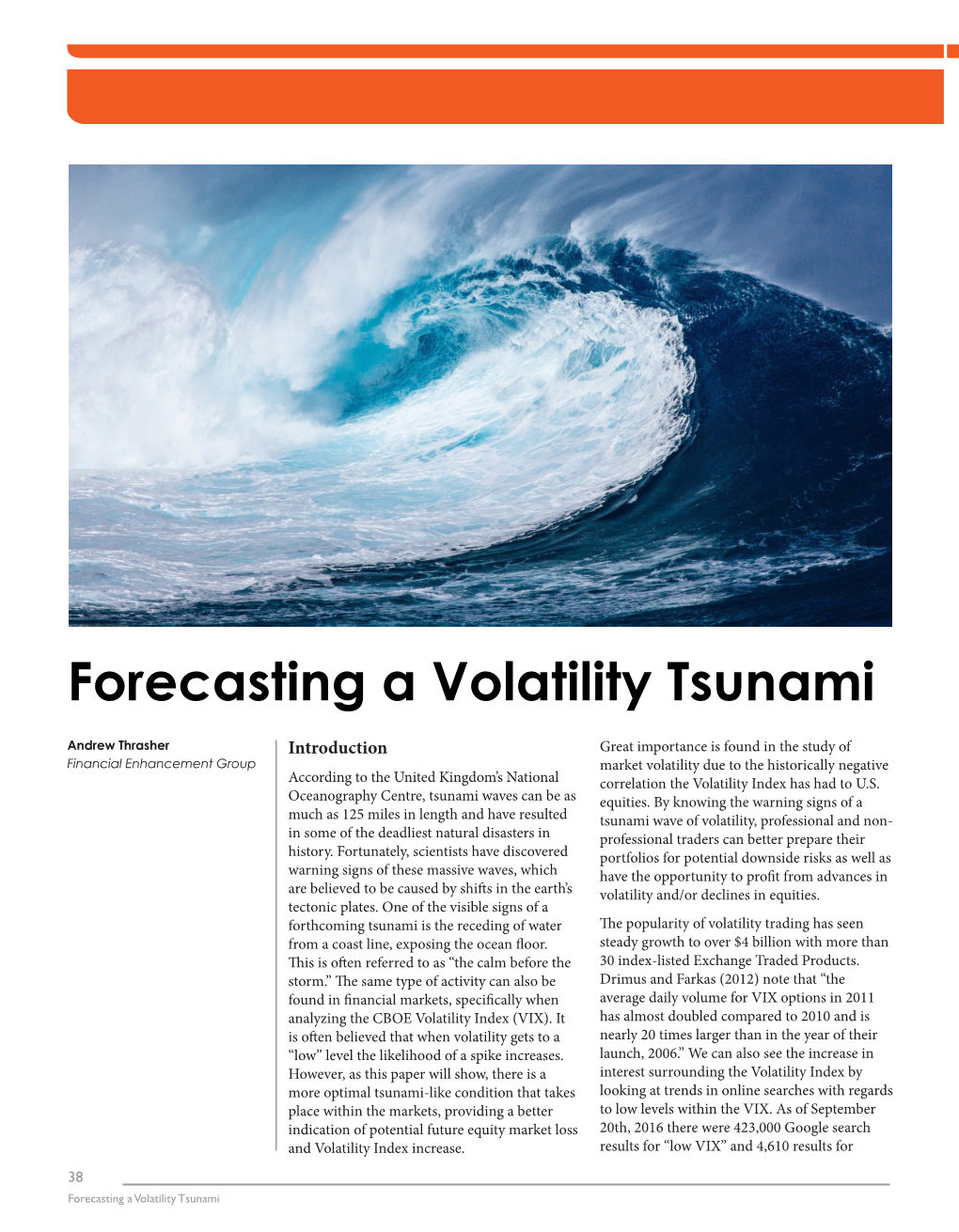

Forecasting a Volatility Tsunami

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Estimating 90-Day Market Volatility with VIX and VXV

