Financial Sector Science-Based Targets Guidance Pilot Version 1.1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Eurazeo Strengthens Its Asset Management Activities with a New Organisation Meeting the Needs of Its Investors

EURAZEO STRENGTHENS ITS ASSET MANAGEMENT ACTIVITIES WITH A NEW ORGANISATION MEETING THE NEEDS OF ITS INVESTORS Christophe Bavière promoted Senior Managing Partner of Eurazeo and Head of Investment Partners Paris, 5 October 2020 Eurazeo is a leading global investment company with more than €18.5 billion in assets under management and provides investors with valuable access to investment strategies diversified across asset classes, industry sectors and geographies. Currently, 65% of these assets are directly invested in companies’ equity or real assets. Similarly, the Group’s activities in private debt and secondary transactions make it a European leader in these areas and have seen steady growth for several years. Underscoring the appeal of its investment strategies to investors, Eurazeo reached new heights with its fundraising bringing in €2.4 billion in 2019. Following a robust first half of this year, with €1.2 billion raised in unfavourable and uncertain market conditions, Eurazeo expects to build on this momentum over the remainder of the year, driven in particular by the success of the Eurazeo Growth III fund. This performance is not only the result of the renewed commitment and confidence of the Group’s long- standing institutional investor partners, but is also driven by Eurazeo’s increasing ability to attract new international partners. In line with this growth trajectory and in order to offer investors services of the highest standards, Eurazeo today announced that it is strengthening its function dedicated to institutional investors and wealth management structures by bringing together the veteran management teams of Eurazeo and Idinvest. The Group’s teams who focus on maintaining and developing these relationships, are staffed by some 30 investment professionals. -

Emerging Markets Debt Survey Q4 2017 the EMD Market Deconstructed

The EMD market deconstructed Emerging Markets Debt Survey Q4 2017 Report run on 14 March 2018 Clear and Independent Institutional Investment Analysis We provide institutional investors, including pension funds, insurance companies and consultants, with data and analysis to assess, research and report on their investments. We are committed to fostering and nurturing strong, productive relationships across the institutional investment sector and are continually innovating new solutions to meet the industry’s complex needs. We enable institutional investors, including pension funds, insurance companies and consultants, to conduct rigorous, evidence-based assessments of more than 5,000 investment products offered by over 700 asset managers. Additionally, our software solutions enable insurance companies to produce consistent accounting, regulatory and audit-ready reports. To discuss your requirements +44 (0)20 3327 5600 [email protected] Find us at camradata.com Join us on LinkedIn Follow us on Twitter @camradata The CAMRADATA Emerging Market Debt (‘EMD’) survey is based on all USD EMD vehicles in CAMRADATA Live four weeks after the end of the report quarter. Contents Section 1: Market Commentary Section 6: Distribution of Returns 3 Years 1. Market Commentary 23. Distribution of Monthly Returns - All EM Debt Funds 2. Survey Highlights 24. Distribution of Monthly Returns - Broad Bond Funds 25. Distribution of Monthly Returns - Corprate Funds 26. Distribution of Monthly Returns - Government Funds Section 2: EM Debt Universe Section 7: Risk Return 3. Number of Products 27. 12 Month Risk Return – All Emerging Market Debt Funds 4. Number of Products over time 28. 36 Month Risk Return – All Emerging Market Debt Funds 5. -

Spotlight: Shareholders Are Dispersed and Diverse

POLICY SPOTLIGHT APRIL 2019 Shareholders Are Dispersed And Diverse Index funds have democratized access to diversified investment for millions of savers, who are investing for long-term goals, like retirement. As index funds are currently growing more quickly than actively managed funds, some critics have expressed concern about increasing concentration of public company ownership in the hands of index fund managers. While it is true that assets under management (or ‘AUM’) in index portfolios have grown, index funds and ETFs represent less than 10% of global equity assets.1 Further, equity investors, and hence public company shareholders, are dispersed across a diverse range of asset owners and asset managers. As of year-end 2017, Vanguard, BlackRock, and State Street manage $3.5 trillion, $3.3 trillion, and $1.8 trillion in global equity assets, respectively.2 These investors represent a minority position in the $83 trillion global equity market. As shown in Exhibit 1, the combined AUM of these three managers represents just over 10% of global equity assets. The largest 20 asset managers only account for 22%. Moreover, about two-thirds of all global equity investment is conducted by asset owners choosing to invest in equities directly rather than by employing an asset manager to make investments on their behalf. Exhibit 1: Equity Market Investors3 Total Equity Market Capitalization 100% All Asset Managers 35% Top 20 Managers 22% Top 10 Managers 17% VGD 4% BLK 4% SSgA 2% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Exhibit 1 alone does not paint a complete picture of the diversity of equity market investors, as there is significant variation amongst asset managers and asset owners. -

