Financial Reporting in the Power and Utilities Industry

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Accounting for Inventories – Write-Off, Write- Down Or Deletion

FINANCIAL ADMINISTRATION MANUAL Issue Date: Effective Date: Responsible Agency: September Immediate Comptroller General 2009 Directive No: 704-4 Chapter: Accounting for Expenditures Directive Title: ACCOUNTING FOR INVENTORIES – WRITE-OFF, WRITE- DOWN OR DELETION 1. POLICY All write-off or deletion of inventory must be in accordance with S.24 or S.64 of the Financial Administration Act (FAA) and this directive. All write-downs must be in accordance with the recommendations of the Public Sector Accounting Board of the Canadian Institute of Chartered Accountants. 2. DEFINITIONS 2.1. Write-off of inventory A write-off of inventory occurs when the inventory can no longer provide any economic benefit to the Government. This may be because it has been damaged, lost, stolen, become obsolete or for some reason no longer has any economic value. The inventory may or may not physically exist. The value of this material that had been carried in the financial records must be written-off. Write-offs of inventory tend to be caused by involuntary acts and usually do not involve any judgment on the part of the public official. Examples of situations that require a write-off are when a property has been damaged beyond repair, is destroyed by fire or has been stolen. Write-offs can be required for inventory within a revolving fund and for inventories carried outside a revolving fund. Deletions, mentioned below, can only occur when the inventory is held within a revolving fund. 2.2. Deletions from a revolving fund Deletions from inventory in a revolving fund occur when the physical inventory is still on hand but its economic benefit has been reduced to an insignificant amount. -

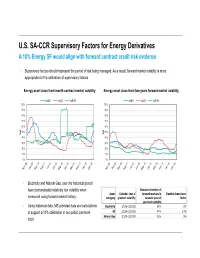

U.S. SA-CCR Supervisory Factors for Energy Derivatives a 10% Energy SF Would Align with Forward Contract Credit Risk Evidence

U.S. SA-CCR Supervisory Factors for Energy Derivatives A 10% Energy SF would align with forward contract credit risk evidence • Supervisory factors should represent the period of risk being managed. As a result, forward market volatility is more appropriate for the calibration of supervisory factors Energy asset class front month contract market volatility Energy asset class front two years forward market volatility VolNG VolOil VolPJM VolNG VolOil VolPJM 100% 100% 90% 90% 80% 80% 70% 70% 60% 60% 50% 50% Vol Vol 40% 40% 30% 30% 20% 20% 10% 10% 0% 0% • Electricity and Natural Gas, over the historical period have demonstrated relatively low volatility when Standard deviation of Asset Calendar year of forward markets in Implied Supervisory measured using forward market history. category greatest volatility calendar year of Factor greatest volatility • Using historical data, MS provided data and calculations Electricity 1/1/08-12/31/08 24% 6% to support a 10% calibration in our public comment Oil 1/1/08-12/31/08 47% 13% Natural Gas 1/1/09-12/31/09 32% 9% letter 1 U.S. SA-CCR Supervisory Factors for Energy Derivatives A 10% Energy SF would align with credit risk in energy derivative transactions 1. Cal18 WTI Swap Pricing: Notional BBLs x Cal18 Prices 2. Cal18 WTI MTM vs SA-CCR vs Mean Positive Exposure 150 90 Oil 1 0 /12 450 1 /10 80 1 1 100 /11 /8 1 1 350 /9 /6 70 1 1 /7 /4 1 1 50 /5 /2 60 250 1 1 /3 50 - $MM 150 $MM 40 $/BBL 50 (50) 30 20 -50 (100) 10 -150 (150) 0 Cal18 MTM SA-CCR RWA Exposure at 40% SF Cal18 MTM ($MM) Notional Quantity (BBLs) * SA-CCR RWA Exposure at 10% SF Max Mean Positive Exposure Cal18 Price ($/BBL) 1/# Spot Contribution to MTM • Energy derivative counterparty credit risk exposures decline, • A 10% Supervisory Factor correctly aligns SA-CCR month by month, as the transaction nears maturity since the credit risk measurements with other reliable counterparty remaining total notional quantity declines credit risk measures (i.e. -

Derivatives and Risk Management in the Petroleum, Natural Gas, and Electricity Industries

