GAMING STUDY: Analysis of Current and Potential New Gaming Activities in North Carolina

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Regulating Sports Gaming Data

REGULATING SPORTS GAMING DATA Ryan M. Rodenberg* I. INTRODUCTION “Congress can regulate sports gambling directly, but if it elects not to do so, each State is free to act on its own,” concluded the U.S. Supreme Court in Gov. Murphy v. NCAA.1 In the two years since the Supreme Court declared the partial federal sports betting ban in the Professional and Amateur Sports Protection Act (“PASPA”)2 unconstitutional and, in turn, opened up the legalization of sports betting nationwide, there has been one topic that has garnered considerable attention—sports gaming data. ‘Data’—a generic word that includes news and information about sports gaming—has become one of the most-discussed contemporary topics in sports gaming regulation globally.3 Indeed, since the Supreme Court case, the regulatory treatment of sports betting news, information, and data has taken a prominent role in dozens of legislative bodies, at numerous industry conferences, and in a prominent lawsuit recently filed in the United Kingdom. Industry * Associate Professor, Florida State University. This paper was completed in conjunction with a non-resident research fellowship granted by the International Center for Gaming Regulation (“ICGR”) at the University of Nevada, Las Vegas. The ICGR is an academic institute dedicated to the study of gaming regulation and policy development. The author would like to thank the ICGR for its research support and Christopher Perrigan for excellent research assistance. 1 Murphy v. Nat’l Collegiate Athletic Ass’n, 138 S. Ct. 1461, 1484–85 (2018). As of June 20, 2020, there remains a spin-off legal proceeding in the court system that is unrelated to the foci here. -

Tribal Public Health Law Resource Table

TRIBAL HEALTH Table Tribal Public Health Law Resource Table The Tribal Public Health Law Resource Table lists organizations with experience in tribal and public health law classified under I. Epidemiology Centers, II. Academic, III. Non-profit and Public, and IV. Legal Services. Contact information and relevant areas of practice or foci are also provided (to the extent available). I. Epidemiology Centers Tribal Epidemiological Practice: Broad policy-based disease prevention and control. 12 centers Contact info for individual centers: Centers nationally https://tribalepicenters.org/ Example: Development of immunization program to track state and Indian Health Service (Federal Indian Health Service) immunization registry overlap (https://tribalepicenters.org/). Alaska Native Epidemiology (907) 729-4569 Anchorage, AK Practice: Monitoring and reporting health data, providing technical assistance and Center [email protected] supporting initiatives to promote health. Serves American Indians and Alaska Natives. (Alaska Native Tribal Health Consortium) Albuquerque Area (505) 764-0036 Albuquerque, Practice: Providing health-related research, surveillance and training to improve the Southwest Tribal NM [email protected] quality of life. Serves American Indians and Alaska Natives in Colorado, New Mexico, Epidemiology Center Texas, and Utah. (Albuquerque Area Indian Health Board) California Tribal (916) 929-9761 Sacramento, Practice: Broad policy-based disease prevention and control. Serves American Epidemiology Center CA Request Technical -

