(ASX100) Women on Boards Analysis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

U Ethical Australian Equities Trust

Quarterly u ethical Australian Equities Performance Trust - Retail Review Quarterly highlights June 2021 • The Australian equity market performed Fund information strongly over the quarter buoyed by solid economic data and positive earnings revisions Inception date 7 July 2003 • The total return for the Trust over the quarter Fund size $91.35 million was 8.0 per cent, slightly below the benchmark Over the last 12 months the Trust has delivered Benchmark S&P/ASX 300 a strong total return of 25.9 per cent Accumulation Index • Sector allocation was a small drag, although Buy/sell spread1 0.25%/0.25%1 security selection was positive with top Management costs Estimated up to 1.315% p.a. performing stocks including ResMed, See Product Disclosure Statement Cleanaway Waste Management and REA Group • Recent lockdowns highlight the ongoing Portfolio manager Jon Fernie Covid-19 risks. Rising inflation and elevated Number of stocks 20-40 valuations relative to historic levels also remain concerns Growth of $1,000 invested† Investment objective The U Ethical Australian Equities Trust has been 3,000 U Ethical AET Benchmark developed for the long-term investor and aims to 2,500 outperform the benchmark after fees over rolling 5-year periods. It invests primarily in Australian 2,000 shares as well as up to 10 per cent in fixed interest and cash. 1,500 1,000 500 0 2006 2008 2010 2012 2014 2016 2018 2020 2022 Performance 3 months 6 months 1 year 3 years 5 years 10 years Since inception % % % p.a. % % p.a. % p.a. % p.a. -

Goodman Plus Trust Annual Report 2011 Cover: 82,015 Sqm Distribution Centre Under Development for Metcash at Bungarribee Industrial Estate

Goodman Plus Trust Annual Report 2011 Cover: 82,015 sqm distribution centre under development for Metcash at Bungarribee Industrial Estate. Goodman Annual 1 PLUS Trust Report 2011 Goodman PLUS Trust Annual Report 2011 Contents Corporate governance 2 Summary of terms of redemption and exchange of Goodman PLUS 12 Financial report 15 Independent auditor’s report 32 Securities information 33 Definitions 35 Corporate directory 39 2 Corporate governance Corporate governance is the framework of rules, systems and processes by which authority is exercised within Goodman and accountability placed. It influences how the objectives of Goodman PLUS Trust (Trust) are set and achieved, how risk is monitored and assessed and how performance is optimised. The Trust recognises that an effective corporate governance culture is critical to success. We have designed and implemented a substantial range of governance initiatives, described in detail below, and we believe that our corporate governance systems are robust and effective. We recognise corporate governance is not static and systems will need to evolve over time to meet the demands of a changing market and corporate circumstances. At all times, we strive to achieve governance outcomes which balance the needs or requirements of the Trust, its stakeholders, regulators and the market. The corporate governance statement below outlines the ways in which the Trust has met the Australian Securities Exchange (ASX) Corporate Governance Council’s Corporate Governance Principles and Recommendations (2nd Edition). Any departures to implementation of the ASX Corporate Governance Council’s Corporate Governance Principles and Recommendations are described in the corporate governance statement below. As a result of the Trust not having employees of its own, and as a result of the limited business activities of the Trust, some of the ASX Corporate Governance Council’s recommendations are undertaken by Goodman Group (Goodman) rather than the Trust, as set out below. -

The State of the Deal and Deloitte Queensland Index

The State of the Deal and Deloitte Queensland Index March 2021 – Queensland Index Exceeds $100 billion THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion Contents Executive Summary 1 Then & Now – Investment Landscape 3 Then & Now – Deloitte Queensland Index 4 Queensland Economic Update 7 The Deloitte Queensland Index Q1 2021 8 Contacts 11 Sources 12 ii THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion Executive Summary Following the significant rebound in the second half of 2020, companies in the Deloitte Queensland Index exceeded $100 billion at 31 March 2021, the highest month end market capitalisation on record for the State. Deloitte Queensland Index S&P/ASX All Ordinaries Companies in the Deloitte return in Q1 2021 return in Q1 2021 Queensland Index 3.5% 2.4% 169 at 31 March 2021 10.6% in Q4 2020 14.0% in Q4 2020 173 at 31 December 2020 90 companies increased Market capitalisation as at Mar-21 market capitalisation (53%) 66 companies decreased market $101.6b capitalisation (39%) 12 no movement (7%) $97.2b as at Dec-20 $18.5b as at Sep-02 5 delistings 1 listing (1%) Announced QLD M&A Disclosed value of announced transactions in Q1 2021 QLD M&A transactions in Q1 2021 64 $1.9b 92 in Q4 2020 $3.3b in Q4 2020 1 THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion The Deloitte Queensland Index increased by 3.5% in Q1 2021 Queensland M&A more broadly remains strong with with total market capitalisation increasing to $101.6b at 64 transactions announced in Q1 2021 including: Mar-21, the highest month end value on record for the State. -