Breakthrough Energy Ventures Europe

SET4BIO RENEWABLE FUELS AND BIOENERGY FOR A LOW- CARBON EUROPE – ACCELERATING THE IMPLEMENTATION OF THE SET-PLAN ACTION 8 Horizon 2020, Grant AgreementA no. 884524 Title of the Deliverable Due date Actual submission date Report on private financing opportunities to support the realisation of the SET Plan IP8 31.08.2021 31.08.2021 Work Package (WP): Funding and financing roadmap and investments Task: Task 1.4 – Identification of private financing opportunities Lead beneficiary for this deliverable: CIRCE Editors/Authors: Paola Mazzucchelli and Carlos Castellano Pellicena Dissemination level: Public Call identifier: H2020-LC-SC3-2019-Joint-Actions-1 Document history V Date Beneficiary Author/Reviewer 3.0 24/08/2021 CIRCE Paola Mazzucchelli This project has received funding from the European Union's Horizon 2020 research and innovation programme under grant agreement No 884524 EXECUTIVE SUMMARY Deliverable 1.3 summarises information related to existing private financing mechanisms that can be of interest to support the development of the projects defined in the Implementation Plan of IP8 dedicated to bioenergy and other renewable fuels. It aims at being a guide for project developers who are looking for private funds to finance their project. Several updates of this report are planned until the project’s end in February 2023. PARTNERS RISE - Research Institutes of Sweden AB, Sweden SINTEF - SINTEF Energi AS, Norway FNR - Fachagentur Nachwachsende Rohstoffe e.V., Germany CIRCE - Fundacion Circe Centro de Investigación de Recursos y Consumos Energéticos, Spain VTT – Teknologian tutkimuskeskus VTT Oy, Finland ETA – ETA Florence Renewable Energies, Italy Statement of Originality This deliverable contains original unpublished work except where clearly indicated otherwise. -

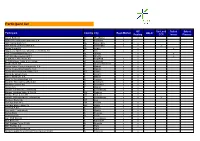

Participant List

Participant list GC SecLend Select Select Participant Country City Repo Market HQLAx Pooling CCP Invest Finance Aareal Bank AG D Wiesbaden x x ABANCA Corporaction Bancaria S.A E Betanzos x ABN AMRO Bank N.V. NL Amsterdam x x ABN AMRO Clearing Bank N.V. NL Amsterdam x x x Airbus Group SE NL Leiden x x Allgemeine Sparkasse Oberösterreich Bank AG A Linz x x ASR Levensverzekering N.V. NL Utrecht x x ASR Schadeverzekering N.V. NL Utrecht x x Augsburger Aktienbank AG D Augsburg x x B. Metzler seel. Sohn & Co. KGaA D Frankfurt x x Baader Bank AG D Unterschleissheim x x Banco Bilbao Vizcaya Argentaria, S.A. E Madrid x x Banco Cooperativo Español, S.A. E Madrid x x Banco de Investimento Global, S.A. PT Lisbon x x Banco de Sabadell S.A. E Alicante x x Banco Santander S.A. E Madrid x x Bank für Sozialwirtschaft AG D Cologne x x Bank für Tirol und Vorarlberg AG A Innsbruck x x Bankhaus Lampe KG D Dusseldorf x x Bankia S.A. E Madrid x x Banque Centrale du Luxembourg L Luxembourg x x Banque Lombard Odier & Cie SA CH Geneva x x Banque Pictet & Cie AG CH Geneva x x Banque Internationale à Luxembourg L Luxembourg x x x Bantleon Bank AG CH Zug x Barclays Bank PLC GB London x x Barclays Bank Ireland Plc IRL Dublin x x BAWAG P.S.K. A Vienna x x Bayerische Landesbank D Munich x x Belfius Bank B Brussels x x Berlin Hyp AG D Berlin x x BGL BNP Paribas L Luxembourg x x BKS Bank AG A Klagenfurt x x BNP Paribas Fortis SA/NV B Brussels x x BNP Paribas S.A. -