Estimating 90-Day Market Volatility with VIX and VXV Larissa J. Adamiec, Corresponding Author, Benedictine University, USA Russell Rhoads, Tabb Group, USA ABSTRACT The CBOE Volatility Index (VIX) has historically been a consistent indicator of 30-day or 1-month (21-day actual) realized market volatility. In addition, the Chicago Board Options Exchange also quotes the CBOE 3-Month Volatility Index (VXV) which indicates the 3-month realized market volatility. This study demonstrates both VIX and VXV are still reliable indicators of their respective realized market volatility periods. Both of the indexes consistently overstate realized volatility, indicating market participants often perceive volatility to be much higher than volatility actually is. The overstatement of expected volatility leads to an indicator which is consistently higher. Perceived volatility in the long-run is often lower than volatility in the short-run which is why VXV is often lower than VIX (VIX is usually lower than VXV). However, the accuracy of the VXV is roughly 35% as compared with the accuracy of the VIX at 60.1%. By combining the two indicators to create a third indicator we were able to provide a much better estimate of 64-Day Realized volatility, with an accuracy rate 41%. Due to options often being over-priced, historical volatility is often higher than both realized volatility or the volatility index, either the VIX or the VXV. Even though the historical volatility is higher we find the estimated historical volatility to be more easily estimated than realized volatility. Using the same time period from January 2, 2008 through December 31, 2016 we find the VIX estimates the 21-Day Historical Volatility with 83.70% accuracy. -

Copyrighted Material

Index 12b-1 fee, 68–69 combining with Western analysis, 3M, 157 122–123 continuation day, 116 ABC of Stock Speculation, 157 doji, 115 accrual accounting, 18 dragonfl y doji, 116–117 accumulated depreciation, 46–47 engulfi ng pattern, 120, 121 accumulation phase, 158 gravestone doji, 116, 117, 118 accumulation/distribution line, hammer, 119 146–147 hanging man, 119 Adaptive Market Hypothesis, 155 harami, 119, 120 Altria, 29, 127, 185–186 indicators 120 Amazon.com, 151 long, 116, 117, 118 amortization, 47, 49 long-legged doji, 118 annual report, 44–46 lower shadow, 115 ascending triangle, 137–138, 140 marubozu, 116 at the money, 192 real body, 114–115 AT&T, 185–186 segments illustrated, 114 shadows, 114 back-end sales load, 67–68 short,116, 117 balance sheet, 46–50 spinning top, 118–119 balanced mutual funds, 70–71 squeeze alert, 121, 122, 123 basket of stocks, 63 tails, 114 blue chip companies, 34 three black crows, 122, 123 Boeing, 134–135 three white soldiers, 122, 123 book value, 169 trend-based, 117–118 breadth, 82–83, 97 upper shadow, 115 breakaway gap, 144 wicks, 114 break-even rate, 16–17 capital assets, 48, 49 breakout, 83–84, 105–106 capitalization-based funds, 71 Buffett, Warren, 152 capitalization-weighted average, 157 bull and bear markets,COPYRIGHTED 81, 174–175 Caterpillar, MATERIAL 52–54, 55, 57, 58, 59, 131 Bureau of Labor Statistics (BLS), 15 CBOE Volatility Index (VIX), 170, 171 Buy-and-hold strategy, 32, 204–205 Chaikin Money Flow (CMF), 146 buy to open/sell to open, 96 channel, 131–132 charting calendar spreads, 200–201 -

“Dividend Policy and Share Price Volatility”

