The Cornwall and Isles of Scilly Local Enterprise Partnership (LEP) Was Launched in May 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Daily Report Thursday, 20 July 2017 CONTENTS

Daily Report Thursday, 20 July 2017 This report shows written answers and statements provided on 20 July 2017 and the information is correct at the time of publication (06:34 P.M., 20 July 2017). For the latest information on written questions and answers, ministerial corrections, and written statements, please visit: http://www.parliament.uk/writtenanswers/ CONTENTS ANSWERS 10 Social Tariffs: Torfaen 19 ATTORNEY GENERAL 10 Taxation: Electronic Hate Crime: Prosecutions 10 Government 19 BUSINESS, ENERGY AND Technology and Innovation INDUSTRIAL STRATEGY 10 Centres 20 Business: Broadband 10 UK Consumer Product Recall Review 20 Construction: Employment 11 Voluntary Work: Leave 21 Department for Business, Energy and Industrial Strategy: CABINET OFFICE 21 Mass Media 11 Brexit 21 Department for Business, Elections: Subversion 21 Energy and Industrial Strategy: Electoral Register 22 Staff 11 Government Departments: Directors: Equality 12 Procurement 22 Domestic Appliances: Safety 13 Intimidation of Parliamentary Economic Growth: Candidates Review 22 Environment Protection 13 Living Wage: Jarrow 23 Electrical Safety: Testing 14 New Businesses: Newham 23 Fracking 14 Personal Income 23 Insolvency 14 Public Sector: Blaenau Gwent 24 Iron and Steel: Procurement 17 Public Sector: Cardiff Central 24 Mergers and Monopolies: Data Public Sector: Ogmore 24 Protection 17 Public Sector: Swansea East 24 Nuclear Power: Treaties 18 Public Sector: Torfaen 25 Offshore Industry: North Sea 18 Public Sector: Wrexham 25 Performing Arts 18 Young People: Cardiff Central -

(Public Pack)Agenda Document for Cornwall and Isles of Scilly Local

Title: CIoS Local Enterprise Partnership Board Date: Wednesday 28 July 2021 Time: 10.00 to 13.00 Venue: : - Council Offices, Chy Trevail, Bodmin, PL31 2FR Livestream Link: https://teams.microsoft.com/l/meetup- join/19%3ameeting_NmFkNzY4NWMtNmVjMy00YTgxLWFhZTMtMDZlZDRlZGIyNTU5 %40thread.v2/0?context=%7b%22Tid%22%3a%22efaa16aa-d1de-4d58-ba2e- 2833fdfdd29f%22%2c%22Oid%22%3a%22fa9d3751-6eb5-4308-b8c3- 006db67ed9ac%22%2c%22IsBroadcastMeeting%22%3atrue%7d&btype=a&role=a Agenda Item Lead Action 1. 10.00 Welcome and Introductions Apologies for Absence Directors: Louis Mathers Officers: Phil Mason, John Curnow 2. 10.05 Declarations of Interest ALL 3. 10.10 LEP Board (31 March 2021) 3 .1 Minutes (Pages 3 - 11) MD To note 3 .2 Action Summary (Page 12) GCG To note 4. Strategic Matters 4 .1 10.20 Chair Update MD To note 4 .2 10.30 CEO Report, with a focus on: (Pages 13 - 65) GCG To note/ Labour market and skills challenges presentation Green Industrial Revolution 4 .3 11.25 Fishing Sector Update (Pages 66 - 68) MD/NC Decision Page 1 4 .4 11.50 Nominations Committee Update (Pages 69 - GCG Decision 122) 4 .5 12.15 Audit & Assurance Committee Update (Pages GCG Decision 123 - 198) 4 .6 12.25 Enterprise Zones Board Update (Pages 199 - SJ/GCG To note 202) 4 .7 12.35 Any other business 5. Exclusion of Press and Public 5 .1 12.40 Investment & Oversight Panel Update (Pages MD/GCG To note 203 - 206) 5 .2 12.50 Any other confidential business ALL Page 2 Agenda No. 3.1 Information Classification: CONTROLLED CORNWALL AND ISLES OF SCILLY LOCAL ENTERPRISE PARTNERSHIP MINUTES of a Meeting of the Cornwall and Isles of Scilly Local Enterprise Partnership held in the Online - Virtual Meeting on Wednesday 31 March 2021 commencing at 10.00 am. -