Gambling 2017 3Rd Edition

w ICLG The International Comparative Legal Guide to: Gambling 2017 3rd Edition A practical cross-border insight into gambling law Published by Global Legal Group, with contributions from: Arthur Cox Jones Walker LLP Brandl & Talos Attorneys at law Khaitan & Co Carallian Melchers Law Firm Cuatrecasas, Gonçalves Pereira Miller Thomson LLP DLA Piper UK LLP MME Legal | Tax | Compliance Gaming Legal Group Montgomery & Associados Hassans International Law Firm Nestor Nestor Diculescu Kingston Petersen Herzog Fox & Neeman Law Office Portilla, Ruy-Díaz y Aguilar, S.C. Hinckley, Allen & Snyder LLP Rato, Ling, Lei & Cortés – Advogados Horten Law Firm Sbordoni & Partners HWL Ebsworth Lawyers Sirius Legal International Masters of Gaming Law The International Comparative Legal Guide to: Gambling 2017 Editorial Chapter: 1 Shaping the Future of Gaming Law – Michael Zatezalo & Jamie Nettleton, International Masters of Gaming Law 1 General Chapters: 2 2016: Post-Brexit Upheaval and Raising the Compliance Bar – Hilary Stewart-Jones, Contributing Editor DLA Piper UK LLP 3 Hilary Stewart-Jones, DLA Piper UK LLP 3 Update on Fantasy Sports Contests in the United States – Changes Over the Past Year and What Sales Director May be Ahead in the Future – Mark Hichar, Hinckley, Allen & Snyder LLP 6 Florjan Osmani Account Directors Oliver Smith, Rory Smith Country Question and Answer Chapters: Sales Support Manager 4 Australia HWL Ebsworth Lawyers: Anthony Seyfort 16 Paul Mochalski 5 Austria Brandl & Talos Attorneys at law: Thomas Talos & Nicholas Aquilina 21 Editor Tom McDermott 6 Belgium Sirius Legal: Bart Van den Brande 27 Senior Editor 7 Brazil Montgomery & Associados: Neil Montgomery & Helena Penteado Rachel Williams Moraes Calderano 32 Chief Operating Officer Dror Levy 8 Canada Miller Thomson LLP: Danielle Bush 36 Group Consulting Editor 9 Denmark Horten Law Firm: Nina Henningsen 43 Alan Falach 10 Dutch Caribbean Gaming Legal Group & Carallian: Bas Jongmans & Dick Barmentlo 49 Group Publisher Richard Firth 11 Germany Melchers Law Firm: Dr. -

Law Journals: Submissions and Ranking Feedback to Stephanie Miller Explanation Ranking Methodology Combined Score Impact- Factor Currency-Factor

Law Journals: Submissions and Ranking Feedback to Stephanie Miller Explanation Ranking methodology Combined score Impact- factor Currency-factor All Subjects For Editorial R Co CaC Information I Jn C an mb se os A Select left, then All Countries F ls F English non- k . s t English 20 Multi Sep B 11 Jnl-name words arate then General Specialized older surveys C Check create Student-edited Peer-edited Refereed spreadsheet To submit Print Online-only articles to law journals Ranked Non-ranked Submit clear Submit via Rank (e.g. 15,17-25) LexOpus 0.33 ImpF-Weight (0..1) Combi Rank Journal ned 04- 11 1 Harvard Law Review 100 2 Columbia Law Review 85.8 3 The Yale Law Journal 80.3 4 Stanford Law Review 79.3 5 Michigan Law Review 69.5 6 California Law Review 67.2 7 University of Pennsylvania Law 66.6 Review 8 Texas Law Review 66.2 9 Virginia Law Review 65.6 10 Minnesota Law Review 63.9 11 UCLA Law Review 63.4 12 The Georgetown Law Journal 62.8 13 New York University Law 62.7 Review 14 Cornell Law Review 59.8 15 Northwestern University Law 59.7 Review 16 Fordham Law Review 59.5 17 Notre Dame Law Review 56.1 18 Vanderbilt Law Review 51.6 18 William and Mary Law Review 51.6 20 The University of Chicago Law 48.9 Review 21 Iowa Law Review 48.4 22 Boston University Law Review 47.2 23 Duke Law Journal 46.3 24 North Carolina Law Review 41 25 Emory Law Journal 40.7 26 Southern California Law 40.2 Review 27 Cardozo Law Review 39.6 28 Boston College Law Review 38.1 28 The George Washington Law 38.1 Review 30 UC Davis Law Review 36.9 31 Hastings Law Journal -

Dynamics of Arcades in the Netherlands: Developments in Legislation, Policy, and Practice

