6 Bollinger Bands® Trading Strategies + Video

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Estimating 90-Day Market Volatility with VIX and VXV

Estimating 90-Day Market Volatility with VIX and VXV Larissa J. Adamiec, Corresponding Author, Benedictine University, USA Russell Rhoads, Tabb Group, USA ABSTRACT The CBOE Volatility Index (VIX) has historically been a consistent indicator of 30-day or 1-month (21-day actual) realized market volatility. In addition, the Chicago Board Options Exchange also quotes the CBOE 3-Month Volatility Index (VXV) which indicates the 3-month realized market volatility. This study demonstrates both VIX and VXV are still reliable indicators of their respective realized market volatility periods. Both of the indexes consistently overstate realized volatility, indicating market participants often perceive volatility to be much higher than volatility actually is. The overstatement of expected volatility leads to an indicator which is consistently higher. Perceived volatility in the long-run is often lower than volatility in the short-run which is why VXV is often lower than VIX (VIX is usually lower than VXV). However, the accuracy of the VXV is roughly 35% as compared with the accuracy of the VIX at 60.1%. By combining the two indicators to create a third indicator we were able to provide a much better estimate of 64-Day Realized volatility, with an accuracy rate 41%. Due to options often being over-priced, historical volatility is often higher than both realized volatility or the volatility index, either the VIX or the VXV. Even though the historical volatility is higher we find the estimated historical volatility to be more easily estimated than realized volatility. Using the same time period from January 2, 2008 through December 31, 2016 we find the VIX estimates the 21-Day Historical Volatility with 83.70% accuracy. -

Copyrighted Material

Index 12b-1 fee, 68–69 combining with Western analysis, 3M, 157 122–123 continuation day, 116 ABC of Stock Speculation, 157 doji, 115 accrual accounting, 18 dragonfl y doji, 116–117 accumulated depreciation, 46–47 engulfi ng pattern, 120, 121 accumulation phase, 158 gravestone doji, 116, 117, 118 accumulation/distribution line, hammer, 119 146–147 hanging man, 119 Adaptive Market Hypothesis, 155 harami, 119, 120 Altria, 29, 127, 185–186 indicators 120 Amazon.com, 151 long, 116, 117, 118 amortization, 47, 49 long-legged doji, 118 annual report, 44–46 lower shadow, 115 ascending triangle, 137–138, 140 marubozu, 116 at the money, 192 real body, 114–115 AT&T, 185–186 segments illustrated, 114 shadows, 114 back-end sales load, 67–68 short,116, 117 balance sheet, 46–50 spinning top, 118–119 balanced mutual funds, 70–71 squeeze alert, 121, 122, 123 basket of stocks, 63 tails, 114 blue chip companies, 34 three black crows, 122, 123 Boeing, 134–135 three white soldiers, 122, 123 book value, 169 trend-based, 117–118 breadth, 82–83, 97 upper shadow, 115 breakaway gap, 144 wicks, 114 break-even rate, 16–17 capital assets, 48, 49 breakout, 83–84, 105–106 capitalization-based funds, 71 Buffett, Warren, 152 capitalization-weighted average, 157 bull and bear markets,COPYRIGHTED 81, 174–175 Caterpillar, MATERIAL 52–54, 55, 57, 58, 59, 131 Bureau of Labor Statistics (BLS), 15 CBOE Volatility Index (VIX), 170, 171 Buy-and-hold strategy, 32, 204–205 Chaikin Money Flow (CMF), 146 buy to open/sell to open, 96 channel, 131–132 charting calendar spreads, 200–201 -

Calibration of Bollinger Bands Parameters for Trading Strategy Development in the Baltic Stock Market

ISSN 1392 – 2785 Inzinerine Ekonomika-Engineering Economics, 2010, 21(3), 244-254 Calibration of Bollinger Bands Parameters for Trading Strategy Development in the Baltic Stock Market Audrius Kabasinskas, Ugnius Macys Kaunas University of Technology K. Donelaicio st. 73, LT-44029, Kaunas, Lithuania e-mail: [email protected], [email protected] In recent decades there was a robust boom in "Bollinger plotter" was developed using the most investment sector in Lithuania, as more people chose to popular mathematical toolbox MatLab in order to solve invest money in investment funds rather than keep money in stated problems. Application is capable of charting the closet. The Baltic States Market turnover has increased Bollinger Bands and 6 other technical indicators with from 721 MEUR in 2000 to 978 MEUR in 2008 (with peak desired period of time. This software is not a fully 2603 MEUR in 2005). When difficult period appeared in automated decision making system, as decisions are global markets, a lot of attention was dedicated towards the usually made based on value judgment. managing of investments. Investment management firms in Since the stock returns usually have distributions with Lithuania gain significance in personal as well as in fat tails, then less than 95% of data fit in the Bollinger business section increasingly; even though these firms are trading channels. However the Bollinger bands trading considerably young (the first one in Lithuania was signals were supported by additional indicators (e.g. %b), established in year 2000). so the loss of data is not significant. Successful investment begins with the financial Our calibration results show that short term investor analysis of stock, asset or index, which you are going to should apply 10 days moving average and use a trading invest. -

