Life Insurance 1. Death Claim

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bulletin Journal of Sport Science and Physical Education

International Council of Sport Science and Physical Education Conseil International pour l‘Education Physique et la Science du Sport Weltrat für Sportwissenschaft und Leibes-/Körpererziehung Consejo International para la Ciencia del Deporte y la Educatión Física Bulletin Journal of Sport Science and Physical Education No 71, October 2016 Special Feature: Exercise and Science in Ancient Times freepik.com ICSSPE/CIEPSS Hanns-Braun-Straße 1, 14053 Berlin, Germany, Tel.: +49 30 311 0232 10, Fax: +49 30 311 0232 29 ICSSPE BULLETIN TABLE OF CONTENT 2 TABLE OF CONTENTS TABLE OF CONTENTS ......................................................................................................... 2 PUBLISHER‘S STATEMENT .................................................................................................. 3 FOREWORD ......................................................................................................................... 4 Editorial Katrin Koenen ...................................................................................................... 4 President‘s Message Uri Schaefer ....................................................................................................... 5 Welcome New Members ................................................................................... 6 SPECIAL FEATURE: Exercise and Science in Ancient Times Introduction Suresh Deshpande .............................................................................................. 8 Aristotelian Science behind Medieval European Martial -

Why I Became a Hindu

Why I became a Hindu Parama Karuna Devi published by Jagannatha Vallabha Vedic Research Center Copyright © 2018 Parama Karuna Devi All rights reserved Title ID: 8916295 ISBN-13: 978-1724611147 ISBN-10: 1724611143 published by: Jagannatha Vallabha Vedic Research Center Website: www.jagannathavallabha.com Anyone wishing to submit questions, observations, objections or further information, useful in improving the contents of this book, is welcome to contact the author: E-mail: [email protected] phone: +91 (India) 94373 00906 Please note: direct contact data such as email and phone numbers may change due to events of force majeure, so please keep an eye on the updated information on the website. Table of contents Preface 7 My work 9 My experience 12 Why Hinduism is better 18 Fundamental teachings of Hinduism 21 A definition of Hinduism 29 The problem of castes 31 The importance of Bhakti 34 The need for a Guru 39 Can someone become a Hindu? 43 Historical examples 45 Hinduism in the world 52 Conversions in modern times 56 Individuals who embraced Hindu beliefs 61 Hindu revival 68 Dayananda Saraswati and Arya Samaj 73 Shraddhananda Swami 75 Sarla Bedi 75 Pandurang Shastri Athavale 75 Chattampi Swamikal 76 Narayana Guru 77 Navajyothi Sree Karunakara Guru 78 Swami Bhoomananda Tirtha 79 Ramakrishna Paramahamsa 79 Sarada Devi 80 Golap Ma 81 Rama Tirtha Swami 81 Niranjanananda Swami 81 Vireshwarananda Swami 82 Rudrananda Swami 82 Swahananda Swami 82 Narayanananda Swami 83 Vivekananda Swami and Ramakrishna Math 83 Sister Nivedita -

July 2015 Edition

2 Yoga Sudha t< iv*aÊ>os<yaegivyaeg< yaegs<i}tm! Vol.XXXI No.7 July, 2015 CONTENTS SUBSCRIPTION RATES Editorial 2 8 Annual (New) ` 500/- $ 50/- 8 Three Years Division of Yoga-Spirituality Brahmasutra - Jagadväcitvät - Prof. Ramachandra G Bhat 3 ` 1400/- $ 150/- ¥ÁvÀAd® AiÉÆÃUÀ±Á¸ÀÛç (14): ¸ÀªÀiÁ¢ü - CªÀĤèsÁªÀ - ²æà gÁeÉñÀ JZï.PÉ. 4 8 Ten Years (Life) ` 4000/- $ 500/- International Day of Yoga Celebration at Raj Path, New Delhi 6 Subscription in favour Prime Minister Sri Narendra Modi’s views on Yoga 9 of ‘Yoga Sudha’, Brief Note on the International Conference Bangalore by held at Vigyan Bhavan, New Delhi 10 Celebration all over the Globe 12 DD/Cheque/MO only Celebration at International Centres of VYASA, S-VYASA 14 Celebration at various parts of Bengaluru 16 ADVERTISEMENT Celebration at various parts of India 23 TARIFF: Complete Color Front Inner - ` 1,20,000/- Back Outer - ` 1,50,000/- Division of Yoga & Life Sciences Curtain Raiser of Madhumeha Mukta Bharat 27 Back Inner - ` 1,20,000/- Front First Inner Page - ` 1,20,000/- Division of Yoga & Physical Sciences Back Last Inner Page - Light in Therapy - Prof. T M Srinivasan 28 ` 1,20,000/- Full Page - ` 60,000/- Half Page - ` 30,000/- Division of Yoga & Management Studies Page Sponsor - ` 1,000/- MBA at S-VYASA 31 Printed at: Division of Yoga & Humanities Sharadh Enterprises, Unforgettable moments with Yogi C R Gururaja Rao 32 Car Street, Halasuru, Resolve to Rise - Dr. K Subrahmanyam 34 Bangalore - 560 008 ph: (080) 2555 6015 e-mail: sharadhenterprises@ VYASA, International gmail.com Updates from Istanbul-Turkey center 36 21st INCOFYRA 38 S-VYASA Yoga University Editor: Dr. -