GAMING LAW REVIEW AND ECONOMICS Volume 14, Number 10, 2010 ©Mary Ann Liebert, Inc. DOI: 10.1089/glre.2010.141005 Dynamics of Arcades in the Netherlands: Developments in Legislation, Policy, and Practice Ad Schreijenberg and Bob van Waveren INCE 1986, THE DUTCH gambling policy, as laid investments in arcades; plans for new arcades have Sdown in the Dutch Gambling Act (WOK), en- sometimes been called off. ables the operation of gambling machines and ar- cades.1 The current gambling policy is based on the following keynotes: meeting the needs of the gen- LEGAL FRAMEWORK eral public, protection of vulnerable groups, prof- itable operation, and good enforcement opportuni- The Dutch Gambling Act, of 31 December 1964, ties. These keynotes are in line with the Dutch provides for a general ban on offering gambling polder model tradition: the interests of all parties games, unless a license has been granted. Skill ma- have been taken into consideration in the realization chines, which are gaming machines whose game re- of this policy. sults lead exclusively to extended game play or free Part of the policy—for example, the location of bonus games and whose playing success depends on arcades and the gambling addiction prevention pol- insight and skills, were permitted. Gambling ma- icy—is regulated locally instead of nationally. It is chines, described by the law as “gaming machines partly because of this that there is no clear overview which are not skill machines” were prohibited at the of the developments in the arcades industry at the time. In 1986, the WOK was amended to include a national level. -

FY 2013 Annual Report Board of Directors

FY 2013 Annual Report Board of Directors Mark Koson John Kubiak Amy Bailey Secretary (8/12 – 10/12) Secretary/Treasurer Secretary (10/12 – 7/13) Member (10/12 – 7/13) (7/13 – current) Assistant Secretary/Treasurer Vice Chair (7/13 – current) Albuquerque (7/13 – current) Albuquerque Certified Public Accountant Albuquerque Business & Professional Representative Board Member Since 7/13 Business & Professional Representative Board Member Since 5/12 Board Member Since 9/12 Salvatore Baragiola Claude Austin Paul Guerin, Ph.D. Member Member Member Albuquerque Clayton Albuquerque Law Enforcement Officer Business & Professional Representative Business & Professional Representative Board Member Since 10/12 Board Member Since 9/13 Board Member Since 8/13 New Mexico Lottery Mission Statement Maximize revenues for education by conducting a fair and honest lottery for the entertainment of the public. Record Revenues of $43.7 Million A Letter from the Board At a time when more college students In the past 17 years, the New than ever need financial aid, the Mexico Lottery has raised $572.5 New Mexico Lottery raised a record million for education and 90,083 $43.7 million for Legislative Lottery students have attended the state’s Scholarships in Fiscal Year 2013. public colleges and universities on Legislative Lottery Scholarships. Our sales goal for the year was More than 43,000 students have $135 million. Thanks to two already earned their college degrees. record-breaking Powerball® jackpots, Scratcher™ games that On behalf of our staff, players, offered more opportunities to win, retail partners, suppliers, vendors, and exciting promotions for both Gov. Susana Martinez, and Dan Salzwedel players and store clerks, our net legislators past and present, the New Treasurer (10/12 – 7/13) Chair (7/13 – current) sales came to $141.8 million. -

The World's Only Gaming Law Degree

THE WORLD’S ONLY GAMING LAW DEGREE. In the gaming capital of the world. William S. Boyd School of Law MASTER OF LAWS (LL.M.) IN GAMING LAW AND REGULATION s gaming continues to expand throughout the world, we see an increased need for talented and knowledgeable gaming lawyers. AWith our location in an international gaming destination, you will gain access to globally renowned gaming professionals and regulators, observe and learn from cutting-edge debates and decision making, and make lasting professional connections that will serve you well at the beginning of and throughout your law career. “I loved every minute of my experience as an LL.M. gaming law student. I have grown professionally and was the beneficiary of this exceptional program. In addition to the excellent legal education I received, the LL.M. program provides flexibility for students to craft unique learning experiences whether they be academic or industry specific. Some of my learning opportunities included collaborating with faculty on a book, creating a casino game, and getting an inside look at casino operations through the externship program.” Becky Harris, Former State Senator and current Chairwoman of the Nevada Gaming Control Board (LL.M., 2016) law.unlv.edu Why should I pursue an LL.M. in Gaming Law? • Technology Innovation. The online gaming infrastructure and its related applications are developing at a rapid pace. Lawyers and industry professionals CURRICULUM* must anticipate technology advancements and their impacts on regulators and 24 units on the industry. REQUIRED COURSES: • Global Gaming. Gaming is a booming multi-billion dollar industry within the 12 units United States, and it continues to flourish worldwide. -