Corporate Business Plan 2016/17 – 2019/20

Business Plan 2016 - 2020 Delivering our Strategy www.cornwall.gov.uk Contents Page Foreword 2 1. Introduction 3 1.1 Our Strategy 3 1.2 Context 4 1.3 Our Corporate Business Plan 5 2. Progress to date – Strategic Overview: 6 Incorporates updates on the ‘Ambitious Cornwall’, ‘Engaging with our communities’ and ‘Partners working together’ strategic aims 3. Delivering the Council Strategy: Greater access, Driving the 10 economy, Stewarding the assets 3.1 Strategy, Economy, Enterprise & Environment 10 3.2 Commissioning & Asset Management 15 3.3 Planning & Enterprise 19 4. Delivering the Council Strategy: Healthier and safe 22 communities 4.1 Children’s Early Help, Psychology & Social Care 22 4.2 Commissioning Performance & Improvement 25 4.3 Adult Care & Support 29 4.4 Public Health 32 4.5 Learning and Achievement 35 4.6 Fire, Rescue and Community Safety 38 4.7 Public Protection 39 5. Delivering the Council Strategy: Being efficient, effective 45 and innovative 5.1 Customers and Communities 45 5.2 Business Planning & Development / People Management, 48 Development & Wellbeing 5.3 Governance and Information 51 6. Managing the Plan 54 6.1 Business & Service Planning 54 6.2 Performance management and reporting 55 6.3 Management of risk 55 6.4 Organisational development framework 56 7. Financial Resources 58 8. Conclusion 59 9. Acronyms 60 Corporate Business Plan 2016/17 – 2019/20 JOINT FOREWORD Welcome to the Council’s Business Plan for the next four years. When we approved our Council Strategy in 2014 we knew that we would be facing some significant challenges over the course of this decade, but also that there were tremendous opportunities for both the Council and for Cornwall if we worked with colleagues in the public, private and community sectors to deliver our ambition of creating a more sustainable and prosperous Cornwall that is resilient and resourceful, a place where communities are strong and where the most vulnerable are protected. -

ERDF Convergence Progress Report, Jun 2014 DRAFT.Pub

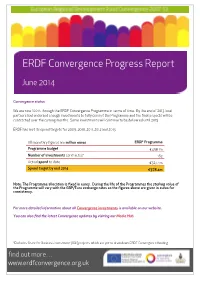

ERDF Convergence Progress Report June 2014 Convergence status We are now 100% through the ERDF Convergence Programme in terms of time. By the end of 2013 local partners had endorsed enough investments to fully commit the Programme and the final projects will be contracted over the coming months. Some investments will continue to be delivered until 2015. ERDF has met its spend targets for 2009, 2010, 2011, 2012 and 2013. All monetary figures are million euros ERDF Programme Programme budget €458.1m Number of investments contracted* 163 Actual spend to date €327.4m Spend target by end 2014 €378.4m Note: The Programme allocation is fixed in euros. During the life of the Programmes the sterling value of the Programme will vary with the GBP/Euro exchange rates so the figures above are given in euros for consistency. For more detailed information about all Convergence investments is available on our website. You can also find the latest Convergence updates by visiting our Media Hub. *Excludes Grant for Business Investment (GBI) projects which are yet to draw down ERDF Convergence funding. find out more… www.erdfconvergence.org.uk CONVERGENCE INVESTMENTS New Investments Apple Aviation Ltd Apple Aviation, an aircraft maintenance, repair and overhaul company, has established a base at Newquay Airport’s Aerohub. Convergence funding from the Grant for Business Investment programme will contribute to salary costs for thirteen new jobs in the business. ERDF Convergence investment: £211,641 (through the GBI SIF) Green Build Hub Located alongside the Eden Project, the Green Build Hub will be a research facility capable of demonstrating and testing the performance of innovative sustainable construction techniques and materials in a real building setting. -