Lynas Corporation Limited

Lynas Corporation Limited Stock Exchange Listing ASX: LYC Company profile Lynas Corporation owns the richest known deposit of Rare Earths, also known as Lanthanides, in the world at Mount Weld, near Laverton in Western Australia. This deposit underpins Lynas’ strategy to create a reliable, fully integrated source of Rare Earths supply from the mine through to customers in the global Rare Earths industry. Lynas has received all environmental approvals and commenced construction of a Concentration Plant at Mount Weld and an Advanced Materials Plant to process the Mount Weld concentrate through to final Rare Earths oxides in the Gebeng Industrial Estate, Kuantan, Pahang, Malaysia. The Company plans to become the benchmark for security of supply and a world leader in quality and environmental responsibility to an international customer base. ‘Rare Earths” is the term given to fifteen metallic elements known as the lanthanide series, plus yttrium. They play a key role in green environmental products, from energy efficient compact fluorescent light bulbs (CFLs) to hybrid cars, automotive catalytic converters and wind turbine generators. They are also essential in the development and manufacturing of many modern technological products, from hard disc drives to flat panel displays, iPods and magnetic resonance imaging (MRI) scans. Click here to access the company's 2009 Annual Report (PDF 2.4MB) Recent Developments Recent developments include: • Capital raising of approximately $450 million fully funded to phase, through a 1-for-1 non-renounceable -

June 2011 Yearly Report

Alleron Investment Management Limited Yearly Report June 2011 Portfolio performance and attribution analysis Market commentary Portfolio commentary Since Inception (Annualised) Year to Date Global markets were lead, over Positives: financial year, by the strong per- CEU: The company’s revenue such Portfolio +10.297% +4.468% formance of the US market which that cash flow now funds their dis- Benchmark + 6.158% +11.503% responded strongly to Federal Re- tribution and reduces their risk pro- serve Bank policy of a second round file. Top 3 and bottom 3 performing stocks of quantitative easing. This along AXA: The stock price was sup- Top 3: ConnectEast Group (CEU), AXA Asia Pacific Holdings with continued government spend- (AXA), Oil Search (OSH). ported by the accepted takeover ing allowed the US economy and offer from AMP and AXA SA. company earnings to maintain Bottom 3: Seven West Media Limited (SWM), Resmed Inc. (RMD), growth into the beginning of 2011. OSH: The company has secured Computershare (CPU). While growth in the US continued, offtake agreements to their LNG European countries were besieged output which remains on schedule. Portfolio changes by the familiar problem of periph- Negatives: Stocks joined or increased significantly: eral nation debt and increased risks of sovereign debt default. Contrar- SWM: Company earnings were hurt Downer Limited (+2.25% New Stock): An Engineering and Contract- ily, strong activity in emerging by weak advertising activity from ing company. The company has developed a strong order book pro- economies has forced monetary uncertainly over the resource tax. viding significant growth potential and has cleared the way to success- authorities there to tighten policy to RMD: Earnings translation was hurt fully complete troubled contracts. -

Schroder Australian Equity Fund Performance Overview

2021 August Schroder Australian Equity Fund Performance overview The S&P / ASX 200 Accumulation Index rose by 2.5%, while the Schroder Wholesale Australian Equity Fund rose by 2.4% (post-fee), underperforming by 0.1% (post-fee) over August 2021. During the month, the Fund added value through stock selection; however, sector allocation proved costly for relative returns. The overweight positions in the Materials and underweight to Financials added value. Conversely, the underweight positions in the Information Technology, Health Care and Consumer Discretionary detracted from relative returns. At a stock level, overweight positions in Alumina, James Hardie, and Vicinity Centres added value. The Nil holdings in Fortescue Metals and Woodside Petroleum, along with the underweight position in BHP Group were also among the best performing stocks. Detracting from performance were the nil holdings in Afterpay, Wisetech Global, Domino’s Pizza and Aristocrat Leisure. The underweight position in CSL and the overweight Rio Tinto were also among the top detractors. Market Summary Only a cursory amount of common sense seems necessary in questioning the connection between a domestic economy which is largely locked down, a global economy still struggling mightily with a pandemic, and booming equity and real estate markets nearly everywhere. Rampant bull market conditions such as those prevailing currently often seem to render discussions on company profits and valuation superfluous. Perceptions of value become determined by the share price or the house price and are rationalised by comparisons to similar egregiously priced companies or houses. There are a thousand great charts around at present put together by sensible people demonstrating the extreme nature of current market conditions. -

