June 2019 42

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

June 2011 Yearly Report

Alleron Investment Management Limited Yearly Report June 2011 Portfolio performance and attribution analysis Market commentary Portfolio commentary Since Inception (Annualised) Year to Date Global markets were lead, over Positives: financial year, by the strong per- CEU: The company’s revenue such Portfolio +10.297% +4.468% formance of the US market which that cash flow now funds their dis- Benchmark + 6.158% +11.503% responded strongly to Federal Re- tribution and reduces their risk pro- serve Bank policy of a second round file. Top 3 and bottom 3 performing stocks of quantitative easing. This along AXA: The stock price was sup- Top 3: ConnectEast Group (CEU), AXA Asia Pacific Holdings with continued government spend- (AXA), Oil Search (OSH). ported by the accepted takeover ing allowed the US economy and offer from AMP and AXA SA. company earnings to maintain Bottom 3: Seven West Media Limited (SWM), Resmed Inc. (RMD), growth into the beginning of 2011. OSH: The company has secured Computershare (CPU). While growth in the US continued, offtake agreements to their LNG European countries were besieged output which remains on schedule. Portfolio changes by the familiar problem of periph- Negatives: Stocks joined or increased significantly: eral nation debt and increased risks of sovereign debt default. Contrar- SWM: Company earnings were hurt Downer Limited (+2.25% New Stock): An Engineering and Contract- ily, strong activity in emerging by weak advertising activity from ing company. The company has developed a strong order book pro- economies has forced monetary uncertainly over the resource tax. viding significant growth potential and has cleared the way to success- authorities there to tighten policy to RMD: Earnings translation was hurt fully complete troubled contracts. -

Monthly NTA and Performance Update

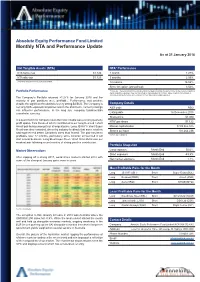

Absolute Equity Performance Fund Limited Monthly NTA and Performance Update As at 31 January 2018 Net Tangible Assets (NTA) NTA* Performance NTA before tax $1.122 1 month 1.27% NTA after tax $1.123 3 months 2.59% $ currency notation refers to Australian Dollars. 12 months 16.02% Since inception (annualised) 3.52% Portfolio Performance *Before tax. These calculations are unaudited and intended to illustrate the performance of the investment portfolio minus corporate expenses. They are calculated on a pre-dividend NTA basis. ‘Since inception (annualised)’ is annualised NTA performance since listing at $1.065 after listing related expenses The Company’s Portfolio returned +1.27% for January 2018 and the majority of pair positions were profitable. Performance was positive despite the significant headwind of a very strong $A/$US. The Company is Company Details net long $US-exposed companies and in the short term, currency swings ASX code AEG can influence performance. In the long run, company fundamentals overwhelm currency. Listing date 16 December 2015 Share price $1.080 In a quiet month for company news the most notable was a strong quarterly NTA* per share $1.122 profit update from Resmed which contributed to our long Resmed / short Ansell pair being amongst our strongest pairs. Long JB Hi-Fi / short Super Market capitalisation $109,365,375 Retail was also rewarded, driven by industry feedback that some retailers Shares on Issue 101,264,236 had experienced better Christmas sales than feared. The pair has been profitable over 12 months, particularly since Amazon announced it will *Before tax ex-dividend start a local business. -

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

Australian Investment Strategy

2 November 2016 Asia Pacific/Australia Equity Research Investment Strategy Australian Investment Strategy Research Analysts STRATEGY Hasan Tevfik ,CFA 61 2 8205 4284 [email protected] Aussie darlings Peter Liu 61 2 8205 4071 ■ Aussies love their darlings: Australia currently has the most expensive [email protected] equity market "Darlings" in the world. Our darlings trade on a forward P/E Damien Boey of 38x. The other commodity-focused market, Canada, has the second 61 2 8205 4615 [email protected] most expensive darlings. Darlings in Australia have been more expensive only during the Nasdaq bubble when they touched 45x. ■ Darling derating: Buying Australian darlings at these valuations has been a poor strategy in the past. Also, the current high valuation for Australia's darlings suggest they are especially vulnerable to rising bond yields and the coming end of the Australian profits recession. A rising discount rate and a lower premium for growth suggest investors should focus on stocks that could be future darlings. ■ Hello Daaarling: Future market darlings have shared many similar characteristics over the last 20 years. They are generally well managed, have strong balance sheets and operate on high margins. Our "Hello Daaarling" strategy highlights potential future darlings and they currently trade on just 17x P/E and include Caltex, Eclipx, Mayne Pharma, Nufarm, Star Entertainment and South 32. We add Eclipx to our long Portfolio. Figure 1: Australia has the most expensive darlings in the world Median 12-month forward P/E of "market darlings" around the world* 40 35 30 25 20 15 10 Australia Canada Cont. -