Download NAAC-SSR Report

SJM Vidyapeetha® SELF STUDY REPORT Submitted to, National Assessment & Accreditation Council Nagarbhavi, Bangalore 560072, Karnataka, India Submitted by, Principal, SJM College of Pharmacy, NH – 4 by pass, SJM Campus, Chitradurga - 577502 Karnataka, India His Holiness, Dr. Shivamurthy Murugha Sharanaru President, SJM Vidyapeetha ® Chitradurga TABLE OF CONTENTS Sl. No Particulars Page No 01 Executive Summary 001-007 02 Profile of the Institution 008-021 03 Criterion Input 022-204 04 Criterion I 022-037 05 Criterion II 038-069 06 Criterion III 070-123 07 Criterion IV 124-155 08 Criterion V 156-175 09 Criterion VI 176-196 10 Criterion VII 197-204 11 Evaluative Report of the Department 205-277 12 Photos of College Activities 278-291 13 Annexures 292-310 EXECUTIVE SUMMARY INTRODUCTION SJM College of Pharmacy is one of the health science institutions of SJM Vidyapeetha®, which was started as an offspring of Sri Murugha Math, Chitradurga in 1966 by the then pontiff Sri Mallikarjuna Murugharajendra Mahaswamigalu, with an intention to take the higher education to the threshold of aspirants. Dr. Shivamurthy Murugha Sharanaru is the present pontiff of Sri Murugha Math and the President of SJM Vidyapeetha. Chitradurga city is known for its unique Fort as one of the famous historical centers of Karnataka. The city is a district Headquarters located 200 kms away from Bangalore, on National Highway No-4. It has good road- railway linkage. SJM College of Pharmacy was started in 1985 with Diploma in Pharmacy as only programme. Now it has raised upto Post Graduation courses and research level. It is the only college in the District. -

CIN/BCIN Company/Bank Name Date of AGM(DD

Note: This sheet is applicable for uploading the particulars related to the unclaimed and unpaid amount pending with company. Make sure that the details are in accordance with the information already provided in e-form IEPF-2 CIN/BCIN L15100TN1982PLC009418 Company/Bank Name PRADHIN LIMITED Date Of AGM( DD-MON-YYYY ) 30-AUG-2018 Sum of unpaid and unclaimed dividend 638982.60 Sum of interest on matured debentures 0.00 Sum of matured deposit 0.00 Sum of interest on matured deposit 0.00 Sum of matured debentures 0.00 Sum of interest on application money due for refund 0.00 Sum of application money due for refund 0.00 Redemption amount of preference shares 0.00 Sales proceed for fractional shares 0.00 Proposed Date of Investor First Investor Middle Investor Last Father/Husband Father/Husband Father/Husband Last DP Id-Client Id- Amount Address Country State District Pin Code Folio Number Investment Type transfer to IEPF Name Name Name First Name Middle Name Name Account Number transferred (DD-MON-YYYY) SAADVILLA, 7/467/1 Amount for unclaimed and AAISHA AFZAL NA MOH.HINDUSTANIAN, CHILKANA INDIA Uttar Pradesh 247001 IN-300011-10695338 120.00 27-OCT-2018 unpaid dividend ROAD, SAHARANPUR (U.P) NO 15/A PLOT NO 13, PURAM Amount for unclaimed and ABDUL BASITH R ABDUL RAHIM PRAGASAM RAO ROAD, BALAJI INDIA Tamil Nadu Chennai 600014 FOLIO00003343 480.00 27-OCT-2018 unpaid dividend NAGAR ROYAPETTAH, MADRAS Amount for unclaimed and ABDUL SAMAD A SHAIKKADHAR R BASHA 22 IST LANE, KATH BADA, MADRAS INDIA Tamil Nadu Chennai 600021 FOLIO00001671 120.00 27-OCT-2018 -