Monthly NTA and Performance Update

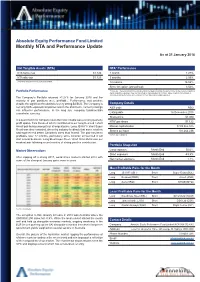

Absolute Equity Performance Fund Limited Monthly NTA and Performance Update As at 31 January 2018 Net Tangible Assets (NTA) NTA* Performance NTA before tax $1.122 1 month 1.27% NTA after tax $1.123 3 months 2.59% $ currency notation refers to Australian Dollars. 12 months 16.02% Since inception (annualised) 3.52% Portfolio Performance *Before tax. These calculations are unaudited and intended to illustrate the performance of the investment portfolio minus corporate expenses. They are calculated on a pre-dividend NTA basis. ‘Since inception (annualised)’ is annualised NTA performance since listing at $1.065 after listing related expenses The Company’s Portfolio returned +1.27% for January 2018 and the majority of pair positions were profitable. Performance was positive despite the significant headwind of a very strong $A/$US. The Company is Company Details net long $US-exposed companies and in the short term, currency swings ASX code AEG can influence performance. In the long run, company fundamentals overwhelm currency. Listing date 16 December 2015 Share price $1.080 In a quiet month for company news the most notable was a strong quarterly NTA* per share $1.122 profit update from Resmed which contributed to our long Resmed / short Ansell pair being amongst our strongest pairs. Long JB Hi-Fi / short Super Market capitalisation $109,365,375 Retail was also rewarded, driven by industry feedback that some retailers Shares on Issue 101,264,236 had experienced better Christmas sales than feared. The pair has been profitable over 12 months, particularly since Amazon announced it will *Before tax ex-dividend start a local business. -

June 2019 42

y 4 6 Equit 2019 June High Conviction High Quarterly NewsletterQuarterly No. Selector Fund In this quarterly edition, we review performance and attribution for the quarter. We highlight the importance of innovation and culture within organisations and profile ResMed and Cochlear, two leading healthcare businesses. We visit Fisher & Paykel Healthcare in New Zealand and look at one of the biggest growth industries in the world today, cyber security. Photo. Selector analyst trekking through the Atlas Mountains and local Berber kids. Selector Funds Management Limited ACN 102756347 AFSL 225316 Level 8, 10 Bridge Street Sydney NSW 2000 Australia Tel 612 8090 3612 www.selectorfund.com.au P Selector is a boutique fund manager. Our team, combined, have over 150 years of experience in financial markets. We believe in long-term wealth creation and building lasting relationships with our investors. We focus on stock selection, the funds are high conviction, concentrated and index unaware. As a result, the portfolios have low turnover and produce tax effective returns. Selector has a 15-year track record of outperformance and we continue to seek businesses with leadership qualities, run by competent management teams, underpinned by strong balance sheets and with a focus on capital management. Selector High Conviction Equity Fund Quarterly Newsletter #64 CONTENTS IN BRIEF – JUNE QUARTER 3 PORTFOLIO OVERVIEW 5 PORTFOLIO CONTRIBUTORS 7 MARKET INSIGHTS AND OBSERVATIONS 13 INNOVATION + CULTURE = SUCCESS 17 RESMED INC. 20 WAKE-UP CALL 31 FISHER & PAYKEL HEALTHCARE – JUNE 2019 42 RISK OUT…UPFRONT 45 COMPANY VISIT DIARY – JUNE 2019 QUARTER 57 2 Selector Funds Management IN BRIEF – JUNE QUARTER Dear Investor, Looking back on 2019, it would be fair to say that few identify the businesses we want to own on a case by case foresaw how the events of the financial year would basis, understand them to the best of our abilities and unfold. -