“Dividend policy and share price volatility” Sew Eng Hooi AUTHORS Mohamed Albaity Ahmad Ibn Ibrahimy Sew Eng Hooi, Mohamed Albaity and Ahmad Ibn Ibrahimy (2015). Dividend ARTICLE INFO policy and share price volatility. Investment Management and Financial Innovations, 12(1-1), 226-234 RELEASED ON Tuesday, 07 April 2015 JOURNAL "Investment Management and Financial Innovations" FOUNDER LLC “Consulting Publishing Company “Business Perspectives” NUMBER OF REFERENCES NUMBER OF FIGURES NUMBER OF TABLES 0 0 0 © The author(s) 2021. This publication is an open access article. businessperspectives.org Investment Management and Financial Innovations, Volume 12, Issue 1, 2015 Sew Eng Hooi (Malaysia), Mohamed Albaity (Malaysia), Ahmad Ibn Ibrahimy (Malaysia) Dividend policy and share price volatility Abstract The objective of this study is to examine the relationship between dividend policy and share price volatility in the Malaysian market. A sample of 319 companies from Kuala Lumpur stock exchange were studied to find the relationship between stock price volatility and dividend policy instruments. Dividend yield and dividend payout were found to be negatively related to share price volatility and were statistically significant. Firm size and share price were negatively related. Positive and statistically significant relationships between earning volatility and long term debt to price volatility were identified as hypothesized. However, there was no significant relationship found between growth in assets and price volatility in the Malaysian market. Keywords: dividend policy, share price volatility, dividend yield, dividend payout. JEL Classification: G10, G12, G14. Introduction (Wang and Chang, 2011). However, difference in tax structures (Ho, 2003; Ince and Owers, 2012), growth Dividend policy is always one of the main factors and development (Bulan et al., 2007; Elsady et al., that an investor will focus on when determining 2012), governmental policies (Belke and Polleit, 2006) their investment strategy. -

Putting Volatility to Work

Wh o ’ s afraid of volatility? Not anyone who wants a true edge in his or her trad i n g , th a t ’ s for sure. Get a handle on the essential concepts and learn how to improve your trading with pr actical volatility analysis and trading techniques. 2 www.activetradermag.com • April 2001 • ACTIVE TRADER TRADING Strategies BY RAVI KANT JAIN olatility is both the boon and bane of all traders — The result corresponds closely to the percentage price you can’t live with it and you can’t really trade change of the stock. without it. Most of us have an idea of what volatility is. We usually 2. Calculate the average day-to-day changes over a certain thinkV of “choppy” markets and wide price swings when the period. Add together all the changes for a given period (n) and topic of volatility arises. These basic concepts are accurate, but calculate an average for them (Rm): they also lack nuance. Volatility is simply a measure of the degree of price move- Rt ment in a stock, futures contract or any other market. What’s n necessary for traders is to be able to bridge the gap between the Rm = simple concepts mentioned above and the sometimes confus- n ing mathematics often used to define and describe volatility. 3. Find out how far prices vary from the average calculated But by understanding certain volatility measures, any trad- in Step 2. The historical volatility (HV) is the “average vari- er — options or otherwise — can learn to make practical use of ance” from the mean (the “standard deviation”), and is esti- volatility analysis and volatility-based strategies. -

Spread, Volatility, and Volume Relationship in Financial Markets

Spread, volatility, and volume relationship in financial markets and market maker’s profit optimization Jack Sarkissian Managing Member, Algostox Trading LLC email: [email protected] Abstract We study the relationship between price spread, volatility and trading volume. We find that spread forms as a result of interplay between order liquidity and order impact. When trading volume is small adding more liquidity helps improve price accuracy and reduce spread, but after some point additional liquidity begins to deteriorate price. The model allows to connect the bid-ask spread and high-low bars to measurable microstructural parameters and express their dependence on trading volume, volatility and time horizon. Using the established relations, we address the operating spread optimization problem to maximize the market-maker’s profit. 1. Introduction When discussing security prices it is customary to describe them with single numbers. For example, someone might say price of Citigroup Inc. (ticker “C”) on April 18, 2016 was $45.11. While good enough for many uses, it is not entirely accurate. Single numbers can describe price only as referring to a particular transaction, in which 푁 units of security are transferred from one party to another at a price $푋 each. Price could be different a moment before or after the transaction, or if the transaction had different size, or if it were executed on a different exchange. To be entirely accurate, one should specify these numerous details when talking about security price. We will take this observation a step further. Technically speaking, other than at the time of transaction we cannot say that price exists as a single number at all. -

Calibration of Bollinger Bands Parameters for Trading Strategy Development in the Baltic Stock Market

ISSN 1392 – 2785 Inzinerine Ekonomika-Engineering Economics, 2010, 21(3), 244-254 Calibration of Bollinger Bands Parameters for Trading Strategy Development in the Baltic Stock Market Audrius Kabasinskas, Ugnius Macys Kaunas University of Technology K. Donelaicio st. 73, LT-44029, Kaunas, Lithuania e-mail: [email protected], [email protected] In recent decades there was a robust boom in "Bollinger plotter" was developed using the most investment sector in Lithuania, as more people chose to popular mathematical toolbox MatLab in order to solve invest money in investment funds rather than keep money in stated problems. Application is capable of charting the closet. The Baltic States Market turnover has increased Bollinger Bands and 6 other technical indicators with from 721 MEUR in 2000 to 978 MEUR in 2008 (with peak desired period of time. This software is not a fully 2603 MEUR in 2005). When difficult period appeared in automated decision making system, as decisions are global markets, a lot of attention was dedicated towards the usually made based on value judgment. managing of investments. Investment management firms in Since the stock returns usually have distributions with Lithuania gain significance in personal as well as in fat tails, then less than 95% of data fit in the Bollinger business section increasingly; even though these firms are trading channels. However the Bollinger bands trading considerably young (the first one in Lithuania was signals were supported by additional indicators (e.g. %b), established in year 2000). so the loss of data is not significant. Successful investment begins with the financial Our calibration results show that short term investor analysis of stock, asset or index, which you are going to should apply 10 days moving average and use a trading invest. -

FOREX WAVE THEORY.Pdf

FOREX WAVE THEORY This page intentionally left blank FOREX WAVE THEORY A Technical Analysis for Spot and Futures Currency Traders JAMES L. BICKFORD McGraw-Hill New York Chicago San Francisco Lisbon London Madrid Mexico City Milan New Delhi San Juan Seoul Singapore Sydney Toronto Copyright © 2007 by The McGraw-Hill Companies. All rights reserved. Manufactured in the United States of America. Except as permitted under the United States Copyright Act of 1976, no part of this publication may be reproduced or distributed in any form or by any means, or stored in a database or retrieval system, without the prior written permission of the publisher. 0-07-151046-X The material in this eBook also appears in the print version of this title: 0-07-149302-6. All trademarks are trademarks of their respective owners. Rather than put a trademark symbol after every occurrence of a trademarked name, we use names in an editorial fashion only, and to the benefit of the trademark owner, with no intention of infringement of the trademark. Where such designations appear in this book, they have been printed with initial caps. McGraw-Hill eBooks are available at special quantity discounts to use as premiums and sales pro- motions, or for use in corporate training programs. For more information, please contact George Hoare, Special Sales, at [email protected] or (212) 904-4069. TERMS OF USE This is a copyrighted work and The McGraw-Hill Companies, Inc. (“McGraw-Hill”) and its licen- sors reserve all rights in and to the work. Use of this work is subject to these terms. -

Asset Allocation POINT WHAT DOES a LOW VIX TELL US June 2017 ABOUT the MARKET? Timely Intelligence and Analysis for Our Clients

PRICE Asset Allocation POINT WHAT DOES A LOW VIX TELL US June 2017 ABOUT THE MARKET? Timely intelligence and analysis for our clients. KEY POINTS . The financial press has been paying considerable attention lately to the Chicago Board Options Exchange Volatility Index (VIX), with many financial pundits citing recent low readings on the VIX as evidence of investor complacency and rising equity risk. Robert Harlow, CFA, CAIA . Quantitative Analyst Media coverage often implies that a low current VIX is a strong signal of expected Asset Allocation future volatility and will be followed by a sell-off in U.S. equities and other risk-seeking assets. Historical evidence shows that, over the near term, investors typically overestimate the next 30-day volatility of the S&P 500 Index. Further, when the VIX has been low, U.S. equities have outperformed U.S. bonds on average over the next 12 months, regardless of the change in the VIX over that horizon. Without a meaningful and prolonged catalyst, we do not believe a low level of the VIX David Clewell, CFA alone implies investor complacency or an immediate danger of a risk-off event. Research Analyst Asset Allocation BACKGROUND There has been much discussion in the financial press recently about the danger of investor complacency—with a low VIX frequently cited as compelling evidence that equity investors have grown too relaxed about potential risks. The problem is that it is difficult to determine whether markets are truly complacent or not; we can’t survey all investors and, even if we could, how many investors would admit that they were complacent? Instead, we take a mental shortcut and presume that something we can measure is a good proxy for the thing we actually care about. -

Forecasting Direction of Exchange Rate Fluctuations with Two Dimensional Patterns and Currency Strength

FORECASTING DIRECTION OF EXCHANGE RATE FLUCTUATIONS WITH TWO DIMENSIONAL PATTERNS AND CURRENCY STRENGTH A THESIS SUBMITTED TO THE GRADUATE SCHOOL OF NATURAL AND APPLIED SCIENCES OF MIDDLE EAST TECHNICAL UNIVERSITY BY MUSTAFA ONUR ÖZORHAN IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF DOCTOR OF PILOSOPHY IN COMPUTER ENGINEERING MAY 2017 Approval of the thesis: FORECASTING DIRECTION OF EXCHANGE RATE FLUCTUATIONS WITH TWO DIMENSIONAL PATTERNS AND CURRENCY STRENGTH submitted by MUSTAFA ONUR ÖZORHAN in partial fulfillment of the requirements for the degree of Doctor of Philosophy in Computer Engineering Department, Middle East Technical University by, Prof. Dr. Gülbin Dural Ünver _______________ Dean, Graduate School of Natural and Applied Sciences Prof. Dr. Adnan Yazıcı _______________ Head of Department, Computer Engineering Prof. Dr. İsmail Hakkı Toroslu _______________ Supervisor, Computer Engineering Department, METU Examining Committee Members: Prof. Dr. Tolga Can _______________ Computer Engineering Department, METU Prof. Dr. İsmail Hakkı Toroslu _______________ Computer Engineering Department, METU Assoc. Prof. Dr. Cem İyigün _______________ Industrial Engineering Department, METU Assoc. Prof. Dr. Tansel Özyer _______________ Computer Engineering Department, TOBB University of Economics and Technology Assist. Prof. Dr. Murat Özbayoğlu _______________ Computer Engineering Department, TOBB University of Economics and Technology Date: ___24.05.2017___ I hereby declare that all information in this document has been obtained and presented in accordance with academic rules and ethical conduct. I also declare that, as required by these rules and conduct, I have fully cited and referenced all material and results that are not original to this work. Name, Last name: MUSTAFA ONUR ÖZORHAN Signature: iv ABSTRACT FORECASTING DIRECTION OF EXCHANGE RATE FLUCTUATIONS WITH TWO DIMENSIONAL PATTERNS AND CURRENCY STRENGTH Özorhan, Mustafa Onur Ph.D., Department of Computer Engineering Supervisor: Prof. -

