Forecasting Direction of Exchange Rate Fluctuations with Two Dimensional Patterns and Currency Strength

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Test of Macd Trading Strategy

A TEST OF MACD TRADING STRATEGY Bill Huang Master of Business Administration, University of Leicester, 2005 Yong Soo Kim Bachelor of Business Administration, Yonsei University, 200 1 PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF BUSINESS ADMINISTRATION In the Faculty of Business Administration Global Asset and Wealth Management MBA O Bill HuangIYong Soo Kim 2006 SIMON FRASER UNIVERSITY Fall 2006 All rights reserved. This work may not be reproduced in whole or in part, by photocopy or other means, without permission of the author. APPROVAL Name: Bill Huang 1 Yong Soo Kim Degree: Master of Business Administration Title of Project: A Test of MACD Trading Strategy Supervisory Committee: Dr. Peter Klein Senior Supervisor Professor, Faculty of Business Administration Dr. Daniel Smith Second Reader Assistant Professor, Faculty of Business Administration Date Approved: SIMON FRASER . UNI~ER~IW~Ibra ry DECLARATION OF PARTIAL COPYRIGHT LICENCE The author, whose copyright is declared on the title page of this work, has granted to Simon Fraser University the right to lend this thesis, project or extended essay to users of the Simon Fraser University Library, and to make partial or single copies only for such users or in response to a request from the library of any other university, or other educational institution, on its own behalf or for one of its users. The author has further granted permission to Simon Fraser University to keep or make a digital copy for use in its circulating collection (currently available to the public at the "lnstitutional Repository" link of the SFU Library website <www.lib.sfu.ca> at: ~http:llir.lib.sfu.calhandlell8921112~)and, without changing the content, to translate the thesislproject or extended essays, if .technically possible, to any medium or format for the purpose of preservation of the digital work. -

Spread, Volatility, and Volume Relationship in Financial Markets

Spread, volatility, and volume relationship in financial markets and market maker’s profit optimization Jack Sarkissian Managing Member, Algostox Trading LLC email: [email protected] Abstract We study the relationship between price spread, volatility and trading volume. We find that spread forms as a result of interplay between order liquidity and order impact. When trading volume is small adding more liquidity helps improve price accuracy and reduce spread, but after some point additional liquidity begins to deteriorate price. The model allows to connect the bid-ask spread and high-low bars to measurable microstructural parameters and express their dependence on trading volume, volatility and time horizon. Using the established relations, we address the operating spread optimization problem to maximize the market-maker’s profit. 1. Introduction When discussing security prices it is customary to describe them with single numbers. For example, someone might say price of Citigroup Inc. (ticker “C”) on April 18, 2016 was $45.11. While good enough for many uses, it is not entirely accurate. Single numbers can describe price only as referring to a particular transaction, in which 푁 units of security are transferred from one party to another at a price $푋 each. Price could be different a moment before or after the transaction, or if the transaction had different size, or if it were executed on a different exchange. To be entirely accurate, one should specify these numerous details when talking about security price. We will take this observation a step further. Technically speaking, other than at the time of transaction we cannot say that price exists as a single number at all. -

Stock Chart Pattern Recognition with Deep Learning

Stock Chart Pattern recognition with Deep Learning Marc Velay and Fabrice Daniel Artificial Intelligence Department of Lusis, Paris, France [email protected] http://www.lusis.fr June 2018 ABSTRACT the number of patterns recognized implies having a human examining candlestick charts in order to deduce signal char- This study evaluates the performances of CNN and LSTM acteristics before implementing the detection using condi- for recognizing common charts patterns in a stock historical tions specific to that pattern. Adding different parameters data. It presents two common patterns, the method used to to modulate ratios allows us to tweak the patterns’ charac- build the training set, the neural networks architectures and teristics. This technique does not have any generalization the accuracies obtained. potential. If the pattern is slightly outside of the defined Keywords: Deep Learning, CNN, LSTM, Pattern recogni- bounds, it will not be detected, even if a human would have tion, Technical Analysis classified it otherwise. Another solution is DTW3 which consists in computing 1 INTRODUCTION the distance between two time series. DTW allows us to Patterns are recurring sequences found in OHLC1 candle- recognize a pattern that could vary in size and length. To stick charts which traders have historically used as buy and use this algorithm, we must use reference time series, which sell signals. Several studies, notably by Bulkowski2, have have to be selected by a human. The references must gener- found some correlation between patterns and future trends, alize well when compared with signals similar to the pattern although to a limited extent. The correlations were found to in order to capture the whole range. -