SR/SMG/2002-01 Derivatives and Risk Management in the Petroleum, Natural Gas, and Electricity Industries October 2002 Energy Information Administration U.S. Department of Energy Washington, DC 20585 This report was prepared by the Energy Information Administration, the independent statistical and analytical agency within the U.S. Department of Energy. The information contained herein should be attributed to the Energy Information Administration and should not be construed as advocating or reflecting any policy position of the Department of Energy or any other organization. Service Reports are prepared by the Energy Information Administration upon special request and are based on assumptions specified by the requester. Contacts This report was prepared by the staff of the Energy The Energy Information Administration would like to Information Administration and Gregory Kuserk of the acknowledge the indispensible help of the Commodity Commodity Futures Trading Commission. General Futures Trading Commission in the research and writ- questions regarding the report may be directed to the ing of this report. EIA’s special expertise is in energy, not project leader, Douglas R. Hale. Specific questions financial markets. The Commission assigned one of its should be directed to the following analysts: senior economists, Gregory Kuserk, to this project. He Summary, Chapters 1, 3, not only wrote sections of the report and provided data, and 5 (Prices and Electricity) he also provided the invaluable professional judgment Douglas R. Hale and perspective that can only be gained from long expe- (202/287-1723, [email protected]). rience. The EIA staff appreciated his exceptional pro- ductivity, flexibility, and good humor. -

Long-Term Swings and Seasonality in Energy Markets Working Paper Nº 1929

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by EPrints Complutense Long-term swings and seasonality in energy markets Instituto Manuel Moreno Complutense Department of Economic Analysis and Finance, University of Castilla-La Mancha, Toledo, Spain de Análisis Económico Alfonso Novales Instituto Complutense de Análisis Económico (ICAE), and Department of Economic Analysis, Facultad de Ciencias Económicas y Empresariales, Universidad Complutense, Madrid, Spain Federico Platania Léonard de Vinci Pôle Universitaire, Paris La Défense, France Abstract This paper introduces a two-factor continuous-time model for commodity pricing under the assumption that prices revert to a stochastic mean level, which shows smooth, periodic fluctuations over long periods of time. We represent the mean reversion price by a Fourier series with a stochastic component. We also consider a seasonal component in the price level, an essential characteristic of many commodity prices, which we represent again by a Fourier series. We obtain analytical pricing expressions for futures contracts. Using futures price data on Natural Gas, we provide evidence on the presence of long-term fluctuations and show how to estimate the long-term component simultaneously with a seasonal component using the Kalman filter. We analyse the in-sample and out-of-sample empirical performance of our pricing model with and without a seasonal component and compare it with the Schwartz and Smith (2000) model. Our findings show the in-sample and out-of-sample superiority of our model with seasonal fluctuations, thereby providing a simple and powerful tool for portfolio management, risk management, and derivative pricing. -

Ipsas 12—Inventories

IPSAS 12—INVENTORIES Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 2 (Revised 2003), “Inventories,” published by the International Accounting Standards Board (IASB). Extracts from IAS 2 are reproduced in this publication of the International Public Sector Accounting Standards Board (IPSASB) of the International Federation of Accountants (IFAC) with the permission of the International Accounting Standards Committee Foundation (IASCF). The approved text of the International Financial Reporting Standards (IFRSs) is that published by IASB in the English language, and copies may be obtained directly from IASB Publications Department, 30 Cannon Street, London EC4M 6XH, United Kingdom. E-mail: [email protected] Internet: http://www.iasb.org IFRSs, IASs, Exposure Drafts, and other publications of the IASB are copyright of the IASCF. “IFRS,” “IAS,” “IASB,” “IASCF,” “International Accounting Standards,” and “International Financial Reporting Standards” are trademarks of the IASCF and should not be used without the approval of the IASCF. IPSAS 12 314 December 2006 IPSAS 12—INVENTORIES CONTENTS Paragraph SECTOR PUBLIC Introduction ............................................................................................. IN1–IN14 Objective .................................................................................................. 1 Scope ....................................................................................................... 2–8 -

The Impact of Energy Derivatives on the Crude Oil Market

THE JAMES A. BAKER III INSTITUTE FOR PUBLIC POLICY OF RICE UNIVERSITY THE IMPACT OF ENERGY DERIVATIVES ON THE CRUDE OIL MARKET JEFF FLEMING ASSISTANT PROFESSOR OF FINANCE JONES SCHOOL OF MANAGEMENT, RICE UNIVERSITY BARBARA OSTDIEK ASSISTANT PROFESSOR OF FINANCE JONES SCHOOL OF MANAGEMENT, RICE UNIVERSITY THE IMPACT OF ENERGY DERIVATIVES ON THE CRUDE OIL MARKET Introduction Beginning in the 1970s, deregulation dramatically increased the degree of price uncertainty in the energy markets, prompting the development of the first exchange- traded energy derivative securities. The success and growth of these contracts attracted a broader range of participants to the energy markets and stimulated trading in an even wider variety of energy derivatives. Today, many exchanges and over-the-counter markets worldwide offer futures, futures options, swap contracts, and exotic options on a broad range of energy products, including crude oil, fuel oil, gasoil, heating oil, unleaded gasoline, and natural gas. It is well known that derivative securities provide economic benefits. The key attribute of these securities is their leverage (i.e., for a fraction of the cost of buying the underlying asset, they create a price exposure similar to that of physical ownership). As a result, they provide an efficient means of offsetting exposures among hedgers or transferring risk from hedgers to speculators. In addition, derivatives promote information dissemination and price discovery. The leverage and low trading costs in these markets attract speculators, and as their presence increases, so does the amount of information impounded into the market price. These effects ultimately influence the underlying commodity price through arbitrage activity, leading to a more broadly based market in which the current price corresponds more closely to its true value. -