The UK's Evolving Human Landscape

The UK’s Evolving Human Landscape Knowledge checklist Key ideas How secure is my knowledge? . Population, economic activities and settlements are key elements of the human landscape and the UK is closely linked to the wider world - Differences between urban core and rural and how UK and EU government policies have attempted to reduce - Why national and international migration over the past 50 years has altered the population geography of the UK and how UK and EU immigration policy has contributed to increasing ethnic and cultural diversity - Why the decline in primary and secondary sectors and the rise of the tertiary and quaternary sectors in urban and rural areas has altered economic and employment structure in contrasting regions of the UK - Why globalisation, free-trade polices (UK and EU) and privatisation has increased foreign direct investment (FDI) and the role of TNCs in the UK economy The context of the city influences its functions and structure, employment, services and opportunities. Further, how the area is improving and also detached from rural areas - Significance of site, situation and connectivity of the city in a national, regional and global context - The city’s structure (Central Business District (CBD), inner city, suburbs, urban-rural fringe), in terms of its functions and variations in building age and density, land-use and environmental quality - Causes of national and international migration that influence growth and character the different parts of the city - Reasons for different levels of inequality, in employment -

The Airport the Airport

THE AIRPORT OPERATOR THE OFFICIAL MAGAZINE OF THE AIRPORT OPERATORS ASSOCIATION AIRPORTS INVESTMENT BOOM Multi-billion plans Features EDINBURGH AOA MANIFESTO Recipe for success Ambitious agenda CORNWALL AIRPORT NEW AIRPORT CHIEF NEWQUAY EXECUTIVES SUMMER 2017 Fastest-growing UK airport Sinclair heads for London City ADVERT 3 ED ANDERSON Introduction to the Airport Operator THE AIRPORT invisible infrastructure in the sky that OPERATOR Welcome has changed little since the 1960’s, THE OFFICIAL MAGAZINE OF THE AIRPORT OPERATORS ASSOCIATION renewed our call for a 50% cut in Air to this Passenger Duty and emphasised the AIRPORT OPERATORS ASSOCIATION importance of having a well-resourced edition Border Force that will be able to cope Ed Anderson with increased passenger flows. Chairman of the Karen Dee Operator, As I write this introduction, the Chief Executive Government is embarking on the first stages of what will no doubt be a long Peter O’Broin which is and complex negotiation to implement Policy Manager published the referendum vote for the UK to Henk van Klaveren leave the European Union. The AOA Public Affairs & PR Manager online on the occasion has worked hard over recent months Roger Koukkoullis of the summer 2017 to explain to officials and politicians of Operations, Safety all parties that aviation currently relies & Commercial Director aviation Parliamentary on the legal framework provided by Claire Humphries reception. EU-level air services agreements for Events & Member Following the General Election the flights to over 40 countries. We have Relations Manager reception will provide us with a timely also emphasised that early certainty on Patricia Page opportunity to meet newly-elected how these agreements will be replaced Executive Assistant and re-elected MPs and to explain is vital, as airlines typically plan their & Office Manager how the Government and Parliament routes 12 to 18 months in advance. -

European Regional Development Fund England Operational Programme 2014 to 2020

European Regional Development Fund England Operational Programme 2014 to 2020 June 2014 Department for Communities and Local Government Draft Version 8.0 01.06.2014 © Crown copyright, 2014 Copyright in the typographical arrangement rests with the Crown. You may re-use this information (not including logos) free of charge in any format or medium, under the terms of the Open Government Licence. To view this licence, www.nationalarchives.gov.uk/doc/open-government-licence/ or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: [email protected]. This document/publication is also available on our website at www.gov.uk/dclg If you have any enquiries regarding this document/publication, email [email protected] or write to us at: Department for Communities and Local Government Eland House Bressenden Place London SW1E 5DU Telephone: 030 3444 0000 For all our latest news and updates follow us on Twitter: https://twitter.com/CommunitiesUK June 2014 ISBN: 978-1-4098-4266-8 2 Draft Version 8.0 01.06.2014 Template and Guidelines for the Content of the Operational Programme The headings in this document correspond to the elements set out in the Articles 24 and 87 of the Common Provisions Regulation. The text boxes provide guidelines on the drafting of the content of the Operational Programme. It is recalled that the Operational Programmes will be directly introduced in the SFC. The character limits proposed are based on the needs of most extensive programmes, the pages estimations are based on a standard page using the font "Times new roman 12". -

