Cios EU Impact Final Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Daily Report Thursday, 20 July 2017 CONTENTS

Daily Report Thursday, 20 July 2017 This report shows written answers and statements provided on 20 July 2017 and the information is correct at the time of publication (06:34 P.M., 20 July 2017). For the latest information on written questions and answers, ministerial corrections, and written statements, please visit: http://www.parliament.uk/writtenanswers/ CONTENTS ANSWERS 10 Social Tariffs: Torfaen 19 ATTORNEY GENERAL 10 Taxation: Electronic Hate Crime: Prosecutions 10 Government 19 BUSINESS, ENERGY AND Technology and Innovation INDUSTRIAL STRATEGY 10 Centres 20 Business: Broadband 10 UK Consumer Product Recall Review 20 Construction: Employment 11 Voluntary Work: Leave 21 Department for Business, Energy and Industrial Strategy: CABINET OFFICE 21 Mass Media 11 Brexit 21 Department for Business, Elections: Subversion 21 Energy and Industrial Strategy: Electoral Register 22 Staff 11 Government Departments: Directors: Equality 12 Procurement 22 Domestic Appliances: Safety 13 Intimidation of Parliamentary Economic Growth: Candidates Review 22 Environment Protection 13 Living Wage: Jarrow 23 Electrical Safety: Testing 14 New Businesses: Newham 23 Fracking 14 Personal Income 23 Insolvency 14 Public Sector: Blaenau Gwent 24 Iron and Steel: Procurement 17 Public Sector: Cardiff Central 24 Mergers and Monopolies: Data Public Sector: Ogmore 24 Protection 17 Public Sector: Swansea East 24 Nuclear Power: Treaties 18 Public Sector: Torfaen 25 Offshore Industry: North Sea 18 Public Sector: Wrexham 25 Performing Arts 18 Young People: Cardiff Central -

(Public Pack)Agenda Document for Cornwall and Isles of Scilly Local

Title: CIoS Local Enterprise Partnership Board Date: Wednesday 28 July 2021 Time: 10.00 to 13.00 Venue: : - Council Offices, Chy Trevail, Bodmin, PL31 2FR Livestream Link: https://teams.microsoft.com/l/meetup- join/19%3ameeting_NmFkNzY4NWMtNmVjMy00YTgxLWFhZTMtMDZlZDRlZGIyNTU5 %40thread.v2/0?context=%7b%22Tid%22%3a%22efaa16aa-d1de-4d58-ba2e- 2833fdfdd29f%22%2c%22Oid%22%3a%22fa9d3751-6eb5-4308-b8c3- 006db67ed9ac%22%2c%22IsBroadcastMeeting%22%3atrue%7d&btype=a&role=a Agenda Item Lead Action 1. 10.00 Welcome and Introductions Apologies for Absence Directors: Louis Mathers Officers: Phil Mason, John Curnow 2. 10.05 Declarations of Interest ALL 3. 10.10 LEP Board (31 March 2021) 3 .1 Minutes (Pages 3 - 11) MD To note 3 .2 Action Summary (Page 12) GCG To note 4. Strategic Matters 4 .1 10.20 Chair Update MD To note 4 .2 10.30 CEO Report, with a focus on: (Pages 13 - 65) GCG To note/ Labour market and skills challenges presentation Green Industrial Revolution 4 .3 11.25 Fishing Sector Update (Pages 66 - 68) MD/NC Decision Page 1 4 .4 11.50 Nominations Committee Update (Pages 69 - GCG Decision 122) 4 .5 12.15 Audit & Assurance Committee Update (Pages GCG Decision 123 - 198) 4 .6 12.25 Enterprise Zones Board Update (Pages 199 - SJ/GCG To note 202) 4 .7 12.35 Any other business 5. Exclusion of Press and Public 5 .1 12.40 Investment & Oversight Panel Update (Pages MD/GCG To note 203 - 206) 5 .2 12.50 Any other confidential business ALL Page 2 Agenda No. 3.1 Information Classification: CONTROLLED CORNWALL AND ISLES OF SCILLY LOCAL ENTERPRISE PARTNERSHIP MINUTES of a Meeting of the Cornwall and Isles of Scilly Local Enterprise Partnership held in the Online - Virtual Meeting on Wednesday 31 March 2021 commencing at 10.00 am. -