Asx Clear – Acceptable Collateral List 28

et6 ASX CLEAR – ACCEPTABLE COLLATERAL LIST Effective from 20 September 2021 APPROVED SECURITIES AND COVER Subject to approval and on such conditions as ASX Clear may determine from time to time, the following may be provided in respect of margin: Cover provided in Instrument Approved Cover Valuation Haircut respect of Initial Margin Cash Cover AUD Cash N/A Additional Initial Margin Specific Cover N/A Cash S&P/ASX 200 Securities Tiered Initial Margin Equities ETFs Tiered Notes to the table . All securities in the table are classified as Unrestricted (accepted as general Collateral and specific cover); . Specific cover only securities are not included in the table. Any securities is acceptable as specific cover, with the exception of ASX securities as well as Participant issued or Parent/associated entity issued securities lodged against a House Account; . Haircut refers to the percentage discount applied to the market value of securities during collateral valuation. ASX Code Security Name Haircut A2M The A2 Milk Company Limited 30% AAA Betashares Australian High Interest Cash ETF 15% ABC Adelaide Brighton Ltd 30% ABP Abacus Property Group 30% AGL AGL Energy Limited 20% AIA Auckland International Airport Limited 30% ALD Ampol Limited 30% ALL Aristocrat Leisure Ltd 30% ALQ ALS Limited 30% ALU Altium Limited 30% ALX Atlas Arteria Limited 30% AMC Amcor Ltd 15% AMP AMP Ltd 20% ANN Ansell Ltd 30% ANZ Australia & New Zealand Banking Group Ltd 20% © 2021 ASX Limited ABN 98 008 624 691 1/7 ASX Code Security Name Haircut APA APA Group 15% APE AP -

Annual Report 2017

17ANNUAL REPORT 2017 p p p p p p 02 04 07 08 32 50 About Us Highlights Chairman’s CEO’s Year Sustainability, Directors’ Introduction In Review Community + + Remuneration People Reports Operating + Financial Review 20 Consolidated Financial Statements 78 Annual General Meeting Group Strategy 22 Executive Team 44 The 54th Annual General Meeting of the Company will be held at 11am on 26 October Group and Divisional Results 24 Directors’ Profiles 48 2017 at the Blackmores Campus, 20 Jubilee Avenue, Warriewood NSW 2102. Financial Review 26 Auditor’s Independence Declaration 72 Cover image: Fiona Yeo, Assistant Marketing Operating Review 28 Independent Auditor’s Report 73 Manger, Export Sales. Fiona is profiled in this Group Risks 30 Directors’ Declaration 77 report on page 42. Additional Information 118 Company Information 119 OUR ANNUAL REPORT 2017 BLACKMORES ANNUAL REPORT 2017 REPORT ANNUAL BLACKMORES OUR OUR #4 STRATEGIC VALUES PURPOSE PRIORITIES Blackmores’ values are at Blackmores improves Blackmores is committed the heart of our business. people’s lives by delivering to superior business These values, known as the world’s best natural performance. Our strategic PIRLS, are both behavioural health solutions. We direction is focused on and aspirational. They achieve this by translating delivering growth and underpin our work practices our unrivalled heritage and continuous improvement to and are supported by legal knowledge into innovative, maintain Blackmores’ leading policies and procedures. quality branded healthcare position in the industry and solutions that work. to achieve ongoing success Passion for Natural Health for our company, our people Integrity and our shareholders. Respect Leadership #1 Consumer Centricity Social Responsibility #2 Asia Growth #3 Product Leadership #4 Operational Effectiveness THE 2017 ANNUAL REPORT OF BLACKMORES LIMITED PROVIDES INFORMATION ON THE ORGANISATION AND COMPANY PERFORMANCE FOR THE YEAR 1 JULY 2016 TO 30 JUNE 2017. -