Proquest Dissertations

INFORMATION TO USERS This manuscript has been reproduced from the microfilm master. UMI films the text directly from the original or copy sutxnitted. Thus, some thesis and dissertation copies are in typewriter face, while others may be from any type of computer printer. The quality of this reproduction is dependent upon the quality of the copy submitted. Broken or indisünct print, colored or poor quality illustrations and photographs, print bleedthrough, substandard margins, and improper alignment can adversely affect reproduction. In the unlikely event that the author did not send UMI a complete manuscript and there are missing pages, these will be noted. Also, if unauthorized copyright material had to be removed, a note will indicate the deletion. Oversize materials (e.g., maps, drawings, charts) are reproduced by sectioning the original, beginning at the upper left-hand comer and continuing from left to right in equal sections with small overlaps. Photographs included in the original manuscript have been reproduced xerographically in this copy. Higher quality 6” x 9” black and white photographic prints are available for any photographs or illustrations appearing in this copy for an additional charge. Contact UMI directly to order. Bell & Howell Information and Leaming 300 North Zeeb Road. Ann Arbor, Ml 48106-1346 USA 800-521-0600 UMÏ METAPHORS OF EXCHANGE AND THE SHANGHAI STOCK MARKET DISSERTATION Presented in Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy in the Graduate School o f The Ohio State University By Susan Diane Menke, M A ***** The Ohio State University 2000 Dissertation committee: Approved by: Dr. -

There's More to Volatility Than Volume

There's more to volatility than volume L¶aszl¶o Gillemot,1, 2 J. Doyne Farmer,1 and Fabrizio Lillo1, 3 1Santa Fe Institute, 1399 Hyde Park Road, Santa Fe, NM 87501 2Budapest University of Technology and Economics, H-1111 Budapest, Budafoki ut¶ 8, Hungary 3INFM-CNR Unita di Palermo and Dipartimento di Fisica e Tecnologie Relative, Universita di Palermo, Viale delle Scienze, I-90128 Palermo, Italy. It is widely believed that uctuations in transaction volume, as reected in the number of transactions and to a lesser extent their size, are the main cause of clus- tered volatility. Under this view bursts of rapid or slow price di®usion reect bursts of frequent or less frequent trading, which cause both clustered volatility and heavy tails in price returns. We investigate this hypothesis using tick by tick data from the New York and London Stock Exchanges and show that only a small fraction of volatility uctuations are explained in this manner. Clustered volatility is still very strong even if price changes are recorded on intervals in which the total transaction volume or number of transactions is held constant. In addition the distribution of price returns conditioned on volume or transaction frequency being held constant is similar to that in real time, making it clear that neither of these are the principal cause of heavy tails in price returns. We analyze recent results of Ane and Geman (2000) and Gabaix et al. (2003), and discuss the reasons why their conclusions di®er from ours. Based on a cross-sectional analysis we show that the long-memory of volatility is dominated by factors other than transaction frequency or total trading volume. -

The Strength of the Euro

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT A: ECONOMIC AND SCIENTIFIC POLICY The strength of the Euro Monetary Dialogue 14 July 2014 COMPILATION OF NOTES Abstract The notes in this compilation discuss the challenges for ECB monetary policy stemming from the recent appreciation of the Euro in the context of a nascent euro area recovery. The notes have been requested by the Committee on Economic and Monetary Affairs (ECON) as an input for the July 2014 session of the Monetary Dialogue between the Members of ECON and the President of the ECB. IP/A/ECON/NT/2014-02 July 2014 PE 518.782 EN This document was requested by the European Parliament's Committee on Economic and Monetary Affairs. AUTHORS Daniel GROS, Cinzia ALCIDI, Alessandro GIOVANNINI (Centre for European Policy Studies) Stefan COLLIGNON, Sebastian DIESSNER (Scuola Superiore Sant'Anna, London School of Economics) Ansgar BELKE (University of Duisburg-Essen) Sylvester C.W. EIJFFINGER, Louis RAES (Tilburg University) Guillermo DE LA DEHESA (Centre for Economic Policy Research) RESPONSIBLE ADMINISTRATOR Dario PATERNOSTER EDITORIAL ASSISTANT Iveta OZOLINA LINGUISTIC VERSIONS Original: EN ABOUT THE EDITOR Policy departments provide in-house and external expertise to support EP committees and other parliamentary bodies in shaping legislation and exercising democratic scrutiny over EU internal policies. To contact the Policy Department or to subscribe to its newsletter please write to: Policy Department A: Economic and Scientific Policy European Parliament B-1047 Brussels E-mail: [email protected] Manuscript completed in July 2014 © European Union, 2014 This document is available on the internet at: http://www.europarl.europa.eu/committees/en/econ/monetary-dialogue.html DISCLAIMER The opinions expressed in this document are the sole responsibility of the authors and do not necessarily represent the official position of the European Parliament. -