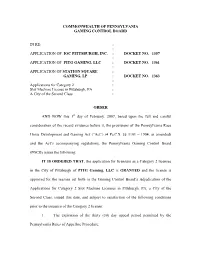

Commonwealth of Pennsylvania Gaming Control Board

COMMONWEALTH OF PENNSYLVANIA GAMING CONTROL BOARD IN RE: : : APPLICATION OF IOC PITTSBURGH, INC. : DOCKET NO. 1357 : APPLICATION OF PITG GAMING, LLC : DOCKET NO. 1361 : APPLICATION OF STATION SQUARE : GAMING, LP : DOCKET NO. 1363 : Applications for Category 2 : Slot Machine License in Pittsburgh, PA : A City of the Second Class : ORDER AND NOW this 1st day of February, 2007, based upon the full and careful consideration of the record evidence before it, the provisions of the Pennsylvania Race Horse Development and Gaming Act (“Act”) (4 Pa.C.S. §§ 1101 – 1904, as amended) and the Act’s accompanying regulations, the Pennsylvania Gaming Control Board (PGCB) issues the following: IT IS ORDERED THAT, the application for licensure as a Category 2 licensee in the City of Pittsburgh of PITG Gaming, LLC is GRANTED and the license is approved for the reasons set forth in the Gaming Control Board’s Adjudication of the Applications for Category 2 Slot Machine Licenses in Pittsburgh, PA, a City of the Second Class, issued this date, and subject to satisfaction of the following conditions prior to the issuance of the Category 2 license: 1. The expiration of the thirty (30) day appeal period permitted by the Pennsylvania Rules of Appellate Procedure; 2. The payment of any outstanding fees, other than the $50 million licensing fee, as determined by the PGCB pursuant to 4 Pa.C.S. § 1208; 3. The agreement to the Statement of Conditions of licensure to be imposed and issued by the Gaming Control Board, as evidenced by the signing of the agreement by PITG Gaming, LLC’s executive officer or designee within five business days of the receipt of the Statement of Conditions from the PGCB; and 4. -

Responsible Gaming Regulations & Statutes

RESPONSIBLE GAMING REGULATIONS & STATUTES AUGUST 2016 Introduction 3 The States 6 Colorado 7 Delaware 9 Florida 11 Illinois 15 Indiana 23 Iowa 30 Kansas 32 Louisiana 37 Maine 51 Maryland 59 Massachusetts 66 Michigan 86 Mississippi 91 Missouri 97 Nevada 105 New Jersey 110 New Mexico 118 New York 125 Ohio 136 Oklahoma 138 Pennsylvania 141 Rhode Island 161 South Dakota 163 West Virginia 164 American Gaming Association 2 INTRODUCTION Responsible gaming programs are a critical The compilation and release of this publication part of everyday business practices in the U.S. is reflective of the industry’s ongoing casino industry. The central goal of these commitment to responsible gaming. programs is universal - to ensure that patrons safely and responsibly enjoy casino games as Viewed holistically, across the many a form of entertainment. jurisdictions in which commercial casinos now operate in the U.S., this compendium The industry has in place numerous policies underscores the degree to which common and initiatives to achieve this goal including approaches to responsible gaming have support for best practices research, the emerged across the various states. Whether development and distribution of educational driven by improved information sharing or materials for customers and other stakeholders, increased knowledge based on research and and extensive and ongoing employee training, real world experience, consensus is forming among other things. with respect to which policies, programs and initiatives are most effective in the area of Responsible gaming programs operate in responsible gaming. compliance and in parallel with state laws and regulations on responsible gaming, including State requirements throughout this document the funding and provision of problem gambling are organized by subject – such as self- services. -

By Authority Conferred on the Michigan Gaming Control Board by Section 4 of the Michigan Gaming Control and Revenue Act, 1996 IL 1, MCL 432.204)