Smallco Investment Fund

Smallco Investment Fund Quarterly Update 30 September 2014 SIF Portfolio Commentary SIF Performance Smallco Investment Fund (SIF) delivered 6.8% during the Return to 30 September 2014 September quarter and for the 12 months was up a solid 12.3%. During the quarter Iress, Isentia Group and Sirtex 3 months 6.8% Medical performed positively, while Carsales.com, Ozforex 1 year 12.3% Group and Macquarie Atlas Roads were negative 3 year p.a. 36.4% contributors. 5 year p.a. 22.5% For the September quarter the Small Ordinaries index was 10 year p.a. 13.6% modestly positive at 1.5% while for the year to 30 Since inception (31.10.00) p.a. 14.2% September it was down -0.1%. Value of $100,000 invested at inception $631,173 In general the Australian market had a solid reporting Fund returns calculated after all fees and expenses and based season and that was reflected in share prices during upon exit price and reinvestment of distributions. August, particularly for Industrial companies. However, towards the end of the quarter, the Australian and international markets became concerned about global political tensions – Ukraine, Iraq and Hong Kong – with a falling iron ore price having a significant negative impact on the Australian resources index. SIF Structure: by sector (look through) One of our major holdings is IRESS (IRE). SIF originally invested in IRE in 2002 when it had a market capitalisation of $260m. At the time we invested it was already the dominant provider of information systems to the professional equity market in Australia and New Zealand (ANZ). -

(ASX100) Women on Boards Analysis

Australia/NZ | Australia Thematic Investing (Citi) Equities 18 August 2011 │ 32 pages ESG: ASX100 Women on Board Analysis Increasing Focus on Board Diversity Women on Boards of ASX100 Companies — The ASX Corporate Governance Council’s new principles and recommendations on diversity commenced on 1 January Elaine Prior 2011. This is likely to lead to increasing focus on companies’ approaches to diversity +61-2-8225-4891 issues, including female representation on company boards. This report looks at data [email protected] on women directors on ASX100 company boards. The number of women directors has Felipe Faria increased, particularly in recent months (Figure 5 to Figure 8). Board diversity may [email protected] enhance effectiveness, by providing a wider range of perspectives and knowledge. Women on Boards Data — We collected and analysed data on female board directors of S&P/ASX100 companies from FY08 to 8 August 2011 (Figure 5 to Figure 9). At 8 August 2011 there were 134 women on ASX100 boards, a 46% increase from FY08. ASX100 companies with no female board directors were AQP, CQO, EGP, FMG, IPL, JHX, LEI, LYC, OSH, PDN, PRY, RHC, RMD, SGM and SWM. Companies with three female directors (the highest number identified) are AMP, BEN, CBA, MQG, QAN, QBE and WBC. Seven female directors each currently hold three ASX100 directorships. Business Case for Gender Diversity — Reibey Institute research found that those ASX500 companies with women directors on 30 June 2010 had a 3-year return on equity (ROE) 10.7% higher than those without any women directors. The 5-year ROE was 11.1% higher. -

Stoxx® Pacific Total Market Index

STOXX® PACIFIC TOTAL MARKET INDEX Components1 Company Supersector Country Weight (%) CSL Ltd. Health Care AU 7.79 Commonwealth Bank of Australia Banks AU 7.24 BHP GROUP LTD. Basic Resources AU 6.14 Westpac Banking Corp. Banks AU 3.91 National Australia Bank Ltd. Banks AU 3.28 Australia & New Zealand Bankin Banks AU 3.17 Wesfarmers Ltd. Retail AU 2.91 WOOLWORTHS GROUP Retail AU 2.75 Macquarie Group Ltd. Financial Services AU 2.57 Transurban Group Industrial Goods & Services AU 2.47 Telstra Corp. Ltd. Telecommunications AU 2.26 Rio Tinto Ltd. Basic Resources AU 2.13 Goodman Group Real Estate AU 1.51 Fortescue Metals Group Ltd. Basic Resources AU 1.39 Newcrest Mining Ltd. Basic Resources AU 1.37 Woodside Petroleum Ltd. Oil & Gas AU 1.23 Coles Group Retail AU 1.19 Aristocrat Leisure Ltd. Travel & Leisure AU 1.02 Brambles Ltd. Industrial Goods & Services AU 1.01 ASX Ltd. Financial Services AU 0.99 FISHER & PAYKEL HLTHCR. Health Care NZ 0.92 AMCOR Industrial Goods & Services AU 0.91 A2 MILK Food & Beverage NZ 0.84 Insurance Australia Group Ltd. Insurance AU 0.82 Sonic Healthcare Ltd. Health Care AU 0.82 SYDNEY AIRPORT Industrial Goods & Services AU 0.81 AFTERPAY Financial Services AU 0.78 SUNCORP GROUP LTD. Insurance AU 0.71 QBE Insurance Group Ltd. Insurance AU 0.70 SCENTRE GROUP Real Estate AU 0.69 AUSTRALIAN PIPELINE Oil & Gas AU 0.68 Cochlear Ltd. Health Care AU 0.67 AGL Energy Ltd. Utilities AU 0.66 DEXUS Real Estate AU 0.66 Origin Energy Ltd. -