Monthly Factsheet

AMUNDI FUNDS PIONEER US EQUITY FUNDAMENTAL GROWTH - A USD FACTSHEET 31/08/2021 EQUITY ■ Objective and Investment Policy The Sub-Fund is a financial product that promotes ESG characteristics pursuant to Article 8 of the Disclosure Regulation. Seeks to increase the value of your investment over the recommended holding period. The Sub-Fund invests mainly in a broad range of equities of companies that are based in, or do most of their business in the U.S.A. The Sub-Fund makes use of derivatives to reduce various risks, for efficient portfolio management and as a way to gain exposure (long or short) to various assets, markets or other investment opportunities (including derivatives which focus on equities). Benchmark : The Sub-Fund is actively managed by reference to and seeks to outperform the Russell 1000 Growth Index. The Sub-Fund is mainly exposed to the issuers of the Benchmark, however, the management of the Sub-Fund is discretionary, and will be exposed to issuers not included in the Benchmark. The Sub-Fund monitors risk exposure in relation to the Benchmark however the extent of deviation from the Benchmark is expected to be significant. Further, the Sub-Fund has designated the benchmark as a reference benchmark for the purpose of the Disclosure Regulation. The Benchmark is a broad market index, which does not assess or include constituents according to environmental characteristics, and therefore is not aligned with the environmental characteristics promoted by the Sub-Fund. Management Process : The Sub-Fund integrates Sustainability Factors in its investment process as outlined in more detail in section "Sustainable Investment" of the Prospectus. -

MGT Teesside Biomass Power Station United Kingdom

MGT Teesside biomass power station United Kingdom Sectors: Biomass Electric Power Generation On record This profile is no longer actively maintained, with the information now possibly out of date Send feedback on this profile By: BankTrack, Biofuelwatch, Dogwood Alliance, Markets for Change & NOAH (Friends of the Earth Denmark) Created on: Dec 9 2016 Last update: Aug 14 2020 Contact: Adam Macon, Dogwood Alliance. Bente Hessellund Andersen, NOAH (Friends of the Earth Denmark) Project website Status Planning Design Agreement Construction Operation Closure Decommission Sectors Biomass Electric Power Generation Location Status Planning Design Agreement Construction Operation Closure Decommission Website http://www.mgtteesside.co.uk/ This project has been identified as an Equator Project About MGT Teesside biomass power station MGT Teesside recently started building a 299 MW biomass power station at Teesport in the northeast of England. This will be the world's biggest purpose-built biomass power station. It will burn up to 1.5 million tonnes of pellets per year, made from around 3 million tonnes of green wood: wood that has been recently cut and therefore has not had an opportunity to dry by evaporation of the internal moisture. MGT Teesside has entered into a sourcing contract with Enviva, the biggest US pellet producer, for one million tonnes of pellets each year. NGOs and reporters have gathered evidence that Enviva is sourcing a significant proportion of their wood from the clearcutting of highly biodiverse coastal wetland forests on the North American Coastal Plain, which has been declared a Global Biodiversity Hotspot. Latest developments Environmental campaigners in US and Denmark urge key investor to withdraw investment from large biomass power station project MGT Teesside Nov 17 2016 MGT Teesside biomass power station reaches financial close Aug 11 2016 What must happen PKA and Macquarie should immediately divest their 50% equity stakes in MGT Power. -

2017-2018 Annual Investment Report Retirement System Investment Commission Table of Contents Chair Report

South Carolina Retirement System Investment Commission 2017-2018 Annual Investment Report South Carolina Retirement System Investment Commission Annual Investment Report Fiscal Year Ended June 30, 2018 Capitol Center 1201 Main Street, Suite 1510 Columbia, SC 29201 Rebecca Gunnlaugsson, Ph.D. Chair for the period July 1, 2016 - June 30, 2018 Ronald Wilder, Ph.D. Chair for the period July 1, 2018 - Present 2017-2018 ANNUAL INVESTMENT REPORT RETIREMENT SYSTEM INVESTMENT COMMISSION TABLE OF CONTENTS CHAIR REPORT Chair Report ............................................................................................................................... 1 Consultant Letter ........................................................................................................................ 3 Overview ................................................................................................................................... 7 Commission ............................................................................................................................... 9 Policy Allocation ........................................................................................................................13 Manager Returns (Net of Fees) ..................................................................................................14 Securities Lending .....................................................................................................................18 Expenses ...................................................................................................................................19 -

En Im Square Secures Significant Financing

EN IM SQUARE SECURES SIGNIFICANT FINANCING SUPPORT FROM EURAZEO AND LAUNCHES ITS US DISTRIBUTION PLATFORM • iM Square announces its renewed objective to invest with current and future shareholders over $500 million within 2 to 4 years • iM Square announces the launch iM Global Partner US, its new American distribution platform PARIS/LONDON (16th of March 2018) iM Square, the sole European investment and development platform dedicated to asset management, successfully secured a new financing commitment from Eurazeo, one of its founding shareholder, after having completed its initial ambitious growth phase. Eurazeo is committed to support iM Square's investments over the next few years and is expected to become its reference shareholder. Other founding shareholder Le Groupe Dassault / La Maison will also participate. This new commitment will enable iM Square to acquire additional 3 to 6 entrepreneurial active asset managers with $1 to 20 billion of AUM, high growth potential and complementary strategies, such as alternative management. Most of the targeted asset managers are based in the US and Europe. In additional to permanent capital, iM Square also brings financial and operational support as well as taylor- maid investment and distribution capabilities to its partners, which makes iM Square’s model unique in Europe. Since 2015, iM Square has successfully acquired minority stakes in two US asset management companies: Polen Capital, an independent management firm specialised in growth stocks and Dolan McEniry Capital, specialised in US corporate bonds. The performances of these two asset managers are remarkable and their AUM continue to undergo strong growth: Polen Capital’s AUM grew from 7.5 to $17.4 billion since the partnership with iM Square in 2016, while Dolan McEniry’s grew from 5.8 to almost $6.5 billion since iM Square’s stake was acquired. -