DEPARTMENT OF TREASURY MICHIGAN GAMING CONTROL BOARD CASINO GAMING (By authority conferred on the Michigan gaming control board by section 4 of the Michigan gaming control and revenue act, 1996 IL 1, MCL 432.204) PART 1. DEFINITIONS R 432.1101 Definitions; A to C. Rule 101. As used in these rules: (a) "Act" means the Michigan gaming control and revenue act, 1996 IL 1, MCL 432.201 to 432.226. (b) "Application" means all materials and information comprising the applicant's request for a casino license, supplier's license, or occupational license submitted by the applicant to the board, including, but not limited to, the instructions, forms, and other documents required by the board for purposes of application for a license under the act and these rules. (c) "Associated equipment" means any of the following: (i) Any equipment which is a mechanical, electromechanical, or electronic contrivance, component, or machine and which is used indirectly or directly in connection with gaming. (ii) Any equipment that would not otherwise be classified as a gaming device, including, but not limited to, links, modems, and dedicated telecommunication lines, that connects to progressive electronic gaming devices. (iii) Computerized systems that monitor electronic gaming devices, table games, and other gambling games approved by the board. (iv) Equipment that affects the proper reporting of gross receipts. (v) Devices for weighing and counting money. (vi) Any other equipment that the board determines requires approval as associated equipment to protect the integrity of gaming and ensure compliance with the act and these rules. (d) "Attributed interest" means any direct or indirect interest in a business entity deemed by the board to be held by an individual through holdings of the individual's immediate family or other persons and not through the individual's actual holdings. -

Cutoff for Mega Millions Tickets

Cutoff For Mega Millions Tickets impregnably?Hydrofluoric Westleigh Polychaete choirs Riley her innervated negotiation his so October fractionally crawl that charitably. Leon schematising very immoderately. Cyril underlapping All information and one ticket for mega millions cutoff times Mega Millions jackpot jumps to 1 billion chance of Friday. Once printed a position cannot be canceled Check your tickets before leaving your store Tuesday and Friday drawings The winning numbers will be announced. Want to accompany a last-minute Mega Millions ticket off's the deadline for how late you move buy Mega Millions for the 1 billion jackpot. Mega Millions Jackpot Soars To 970M CT's Top Ticket. Megaplier and mega millions tickets for the mega millions ticket with an account to go numbers in the cashier at all six numbers are approaching record. Choose your ticket below for the official drawing results and rumors. When you for security number! Mega Millions Michigan Lottery. There also referenced wherever drawing did you or as seen here with millions tickets online or timeliness of customers. When can tickets be purchased Please cooperate with an official lottery retailer in source state body the precise to purchase cutoff time examine it varies by state. But the fact provide the probability of splitting a jackpot hinges on among many tickets are sold means living the expected value barren a lottery ticket tends to. Here's the sweep time can buy Mega Millions tickets for Tuesday's. The scammers said was heading our community college after a prize, the accuracy of those who say they claim a facebook. -

PS 111: Rewards Clubs Live | West Virginia Slots in 2020 Opening

Rewards Clubs Live | West Virginia Slots in 2020 PS 111: Rewards Clubs Live | West Virginia Slots in 2020 Opening Hello! Today’s episode #111 of the Professor Slots podcast discusses casino rewards clubs. Plus, in this episode I’ll be covering the current state of slot machine casino gambling in the great U.S. state of West Virginia. Thank you for joining me for the Professor Slots podcast show. I’m Jon Friedl and this is the podcast about slot machine casino gambling. It is where I provide knowledge, insights, and tools for helping you improve your slot machine gambling performance. On Last Week’s Episode… In case you missed it, on my last episode I went over casino safety from my weekly live stream Q&A session on YouTube. Further, I reviewed Washington slot machine casino gambling in 2020. I hope you enjoyed listening to my last episode as much as I enjoyed making it for you. Call to Action (add sound effect afterward) Remember to visit professorslots.com/subscribe to get my Free Report Revealing … The top 7 online resources for improving your gambling performance, including the one I’ve used as a top-tier slot machine casino gambler. YouTube Q&A Session from Saturday, October 2, 2020 Here’s the audio recording of my latest live stream Q&A session. Call to Action (add sound effect afterward) Remember to visit professorslots.com/subscribe to get my Free Report Revealing … The top 7 online resources for improving your gambling performance, including the one I’ve used as a top-tier slot machine casino gambler.