ESG Reporting by the ASX200

Australian Council of Superannuation Investors ESG Reporting by the ASX200 August 2019 ABOUT ACSI Established in 2001, the Australian Council of Superannuation Investors (ACSI) provides a strong, collective voice on environmental, social and governance (ESG) issues on behalf of our members. Our members include 38 Australian and international We undertake a year-round program of research, asset owners and institutional investors. Collectively, they engagement, advocacy and voting advice. These activities manage over $2.2 trillion in assets and own on average 10 provide a solid basis for our members to exercise their per cent of every ASX200 company. ownership rights. Our members believe that ESG risks and opportunities have We also offer additional consulting services a material impact on investment outcomes. As fiduciary including: ESG and related policy development; analysis investors, they have a responsibility to act to enhance the of service providers, fund managers and ESG data; and long-term value of the savings entrusted to them. disclosure advice. Through ACSI, our members collaborate to achieve genuine, measurable and permanent improvements in the ESG practices and performance of the companies they invest in. 6 INTERNATIONAL MEMBERS 32 AUSTRALIAN MEMBERS MANAGING $2.2 TRILLION IN ASSETS 2 ESG REPORTING BY THE ASX200: AUGUST 2019 FOREWORD We are currently operating in a low-trust environment Yet, safety data is material to our members. In 2018, 22 – for organisations generally but especially businesses. people from 13 ASX200 companies died in their workplaces. Transparency and accountability are crucial to rebuilding A majority of these involved contractors, suggesting that this trust deficit. workplace health and safety standards are not uniformly applied. -

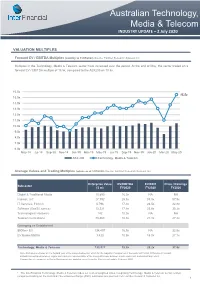

Australian Technology, Media & Telecom

Australian Technology, Media & Telecom INDUSTRY UPDATE – 2 July 2020 VALUATION MULTIPLES Forward EV / EBITDA Multiples (monthly to 31/05/2020) Source: FactSet Research Systems Inc. Multiples in the Technology, Media & Telecom sector have increased over the period. At the end of May, the sector traded on a forward EV / EBITDA multiple of 15.5x, compared to the ASX200 on 10.5x. 16.0x 15.5x 15.0x 14.0x 13.0x 12.0x 11.0x 10.0x 9.0x 8.0x 7.0x 6.0x May-18 Jul-18 Sep-18 Nov-18 Jan-19 Mar-19 May-19 Jul-19 Sep-19 Nov-19 Jan-20 Mar-20 May-20 ASX 200 Technology, Media & Telecom Average Values and Trading Multiples (values as at 1/07/2020) Source: FactSet Research Systems Inc. Enterprise Value EV/EBITDA EV/EBIT Price / Earnings Subsector ($ m) FY2020 FY2020 FY2020 Digital & Traditional Media 10,890 16.9x NA NA Internet, IoT 27,792 25.3x 33.3x 57.9x IT Services, Fintech 5,796 17.3x 24.5x 32.8x Software (SaaS/Licence) 13,221 17.9x 23.9x 35.2x Technological Hardware 142 10.0x NA NA Telecommunications 73,468 10.3x 21.1x 27.2x Emerging vs Established $500m+ EV 134,497 16.9x NA 32.9x EV Below $500m 1,420 10.9x 15.0x 27.7x Technology, Media & Telecom 135,917 15.5x 29.2x 31.8x Note: Multiples are based on the forward year of the unreported period, which for the majority of companies in the sector is FY2020. Difference in forward EV/EBITDA multiples between Figure and Table are representative of the timing difference between month-end result, and current day result. -

For Personal Use Only Use Personal For

The Leading Edge In this edition of the Leading Edge we consider opportunities to invest in healthcare, one of the few growth sectors in the Australian share market QUARTERLY REPORT | December 2013 For personal use only Watermark Funds Management Level 5, 139 Macquarie Street NSW Sydney 2000 TEL (02) 9252 0225 FAX (02) 9252 1220 [email protected] www.wfunds.com.au This report has been prepared by Watermark Funds Management Pty Limited. This report is for distribution only under such circumstances as may be permitted by applicable law. It has no regard to the specific investment objectives, financial situation or particular needs of any specific recipient. It is published solely for informational purposes and is not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained For personal use only herein nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in the report. The report should not be regarded by recipients as a substitute for the exercise of their own judgement. Any opinions expressed in this report are subject to change without notice. The analysis contained herein is based on numerous assumptions. Different assumptions could result in materially different results. Watermark Funds Management Pty Limited is under no obligation to update or keep current the information contained herein. Past performance is not necessarily a guide to future performance.