Metcash Limited Annual Report Successful Independents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

June 2019 42

y 4 6 Equit 2019 June High Conviction High Quarterly NewsletterQuarterly No. Selector Fund In this quarterly edition, we review performance and attribution for the quarter. We highlight the importance of innovation and culture within organisations and profile ResMed and Cochlear, two leading healthcare businesses. We visit Fisher & Paykel Healthcare in New Zealand and look at one of the biggest growth industries in the world today, cyber security. Photo. Selector analyst trekking through the Atlas Mountains and local Berber kids. Selector Funds Management Limited ACN 102756347 AFSL 225316 Level 8, 10 Bridge Street Sydney NSW 2000 Australia Tel 612 8090 3612 www.selectorfund.com.au P Selector is a boutique fund manager. Our team, combined, have over 150 years of experience in financial markets. We believe in long-term wealth creation and building lasting relationships with our investors. We focus on stock selection, the funds are high conviction, concentrated and index unaware. As a result, the portfolios have low turnover and produce tax effective returns. Selector has a 15-year track record of outperformance and we continue to seek businesses with leadership qualities, run by competent management teams, underpinned by strong balance sheets and with a focus on capital management. Selector High Conviction Equity Fund Quarterly Newsletter #64 CONTENTS IN BRIEF – JUNE QUARTER 3 PORTFOLIO OVERVIEW 5 PORTFOLIO CONTRIBUTORS 7 MARKET INSIGHTS AND OBSERVATIONS 13 INNOVATION + CULTURE = SUCCESS 17 RESMED INC. 20 WAKE-UP CALL 31 FISHER & PAYKEL HEALTHCARE – JUNE 2019 42 RISK OUT…UPFRONT 45 COMPANY VISIT DIARY – JUNE 2019 QUARTER 57 2 Selector Funds Management IN BRIEF – JUNE QUARTER Dear Investor, Looking back on 2019, it would be fair to say that few identify the businesses we want to own on a case by case foresaw how the events of the financial year would basis, understand them to the best of our abilities and unfold. -

Australian Investment Strategy

2 November 2016 Asia Pacific/Australia Equity Research Investment Strategy Australian Investment Strategy Research Analysts STRATEGY Hasan Tevfik ,CFA 61 2 8205 4284 [email protected] Aussie darlings Peter Liu 61 2 8205 4071 ■ Aussies love their darlings: Australia currently has the most expensive [email protected] equity market "Darlings" in the world. Our darlings trade on a forward P/E Damien Boey of 38x. The other commodity-focused market, Canada, has the second 61 2 8205 4615 [email protected] most expensive darlings. Darlings in Australia have been more expensive only during the Nasdaq bubble when they touched 45x. ■ Darling derating: Buying Australian darlings at these valuations has been a poor strategy in the past. Also, the current high valuation for Australia's darlings suggest they are especially vulnerable to rising bond yields and the coming end of the Australian profits recession. A rising discount rate and a lower premium for growth suggest investors should focus on stocks that could be future darlings. ■ Hello Daaarling: Future market darlings have shared many similar characteristics over the last 20 years. They are generally well managed, have strong balance sheets and operate on high margins. Our "Hello Daaarling" strategy highlights potential future darlings and they currently trade on just 17x P/E and include Caltex, Eclipx, Mayne Pharma, Nufarm, Star Entertainment and South 32. We add Eclipx to our long Portfolio. Figure 1: Australia has the most expensive darlings in the world Median 12-month forward P/E of "market darlings" around the world* 40 35 30 25 20 15 10 Australia Canada Cont. -

Smallco Investment Fund

Smallco Investment Fund Quarterly Update 30 September 2014 SIF Portfolio Commentary SIF Performance Smallco Investment Fund (SIF) delivered 6.8% during the Return to 30 September 2014 September quarter and for the 12 months was up a solid 12.3%. During the quarter Iress, Isentia Group and Sirtex 3 months 6.8% Medical performed positively, while Carsales.com, Ozforex 1 year 12.3% Group and Macquarie Atlas Roads were negative 3 year p.a. 36.4% contributors. 5 year p.a. 22.5% For the September quarter the Small Ordinaries index was 10 year p.a. 13.6% modestly positive at 1.5% while for the year to 30 Since inception (31.10.00) p.a. 14.2% September it was down -0.1%. Value of $100,000 invested at inception $631,173 In general the Australian market had a solid reporting Fund returns calculated after all fees and expenses and based season and that was reflected in share prices during upon exit price and reinvestment of distributions. August, particularly for Industrial companies. However, towards the end of the quarter, the Australian and international markets became concerned about global political tensions – Ukraine, Iraq and Hong Kong – with a falling iron ore price having a significant negative impact on the Australian resources index. SIF Structure: by sector (look through) One of our major holdings is IRESS (IRE). SIF originally invested in IRE in 2002 when it had a market capitalisation of $260m. At the time we invested it was already the dominant provider of information systems to the professional equity market in Australia and New Zealand (ANZ). -