FOREX WAVE THEORY.Pdf

FOREX WAVE THEORY This page intentionally left blank FOREX WAVE THEORY A Technical Analysis for Spot and Futures Currency Traders JAMES L. BICKFORD McGraw-Hill New York Chicago San Francisco Lisbon London Madrid Mexico City Milan New Delhi San Juan Seoul Singapore Sydney Toronto Copyright © 2007 by The McGraw-Hill Companies. All rights reserved. Manufactured in the United States of America. Except as permitted under the United States Copyright Act of 1976, no part of this publication may be reproduced or distributed in any form or by any means, or stored in a database or retrieval system, without the prior written permission of the publisher. 0-07-151046-X The material in this eBook also appears in the print version of this title: 0-07-149302-6. All trademarks are trademarks of their respective owners. Rather than put a trademark symbol after every occurrence of a trademarked name, we use names in an editorial fashion only, and to the benefit of the trademark owner, with no intention of infringement of the trademark. Where such designations appear in this book, they have been printed with initial caps. McGraw-Hill eBooks are available at special quantity discounts to use as premiums and sales pro- motions, or for use in corporate training programs. For more information, please contact George Hoare, Special Sales, at [email protected] or (212) 904-4069. TERMS OF USE This is a copyrighted work and The McGraw-Hill Companies, Inc. (“McGraw-Hill”) and its licen- sors reserve all rights in and to the work. Use of this work is subject to these terms. -

Asset Allocation POINT WHAT DOES a LOW VIX TELL US June 2017 ABOUT the MARKET? Timely Intelligence and Analysis for Our Clients

PRICE Asset Allocation POINT WHAT DOES A LOW VIX TELL US June 2017 ABOUT THE MARKET? Timely intelligence and analysis for our clients. KEY POINTS . The financial press has been paying considerable attention lately to the Chicago Board Options Exchange Volatility Index (VIX), with many financial pundits citing recent low readings on the VIX as evidence of investor complacency and rising equity risk. Robert Harlow, CFA, CAIA . Quantitative Analyst Media coverage often implies that a low current VIX is a strong signal of expected Asset Allocation future volatility and will be followed by a sell-off in U.S. equities and other risk-seeking assets. Historical evidence shows that, over the near term, investors typically overestimate the next 30-day volatility of the S&P 500 Index. Further, when the VIX has been low, U.S. equities have outperformed U.S. bonds on average over the next 12 months, regardless of the change in the VIX over that horizon. Without a meaningful and prolonged catalyst, we do not believe a low level of the VIX David Clewell, CFA alone implies investor complacency or an immediate danger of a risk-off event. Research Analyst Asset Allocation BACKGROUND There has been much discussion in the financial press recently about the danger of investor complacency—with a low VIX frequently cited as compelling evidence that equity investors have grown too relaxed about potential risks. The problem is that it is difficult to determine whether markets are truly complacent or not; we can’t survey all investors and, even if we could, how many investors would admit that they were complacent? Instead, we take a mental shortcut and presume that something we can measure is a good proxy for the thing we actually care about. -

Modeling and Analyzing Stock Trends

Modeling and Analyzing Stock Trends A Major Qualifying Project Submitted to the Faculty of Worcester Polytechnic Institute in partial fulllment of the requirements for the Degree in Bachelor of Science Mathematical Sciences By Laura Cintron Garcia Date: 5/6/2021 Advisor: Dr. Mayer Humi This report represents work of WPI undergraduate students submitted to the faculty as evidence of a degree requirement. WPI routinely publishes these reports on its web site without editorial or peer review. For more information about the projects program at WPI, see http://www.wpi.edu/Academics/Projects 1 Abstract Abstract The goal of this project is to create and compare several dierent stock prediction models and nd a correlation between the predic- tions and volatility for each stock. The models were created using the historical data, DJI index, and moving averages. The most accurate prediction model had an average of 5.3 days spent within a predic- tion band. A correlation of -0.0438 was found between that model an a measure of volatility, indicating that more prediction days means lower volatility. 2 2 Acknowledgments Without the help of some people, it would have been signicantly more di- cult to complete this project without a group. I want to extend my gratitude to Worcester Polytechnic Institute and the WPI Math Department for their great eorts and success this year regarding school and projects during the pandemic. They did everything they could to ensure these projects was still a rich experience for the students despite everything. I would also like to thank my MQP advisor, Professor Mayer Humi for his assistance and guidance on this project, for allowing me to work indepen- dently while always being willing to meet with me or answer any questions, and for continuously encouraging me to do what I thought was best for the project. -