Welcome to the 12Th Annual INSEAD Private Equity Conference

Welcome to the 12th Annual INSEAD Private Equity Conference INSEAD welcomes you to the 12th Annual Private Equity Conference. The conference, inaugurated in 2003, has become the most successful private equity and venture capital event hosted by a European academic institution. With over 1,500 alumni working in the industry worldwide, INSEAD’s presence in the private equity community is well-recognized. This conference is a gathering amongst leading practitioners, academics and the INSEAD community to debate the forces shaping the private equity industry. We are delighted to host an impressive and diverse group of experienced industry professionals here on INSEAD Europe Campus. Since the financial crisis, one of the strongest trends in private equity has been increased focus on value creation. This year’s theme, “How to achieve alpha in the current environment,” aims to delve into the topic of generating returns through operational change, and assess the implications of this trend for the future of private equity. Our keynote speakers, leveraged buyouts and operational excellence panels will explore the topic of value creation deeper. Beyond value creation, the industry is further being shaped by a number of different dynamics and intense competition. To further develop the main theme, we have lined up a focused range of panels and have assembled a diverse group of outstanding panelists and moderators for you. Our panels will attempt to give an update on the current state in different parts of the industry, such as distressed investing, infrastructure and real assets, emerging strategies and limited partner relationships. The annual conference is organized by student and alumni members of the INSEAD Private Equity Club, Global Private Equity Initiative (INSEAD faculty body focused on research in Private Equity industry), Alumni Relations and Student Life offices. -

Fidelity® International Sustainability Index Fund

Fidelity® International Sustainability Index Fund Annual Report October 31, 2020 See the inside front cover for important information about access to your fund’s shareholder reports. Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of a fund’s shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the fund or from your financial intermediary, such as a financial advisor, broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from a fund electronically, by contacting your financial intermediary. For Fidelity customers, visit Fidelity’s web site or call Fidelity using the contact information listed below. You may elect to receive all future reports in paper free of charge. If you wish to continue receiving paper copies of your shareholder reports, you may contact your financial intermediary or, if you are a Fidelity customer, visit Fidelity’s website, or call Fidelity at the applicable toll-free number listed below. Your election to receive reports in paper will apply to all funds held with the fund complex/your financial intermediary. Account Type Website -

Succès De L'émission De L'obligation « Senior

COMMUNIQUE DE PRESSE Paris, le 15 juin 2020 La Banque Postale : succès de l’émission de l’obligation « Senior Non Préférée » de 750 M€ Dans le contexte de crise sanitaire et économique, La Banque Postale a émis avec succès une obligation « Senior Non Préférée » pour un montant de 750 M€. La maturité de 6 ans est assortie d’un coupon fixe de 0,50 % sur 5 ans, puis d'un coupon variable en cas de non exercice de l'option de rappel à l'année 5. Cette émission est conforme à la stratégie de La Banque Postale de renforcer ses ressources éligibles au MREL 1. Le carnet d’ordres final de la transaction atteint 2,5 Md€ (soit un taux de souscription de 3,3 fois par plus de 137 investisseurs différents), grâce à une forte demande des gestionnaires d’actifs. La répartition géographique du carnet d’ordres est bien diversifiée pour cette émission : France 40 %, Allemagne, Suisse & Autriche 22 %, Benelux 12 %, Angleterre & Irlande 10 %, Europe du Sud 9 %, Europe du Nord 6 %. La transaction, notée BBB+ par Fitch et BBB par S&P présente un spread final resserré à MS + 88 bp. La Banque Postale, BNP Paribas, Commerzbank, Citigroup, UBS Europe et UniCredit ont été mandatés par La Banque Postale en tant que co-chefs de file sur cette opération. 1 Minimum Requirement for own funds and eligible liabilities A propos de La Banque Postale La Banque Postale, forme avec ses filiales dont CNP Assurances, un grand groupe de bancassurance, filiale du Groupe La Poste, présent sur les marchés de la banque de détail, de l’assurance, de la banque de financement et de la gestion d’actifs.