Stoxx® Pacific Total Market Index

STOXX® PACIFIC TOTAL MARKET INDEX Components1 Company Supersector Country Weight (%) CSL Ltd. Health Care AU 7.79 Commonwealth Bank of Australia Banks AU 7.24 BHP GROUP LTD. Basic Resources AU 6.14 Westpac Banking Corp. Banks AU 3.91 National Australia Bank Ltd. Banks AU 3.28 Australia & New Zealand Bankin Banks AU 3.17 Wesfarmers Ltd. Retail AU 2.91 WOOLWORTHS GROUP Retail AU 2.75 Macquarie Group Ltd. Financial Services AU 2.57 Transurban Group Industrial Goods & Services AU 2.47 Telstra Corp. Ltd. Telecommunications AU 2.26 Rio Tinto Ltd. Basic Resources AU 2.13 Goodman Group Real Estate AU 1.51 Fortescue Metals Group Ltd. Basic Resources AU 1.39 Newcrest Mining Ltd. Basic Resources AU 1.37 Woodside Petroleum Ltd. Oil & Gas AU 1.23 Coles Group Retail AU 1.19 Aristocrat Leisure Ltd. Travel & Leisure AU 1.02 Brambles Ltd. Industrial Goods & Services AU 1.01 ASX Ltd. Financial Services AU 0.99 FISHER & PAYKEL HLTHCR. Health Care NZ 0.92 AMCOR Industrial Goods & Services AU 0.91 A2 MILK Food & Beverage NZ 0.84 Insurance Australia Group Ltd. Insurance AU 0.82 Sonic Healthcare Ltd. Health Care AU 0.82 SYDNEY AIRPORT Industrial Goods & Services AU 0.81 AFTERPAY Financial Services AU 0.78 SUNCORP GROUP LTD. Insurance AU 0.71 QBE Insurance Group Ltd. Insurance AU 0.70 SCENTRE GROUP Real Estate AU 0.69 AUSTRALIAN PIPELINE Oil & Gas AU 0.68 Cochlear Ltd. Health Care AU 0.67 AGL Energy Ltd. Utilities AU 0.66 DEXUS Real Estate AU 0.66 Origin Energy Ltd. -

ESG Reporting by the ASX200

Australian Council of Superannuation Investors ESG Reporting by the ASX200 August 2019 ABOUT ACSI Established in 2001, the Australian Council of Superannuation Investors (ACSI) provides a strong, collective voice on environmental, social and governance (ESG) issues on behalf of our members. Our members include 38 Australian and international We undertake a year-round program of research, asset owners and institutional investors. Collectively, they engagement, advocacy and voting advice. These activities manage over $2.2 trillion in assets and own on average 10 provide a solid basis for our members to exercise their per cent of every ASX200 company. ownership rights. Our members believe that ESG risks and opportunities have We also offer additional consulting services a material impact on investment outcomes. As fiduciary including: ESG and related policy development; analysis investors, they have a responsibility to act to enhance the of service providers, fund managers and ESG data; and long-term value of the savings entrusted to them. disclosure advice. Through ACSI, our members collaborate to achieve genuine, measurable and permanent improvements in the ESG practices and performance of the companies they invest in. 6 INTERNATIONAL MEMBERS 32 AUSTRALIAN MEMBERS MANAGING $2.2 TRILLION IN ASSETS 2 ESG REPORTING BY THE ASX200: AUGUST 2019 FOREWORD We are currently operating in a low-trust environment Yet, safety data is material to our members. In 2018, 22 – for organisations generally but especially businesses. people from 13 ASX200 companies died in their workplaces. Transparency and accountability are crucial to rebuilding A majority of these involved contractors, suggesting that this trust deficit. workplace health and safety standards are not uniformly applied. -