Futures & Options on the VIX® Index

Futures & Options on the VIX® Index Turn Volatility to Your Advantage U.S. Futures and Options The Cboe Volatility Index® (VIX® Index) is a leading measure of market expectations of near-term volatility conveyed by S&P 500 Index® (SPX) option prices. Since its introduction in 1993, the VIX® Index has been considered by many to be the world’s premier barometer of investor sentiment and market volatility. To learn more, visit cboe.com/VIX. VIX Futures and Options Strategies VIX futures and options have unique characteristics and behave differently than other financial-based commodity or equity products. Understanding these traits and their implications is important. VIX options and futures enable investors to trade volatility independent of the direction or the level of stock prices. Whether an investor’s outlook on the market is bullish, bearish or somewhere in-between, VIX futures and options can provide the ability to diversify a portfolio as well as hedge, mitigate or capitalize on broad market volatility. Portfolio Hedging One of the biggest risks to an equity portfolio is a broad market decline. The VIX Index has had a historically strong inverse relationship with the S&P 500® Index. Consequently, a long exposure to volatility may offset an adverse impact of falling stock prices. Market participants should consider the time frame and characteristics associated with VIX futures and options to determine the utility of such a hedge. Risk Premium Yield Over long periods, index options have tended to price in slightly more uncertainty than the market ultimately realizes. Specifically, the expected volatility implied by SPX option prices tends to trade at a premium relative to subsequent realized volatility in the S&P 500 Index. -

An Interview with John Bollinger

® AIQ Opening BellMonthly IN THIS ISSUE VOL. 6 ISSUE 2 FEBRUARY 1997 TRADING TECHNIQUES Feature John Bollinger discusses his Bollinger Bands .................. 1 AN INTERVIEW WITH JOHN BOLLINGER Se ctions account program, what percent of the By David Vomund investments are in equities and what is Price Volume Divergence your average holding period? Report .................................. 5 his month we are pleased to JB: We are primarily equity Market Review ..................... 8 present an interview with John investors. We dont buy any futures. Data Maintenance ............... 8 Bollinger, a keynote speaker at Our growth model is currently allo- Tour March seminar in Dallas. Mr. cated approximately 60% to the stock Bollinger is market, 20% to the president of bond market, and Bollinger Capital 20% to the interna- Management. He tional stock mar- provides money ket. We are management primarily interme- services and diate term traders. publishes the Our research tends Capital Growth to center on a Letter. He is best holding period of known for his three to six months Bollinger Bands, with most of the which is a feature emphasis on six in TradingExpert. months. However, For information on that doesnt Bollinger Capital preclude us from The Opening Bell Monthly Managements John Bollinger, CFA, CMT taking advantage is a publication of products and of short term AIQ Incorporated services, call 310-798-8855 or write to opportunities, for example when we see David Vomund, Chief Analyst P.O. Box 3358, Manhattan Beach, CA an attractive technical non-confirma- P.O. Box 7530 90266. Send e-mail to tion. Incline Village, Nevada 89452 [email protected]. -

Investing with Bollinger Bands

Investing with Bollinger Bands This article was written some years ago, but is very relevant to today. The charts used to illustrate the text are now somewhat dated, but still relevant for the present purpose of teaching a technique. As moving averages became more popular, some analysts noticed that when prices were moving upward, they had a tendency to rise only so far above the moving average. When prices were falling they tended to fall only so far below the moving average. How far they rose or fell seemed to vary from stock to stock and also from time to time. However, the tendency was so consistent that it could be useful to both traders and investors. These early analysts hit on the idea of drawing lines a certain percentage of the moving average above and below the moving average line. They selected the percentage stock-by-stock so that it seemed to catch most of the price action on the chart, typically 90% or more of the price action. GWT - GWA INTERNATIONAL > -2 to 291 D @ D 020103-070604 320 MOV AVS 22(0) 5 band 310 300 290 280 270 260 250 240 230 JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC JAN FEB MAR APR MAY JUN 03 04 Chart 1: Daily Line Chart of GWA International with a 22-day Moving Average and 5% Bands The result was something like Chart 1, where we have a daily line chart, on which is drawn a 22-day moving average, with 5% bands above and below it. -