Cornwall. Pub 1445

TRADES DIRECTORY.] CORNWALL. PUB 1445 . Barley Sheaf, Mrs. Mary Hawken, Lower Bore st. Bodmin Commercial hotel,John Wills,Dowugate,Linkiuhorne,Liskrd Barley Sheaf, Mrs. Elizabeth Hill, Church street, Liskeard Commercial hotel & posting house, Abraham Bond, Gunnis~ Barley Sheaf inn, Fred Liddicoat, Union square, St. Columb lake, Tavistock Major R.S.O Commercial hotel & posting establishment (Herbert Henry Barley Sheaf hotel, Mrs. Elizh. E. Reed, Old Bridge st. Truro Hoare, proprietor), Grampound Road Barley Sheaf, William Richards, Gorran, St. Austell Commercial hotel, family, commercial & posting house, Basset Arms, William Laity, Basset road, Camborne William Alfred Holloway, Porthleven, Helston Basset Arms, Solomon Rogers, Pool, Carn Brea R.S. 0 Commercial hotel, family, commercial & posting, Richard Basset Arms, Charles Wills, Portreath, Redruth Lobb. South quay, Padstow R.S.O Bay Tree, Mrs. Elizabeth Rowland, Stratton R.S.O Cornish Arms, Thomas Butler, Crockwell street, Bodmin .Bennett's Arms, Charles Barriball, Lawhitton, Launceston Cornish Arms, Jarues Collins, Wadebridge R.S.O Bell inn, William Ca·rne, Meneage street, Helston Cornish Arms, Mrs. Elizh. Eddy, Market Jew st. Penzance Bell inn, Daniel Marshall, Tower street, Launceston Cornish Arms, Jakeh Glasson, Trelyon, St. Ives R.S.O Bell commercial hotel & posting house, Mrs. Elizabeth Cornish Arms, Nicholas Hawken, Pendoggett, St. Kew, Sargent, Church street, Li.skeard Wadebridge R.S.O Bideford inn, Lewis Butler, l:ltratton R.S. 0 Cornish Arms, William LObb, St. Tudy R.S.O Black Horse, Richard Andrew, Kenwyn street, Truro CornishArms,Mrs.M.A. Lucas,St. Dominick,St. MellionR. S. 0 BliBland inn, Mrs. R. Williams, Church town,Blislaud,Bodmin Cornish Arms, Rd. -

The Cornwall and Isles of Scilly Local Enterprise Partnership (LEP) Was Launched in May 2011

Written evidence submitted by Cornwall and Isles of Scilly Local Enterprise Partnership (INS0039) The Cornwall and Isles of Scilly Local Enterprise Partnership (LEP) was launched in May 2011. Private sector-led, it is a partnership between the private and public sectors and is driving the economic strategy for the region, determining local priorities and undertaking activities to drive growth and the creation of local jobs. Executive Summary The Government’s Industrial Strategy should be refreshed to include wider economic, social and environmental factors that are now in play post Covid 19 by building on all of England’s Local Industrial Strategies. Industrial Strategy Grand Challenges should be updated and localised, within a national framework, and should consider the levelling up agenda, climate change, regional imbalances and measures to reduce inequality/social inclusion. The refresh should use the guiding principle of devolving decision making and delivery. The focus on key sectors in the current Industrial Strategy is sufficient if a narrow view on “growth” is used or if “trickle down” economic policies are adopted. However, whilst this approach will raise the productivity and growth of some areas it will not benefit all areas equally and those areas furthest from key industrial centres will see little or no benefit. As the future prosperity of the UK depends on unlocking the potential of all its areas, towns, high streets businesses and residents the revised Industrial Strategy needs to be more inclusive and allow for different areas to make different contributions to overall productivity levels and growth. The immense productivity gap that currently exists between the prosperous South East of England and the rest of the country on the other must be therefore be levelled-up by investing in the LEP areas that are currently lagging behind. -