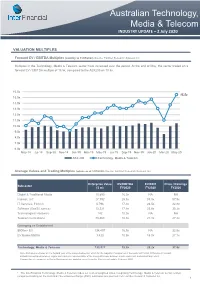

Australian Technology, Media & Telecom

Australian Technology, Media & Telecom INDUSTRY UPDATE – 2 July 2020 VALUATION MULTIPLES Forward EV / EBITDA Multiples (monthly to 31/05/2020) Source: FactSet Research Systems Inc. Multiples in the Technology, Media & Telecom sector have increased over the period. At the end of May, the sector traded on a forward EV / EBITDA multiple of 15.5x, compared to the ASX200 on 10.5x. 16.0x 15.5x 15.0x 14.0x 13.0x 12.0x 11.0x 10.0x 9.0x 8.0x 7.0x 6.0x May-18 Jul-18 Sep-18 Nov-18 Jan-19 Mar-19 May-19 Jul-19 Sep-19 Nov-19 Jan-20 Mar-20 May-20 ASX 200 Technology, Media & Telecom Average Values and Trading Multiples (values as at 1/07/2020) Source: FactSet Research Systems Inc. Enterprise Value EV/EBITDA EV/EBIT Price / Earnings Subsector ($ m) FY2020 FY2020 FY2020 Digital & Traditional Media 10,890 16.9x NA NA Internet, IoT 27,792 25.3x 33.3x 57.9x IT Services, Fintech 5,796 17.3x 24.5x 32.8x Software (SaaS/Licence) 13,221 17.9x 23.9x 35.2x Technological Hardware 142 10.0x NA NA Telecommunications 73,468 10.3x 21.1x 27.2x Emerging vs Established $500m+ EV 134,497 16.9x NA 32.9x EV Below $500m 1,420 10.9x 15.0x 27.7x Technology, Media & Telecom 135,917 15.5x 29.2x 31.8x Note: Multiples are based on the forward year of the unreported period, which for the majority of companies in the sector is FY2020. Difference in forward EV/EBITDA multiples between Figure and Table are representative of the timing difference between month-end result, and current day result. -

Pengana Emerging Companies Fund

QUARTERLY REVIEW PENGANA EMERGING COMPANIES FUND December 2018 Quarterly Review DECEMBER 2018 FUND PERFORMANCE Net performance for periods ending 31 December 20181 Since 1 mth 3 mths 1 yr 3 yrs p.a. 5 yrs p.a. 10 yrs p.a. Inception p.a.2 Pengana Emerging Companies Fund -6.2% -18.6% -9.9% 5.2% 9.4% 15.4% 12.6% S&P/ASX Small Ordinaries Index -4.2% -13.7% -8.7% 7.4% 5.6% 6.9% 4.0% Outperformance -2.0% -4.9% -1.2% -2.2% 3.8% 8.5% 8.6% S&P/ASX Small Industrials Index3 -3.9% -13.4% -6.5% 4.7% 6.3% 9.8% 4.9% Outperformance -2.3% -5.2% -3.4% 0.5% 3.1% 5.6% 7.7% FUND COMMENTARY The Fund fell 18.6%1 over the December quarter, underperforming the Small Industrials Index by 5.2% and the Small Ordinaries Index by 4.9%. For the 12 months to December, the Fund was down 9.9%1, underperforming the Small Industrials Index by 3.4% and the Small Ordinaries Index by 1.2%. The Australian share market had the worst close to a year since 2011, with the ASX 200 index closing the quarter 8.5% lower. Global markets generally fared worse with the S&P 500 in the US down 14.3%, the technology heavy US Nasdaq index down 17% and the Nikkei in Japan down over 17%. The nervousness largely centred around concerns over global economic growth pending a US-China trade war, rising US interest rates and sluggish economic growth from China. -

Annual Report Year Ended 30 June 2019

Annual Report Year Ended 30 June 2019 GENERAL Year in Review 4 Creating Value 6 Performance 8 Diversity Snapshot 12 Chair’s Review 14 Chief Executive Officer’s Review 15 Delivering Our Group Strategy 16 About SkyCity 24 Auckland 27 Hamilton 31 Adelaide 32 Queenstown 34 International Business 35 Our Risk Profile and Management 36 Our Board 40 Our Senior Leadership Team 44 SUSTAINABILITY Our Sustainability 48 Our Sustainability Pillars Our Customers 52 Our People 58 Our Communities 72 Our Suppliers 78 Our Environment 84 Independent Limited Assurance Statement 91 CORPORATE GOVERNANCE STATEMENT AND OTHER DISCLOSURES Corporate Governance Statement 92 Director and Employee Remuneration 104 Shareholder and Bondholder Information 118 Directors’ Disclosures 121 Company Disclosures 123 This annual report is dated 14 August 2019 and is signed on behalf of the Board of directors of SkyCity Entertainment Group Limited (SkyCity or the company and, together with its subsidiaries, the Group) by: FINANCIAL STATEMENTS Independent Auditor’s Report 127 Income Statement 134 Statement of Comprehensive Income 135 Rob Campbell Bruce Carter Balance Sheet 136 Chair Deputy Chair Statement of Changes in Equity 137 An electronic copy of this annual report is available in the Investor Centre section of the company’s Statement of Cash Flows 138 website at www.skycityentertainmentgroup.com Notes to the Financial Statements 139 Reconciliation of Normalised Results to Reported Results 174 GRI CONTENT INDEX 178 ABOUT THIS ANNUAL REPORT GLOSSARY 182 Unless otherwise stated, all dollar amounts in this annual report are expressed in New Zealand dollars. DIRECTORY 183 Where appropriate, information is also provided in relation to activities that have occurred after 30 June 2019, but prior to publication of this annual report. -