Form No. 17 Note: 1. Examination Work Is Mandatory. 2. in Case, If You

Form No. 17 RAJIV GANDHI UNIVERSITY OF HEALTH SCIENCES, KARNATAKA 4TH 'T' BLOCK, JAYANAGAR, BANGALORE - 560 041 Dr.M.K.Ramesh Ph. : 080-26961930, Registrar (Evaluation) Fax. : 080-26961931 R(E)/DR(E)-I/Ex-I/UG/Aug/Sept - 2018 Date : 10-09-2018 REPLY URGENT DR. POORNIMA S {T0003748} ASSO.PROF DEPT. OF MEDICAL Mandya Institute of Medical Sciences, District Hospital Premises, Mandya - 571 401 COLL Ph.: 231001, 222086 Fax 08232 - 231001 MOBILE : 9535916816 Sir, Sub: Conduct of University UG Examinations September - 2018. Appointment as OBSERVER CUM SQUAD CHIEF - - - - - I am happy to inform you, that the Vice-Chancellor is pleased to appoint you as OBSERVER CUM SQUAD CHIEF in connection with the conduct of Under Graduate Theory examination scheduled to be on 11-09-2018 to 19-09-2018 in the following centre CENTRE :GOVERNMENT AYURVEDIC MEDICAL COLLEGE A001 DHANVANTRI ROAD, BANGALORE - 560 009 CNT PH. : 080 22872848 - 080 - 22872848 You are requested to contact the Principal and Chief Superintendent of the said examination centre and get yourself acquainted with the assigned work. Kindly send your acceptance immediately in the enclosed form by return post. Another copy of the acceptance form may kindly be sent to the Chief Superintendent of the Examination Centre. Your co-operation to conduct the examination in a smooth manner is solicited. Sd/- Dr. M.K.Ramesh Registrar (Evaluation) Encl: 1. Two Acceptance Forms 2. Observer / Squad - Power and functions / Daily Report Check List (Refer RGUHS website). Copy to: 1.The Principal, Mandya Institute of Medical Sciences, , District Hospital Premises, Mandya - 571 401 is requested to spare the services of the said teacher for university examination. -

Yoga-Body-Origins.Pdf

YOGA BODY Praise for Yoga Body: The Origins of Modern Posture Practice Mark Singleton “Mark Singleton’s Yoga Body: The Origins of Modern Posture Practice is an out- standing scholarly work which brings so much insight and clarity to the historic and cultural background of modern hathạ yoga. I highly recommend this book, especially for all sincere students of yoga.”—John Friend, founder of Anusara Yoga “From the moment I started reading Mark Singleton’s Yoga Body I couldn’t put it down. It is beautifully written, extensively researched, and full of fascinating information. It stands alone in its depth of insight into a subject which has intrigued me for forty years.”—David Williams, the fi rst non-Indian to learn the complete Ashtanga Yoga syllabus “Mark Singleton’s book Yoga Body traces the evolution of the ever-expanding practice of a¯sana world-wide. His work offers a much needed historical perspec- tive that will help correct much of the mythology and group-think that is emerg- ing in the modern a¯sana based ‘yoga world.’ Any serious a¯sana practitioner who wishes to understand the place of a¯sana in the greater tradition of yoga will do well to read it carefully.”—Gary Krafstow, founder of the American Viniyoga Institute, author of Yoga for Wellness and Yoga for Transformation “Mark Singleton has written a sweeping and nuanced account of the origins and development of modern postural yoga in early twentieth-century India and the West, arguing convincingly that yoga as we know it today does not fl ow directly from the Yoga Sūtras or India’s medieval hathạ yoga traditions, but rather emerged out of a confl uence of practices, movements and ideologies, ranging from contortionist acts in carnival sideshows, British Army calisthenics and women’s stretching exercises to social Darwinism, eugenics, and the Indian nationalist movement. -