Corporate Business Plan 2016/17 – 2019/20

Business Plan 2016 - 2020 Delivering our Strategy www.cornwall.gov.uk Contents Page Foreword 2 1. Introduction 3 1.1 Our Strategy 3 1.2 Context 4 1.3 Our Corporate Business Plan 5 2. Progress to date – Strategic Overview: 6 Incorporates updates on the ‘Ambitious Cornwall’, ‘Engaging with our communities’ and ‘Partners working together’ strategic aims 3. Delivering the Council Strategy: Greater access, Driving the 10 economy, Stewarding the assets 3.1 Strategy, Economy, Enterprise & Environment 10 3.2 Commissioning & Asset Management 15 3.3 Planning & Enterprise 19 4. Delivering the Council Strategy: Healthier and safe 22 communities 4.1 Children’s Early Help, Psychology & Social Care 22 4.2 Commissioning Performance & Improvement 25 4.3 Adult Care & Support 29 4.4 Public Health 32 4.5 Learning and Achievement 35 4.6 Fire, Rescue and Community Safety 38 4.7 Public Protection 39 5. Delivering the Council Strategy: Being efficient, effective 45 and innovative 5.1 Customers and Communities 45 5.2 Business Planning & Development / People Management, 48 Development & Wellbeing 5.3 Governance and Information 51 6. Managing the Plan 54 6.1 Business & Service Planning 54 6.2 Performance management and reporting 55 6.3 Management of risk 55 6.4 Organisational development framework 56 7. Financial Resources 58 8. Conclusion 59 9. Acronyms 60 Corporate Business Plan 2016/17 – 2019/20 JOINT FOREWORD Welcome to the Council’s Business Plan for the next four years. When we approved our Council Strategy in 2014 we knew that we would be facing some significant challenges over the course of this decade, but also that there were tremendous opportunities for both the Council and for Cornwall if we worked with colleagues in the public, private and community sectors to deliver our ambition of creating a more sustainable and prosperous Cornwall that is resilient and resourceful, a place where communities are strong and where the most vulnerable are protected. -

Cornwall Council Altarnun Parish Council

CORNWALL COUNCIL THURSDAY, 4 MAY 2017 The following is a statement as to the persons nominated for election as Councillor for the ALTARNUN PARISH COUNCIL STATEMENT AS TO PERSONS NOMINATED The following persons have been nominated: Decision of the Surname Other Names Home Address Description (if any) Returning Officer Baker-Pannell Lisa Olwen Sun Briar Treween Altarnun Launceston PL15 7RD Bloomfield Chris Ipc Altarnun Launceston Cornwall PL15 7SA Branch Debra Ann 3 Penpont View Fivelanes Launceston Cornwall PL15 7RY Dowler Craig Nicholas Rivendale Altarnun Launceston PL15 7SA Hoskin Tom The Bungalow Trewint Marsh Launceston Cornwall PL15 7TF Jasper Ronald Neil Kernyk Park Car Mechanic Tredaule Altarnun Launceston Cornwall PL15 7RW KATE KENNALLY Dated: Wednesday, 05 April, 2017 RETURNING OFFICER Printed and Published by the RETURNING OFFICER, CORNWALL COUNCIL, COUNCIL OFFICES, 39 PENWINNICK ROAD, ST AUSTELL, PL25 5DR CORNWALL COUNCIL THURSDAY, 4 MAY 2017 The following is a statement as to the persons nominated for election as Councillor for the ALTARNUN PARISH COUNCIL STATEMENT AS TO PERSONS NOMINATED The following persons have been nominated: Decision of the Surname Other Names Home Address Description (if any) Returning Officer Kendall Jason John Harrowbridge Hill Farm Commonmoor Liskeard PL14 6SD May Rosalyn 39 Penpont View Labour Party Five Lanes Altarnun Launceston Cornwall PL15 7RY McCallum Marion St Nonna's View St Nonna's Close Altarnun PL15 7RT Richards Catherine Mary Penpont House Altarnun Launceston Cornwall PL15 7SJ Smith Wes Laskeys Caravan Farmer Trewint Launceston Cornwall PL15 7TG The persons opposite whose names no entry is made in the last column have been and stand validly nominated. -

ERDF Convergence Progress Report, Jun 2014 DRAFT.Pub

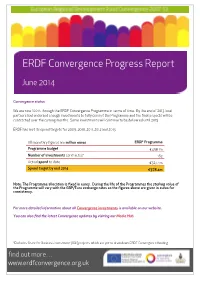

ERDF Convergence Progress Report June 2014 Convergence status We are now 100% through the ERDF Convergence Programme in terms of time. By the end of 2013 local partners had endorsed enough investments to fully commit the Programme and the final projects will be contracted over the coming months. Some investments will continue to be delivered until 2015. ERDF has met its spend targets for 2009, 2010, 2011, 2012 and 2013. All monetary figures are million euros ERDF Programme Programme budget €458.1m Number of investments contracted* 163 Actual spend to date €327.4m Spend target by end 2014 €378.4m Note: The Programme allocation is fixed in euros. During the life of the Programmes the sterling value of the Programme will vary with the GBP/Euro exchange rates so the figures above are given in euros for consistency. For more detailed information about all Convergence investments is available on our website. You can also find the latest Convergence updates by visiting our Media Hub. *Excludes Grant for Business Investment (GBI) projects which are yet to draw down ERDF Convergence funding. find out more… www.erdfconvergence.org.uk CONVERGENCE INVESTMENTS New Investments Apple Aviation Ltd Apple Aviation, an aircraft maintenance, repair and overhaul company, has established a base at Newquay Airport’s Aerohub. Convergence funding from the Grant for Business Investment programme will contribute to salary costs for thirteen new jobs in the business. ERDF Convergence investment: £211,641 (through the GBI SIF) Green Build Hub Located alongside the Eden Project, the Green Build Hub will be a research facility capable of demonstrating and testing the performance of innovative sustainable construction techniques and materials in a real building setting. -