Metcash Limited ABN 32 112 073 480 1 Thomas Holt Drive Macquarie Park NSW 2113 Australia

Metcash Limited ABN 32 112 073 480 1 Thomas Holt Drive Macquarie Park NSW 2113 Australia 5 December 2019 Market Announcements Office Australian Securities Exchange Limited 20 Bridge Street Sydney NSW 2000 Dear Sir/Madam METCASH LIMITED – 2020 HALF YEAR RESULTS AND FINANCIAL REPORT In accordance with ASX Listing Rule 4.2A, please find attached the following documents for release to the market: a) ASX Announcement – Metcash Limited 2020 Half Year Results b) Appendix 4D and Financial Report (including the Directors’ Report and Independent Auditor’s Review Report) of Metcash Limited and its controlled entities for the half year ended 31 October 2019. Yours faithfully Julie Hutton Company Secretary Metcash Limited ABN 32 112 073 480 1 Thomas Holt Drive Macquarie Park NSW 2113 Australia 5 December 2019 ASX Announcement Metcash Limited 2020 Half Year Results • Group highlights: o Total Food pillar sales (including charge-through sales) increased 1.2%, with Supermarkets wholesale sales ex tobacco being positive1 for the first time since FY12 o Liquor delivered its sixth consecutive year of earnings growth o Our Trade-focused Hardware pillar continued to perform well despite difficult trading conditions o MFuture programs progressing across all pillars • Statutory results for 1H20 reflect adoption of the new Accounting Standard AASB16 Leases. Prior period comparatives have not been restated for the impact of AASB16. To enable comparison, the results for 1H20 have been adjusted, where appropriate, to exclude the impact of AASB16 • Group sales (including -

Appendix 4E (Rule 4.3A) for the Year Ended 30 June 2020

FINANCIAL REPORT– 30 JUNE 2020 Appendix 4E (Rule 4.3A) for the year ended 30 June 2020 Results for Announcement to the Market 2020 2019 Key Financial Information $’000 $’000 Continuing operations Revenue from ordinary activities, excluding specific items Up by 17% 2,172,021 1,854,676 (Loss)/Profit from ordinary activities after tax n/m (508,778) 216,566 Net profit after tax, excluding specific items Down by 17% 155,937 187,064 Discontinued operations (Loss)/Profit from ordinary activities after tax n/m (66,189) 17,314 Total income attributable to: Net (loss)/profit from ordinary activities after tax — owners of the parent n/m (590,033) 221,229 Net profit from ordinary activities after tax — non-controlling interest Up by 19% 15,066 12,651 n/m: not meaningful. Refer to the attached Financial Report, Results Announcement and Investor Presentation for management commentary on the results. Dividends An interim fully franked dividend of 5 cents per share was paid on 20 April 2020. Since the end of the financial year, the directors have determined that a fully franked dividend of 2 cents per share will be payable in October 2020 in respect of the year ended 30 June 2020. Dividend and AGM Dates Ex-dividend date: 9 September 2020 Record date: 10 September 2020 Payment date: 20 October 2020 Annual General Meeting date: 12 November 2020 Net Tangible Assets per Share 2020 2019 Reported cents cents Net tangible asset (deficit)/backing per ordinary share1 (39.0) (10.9) Net asset backing per ordinary share 110.6 162.6 1 If right-of-use assets are included then the net tangible assets backing per share is (25.8) cents (2019: N/A). -

