to over $4 billion with more than This is often referred to as “the calm before the 30 index-listed Exchange Traded Products. storm.” The same type of activity can also be Drimus and Farkas (2012) note that “the found in financial markets, specifically when average daily volume for VIX options in 2011 analyzing the CBOE Volatility Index (VIX). It has almost doubled compared to 2010 and is is often believed that when volatility gets to a nearly 20 times larger than in the year of their “low” level the likelihood of a spike increases. launch, 2006.” We can also see the increase in However, as this paper will show, there is a interest surrounding the Volatility Index by more optimal tsunami-like condition that takes looking at trends in online searches with regards place within the markets, providing a better to low levels within the VIX.