District Wise Taluk Wise Center Address

KARNATAKA SECONDARY EDUCATION EXAMINATION BOARD MALLESHWARAM,BENGALURU DISTRICT WISE TALUQ WISE CENTER CODE AND ADDRESS DISTRICT CODE AN DISTRICT NAME:BENGALURU NORTH TALUK CODE AN01 TALUK NAME: BENGALURU NORTH-1 SL NO CENTER COD CENTER ADDRESS 1 002AN BASAVESWARA BOYS HIGH SCHOOL,RAJAJINAGAR,BENGALURU NORTH, 2 003AN VIDYA VARDHAKA SANGHA HIGH SCHOOL,I BLOCK RAJAJINGAR,BENGALURU NORTH, 3 004AN GOVERNMENT HIGH SCHOOL,POLICE COLONY MAGADI ROAD,BENGALURU NORTH, 4 005AN CARMEL HIGH SCHOOL,II BLOCK III STAGE WOC RD BASVESWARNAGAR,BENGALURU NORTH, 5 006AN AMBEDKAR MEMORIAL HIGH SCHOOL,CA.NO.2 II STAGE W.C.R. RAJAJINAGAR,BENGALURU NORTH, 6 007AN GOVERNMENT JUNIOR COLLEGE,PEENYA,BENGALURU NORTH, 7 008AN PANCHAJANYA VIDYAPEETHA RES.GHS,I-N BLOCK RAJAJINAGAR,BENGALURU NORTH, 8 009AN SRI AUROBINDA VIDYAMANDIR HIGH SCHOOL,5TH A MAIN II STAGE W.C.R. RAJAJINAGAR,BENGALURU NORTH, 9 010AN JINDAL HIGH SCHOOL,16TH K.M. TUMAKURU ROAD,BENGALURU NORTH, 10 011AN FLORENCE HIGH SCHOOL,BASAVESHWARA NAGAR III STAGE R NAGAR,BENGALURU NORTH, 11 014AN ANUPAMA ENGLISH HIGH SCHOOL,WEST OF CHORD RD,IISTAGE MAHALAKSHMI PRM,BENGALURU NORTH, 12 015AN MOTHER THERESA HIGH SCHOOL,SHANKARANGARA,BENGALURU, 13 016AN ST.ANN'S HIGH SCHOOL,742 VI BLOCK RAJAJINAGAR,BENGALURU NORTH, 14 018AN GOUTAM PUBLIC HIGH SCHOOL,NO 173, 1ST MAIN ROAD,,KAMALANAGAR,,BENGALURU 15 020AN GOVERNMENT HIGH SCHOOL,CHIKKABIDARAKALLU,BENGALURU, 16 021AN INDIAN HIGH SCHOOL,NO.74, IST STAGE, 3RD PHASE,WEST OF CHORD ROAD,MANJUNATHANAGARA ,BENGALURU 17 024AN DEENA SEVA HIGH SCHOOL,NO 260 KAMALNAGARA,BENGALURU, 18 025AN VIJAYA BHARATHI HIGH SCHOOL,,BHUVANESHWARINAGAR, T.DASARAHALLI EXTN.,,BENGALURU NORTH, 19 026AN SCHOENSTATT ST. -

CIN/BCIN Company/Bank Name Date of AGM(DD

Note: This sheet is applicable for uploading the particulars related to the unclaimed and unpaid amount pending with company. Make sure that the details are in accordance with the information already provided in e-form IEPF-2 CIN/BCIN L28931TN1982PLC009418 Company/Bank Name BHAGWANDAS METALS LIMITED Date Of AGM( DD-MON-YYYY ) 25-SEP-2017 Sum of unpaid and unclaimed dividend 220446.00 Sum of interest on matured debentures 0.00 Sum of matured deposit 0.00 Sum of interest on matured deposit 0.00 Sum of matured debentures 0.00 Sum of interest on application money due for refund 0.00 Sum of application money due for refund 0.00 Redemption amount of preference shares 0.00 Sales proceed for fractional shares 0.00 Proposed Date of Investor First Investor Middle Investor Last Father/Husband Father/Husband Father/Husband Last DP Id-Client Id- Amount Address Country State District Pin Code Folio Number Investment Type transfer to IEPF Name Name Name First Name Middle Name Name Account Number transferred (DD-MON-YYYY) SAADVILLA, 7/467/1 Amount for unclaimed and AAISHA AFZAL NA MOH.HINDUSTANIAN, CHILKANA INDIA Uttar Pradesh 247001 IN-300011-10695338 120.00 27-OCT-2018 unpaid dividend ROAD, SAHARANPUR (U.P) NO 15/A PLOT NO 13, PURAM Amount for unclaimed and ABDUL BASITH R ABDUL RAHIM PRAGASAM RAO ROAD, BALAJI INDIA Tamil Nadu Chennai 600014 FOLIO00003343 480.00 27-OCT-2018 unpaid dividend NAGAR ROYAPETTAH, MADRAS Amount for unclaimed and ABDUL SAMAD A SHAIKKADHAR R BASHA 22 IST LANE, KATH BADA, MADRAS INDIA Tamil Nadu Chennai 600021 FOLIO00001671 120.00 -