Dear Mr Sunak Letter from Cornwall and the Isles of Scilly Leadership

Information Classification: CONTROLLED The Rt Hon Rishi Sunak MP Chancellor of the Exchequer Via email: [email protected] 8 April 2020 Dear Mr Sunak Letter from Cornwall and the Isles of Scilly Leadership Board regarding the UK government response to COVID19 We warmly welcome the quick and comprehensive package of support that the UK government has put in place to support the economy across the UK at this difficult time, and we would like to thank you personally for the strong leadership you have shown in this respect. At a local level we are in direct contact with the businesses and individuals that are accessing these support measures, and the feedback that they are giving us has enabled us to identify some gaps and unintended consequences that need to be addressed urgently in order to ensure that our local economy will be able to rebound quickly once we have steered clear of the public health crisis that we currently find ourselves in. In order to ensure that our local businesses and communities can remain viable, to support businesses be to agile and responsive to opportunities and ultimately to ensure that we can protect jobs and prosperity long term, we have the following asks: • Furloughed workers. More flexibility is needed in relation to two key aspects. Firstly, there is a lack of flexibility for employers to bring back furloughed staff on a part time or short term basis to fulfil orders or to address a specific piece of work such as opening up closed down holiday accommodation for the use of key workers. -

The South Coast Marine Cluster: Marine Inward Investment Evidence Study

The South Coast Marine Cluster: Marine Inward Investment Evidence Study June 2017 Wavehill Ltd. • Wales office: 21 Alban Square, Aberaeron, Ceredigion, SA46 0DB (registered office) • West England office: 217 Paintworks, Arnos Vale, Bristol, BS4 3AH Contact details: Tel: 01545 571711 Email: [email protected] Twitter: @wavehilltweets More information: www.wavehill.com https://twitter.com/wavehilltweets © Wavehill Ltd. This report is subject to copyright. The authors of the report (Wavehill Ltd.) should be acknowledged in any reference that is made to its contents. Authors: Andrew Engeli Anna Burgess Dareece James Any questions in relation to this report should be directed in the first instance to Andrew Engeli ([email protected]) Date of document: 29th June 2017 Version: Final Client contact: Julia Stuckey [email protected] The South Coast Marine Cluster: Marine Inward Investment Evidence Study Acknowledgements We would like to thank the many individuals who gave their time to assist in the evaluation, including Julia Stuckey, Mark Pemberton, Alex Clothier, Thomas Clenaghan, Jim Grant, Sheldon Ryan, Steven Rice, Eifion Jones, Anthony Payne, Kevin Forshaw, and the other members of the SCMC partnership, all of whom were important in the writing of this report. This evaluation would not have been possible without all of these contributions. We would also like to thank the generosity of the senior decision makers in the companies interviewed for workstream three, whose time and patience answering our detailed question contributed enormously to enriching the portrait of the SCMC as a vibrant and diverse home for Marine and Maritime related activities. List of abbreviations SCMC South Coast Marine Cluster MMS Marine and maritime sector i The South Coast Marine Cluster: Marine Inward Investment Evidence Study Contents Table of tables ...................................................................................................................... -