Energy Derivatives and Risk Management

Department of Business and Management Master thesis in Advanced Corporate Finance ENERGY DERIVATIVES AND RISK MANAGEMENT SUPERVISOR: CANDIDATE: Prof. Raffaele Oriani Alessia Gidari 643081 CO-SUPERVISOR: Prof. Simone Mori ACADEMIC YEAR 2012-2013 1 Table of contents Abstract ...........................................................................................................................4 Introduction......................................................................................................................5 1. Risk management 1.1. A brief historical background……………………………………………………………….9 1.2. Risk definition and measurement……………………………………………………….10 1.3. The risk in corporate finance……………………………………………………………….12 1.4. The reasons for hedging……………………………………………………………………..13 1.5. The risk in capital investment……………………………………………………………..15 1.6. From hedging to risk management……………………………………………………..17 2. Enterprise risk management 2.1. Definition……………………………………………………………………………………………19 2.2. Implementation………………………………………………………………………………….20 2.3. Case studies in literature…………………………………………………………………….23 2.4. Empirical observations………………………………………………………………………..26 2.5. Evolution of risk management…………………………………………………………….32 3. The quantitative tools of risk management 3.1. The Black-Scholes model…………………………………………………………………….35 3.2. The main VaR methodologies……………………………………………………………..37 3.2.1. The historical simulation…………………………………………………………38 3.2.2. The Variance-covariance or analytical method……………………….39 3.2.3. The Monte Carlo method………………………………………………………..41 -

A Market Consistent Gas Storage Modelling Framework: Valuation, Calibration, & Model Risk

A Market Consistent Gas Storage Modelling Framework: Valuation, Calibration, & Model Risk by Greg Kiely B.Sc, National University of Ireland, Galway, (1st Hons.) M.Sc University of Limerick, (1st Hons.) Submitted to the Department of Accounting and Finance, Kemmy Business School, University of Limerick in December 2015, in partial fulfillment of the requirements for the degree of Doctor of Philosophy Abstract A typical natural gas derivatives book within an energy trading business, bank, or even large utility will generally be exposed to two broad categories of market risk. The first being outright price volatility, where contracts such as caps/floors, options and swing, will have a non-linear exposure to the variability of the gas price level. The second, although equally as prominent, is time-spread volatility where gas storage, take-or-pay contracts, and calendar spread options will be exposed to the realized variability of different time-spreads. Developing a market consistent valuation framework capable of capturing both risk exposures, and thus allowing for risk diversification within a natural gas trading book, is the primary goal of this thesis. To accomplish this, we present a valuation methodology which is capable of pricing the two most actively traded natural gas derivative contracts, namely monthly options and storage, in a consistent manner. The valuation of the former is of course trivial as the prices are set by the market, therefore the primary focus of this thesis is in obtaining market-based pricing measures for the purpose of storage valuation. A consistent pricing and risk management framework will, by definition, accurately reflect the cost of hedging both outright and spread volatility and thus our work can be viewed as a ba- sis capable of incorporating the other less actively traded contracts listed above. -

Characteristics of Inventories

Characteristics of Inventories • belong to current assets • kept in stock either to be sold to customers or to be consumed by activities of the accounting entity • Retailer, wholesaler – merchandise inventory • Manufacturer – finished goods – work in progress: goods not yet ready for sale – raw materials and purchased parts • Most relevant standard: IAS 2 • Aside: optimal level of inventory – trade-off between holding costs, ordering cost, service level, customer satisfaction, smooth production 1 The Inventory Balance Equation • Value of inventory at time t = Initial inventory + inflows – outflows up to t – initial inventory: from past period; zero at start of business • depends on valuation method used for inflows and outflows – inflows: valued at cost • same as for fixed assets: „all costs incurred in order to bring the inventories to their present location and condition“ – outflows: different approaches • direct identification • assumed order of depletion • averaging – determine market value of ending inventory and apply balance equation 2 Importance of Inventory Valuation • inventory valuation affects the income statement and the balance sheet • impact on ratios used in financial statement analysis • The Gross Profit Equation: Gross profit = Sales Revenue ⎧ ⎪ -( beginning inventory ⎪ COGS ⎨ ⎪ +purchases ⎩⎪ – ending inventory) • Effect of inventory valuation on gross profit: – closing inventory understated (overstated) Î gross profit for the period understated (overstated) – opening inventory understated (overstated) Î gross profit -