The Gazette of India

REGD. NO, D. L.-33004/99 The Gazette of India EXTRAORDINARY PART II—Section 3—Sub-section (i) PUBLISHED BY AUTHORITY No. 351] NEW DELHI, MONDAY, JULY 29, 2002/SRAVANA 7,1924 2378 GI/2002 (1) 2 THE GAZETTE OF INDIA : EXTRAORDINARY [PART II—SEC. 3(i)] 3 4 THE GAZETTE OF INDIA : EXTRAORDINARY [PART II—SEC, 3(i)] 5 6 THE GAZETTE OF INDIA EXTRAORDINARY [PART II—SEC 3(i)] 7 8 THE GAZETTE OF INDIA: EXTRAORDINARY [PART II—SEC 3(i)J 9 10 THE GAZETTE OF INDIA EXTRAORDINARY |PARF II—SKC 3(IJ] 11 12 THE GAZETTE OF INDIA: EXTRAORDINARY [PART II—SEC. 3(i)| 13 14 THE GAZETTE OF INDIA. EXTRAORDINARY [PART II—SEC 3(i)j 15 16 THE GAZETTE OF INDIA EXTRAORDINARY [PART II—SEC 3(I)] 17 2378GI/2002—3A 18 THE GAZETTE OF INDIA: EXTRAORDINARY [PART II—SEC. 3(i)] 2378 GI/2002—3B 19 20 THE GAZETTE OF INDIA EXTRAORDINARY [PART II—SEC 3(I)J 21 22 THE GAZETTE OF INDIA: EXTRAORDINARY [PART II—SEC. 3(i)] 23 24 THE GAZETTE OF INDIA: EXTRAORDINARY [PART II—SKC. 3(i)] 25 26 THE GAZETTE OF INDIA EXTRAORDINARY |PART II—Szr Mi)] 27 28 THE GAZETTE OF INDIA EXTRAORDINARY (PARI II—SF.C 3(i)| 29 30 THE GAZETTE OF INDIA EXTRAORDINARY [PART II—SEC 3(i)] 31 32 THE GAZETTE OF INDIA EXTRAORDINARY [PART II—SEC 3(i)| 33 2378 GI/2002—4A 34 THE GAZETTE OF INDIA EXTRAORDINARY [PART II—Sfec. 3(i)] 2378 GI/2002—4B 35 16 THE GAZETTE OF INDIA EXTRAORDINARY [PARI II—SEC. -