Point and Figure Relative Strength Signals

February 2016 Point and Figure Relative Strength Signals JOHN LEWIS / CMT, Dorsey, Wright & Associates Relative Strength, also known as momentum, has been proven to be one of the premier investment factors in use today. Numerous studies by both academics and investment ABOUT US professionals have demonstrated that winning securities continue to outperform. This phenomenon has been found Dorsey, Wright & Associates, a Nasdaq Company, is a in equity markets all over the globe as well as commodity registered investment advisory firm based in Richmond, markets and in asset allocation strategies. Momentum works Virginia. Since 1987, Dorsey Wright has been a leading well within and across markets. advisor to financial professionals on Wall Street and investment managers worldwide. Relative Strength strategies focus on purchasing securities that have already demonstrated the ability to outperform Dorsey Wright offers comprehensive investment research a broad market benchmark or the other securities in the and analysis through their Global Technical Research Platform investment universe. As a result, a momentum strategy and provides research, modeling and indexes that apply requires investors to purchase securities that have already Dorsey Wright’s expertise in Relative Strength to various appreciated quite a bit in price. financial products including exchange-traded funds, mutual funds, UITs, structured products, and separately managed There are many different ways to calculate and quantify accounts. Dorsey Wright’s expertise is technical analysis. The momentum. This is similar to a value strategy. There are Company uses Point and Figure Charting, Relative Strength many different metrics that can be used to determine a Analysis, and numerous other tools to analyze market data security’s value. -

Moving Average Convergence Divergence (MACD)

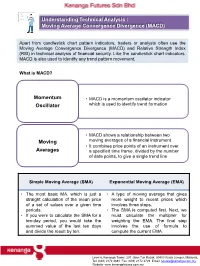

Understanding Technical Analysis : Moving Average Convergence Divergence (MACD) Apart from candlestick chart pattern indicators, traders or analysts often use the Hi 74.57 Moving Average Convergence Divergence (MACD) and Relative Strength Index Potential supply (RSI) in technical analysis of financial security. Like the candlestickdisruption chart indicators, due to MACD is also used to identify any trend pattern movement. attacks on two oil Brent tankers near Iran What is MACD? WTI Momentum • MACD is a momentum oscillator indicator WTI Oscillator which is used to identify trend formation Lo 2,237.40 (24 Mar 2020) • MACD shows a relationship betweenLo 18,591.93 two (24 Mar 2020) Moving moving averages of a financial instrument. • It combines price points of an instrument over Averages a specified time frame, divided by the number of data points, to give a single trend line Simple Moving Average (SMA) Exponential Moving Average (EMA) • The most basic MA, which is just a • A type of moving average that gives straight calculation of the mean price more weight to recent prices which of a set of values over a given time involves three steps. periods. • The SMA is computed first. Next, we • If you were to calculate the SMA for a must calculate the multiplier for ten-day period, you would take the weighting the EMA. The final step summed value of the last ten days involves the use of formula to and divide the result by ten. compute the current EMA. Level 6, Kenanga Tower, 237 Jalan Tun Razak, 50400 Kuala Lumpur, Malaysia. Tel: (603) 2172 3888 Fax: (603) 2172 2729 Email: [email protected] Website: www.kenangafutures.com.my How MACD works? MACD is generated by subtracting the long term EMAs (26 period) from the short term EMAs (12 periods) to form the main line known as MACD line. -

Active, Passive, Or a Third Way?

FEATURE | THE NEW GEOGRAPHY OF INVESTING RETHINKING FOREIGN EXCHANGE IN YOUR INVESTMENT PORTFOLIO: Active, Passive, or a Third Way? By David Cohen ack in 2009 I was fortunate enough Perhaps it’s time we rethink foreign exchange U.S. dollar, but during the past 43 years the to hear a leading bond fund manager (FX). yen has appreciated at an average annual Bspeak about the future. As he held up rate in excess of 3 percent. In January 1971, a $1 bill, he prophesized that one day we Passive currency management is most often the exchange rate of the Japanese yen to the would be telling our grandchildren about the default strategy for the following reasons: U.S. dollar was 358:1, and as of December these little pieces of paper that people used 2013 the exchange rate was about 103:1. to exchange for goods and services. The 1. Short-term currency movements gener- Whether this type of change in fundamen- history-mindful manager had a theory that ally are difficult to predict and the man- tal valuation is the natural evolution for the currency devaluation was the central bank agement of domestic currency valuation currency of a country progressing from an elixir to the developed-market financial fluctuations relative to foreign purchas- emerging market to a developed market is crisis. At the time, it seemed like just a sim- ing power does not factor into portfolio beyond the scope of this article. The data, ple prognostication, but in reality it was a performance evaluations. however, suggest that currency valuations prescient forecast of the beggar-thy-neigh- 2. -

With Cross-Border Investments, Realize That Currencies Will Mean Revert March 2021