COVID-19 Update Overview

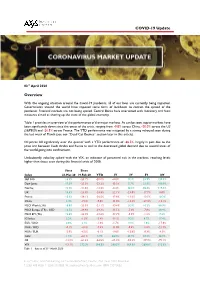

COVID-19 Update 03rd April 2020 Overview With the ongoing situation around the Covid-19 pandemic, all of our lives are currently being impacted. Governments around the world have imposed some form of lockdown to contain the spread of the pandemic. Financial markets are not being spared. Central Banks have intervened with monetary and fiscal measures aimed at shoring up the state of the global economy. Table 1 provides an overview of the performance of the major markets. As can be seen, equity markets have been significantly down since the onset of the crisis, ranging from -9.8% across China, -20.0% across the US (S&P500) and -26.5% across France. The YTD performance was mitigated by a strong rebound seen during the last week of March (see our “Dead Cat Bounce” section later in this article). Oil prices fell significantly over the quarter with a YTD performance of -66.5%, largely in part due to the price war between Saudi Arabia and Russia as well as the decreased global demand due to several areas of the world going into confinement. Undoubtedly volatility spiked with the VIX, an indicator of perceived risk in the markets, reaching levels higher than those seen during the financial crisis of 2008. Since Since Index 23-Mar-20 19-Feb-20 YTD 1Y 3Y 5Y 10Y S&P 500 15.5% -23.7% -20.0% -8.8% 9.1% 23.9% 120.3% Dow Jones 17.9% -25.3% -23.2% -15.5% 5.7% 21.9% 100.9% Nasdaq 12.2% -21.6% -14.2% -0.4% 30.2% 55.6% 219.4% UK 13.6% -23.9% -24.8% -22.1% -23.0% -17.7% 0.0% France 12.3% -28.1% -26.5% -17.8% -13.6% -13.5% 10.3% China 3.4% -7.6% -9.8% -11.0% -

The DB Currency Volatility Index (CVIX): a Benchmark for Volatility

Global Foreign Excahnge Deutsche Bank@ October 2007 Deutsche Bank Guide To Currency Indices Global Markets Saravelos Global Hzead Global Head FX StrategyBilal Jason Rashid James Torquil George Hafeez Batt Hoosenally Malcolm Wheatley Editor Contributors George Saravelos Mirza Baig Jason Batt Bilal Hafeez FX Strategy EM FX Strategy Global Head Global Head FX Index Products FX Strategy Rashid Hoosenally Caio Natividade James Malcolm Global Head FX Derivatives Strategy EM FX Strategy Global Risk Strategy Deutsche Bank@ Guide to Currency Indices October 2007 Table of Contents Introduction............................................................................................................................. 3 Overview ................................................................................................................................ 4 The Deutsche Bank Menu of Currency Indices...................................................................... 7 Currency Markets: Money Left on the Table?........................................................................ 9 Tactical Currency Indices DB G10 Trade-Weighted Indices: From Theory to Practice.................................................. 18 DB EM Asia Policy Baskets .................................................................................................. 22 The Emerging Asia Reserves, Liquidity and Yield (EARLY) Index......................................... 26 The DB Currency Volatility Index (CVIX): A Benchmark for Volatility ................................... -

Earth & Sky Trading System

Earth & Sky Trading System By Pierre Du Plessis 1 Copyright © Forex Mentor Pro 2011. All rights reserved. Any redistribution or reproduction of part or all of the contents in any form is prohibited other than the following: You may print or download to a local hard disk copies for your personal and non- commercial use only; You may not, except with our express written permission, distribute or commercially exploit the content. Nor may you transmit it or store it in any other website or other form of electronic retrieval system. Risk Disclosure Statement The contents of this e-Book are for informational purposes only. No part of this publication is a solicitation or an offer to buy or sell any financial market. Examples are provided for illustration purposes only and should not be construed as investment advice or strategy. All trade examples are hypothetical. No representation is made that any account or trader will or is likely to achieve profits or loses similar to those discussed in this e-Book. By purchasing this e-Book, and/or subscribing to our mailing list you will be deemed to have accepted these and all other terms found on our web page ForexMentorPro.com in full. The information found in this e-Book is not intended for distribution to, or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to the law or regulation or which would subject us to any registration requirement within such jurisdiction or country. CFTC RULE 4.41 HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS.