2012 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

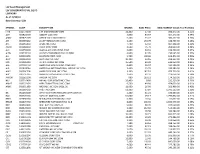

LSV Asset Management LSV CONSERVATIVE VAL EQ FD LSVFNDRV As Of: 9/30/19 Base Currency: USD

LSV Asset Management LSV CONSERVATIVE VAL EQ FD LSVFNDRV As of: 9/30/19 Base Currency: USD SYMBOL CUSIP DESCRIPTION SHARES BASE PRICE BASE MARKET VALUE% of Portfolio FITB 316773100 5TH 3RD BANCORP COM 14,400 27.38 394,272.00 0.51% ABT 002824100 ABBOTT LAB COM 3,600 83.67 301,212.00 0.39% ABBV 00287Y109 ABBVIE INC COM USD0.01 5,100 75.72 386,172.00 0.50% AYI 00508Y102 ACUITY BRANDS INC COM 1,400 134.79 188,706.00 0.24% AFL 001055102 AFLAC INC COM 7,400 52.32 387,168.00 0.50% AGCO 001084102 AGCO CORP COM 3,500 75.70 264,950.00 0.34% ALK 011659109 ALASKA AIR GROUP INC COM 3,000 64.91 194,730.00 0.25% ALSN 01973R101 ALLISON TRANSMISSION HOLDING 4,900 47.05 230,545.00 0.30% ALL 020002101 ALLSTATE CORP COM 5,700 108.68 619,476.00 0.80% ALLY 02005N100 ALLY FINL INC COM 10,200 33.16 338,232.00 0.44% MO 02209S103 ALTRIA GROUP INC COM 15,500 40.90 633,950.00 0.82% AAL 02376R102 AMERICAN AIRLINES INC COM USD1 6,800 26.97 183,396.00 0.24% AIG 026874784 AMERICAN INTERNATIONAL GROUP INC COM 3,400 55.70 189,380.00 0.24% AMP 03076C106 AMERIPRISE FINL INC COM 3,200 147.10 470,720.00 0.61% ABC 03073E105 AMERISOURCEBERGEN CORP COM 2,600 82.33 214,058.00 0.28% AMGN 031162100 AMGEN INC COM 900 193.51 174,159.00 0.22% NLY 035710409 ANNALY CAP MGMT INC COM 26,400 8.80 232,320.00 0.30% AMAT 038222105 APPLIED MATERIALS INC COM 9,500 49.90 474,050.00 0.61% ARNC 03965L100 ARCONIC INC COM USD1.00 11,900 26.00 309,400.00 0.40% T 00206R102 AT&T INC COM 51,300 37.84 1,941,192.00 2.50% BK 064058100 BANK NEW YORK MELLON CORP COM STK 4,300 45.21 194,403.00 0.25% BAC 060505104 -

Ingredion Annual Report 2021

Ingredion Annual Report 2021 Form 10-K (NYSE:INGR) Published: February 24th, 2021 PDF generated by stocklight.com UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2020 or ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number 1-13397 INGREDION INCORPORATED (Exact name of registrant as specified in its charter) Delaware 22-3514823 (State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification No.) 5 Westbrook Corporate Center, Westchester, Illinois 60154 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including area code (708) 551-2600 Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol(s) Name of each exchange on which registered Common Stock, par value $0.01 per share INGR New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒ Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Features & Benefits

NOVATION TM 4600 Description: Pregelatinized food starch refined from waxy maize Appearance: Fine, cream / off-white coloured powder Features Benefits 4600 Consumer friendly simple "starch" labelling Potential for marketing and labelling claims (e.g. can enable TM a no additives claim*). Ideal in wide range of foods, where thickening combined with clean, simple consumer friendly Classed as a food ingredient in the EU labelling is a requirement. May be used in foods labelled as organic, permitted within 5% of the ingredients of non- organic origin. *depends on other ingredients in the recipe Cold water swelling For the food manufacturer requiring instant thickening. NOVATION 4600 is a fine powder and therefore may require dispersion with other dry ingredients or oil to avoid lumping. Bland flavour profile Allows the inherent flavours within a recipe to be NOVATION delivered cleanly with no masking. Excellent process tolerance Will withstand moderate amounts of heat and shear in a process. Suitable for a wide range of applications from mayonnaise production to fruit preparations for pie fillings. Smooth, short texture Improved textural properties and gloss when compared to a traditional drum dried product. Shelf life stable Provides thickening and stability to applications and does not gel over life. APPLICATION AND USAGE INFORMATION Application Summary: NOVATION 4600 is a functional native food starch with cold water swelling properties. It has been designed as a thickener and stabilising agent for a wide range of cold prepared food products. Typical applications include: Chilled dips & dressings: For chilled dips and dressings where a “clean label” is a must this product excels. -

Docket No.: 20-0606 Meeting: 5/10/21 Deadline: 5/21/21 M E M O R a N D U M______

Docket No.: 20-0606 Meeting: 5/10/21 Deadline: 5/21/21 M E M O R A N D U M___________________________________________________ TO: The Commission FROM: Jessica L. Cardoni, Administrative Law Judge DATE: May 7, 2021 SUBJECT: Northern Illinois Gas Company d/b/a Nicor Gas Company Proposed Revenue-Neutral Tariff Filing to Address Issues Arising From the Storage Study Presented in Docket No. 18- 1775. (tariffs filed on June 30, 2020) RECOMMENDATION: Grant Motion to Modify Oral Argument Time Allotment. I. PROCEDURAL HISTORY On June 30, 2020, Northern Illinois Gas Company d/b/a Nicor Gas Company (“Nicor Gas” or the “Company”) filed tariffs with the Illinois Commerce Commission (“Commission”) to revise its Transportation program. The tariff filing was based on a study (“Storage Study”) assessing the implications of how Transportation customers currently use storage. Staff of the Commission (“Staff”) participated in this proceeding. Petitions to Intervene were filed on behalf of Constellation NewEnergy – Gas Division, LLC (“CNEG”); Cargill, Inc., Caterpillar Inc., Sterling Steel Company, Ingredion Incorporated, and ExxonMobil Power & Gas Services, Inc., who collectively formed the Illinois Industrial Energy Consumers (“IIEC”); Grain and Feed Association of Illinois (“GFAI”); Illinois Competitive Energy Association (“ICEA”); Retail Energy Supply Association (“RESA”); Illinois Manufacturer’s Association (“IMA”); Illinois Asphalt Pavement Association (“IAPA”); Nucor Steel Kankakee, Inc. (“Nucor”); Sequent Energy Management, L.P. (“Sequent”); and Illinois Energy, USA, LLC (“IE”). The Administrative Law Judge granted these Petitions to Intervene. An evidentiary hearing was held on February 10, 2021, and a Proposed Order was served on April 7, 2021. Briefs on Exceptions (“BOEs”) were filed on April 21, 2021 by the following parties: Nicor Gas, Staff, CNEG, ICEA, RESA, and IIEC. -

Chicago's Largest Publicly Traded Companies | Crain's Book of Lists

Chicago’s Largest Publicly Traded Companies | Crain’s Book of Lists 2018 Company Website Location Walgreens Boots Alliance Inc. www.walgreensbootsalliance.com Deerfield, IL Boeing Co. www.boeing.com Chicago, IL Archer Daniels Midland Co. www.adm.com Chicago, IL Caterpillar Inc. www.caterpillar.com Peoria, IL United Continental Holdings Inc. www.unitedcontinental-holdings.com Chicago, IL Allstate Corp. www.allstate.com Northbrook, IL Exelon Corp. www.exeloncorp.com Chicago, IL Deere & Co. www.deere.com Moline, IL Kraft Heinz Co. www.kraftheinz-company.com Chicago, IL Mondelez International Inc. www.mondelez-international.com Deerfield, IL Abbvie Inc. www.abbvie.com North Chicago, IL McDonald’s Corp. www.aboutmcdonalds.com Oak Brook, IL US Foods Holding Corp. www.USfoods.com Rosemont, IL Sears Holdings Corp. www.searsholdings.com Hoffman Estates, IL Abbott Laboratories www.abbott.com North Chicago, IL CDW Corp. www.cdw.com Lincolnshire, IL Illinois Tool Works Inc. www.itw.com Glenview, IL Conagra Brands Inc. www.conagrabrands.com Chicago, IL Discover Financial Services Inc. www.discover.com Riverwoods, IL Baxter International Inc. www.baxter.com Deerfield, IL W.W. Grainger Inc. www.grainger.com Lake Forest, IL CNA Financial Corp. www.cna.com Chicago, IL Tenneco Inc. www.tenneco.com Lake Forest, IL LKQ Corp. www.lkqcorp.com Chicago, IL Navistar International Corp. www.navistar.com Lisle, IL Univar Inc. www.univar.com Downers Grove, IL Anixter International Inc. www.anixter.com Glenview, IL R.R. Donnelly & Sons Co. www.rrdonnelly.com Chicago, IL Jones Lang LaSalle Inc. www.jll.com Chicago, IL Dover Corp. www.dovercorporation.com Downers Grove, IL Treehouse Foods Inc. -

Growing Exponentially | 2013 Annual Report Darcell Creswell (2013 Graduate) Girls 4 Science Participant Receiving Scholarship from Board Member Elaine Harris

1 Girls 4 Science: Growing Exponentially | 2013 Annual Report Darcell Creswell (2013 graduate) Girls 4 Science Participant receiving scholarship from Board member Elaine Harris Participating in Girls 4 Science has made it clear to me that the infl uence of women in science, technology, engineering and math is every woman’s legacy from birth. I am now more interested in subjects like Horticulture, Genetics and Engineering because of the mentors who took time out of their schedules to facilitate themed fi eld trips and class activities while I was in G4S. I am very thankful to have been recognized as a 2013 G4S scholarship recipient and I will use my education at Western Illinois University to continue to “overcome barriers and excel in STEM. ” Contents 1 Girls 4 Science Graduate, Darcell Creswell 3 Letter from the Executive Director, Jackie Lomax 4 Girls 4 Science: Girls Growing Exponentially 5 Partnerships Helping Girls 4 Science Grow Exponentially 6 Girls 4 Science 2013 Report Card 7 Oh the Places You’ll Go- 2013 Explorations 8 Girls 4 Science Sites of Operation 9 Girls 4 Science Graduate, Leona Barnes 10 Girls 4 Science Accomplishments: Heights Reached 11 Letter from the Board President, Linda Boasmond 12 Girls 4 Science Leadership 13 Girls 4 Science Financial Report: 2013 in Review 14 2013 Giving List 15 Girls 4 Science Volunteers The mission of Girls 4 Science (G4S) is to increase science literacy amongst girls ages 10-18 through scientifi c discovery and collaboration with external partnerships. 3 Girls 4 Science: Growing Exponentially | 2013 Annual Report irls 4 Science (G4S) continues to make great strides for science, technology, engineering and Letter from mathematics equality through its Saturday Science Academy program. -

For a Sustainabletomorrow

Company of choice for a sustainable tomorrow MESSAGE FROM OUR CEO SAFETY & HEALTH SOCIAL ACCOUNTABILITY ENVIRONMENTAL CONSERVATION OPERATIONAL EXCELLENCE SUSTAINABLE SOURCING INNOVATION COMMUNITY ENGAGEMENT GOVERNANCE, INTEGRITY & TRUST GOAL SUMMARY AWARDS & RECOGNITION INGREDION LOCATIONS 2015 Sustainability Update To our customers, shareholders and neighbors, In 2015 we continued our Ingredion Company of Choice for a Sustainable MESSAGE FROM OUR CEO Tomorrow plan, a program rolled out in 2014 that outlines our sustainability agenda and includes performance and reduction targets in eight key areas. SAFETY & HEALTH These eight focal areas, identified by chapters in this update, are aligned with our customers’ objectives and are directed where our sustainability efforts can have the most meaningful and positive impact. SOCIAL ACCOUNTABILITY Safety is and always has been our most important value. Last year we Mission announced a lofty target to achieve an employee Total Recordable Incident We believe that our success as a company is tied to the well- ENVIRONMENTAL CONSERVATION Rate of 0.20 by 2020. In 2015 we continued to develop programs and implement processes detailed in this update that help to further indoctrinate being of our employees and the health of our communities OPERATIONAL EXCELLENCE our safety culture throughout our global network. Nothing we do is worth and the environment. We aspire to operate our business in a getting hurt for, and through training, communication and improved sustainable manner to become the employer, -