By: Ivan Oscar Asensio, Ph.D., David Song SVB FX Risk Advisory for PE/VC Investors With cross-border investments, realize that currencies will mean revert March 2021 Key takeaways It’s important to consider Our machine learning model trained on The gravitational pull of mean reversion where a currency trades 30 years of data demonstrates that a currency may take years to take hold, so this relative to its historical hedging strategy based on SVB’s proprietary strategy is appropriate for private mean when allocating signals could add significant internal rate of equity and growth investors with capital overseas. return (IRR) to overseas investments. long-dated investment horizons. Currency: A major risk for private equity and venture investors, can be material and often overlooked The focus of this paper is to introduce an objective framework Private equity and venture investors tend to have long time to arrive at a hedging decision — horizons. Investments exited in 2019 had an average holding when to hedge and how much to period of almost six years, on average, according to Pitchbook. hedge — to maximize the economic Those long investment durations heighten currency risk for PE value of the hedges on the basis and VC investors who inherit foreign exchange (FX) risk as a by- of risk versus reward. product of allocating capital abroad. Cross-border investments typically are denominated in a foreign currency1, introducing the risk that depreciation in the destination currency between the entry and exit date could undermine the investment’s IRR. 6.02 Years Average holding period of 5.84 5.82 5.76 private equity investments 5.91 5.80 5.75 5.47 5.04 5.31 4.52 4.45 4.33 4.27 4.34 4.07 4.23 4.29 4.26 3.77 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 Source: Pitchbook, August 1, 2019 1 Applies when both the acquisition and the exit price are denominated in a foreign currency. -

Candlesticks, Fibonacci, and Chart Pattern Trading Tools

ffirs.qxd 6/17/03 8:17 AM Page iii CANDLESTICKS, FIBONACCI, AND CHART PATTERN TRADING TOOLS A SYNERGISTIC STRATEGY TO ENHANCE PROFITS AND REDUCE RISK ROBERT FISCHER JENS FISCHER JOHN WILEY & SONS, INC. ffirs.qxd 6/17/03 8:17 AM Page iii ffirs.qxd 6/17/03 8:17 AM Page i CANDLESTICKS, FIBONACCI, AND CHART PATTERN TRADING TOOLS ffirs.qxd 6/17/03 8:17 AM Page ii Founded in 1870, John Wiley & Sons is the oldest independent publishing company in the United States. With offices in North America, Europe, Australia, and Asia, Wiley is globally committed to developing and market- ing print and electronic products and services for our customers’ professional and personal knowledge and understanding. The Wiley Trading series features books by traders who have survived the market’s ever-changing temperament and have prospered—some by re- investing systems, others by getting back to basics. Whether a novice trader, professional, or somewhere in-between, these books will provide the advice and strategies needed to prosper today and well into the future. For a list of available titles, visit our web site at www.WileyFinance.com. ffirs.qxd 6/17/03 8:17 AM Page iii CANDLESTICKS, FIBONACCI, AND CHART PATTERN TRADING TOOLS A SYNERGISTIC STRATEGY TO ENHANCE PROFITS AND REDUCE RISK ROBERT FISCHER JENS FISCHER JOHN WILEY & SONS, INC. ffirs.qxd 6/17/03 8:17 AM Page iv Copyright © 2003 by Robert Fischer, Dr. Jens Fischer. All rights reserved. Published by John Wiley & Sons, Inc., Hoboken, New Jersey. Published simultaneously in Canada. PHI-spirals, PHI-ellipse, PHI-channel, and www.fibotrader.com are registered trademarks and protected by U.S. -

Technical-Analysis-Bloomberg.Pdf

TECHNICAL ANALYSIS Handbook 2003 Bloomberg L.P. All rights reserved. 1 There are two principles of analysis used to forecast price movements in the financial markets -- fundamental analysis and technical analysis. Fundamental analysis, depending on the market being analyzed, can deal with economic factors that focus mainly on supply and demand (commodities) or valuing a company based upon its financial strength (equities). Fundamental analysis helps to determine what to buy or sell. Technical analysis is solely the study of market, or price action through the use of graphs and charts. Technical analysis helps to determine when to buy and sell. Technical analysis has been used for thousands of years and can be applied to any market, an advantage over fundamental analysis. Most advocates of technical analysis, also called technicians, believe it is very likely for an investor to overlook some piece of fundamental information that could substantially affect the market. This fact, the technician believes, discourages the sole use of fundamental analysis. Technicians believe that the study of market action will tell all; that each and every fundamental aspect will be revealed through market action. Market action includes three principal sources of information available to the technician -- price, volume, and open interest. Technical analysis is based upon three main premises; 1) Market action discounts everything; 2) Prices move in trends; and 3) History repeats itself. This manual was designed to help introduce the technical indicators that are available on The Bloomberg Professional Service. Each technical indicator is presented using the suggested settings developed by the creator, but can be altered to reflect the users’ preference.