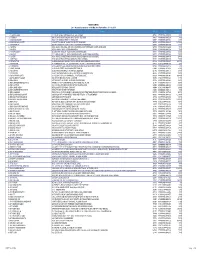

SR NO NAME Address Pincode Folio Amount

SIEMENS LIMITED List of Outstanding warrant as on 11th Mar, 2019 ( Payment Date:- SI 11-02-2019 ) SR NO NAME Address Pincode Folio Amount 1 A P RAJALAKSHMY A-6 VARUN I RAHEJA TOWNSHIP MALAD EAST MUMBAI 400097 0000000000SIA0004682 49.00 2 A PADMAJA G44, MADHURA NAGAR COLONY YOUSUFGUDA HYDERABAD 500037 0000000000SIA0005290 70.00 3 A NARAYANASWAMY NO: 60, 3RD CROSS CUBBON PET BANGALORE 560002 0000000000SIA6000582 140.00 4 A KMUDDURAMAIAH SETTY A K M SETTY & SONS W 104 OLD THARAGUPET BANGALORE 560002 0000000000SIA0000502 13,510.00 5 A RAMAMURTHY 59/A WEST ANJANEYA TEMPLE STREET BASAVANAGUDI BANGALORE 560004 0000000000SIA6001645 140.00 6 A GEORGE NO.35, SNEHA, 2ND CROSS, 2ND MAIN, CAMBRIDGE LAYOUT EXTENSION, ULSOOR, BANGALORE 560008 0000IN30023912036499 70.00 7 A GEORGE NO.263 MURPHY TOWN ULSOOR BANGALORE 560008 0000000000SIA6000604 70.00 8 A KUMARASWAMY 645 22ND MAIN ROAD 4TH T BLOCK JAYANAGAR BANGALORE 560011 0000000000SIA6000303 140.00 9 A REGINA 11/12 LANGFAR ROAD 1ST CROSS NANJAAPPA CIRCLE SHANTINAGAR BANGALORE 560027 0000000000SIA6000323 280.00 10 A SAVERI NO 111 RAMDEU GARDEN KANCHARAKAMA HOLLI HENNOOR MAIN RD BANGALORE 560084 0000000000SIA6000376 280.00 11 A SREEPADA SHRIDHARA ASHRAMA B H ROAD,SOMAITHA LAYOUT SHIMOGA 577201 0000000000SIA6000285 210.00 12 A RAMANATHAN ANANDAPADMANABHA RAMANATHAN 23/6 SHENOY ROAD NUNGAMBAKKAM MADRAS 600034 0000000000SIA0003867 4,235.00 13 A RAJENDRAN B-4, KUMARAGURU FLATS 12, SIVAKAMIPURAM 4TH STREET, TIRUVANMIYUR CHENNAI 600041 00SI1203690000017100 56.00 14 A CHINNAPPAN 27/8-B, GROUND FLOOR 3RD MAIN ROAD RAJALAKSHMI NAGAR VELACHERY, CHENNAI 600042 0000IN30232410970115 77.00 15 A RAMESH KUMAR 10 VELLALAR STREET VALAYALKARA STREET KARUR 639001 0000IN30039413174239 140.00 16 A VL NARAYAN 55 WEST RAMALINGAM ROAD R S PURAM COIMBATORE 641002 0000000000SIA6000551 210.00 17 A R MUKUNDA S/O A G RANGAPPA CHICKAJAJUR HOLALKERE TALUK KARNATAKA INDIA 999999 0000000000SIA6000352 280.00 18 AASHISH KUMAR GUPTA 127 V BLOCK II CROSS KORAMANGALA LAYOUT BANGALORE 560034 0000000000SIA0005415 4,200.00 19 AASTHA ABHAY PUSALKAR H NO. -

Microsoft India (R&D) Pvt. Ltd., C2008. 100 Himal

Title Author Publisher .in Microsoft India Development Center Gachibowli.: Microsoft India (R&D) Pvt. Ltd., c2008. 100 Himalayan flowers Mehta, Ashvin. New York: Vendome Press, 1991. 100 red listed medicinal plants of conservation concern in Southern India Ravikumar, K. Bangalore: FRLHT, 2000. 1000 animal quiz Gandhi, Meneka. Allahabad: Rupa & Co., c1992. 1000 plant quiz Padma Vijay, G. Allahabad: Rupa & Co., c1992. 1001 ways to energize employees Nelson, Bob-1956 New York: Workman Pub., c1997. 1001 ways to reward employees Nelson, Bob-1956 New York: Workman Pub., c2005. 125 Medicinal plants grown at Rajegaon Deokar, A.B. Pune: DS Manav Vikas Foundation, 1998. 150 ECG problems Hampton, John R. Edinburgh: Churchill Livingstone, 2008. Gland, Switzerland: International Union for Conservation of Nature and Natural 1997 IUCN red list of threatened plants Kerry S. Walter & Harriet J. Gillett Resources, 1998. 2010 : odyssey two Clarke, Arthur C.-1917-2008. New York: Ballantine Publishing, 1982. 2012 end or beginning Bangalore: Manasa Foundation (R, 2009. 2nd chance Patterson, James-1947 New York: Warner Vision Books, c2002. 4448 vyadhigal vilakkam Angarasan, S. Thanjavur: Sarasvati Mahal Library, c2006. 448 viyathigal vilakam Angarasan, S. Thanjavur: Sarasvati Mahal Library, c2006. 50 Fascinating case studies Volume 1 Misra, K.P. Hyderabad: Orient Longman Pvt. Ltd., c2006. 50 Fascinating case studies Volume 2 Misra, K.P. Hyderabad: Orient Longman Pvt. Ltd., c2006. 50 Fascinating case studies Volume 3 Misra, K.P. Hyderabad: Orient Longman Pvt. Ltd., c2007. 5000 days to save the planet Goldsmith, Edward. London: Paul Hamlyn Publishing, c1990. 65 successful Harvard Business School application essays / with analysis by the staff of The Harbus, the Harvard Business School newspaper.