Product Data Sheet Confidential

® COLFLO 67 (06442106) US Label Designation Food Starch-Modified Canada Label Designation Modified Corn Starch Source Waxy Maize PHYSICAL AND CHEMICAL CHARACTERISTICS (*): Color White to Off-White Form Fine Powder Granulation Through USSS #100 >95% Through USSS #200 >85% confidential PHYSICAL AND CHEMICAL SPECIFICATIONS: Viscosity (CML-M105) End 600 – 950 MVU Moisture 13% maximum pH (20% slurry) 4.8 – 6.7 MICROBIOLOGICAL SPECIFICATIONS: Total Plate Count 10,000/g maximum Yeast 200/g maximum Mold 200/g maximum E. coli negative Salmonella negative Meets NFPA specifications for thermophilic bacteria. PACKAGING AND STORAGE COLFLO 67 is packaged in multi wall kraft paper bags with a net weight of 50 lbs. We recommend that COLFLO 67 be stored in a clean, dry area at ambient temperature and away from heavily aromatic material. The best before date for COLFLO 67 is 24 months from the date of manufacture. (*) While this information is typical of COLFLO 67 it should not be considered as a specification. product data sheet product Effective Date: May 10, 2012 The information described above is offered solely for your consideration, investigation, and independent verification. 10 Finderne Avenue 106 Summerlea Road It is up to you to decide whether and how to use this information. Ingredion Incorporated and the Ingredion group Bridgewater, NJ 08807 Brampton, Ontario L6T 4X3 of companies make no warranty about the accuracy or completeness of the information contained above or the USA Canada suitability of any of their products for your specific intended use. Furthermore, all express or implied warranties of noninfringement, merchantability, or fitness for a particular purpose are hereby disclaimed. -

Tour Group X

February 9-11, 2014 Chicago, Ill. Food Institute Tour Group X ® Food Institute February 9-11, 2014 l Chicago, Ill. Agriculture Future of America’s mission is to identify, encourage and support outstanding college men and women preparing for careers in the agriculture and food industry. AFA Leader Development Programs include a growing series of AFA Leader Institutes for college men and women allowing exposure and connectivity to specific sectors of the agriculture industry. The AFA Food Institute, held annually in February, brings 75 talented college men and women together in a food concentration center to take part in a three-day program. Students are selected through a competitive application process and have expressed a specific interest in the food sector. The itinerary provides interaction between students and food sector leaders; exposes students to area processors, businesses and other related service providers and includes discussion and training to enhance student preparation to enter careers in the agriculture and food industry. Objectives • Increase the profile of food systems, processing, marketing and related service careers to students interested in the food sector • Create an understanding of joint interests of food processors around global supply and food safety • Enhance awareness of the integration of the food system from production to retail • Discuss issues, trends and opportunities facing the industry • Provide students with a visual representation of participating organizations business, environment and culture • Network to create relationships that may aid in internship and work experiences for the mutual benefit of future employment • Close the gap between workforce needs and career preparation in the food industry 2014 Food Institute Partner AFA thanks Cargill for providing program support toward the efforts of the 2014 AFA Food Institute. -