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

JMAD Media Ownership Report

JMAD New Zealand Media Ownership Report 2014 Published: 2014 December 5 Author: Merja Myllylahti This New Zealand Ownership Report 2014 is the fourth published by AUT’s Centre for Journalism, Media and Democracy (JMAD). The report finds that the New Zealand media market has failed to produce new, innovative media outlets, and that all the efforts to establish non-profit outlets have proved unsustainable. The report confirms the general findings of previous reports that New Zealand media space has remained highly commercial. It also confirms the financialisation of media ownership in the form of banks and fund managers. The report also observes that in 2014 convergence between New Zealand mass media and the communications sector generally was in full swing. Companies, such as Spark (former Telecom NZ), started to compete head-to-head with the traditional broadcasters on the online on-demand video and television markets. The American online video subscription service Netflix is entering the NZ market in March 2015. Additionally, the report notes evidence of uncomfortable alliances between citizen media, politicians, PR companies and legacy media. As Nicky Hager’s Dirty Politics book revealed, the National Party and PR practitioners used the Whale Oil blog to drive their own agendas. Also, events related to Maori TV, TVNZ and Scoop raise questions about political interference in media affairs. It is now evident that the boundaries between mainstream media, bloggers, public relations practitioners and politicians are blurring. Key events and trends concerning New Zealand media Financialisation of mass media ownership confirmed Substantial changes in Fairfax, APN and MediaWorks ownership Competition heats up in online television and video markets Turbulence at Maori TV Blurred lines among politicians, bloggers, journalists and PR practitioners The JMAD New Zealand media ownership reports are available here: http://www.aut.ac.nz/study- at-aut/study-areas/communications/media-networks/journalism,-media-and-democracy-research- centre/journalists-and-projects 1 1. -

Westpac Online Investment Loan Acceptable Securities List - Effective 3 September2021

Westpac Online Investment Loan Acceptable Securities List - Effective 3 September2021 ASX listed securities ASX Code Security Name LVR ASX Code Security Name LVR A2M The a2 Milk Company Limited 50% CIN Carlton Investments Limited 60% ABC Adelaide Brighton Limited 60% CIP Centuria Industrial REIT 50% ABP Abacus Property Group 60% CKF Collins Foods Limited 50% ADI APN Industria REIT 40% CL1 Class Limited 45% AEF Australian Ethical Investment Limited 40% CLW Charter Hall Long Wale Reit 60% AFG Australian Finance Group Limited 40% CMW Cromwell Group 60% AFI Australian Foundation Investment Co. Ltd 75% CNI Centuria Capital Group 50% AGG AngloGold Ashanti Limited 50% CNU Chorus Limited 60% AGL AGL Energy Limited 75% COF Centuria Office REIT 50% AIA Auckland International Airport Limited 60% COH Cochlear Limited 65% ALD Ampol Limited 70% COL Coles Group Limited 75% ALI Argo Global Listed Infrastructure Limited 60% CPU Computershare Limited 70% ALL Aristocrat Leisure Limited 60% CQE Charter Hall Education Trust 50% ALQ Als Limited 65% CQR Charter Hall Retail Reit 60% ALU Altium Limited 50% CSL CSL Limited 75% ALX Atlas Arteria 60% CSR CSR Limited 60% AMC Amcor Limited 75% CTD Corporate Travel Management Limited ** 40% AMH Amcil Limited 50% CUV Clinuvel Pharmaceuticals Limited 40% AMI Aurelia Metals Limited 35% CWN Crown Limited 60% AMP AMP Limited 60% CWNHB Crown Resorts Ltd Subordinated Notes II 60% AMPPA AMP Limited Cap Note Deferred Settlement 60% CWP Cedar Woods Properties Limited 45% AMPPB AMP Limited Capital Notes 2 60% CWY Cleanaway Waste -

16 August 2021 Company Announcements Office Australian

16 August 2021 Company Announcements Office Australian Securities Exchange Limited 20 Bridge Street SYDNEY NSW 2000 2021 FULL YEAR RESULTS – ANNUAL REPORT Seven West Media Limited (ASX: SWM) attaches the Annual Report for the year ended 26 June 2021. This release has been authorised to be given to ASX by the Board of Seven West Media Limited. For further information, please contact: Investors/Analysts Media Alan Stuart Rob Sharpe T: +61 2 8777 7211 T: +61 437 928 884 E: [email protected] E: [email protected] Seven West Media Limited / 50 Hasler Road, Osborne Park WA 6017 Australia / PO Box 7077, Alexandria NSW 2015 Australia T +61 2 8777 7777 / ABN 91 053 480 845 Repositioned for growth. Annual Report 2021 Big Brother Contents Our Strategy Who We Are 2 Our Strategic Priorities and Performance Dashboard 4 Executive Letters Letter from the Chairman 6 Letter from the Managing Director and Chief Executive Officer 8 Review of Operations Group Performance – Key Highlights and Summary of Financial Performance 11 Seven Network 17 The West 20 Corporate Social Responsibility Risk, Environment, People and Social Responsibility 22 Seven in the Community 28 Governance Board of Directors 33 Corporate Governance Statement 36 Directors’ Report 47 Remuneration Report 52 Auditor’s Independence Declaration 73 Financial Statements Financial Statements 74 Directors’ Declaration 132 Independent Auditor’s Report 133 Investor Information 138 Shareholder Information 139 Company Information 141 1 Section 1: Our Strategy Seven West Media Limited Annual Report 2021 Who We Are Transforming to lead Seven West Media is being transformed to drive long-term success.