RETALLACK SURNAME March 9 2000 by Greg Retallack

RETALLACK SURNAME March 9 2000 by Greg Retallack, Department of Geological Sciences, University of Oregon, Eugene, OR 97403-1272:gregr@ darkwing.uoregon.edu;http://darkwing.uoregon.edu/~dogsci Abstract Retallack is a name endemic to Cornwall, and traceable in that southwestern English county back to 1497. The name is probably derived from Talek, recorded back to 1349, by addition of a demonstrative pronoun (those Taleks!). Talek in turn is most likely from the old Cornish talawg meaning high forehead. The comparable Welsh name Tallwch and Pictish Talorc can be traced back to the 6th century. There are numerous other ideas concerning the origin of the Retallack surname from Cornish place names, Cornish saints, mine workings and Norse and Greek gods, and these are all reviewed here. Retallacks in Cornwall were largely miners and farmers. Many left Cornwall for the United States and Australia in the 1850's. I emigrated to the U.S.A. in 1977, but my great great grandfather emigrated in 1852 to Australia, where I was born and raised. Introduction The Retallack name is unusual and often requires careful spelling out. Pronunciation is also a challenge (correct is r'-TAL-lack, rhymes with metallic). With the advent of the internet and computer-generated genealogical research I have been getting frequent requests for information on the surname and its ancestry. Here is as much as I can reconstruct. Retallack is endemic to Cornwall, England, where it has been a rare name back to the 15th century (Table 1). Since the 19th century it has been part of a global emigration (Table 2) so that there are now more Retallacks in Australia and the U.S. -

Journeys of the Cornish & History of Settlement in North America

Journeys of the Cornish & History of Settlement in North America Rosalie Armstrong February 2008 INTRODUCTION This presentation will look at some journeys of the Cornish and a little of the history of the Cornish settlement in America, especially in Ontario. Much of the material comes from surveys that Toronto Cornish Association members filled in for me in 2007 and from other CAHS members earlier - Americans who came to Ontario first. This will not be a formal history but an impression in photographs, poetry, and words from your ancestors, to evoke the painful and exciting story of a people moving from one continent to another, from one culture to FOUND another, in a very different world. Your ancestors who left Cornwall were mainly farmers. It is sure you know more of the history of Ontario than I do, and it goes without saying that you have more intense tales from your ancestors than I have. Perhaps I can hope to do justice to both from a Cornish perspective; almost two hundred years after those brave souls risked all to find a better life in the New World. Even growing up in Cornwall in the mid-20th century, from a very early age I was aware of America. My mother sang "John Brown's Body" and "God Bless America" as she pinned the clothes on the line in a windy Cornish garden, in memory of those, still treasured, who had left. Now we have come full circle and in your return on holidays in Cornwall, in your genealogical excavations of your people, you give to the Cornish a sense of pride just when it is needed, just when the speed of change threatens so much. -

Cios EU Impact Final Report

Report The benefit of EU Structural Investment Funds for Cornwall and the Isles of Scilly November 2019 Ash Futures Impact of EU funding in Cornwall and the Isles of Scilly 1 Ash Futures CONTENTS 1 Executive Summary 3 2 Introduction 8 3 Review of Operational Programmes 9 4 Themes 16 5 Case Studies 39 6 Benchmarking 53 7 What if Scenarios 63 8 Lessons Learned 76 9 Further Questions 81 Annexes - 83 ASH FUTURES LTD Lead author: Shane Vallance Other contributions: Simon Hooton, Jo Talbot, Robin Miller, Rebekah Southern Impact of EU funding in Cornwall and the Isles of Scilly 2 Ash Futures 1. EXECUTIVE SUMMARY Benchmarking This report looks at the impact to date, and ongoing impact expected The aim of the benchmarking exercise is to understand CIoS from, the current and previous rounds of European investment within performance against a number of areas that display similar Cornwall and the Isles of Scilly (CIoS). This covers three programme characteristics. All areas within the UK differ and, in that respect, CIoS periods: Objective One (1999-2006), Convergence (2007-2013) and cannot be compared directly to any single area. For the purposes of Growth Programme (2014-2020). this exercise, output (as measured by GVA) in 1997 (in £m) and population in 2018 were used to identify potential suitable areas The report considers all sources of EU funding which have been through a proximity analysis. We identified eight alternative areas available as a result of CIoS being recognised as a ‘Less Developed against which to compare CIoS performance. While most were rural to Region’ for EU Structural Fund support.