North American Rail Shippers Association Annual Meeting

North American Rail Shippers Association Annual Meeting Registration by Name, as of May 7, 2019 First Name Last Name Title Company Frank Adcock AVP Marketing TTX Company Folu Adepitan Sr Sales Rep Kansas City Southern Terry Allen Executive Director SEARS FABIAN ALVAREZ CONTROLLER GIGO TRANSPORT, INC. Tim Atkinson VP of Sales Stimson Lumber Company Adam Avants Account Manager GATX Corporation Chuck Baker President and CEO ASLRRA Michael Barth Vice President Transportation United Sugars Corporation Jason Barton Vice President - Midwest RailPros Kirk Bastyr Progressive Railroading Randy Bennett COO Rail Logix Lauren Berrey VP - Sales MUL Railcars Inc David Bertram Vice President RGCX Railcars Hugh Blair National Accounts Manager Telgian Steve Blinn Director Sales Norfolk Southern Railroad Steve Bobb Executive Vice President & CMO BNSF Railway Jackson Bogatz Manager- Industrial Sales Union Pacific Railroad Will Braden Sales Manager Industrial Networks Jessica Brink ICL Americas LLC Graham Brisben CEO PLG Consulting Audrey Brodrick Attorney Fletcher & Sippel LLC Aaron Brown Project Manager RailPros Chris Brown Manager Civil Asset Management & Engineering Aurizon Gary Brown Executive Director PNWARS Dana Burleigh VP Operations Lynch Logistics George P Bush Commissioner Texas General Land Commission Mark Byars Director Project Dev. - Rail and Civil Construction Trans-Global Solutions, Inc. Angela Caddell VP - Industrial Products BNSF Railway Donald Cameron Director of Sales Celtic Intermodal Tom Cargill Logistics Manager - Rail Operations Commercial Metals Casey Carmody Head of Logistics BIOURJA TRADING LLC Jay Carter Strategic Market Manager The Greenbrier Companies Joel ChristensenRegional VP Sales Bourque Logistics North American Rail Shippers Association Annual Meeting Registration by Name, as of May 7, 2019 Zach Coccoli Attorney MT Wheat and Barley Committee EDUARDO CONTRERASMANAGING DIRECTOR GIGO TRANSPORT, INC. -

Looking to a More Sustainable Future

All Life 2019 Sustainability Report Looking to a More Sustainable Future MESSAGE FROM OUR CEO MATERIALITY MATRIX EVERYDAY LIFE GOVERNANCE INGREDION INCORPORATED 2030 GOALS AWARDS & RECOGNITION PLANET LIFE COMPANY OVERVIEW 2019 SUSTAINABILITY REPORT 2030 ALL LIFE STRATEGY CONNECTED LIFE To Our Customers, Shareholders, Employees and Neighbors: s we publish Ingredion’s ninth annual Sustainability Report, it is a time to reflect on the 50th anniver- sary of Earth Day, which will be celebrated around the globe. As a leading food ingredients company, Ingredion is increasingly focusing its energies and efforts on new ways to operate and innovate aligned with Earth Day’s purpose of protecting the environment. As we grow our business globally, I am pleased Athat our sustainability results continue to drive environmental improvement within our communities for our customers, employees, suppliers and shareholders. During 2019, Ingredion’s global Sustainability Council continued its historically collaborative outreach, consulting with customers, suppliers, NGOs and industry experts. As a result, we are working to further align our efforts with the United Nations Sustainable Development Goals (SDGs). We have made significant progress toward realizing our vision across principal areas of social and environmental impact, but we know more work must be done together with stakeholders inside and outside Ingredion. The All Life sustainability plan sets out our bold ambition to drive meaningful change on social and environ- mental issues. Consumers today are looking for food and beverages made with real ingredients that are familiar, trusted and authentic. In support of this strong and growing consumer preference, we are excited to share our bold commitment to sustainably source 100 percent of our corn, tapioca, potato, pulses and stevia by 2025. -

What's Next in Sustainability

What’s next in sustainability 2020 REPORT continuing to conduct Sedex Member Ethical Trade Audits (SMETA) MAKING LIFE BETTER despite accessibility challenges—and to remain even more vigilant about aligning our environmental impact goals around science-based criteria. It has also meant engaging in COVID-related support initiatives with local communities from South America to Southeast Asia. FOR ALL And with a focus on the world’s pressing need for social justice, we’re Ten years have passed since the publication of our first sustainability also pleased to share that this year will mark the publication of our first report. Ten years of establishing, articulating and implementing goals. dedicated Diversity, Equity and Inclusion report. The report focuses on the Ten years of making progress toward them in the face of changing many positive initiatives we have progressed to strengthen our culture in regulations, unexpected challenges and evolving stakeholder line with our value of “Everyone Belongs.” expectations. And ten years of seeing each report grow in both importance and impact. Finally, as you review these pages, I can’t overemphasize the importance of our employees in helping to advance our shared goals. They embrace We take great pride in what has been accomplished over the past decade our purpose and live our values every day. They make a positive difference even as we’re humbled by the work that remains. Our stakeholders count for our customers, shareholders and communities around the world. And on us to continue executing against the 2030 All Life commitments when it comes to our All Life commitments, they truly understand what it introduced last year and that are described on these pages—and to takes to achieve them—and BE WHAT’S NEXT in sustainability.