18. Energy Futures Markets for Managing Risk

Self Test Energy Futures Markets for Managing Risk Click on True or False to test your knowledge of the chapter. 1. True False Riskiness of the energy industry is perceived as a "chance of loss" in the popular sense. 2. True False Financial risk includes the possibility of accidents that have health and safety implications, examples such as power plant melt down, oil spill, an LNG explosion, smog etc. 3. True False There are six types of financial risk including market, credit, premium, liquidity, operational, and legal. 4. True False A risk neutral individual would be indifferent between $200 and an asset that has 20% chance of paying $1000 and 80% chance of paying nothing. 5. True False To find the optimal hedge ratio (the ratio which minimizes risk or variance), we T use the following formula: δ = ρ + μ+ (lnSt - lnFt )/T. 6. True False The efficient market hypothesis suggests that the spot price plus any necessary risk premium (RP) is a good predictor of future energy prices. 7. True False A derivative is a financial instrument whose value depends on the value of an underlying asset. 8. True False Suppose you have purchased a futures contract of 1,000 barrels for $35/bbl for June delivery and you have posted a margin of $3400, and the price of crude for June delivery increases to $35.50 tomorrow, and you decide to cash out tomorrow. Your margin will increase to $3900, and if you decide to cash out, you will have $500 less a transaction fee. 9. True False High volatility of energy prices since 1973 is one of the reasons that drove the development of financial derivative markets. -

Energy and Power Risk Management

Additional Praise for Energy and Power Risk Management “Eydeland and Wolyniec give a very detailed, yet quite readable, presenta- tion of the risk management tools in energy markets. The book will be a valuable resource for anyone studying or participating in energy markets.” —Severin Borenstein E.T. Grether Professor of Business Administration and Public Policy, Haas School of Business, University of California, Berkeley Director, University of California Energy Institute “Activity in the power sector exposes all participants to complex and unique risk. Deregulation and the collapse of Enron have only increased the need to understand and control these risks. Covering the spectrum of risk and valu- ation, from the fundamentals of price movement and modeling with poor data, to physical asset valuation and the complex energy derivatives, this book offers a firm foundation from which to solve real world problems.” —Dr. Chris Harris General Manager, Commercial Operations, InnogyOne Founded in 1807, John Wiley & Sons is the oldest independent publishing company in the United States. With offices in North America, Europe, Aus- tralia, and Asia, Wiley is globally committed to developing and marketing print and electronic products and services for our customers’ professional and personal knowledge and understanding. The Wiley Finance series contains books written specifically for finance and investment professionals as well as sophisticated individual investors and their financial advisors. Book topics range from portfolio management to e- commerce, risk management, financial engineering, valuation and financial instrument analysis, as well as much more. For a list of available titles, please visit our web site at www.WileyFinance.com. Energy and Power Risk Management New Developments in Modeling, Pricing, and Hedging ALEXANDER EYDELAND KRZYSZTOF WOLYNIEC John Wiley & Sons, Inc. -

Recognition of Lack of Recoverability of Inventories (US GAAP)

Because Experience Matters Recognition of Lack of Recoverability of Inventories (US GAAP) 546 Fifth Ave, New York, NY 10036 212-808-0070 565 Taxter Road, Elmsford, NY 10523 914-523-2047 [email protected] lhfcpa.com Final Logos co. LHF L Frishkoff Company Accounting Tax Assurance co. LHF L Frishkoff Company Accounting Tax Assurance Accounting for the recognition of lack of recoverability of inventories can be a complex area that often requires the exercise of judgment. Although, US GAAP provides guidance under ASC 330, Inventory, it is the obligation of each entity to establish procedures to comply with the guidance. In this post, we’ll take a deeper dive into accounting for recognition of lack of recoverability of inventories. I. US GAAP – Recognition of Lack of Recoverability A. Lower of Cost or Net Realizable Value ASC 330-10-35-1B Inventory measured using any method other than LIFO or the retail inventory method (for example, inventory measured using first-in, first-out (FIFO) or average cost) shall be measured at the lower of cost and net realizable value. When evidence exists that the net realizable value of inventory is lower than its cost, the difference shall be recognized as a loss in earnings in the period in which it occurs. That loss may be required, for example, due to damage, physical deterioration, obsolescence, changes in price levels, or other causes. Although cost is the primary basis for inventory pricing, a departure from cost is required when the loss of usefulness of an item or other factors indicate that cost will not be recovered when the item is sold.