Stoxx® Australia 150 Index

STOXX® AUSTRALIA 150 INDEX Components1 Company Supersector Country Weight (%) Commonwealth Bank of Australia Banks Australia 8.37 CSL Ltd. Health Care Australia 7.46 BHP GROUP LTD. Basic Resources Australia 7.23 National Australia Bank Ltd. Banks Australia 4.37 Westpac Banking Corp. Banks Australia 4.09 Australia & New Zealand Bankin Banks Australia 3.75 Wesfarmers Ltd. Retail Australia 3.30 WOOLWORTHS GROUP Personal Care, Drug & Grocery Australia 2.87 Macquarie Group Ltd. Financial Services Australia 2.84 Rio Tinto Ltd. Basic Resources Australia 2.48 Fortescue Metals Group Ltd. Basic Resources Australia 2.27 Transurban Group Industrial Goods & Services Australia 2.20 Telstra Corp. Ltd. Telecommunications Australia 2.05 Goodman Group Real Estate Australia 1.77 AFTERPAY Industrial Goods & Services Australia 1.54 Coles Group Personal Care, Drug & Grocery Australia 1.39 Woodside Petroleum Ltd. Energy Australia 1.28 Newcrest Mining Ltd. Basic Resources Australia 1.27 Aristocrat Leisure Ltd. Travel & Leisure Australia 1.11 XERO Technology Australia 1.00 SYDNEY AIRPORT Industrial Goods & Services Australia 0.93 Brambles Ltd. Industrial Goods & Services Australia 0.91 Sonic Healthcare Ltd. Health Care Australia 0.90 ASX Ltd. Financial Services Australia 0.82 SCENTRE GROUP Real Estate Australia 0.80 Cochlear Ltd. Health Care Australia 0.74 QBE Insurance Group Ltd. Insurance Australia 0.73 SUNCORP GROUP LTD. Insurance Australia 0.71 South32 Australia Basic Resources Australia 0.71 Santos Ltd. Energy Australia 0.68 Ramsay Health Care Ltd. Health Care Australia 0.66 Insurance Australia Group Ltd. Insurance Australia 0.65 Mirvac Group Real Estate Australia 0.60 DEXUS Real Estate Australia 0.59 SEEK Ltd. -

Global Equity Fund Description Plan 3S DCP & JRA MICROSOFT CORP

Global Equity Fund June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA MICROSOFT CORP 2.5289% 2.5289% APPLE INC 2.4756% 2.4756% AMAZON COM INC 1.9411% 1.9411% FACEBOOK CLASS A INC 0.9048% 0.9048% ALPHABET INC CLASS A 0.7033% 0.7033% ALPHABET INC CLASS C 0.6978% 0.6978% ALIBABA GROUP HOLDING ADR REPRESEN 0.6724% 0.6724% JOHNSON & JOHNSON 0.6151% 0.6151% TENCENT HOLDINGS LTD 0.6124% 0.6124% BERKSHIRE HATHAWAY INC CLASS B 0.5765% 0.5765% NESTLE SA 0.5428% 0.5428% VISA INC CLASS A 0.5408% 0.5408% PROCTER & GAMBLE 0.4838% 0.4838% JPMORGAN CHASE & CO 0.4730% 0.4730% UNITEDHEALTH GROUP INC 0.4619% 0.4619% ISHARES RUSSELL 3000 ETF 0.4525% 0.4525% HOME DEPOT INC 0.4463% 0.4463% TAIWAN SEMICONDUCTOR MANUFACTURING 0.4337% 0.4337% MASTERCARD INC CLASS A 0.4325% 0.4325% INTEL CORPORATION CORP 0.4207% 0.4207% SHORT-TERM INVESTMENT FUND 0.4158% 0.4158% ROCHE HOLDING PAR AG 0.4017% 0.4017% VERIZON COMMUNICATIONS INC 0.3792% 0.3792% NVIDIA CORP 0.3721% 0.3721% AT&T INC 0.3583% 0.3583% SAMSUNG ELECTRONICS LTD 0.3483% 0.3483% ADOBE INC 0.3473% 0.3473% PAYPAL HOLDINGS INC 0.3395% 0.3395% WALT DISNEY 0.3342% 0.3342% CISCO SYSTEMS INC 0.3283% 0.3283% MERCK & CO INC 0.3242% 0.3242% NETFLIX INC 0.3213% 0.3213% EXXON MOBIL CORP 0.3138% 0.3138% NOVARTIS AG 0.3084% 0.3084% BANK OF AMERICA CORP 0.3046% 0.3046% PEPSICO INC 0.3036% 0.3036% PFIZER INC 0.3020% 0.3020% COMCAST CORP CLASS A 0.2929% 0.2929% COCA-COLA 0.2872% 0.2872% ABBVIE INC 0.2870% 0.2870% CHEVRON CORP 0.2767% 0.2767% WALMART INC 0.2767%