The UK's Evolving Human Landscape

The UK’s Evolving Human Landscape Knowledge checklist Key ideas How secure is my knowledge? . Population, economic activities and settlements are key elements of the human landscape and the UK is closely linked to the wider world - Differences between urban core and rural and how UK and EU government policies have attempted to reduce - Why national and international migration over the past 50 years has altered the population geography of the UK and how UK and EU immigration policy has contributed to increasing ethnic and cultural diversity - Why the decline in primary and secondary sectors and the rise of the tertiary and quaternary sectors in urban and rural areas has altered economic and employment structure in contrasting regions of the UK - Why globalisation, free-trade polices (UK and EU) and privatisation has increased foreign direct investment (FDI) and the role of TNCs in the UK economy The context of the city influences its functions and structure, employment, services and opportunities. Further, how the area is improving and also detached from rural areas - Significance of site, situation and connectivity of the city in a national, regional and global context - The city’s structure (Central Business District (CBD), inner city, suburbs, urban-rural fringe), in terms of its functions and variations in building age and density, land-use and environmental quality - Causes of national and international migration that influence growth and character the different parts of the city - Reasons for different levels of inequality, in employment -

The Airport the Airport

THE AIRPORT OPERATOR THE OFFICIAL MAGAZINE OF THE AIRPORT OPERATORS ASSOCIATION AIRPORTS INVESTMENT BOOM Multi-billion plans Features EDINBURGH AOA MANIFESTO Recipe for success Ambitious agenda CORNWALL AIRPORT NEW AIRPORT CHIEF NEWQUAY EXECUTIVES SUMMER 2017 Fastest-growing UK airport Sinclair heads for London City ADVERT 3 ED ANDERSON Introduction to the Airport Operator THE AIRPORT invisible infrastructure in the sky that OPERATOR Welcome has changed little since the 1960’s, THE OFFICIAL MAGAZINE OF THE AIRPORT OPERATORS ASSOCIATION renewed our call for a 50% cut in Air to this Passenger Duty and emphasised the AIRPORT OPERATORS ASSOCIATION importance of having a well-resourced edition Border Force that will be able to cope Ed Anderson with increased passenger flows. Chairman of the Karen Dee Operator, As I write this introduction, the Chief Executive Government is embarking on the first stages of what will no doubt be a long Peter O’Broin which is and complex negotiation to implement Policy Manager published the referendum vote for the UK to Henk van Klaveren leave the European Union. The AOA Public Affairs & PR Manager online on the occasion has worked hard over recent months Roger Koukkoullis of the summer 2017 to explain to officials and politicians of Operations, Safety all parties that aviation currently relies & Commercial Director aviation Parliamentary on the legal framework provided by Claire Humphries reception. EU-level air services agreements for Events & Member Following the General Election the flights to over 40 countries. We have Relations Manager reception will provide us with a timely also emphasised that early certainty on Patricia Page opportunity to meet newly-elected how these agreements will be replaced Executive Assistant and re-elected MPs and to explain is vital, as airlines typically plan their & Office Manager how the Government and Parliament routes 12 to 18 months in advance. -