FX Effects: Currency Considerations for Multi-Asset Portfolios

Investment Research FX Effects: Currency Considerations for Multi-Asset Portfolios Juan Mier, CFA, Vice President, Portfolio Analyst The impact of currency hedging for global portfolios has been debated extensively. Interest on this topic would appear to loosely coincide with extended periods of strength in a given currency that can tempt investors to evaluate hedging with hindsight. The data studied show performance enhancement through hedging is not consistent. From the viewpoint of developed markets currencies—equity, fixed income, and simple multi-asset combinations— performance leadership from being hedged or unhedged alternates and can persist for long periods. In this paper we take an approach from a risk viewpoint (i.e., can hedging lead to lower volatility or be some kind of risk control?) as this is central for outcome-oriented asset allocators. 2 “The cognitive bias of hindsight is The Debate on FX Hedging in Global followed by the emotion of regret. Portfolios Is Not New A study from the 1990s2 summarizes theoretical and empirical Some portfolio managers hedge papers up to that point. The solutions reviewed spanned those 50% of the currency exposure of advocating hedging all FX exposures—due to the belief of zero expected returns from currencies—to those advocating no their portfolio to ward off the pain of hedging—due to mean reversion in the medium-to-long term— regret, since a 50% hedge is sure to and lastly those that proposed something in between—a range of values for a “universal” hedge ratio. Later on, in the mid-2000s make them 50% right.” the aptly titled Hedging Currencies with Hindsight and Regret 3 —Hedging Currencies with Hindsight and Regret, took a behavioral approach to describe the difficulty and behav- Statman (2005) ioral biases many investors face when incorporating currency hedges into their asset allocation. -

Modeling and Analyzing Stock Trends

Modeling and Analyzing Stock Trends A Major Qualifying Project Submitted to the Faculty of Worcester Polytechnic Institute in partial fulllment of the requirements for the Degree in Bachelor of Science Mathematical Sciences By Laura Cintron Garcia Date: 5/6/2021 Advisor: Dr. Mayer Humi This report represents work of WPI undergraduate students submitted to the faculty as evidence of a degree requirement. WPI routinely publishes these reports on its web site without editorial or peer review. For more information about the projects program at WPI, see http://www.wpi.edu/Academics/Projects 1 Abstract Abstract The goal of this project is to create and compare several dierent stock prediction models and nd a correlation between the predic- tions and volatility for each stock. The models were created using the historical data, DJI index, and moving averages. The most accurate prediction model had an average of 5.3 days spent within a predic- tion band. A correlation of -0.0438 was found between that model an a measure of volatility, indicating that more prediction days means lower volatility. 2 2 Acknowledgments Without the help of some people, it would have been signicantly more di- cult to complete this project without a group. I want to extend my gratitude to Worcester Polytechnic Institute and the WPI Math Department for their great eorts and success this year regarding school and projects during the pandemic. They did everything they could to ensure these projects was still a rich experience for the students despite everything. I would also like to thank my MQP advisor, Professor Mayer Humi for his assistance and guidance on this project, for allowing me to work indepen- dently while always being willing to meet with me or answer any questions, and for continuously encouraging me to do what I thought was best for the project. -

An Interview with John Bollinger

® AIQ Opening BellMonthly IN THIS ISSUE VOL. 6 ISSUE 2 FEBRUARY 1997 TRADING TECHNIQUES Feature John Bollinger discusses his Bollinger Bands .................. 1 AN INTERVIEW WITH JOHN BOLLINGER Se ctions account program, what percent of the By David Vomund investments are in equities and what is Price Volume Divergence your average holding period? Report .................................. 5 his month we are pleased to JB: We are primarily equity Market Review ..................... 8 present an interview with John investors. We dont buy any futures. Data Maintenance ............... 8 Bollinger, a keynote speaker at Our growth model is currently allo- Tour March seminar in Dallas. Mr. cated approximately 60% to the stock Bollinger is market, 20% to the president of bond market, and Bollinger Capital 20% to the interna- Management. He tional stock mar- provides money ket. We are management primarily interme- services and diate term traders. publishes the Our research tends Capital Growth to center on a Letter. He is best holding period of known for his three to six months Bollinger Bands, with most of the which is a feature emphasis on six in TradingExpert. months. However, For information on that doesnt Bollinger Capital preclude us from The Opening Bell Monthly Managements John Bollinger, CFA, CMT taking advantage is a publication of products and of short term AIQ Incorporated services, call 310-798-8855 or write to opportunities, for example when we see David Vomund, Chief Analyst P.O. Box 3358, Manhattan Beach, CA an attractive technical non-confirma- P.O. Box 7530 90266. Send e-mail to tion. Incline Village, Nevada 89452 [email protected].