Gardens Guide

Gardens of Cornwall map inside 2015 & 2016 Cornwall gardens guide www.visitcornwall.com Gardens Of Cornwall Antony Woodland Garden Eden Project Guide dogs only. Approximately 100 acres of woodland Described as the Eighth Wonder of the World, the garden adjoining the Lynher Estuary. National Eden Project is a spectacular global garden with collection of camellia japonica, numerous wild over a million plants from around the World in flowers and birds in a glorious setting. two climatic Biomes, featuring the largest rainforest Woodland Garden Office, Antony Estate, Torpoint PL11 3AB in captivity and stunning outdoor gardens. Enquiries 01752 814355 Bodelva, St Austell PL24 2SG Email [email protected] Enquiries 01726 811911 Web www.antonywoodlandgarden.com Email [email protected] Open 1 Mar–31 Oct, Tue-Thurs, Sat & Sun, 11am-5.30pm Web www.edenproject.com Admissions Adults: £5, Children under 5: free, Children under Open All year, closed Christmas Day and Mon/Tues 5 Jan-3 Feb 16: free, Pre-Arranged Groups: £5pp, Season Ticket: £25 2015 (inclusive). Please see website for details. Admission Adults: £23.50, Seniors: £18.50, Children under 5: free, Children 6-16: £13.50, Family Ticket: £68, Pre-Arranged Groups: £14.50 (adult). Up to 15% off when you book online at 1 H5 7 E5 www.edenproject.com Boconnoc Enys Gardens Restaurant - pre-book only coach parking by arrangement only Picturesque landscape with 20 acres of Within the 30 acre gardens lie the open meadow, woodland garden with pinetum and collection Parc Lye, where the Spring show of bluebells is of magnolias surrounded by magnificent trees. -

Tremayne Family History

TREMAYNE FAMILY HISTORY 1 First Generation 1 Peter/Perys de Tremayne (Knight Templar?) b abt 1240 Cornwall marr unknown abt 1273.They had the following children. i. John Tremayne b abt 1275 Cornwall ii. Peter Tremayne b abt 1276 Cornwall Peter/Perys de Tremayne was Lord of the Manor of Tremayne in St Martin in Meneage, Cornwall • Meneage in Cornish……Land of the Monks. Peter named in De Banco Roll lEDWl no 3 (1273) SOME FEUDAL COATS of ARMS by Joseph Foster Perys/Peter Tremayne. El (1272-1307). Bore, gules, three dexter arms conjoined and flexed in triangle or, hands clenched proper. THE CARTULARY OF ST. MICHAELS MOUNT. The Cartulary of St Michaels Mount contains a charter whereby Robert, Count of Mortain who became Earl of Cornwall about 1075 conferred on the monks at St Michaels Mount 3 acres in Manech (Meneage) namely Treboe, Lesneage, Tregevas and Carvallack. This charter is confirmed in substance by a note in the custumal of Otterton Priory that the church had by gift of Count Robert 2 plough lands in TREMAINE 3 in Traboe 3 in Lesneage 2 in Tregevas and 2 in Carvallack besides pasture for all their beasts ( i.e. on Goonhilly) CORNISH MANORS. It was usual also upon Cornish Manors to pay a heriot (a fine) of the best beast upon the death of a tenant; and there was a custom that if a stranger passing through the County chanced to die, a heriot of his best beast was paid, or his best jewel, or failing that his best garments to the Lord of the Manor. -

COM 575 Wicca, Treveal, Tremedda, Tregerthen36 Long Stone Croft

Application Decision Hearing held on 18 February 2015 by Heidi Cruickshank BSc MSc MIPROW Appointed by the Secretary of State for Environment, Food and Rural Affairs Decision date: 21 April 2015 Application Ref: COM 575 Tremedda, Tregerthen, Wicca and Treveal Cliff, Zennor, Cornwall Register Unit No: CL7041 Commons Registration Authority: Cornwall Council The application, dated 26 March 2013, is made under paragraph 4 of Schedule 2 of the Commons Act 2006. The application is made by Mr D Coles on behalf of Save Penwith Moors. The application is to register waste land of a manor in the Register of Common Land. Decision 1. The application is approved in part. The land outlined and cross-hatched in red on the plan attached to this decision shall be added to the Register of Common Land (“the RCL”). Preliminary Matters Guidance 2. The applicants, Save Penwith Moors (“SPM”), argued that the Department for Environment, Food and Rural Affairs (“defra”) guidance that should be referred to in this case was that which was extant at the date of their application. The application was received by Cornwall Council, the Commons Registration Authority (“the CRA”) on 10 April 2013. 3. Cornwall was one of the pilot areas and, therefore, the “Part 1 of the Commons Act 2006, Guidance to commons registration authorities and the Planning Inspectorate for the pioneer implementation” was relevant guidance. Revisions have been made, with the latest, published in December 2014 (“the guidance”). “Part 1 of the Commons Act 2006, Guidance to commons registration authorities and the Planning Inspectorate”, version 2.0 relates to the full implementation of Part 1 of the Commons Act 2006 (“the 2006 Act”) in a minority of registration authorities and the partial implementation in remaining registration authorities through The Commons Registration (England) Regulations 20142.