Zero Emission Road Freight Strategy 2020-2025

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

T680 76-Inch Sleeper KENWORTH the WORLD’S BEST

T680 76-Inch Sleeper KENWORTH THE WORLD’S BEST. BOLD INTELLIGENT PRODUCTIVE THE CONTINUED BENCHMARK IN PERFORMANCE AND PROFITABILITY Kenworth’s T680 is a true game changer in the business of running trucks at a profit. Aggressive aerodynamic design. A fully integrated, highly efficient PACCAR Powertrain. REWARDING Uptime engineering that results in an unmatched work ethic. Plus a level of luxury, craftsmanship and intuitive control that makes the T680 The Driver’s Truck™ — a factor that helps every Kenworth fleet attract and retain the industry’s best operators. T680 76-Inch Sleeper THE CUTTING EDGE JUST GOT A WHOLE LOT SHARPER. Start with the most highly evolved aerodynamic long-haul tractor, the Kenworth T680. Add special factory-installed aerodynamic enhancements for the tractor that combine to reduce drag to an absolute minimum. Optimize the powertrain with the fuel efficient PACCAR MX-13 engine, PACCAR transmission and PACCAR drive axles. Incorporate Kenworth’s Idle Management System, which eliminates the need to run the truck for off-duty temperature control. And integrate real-time reporting technology to help the driver run in the sweet spot for maximum fuel efficiency. Kenworth luxury, craftsmanship, reliability and driver satisfaction also come as part of the deal. KENWORTH THE WORLD’S BEST. Fuel Saving Intelligence: • Most advanced and aerodynamic truck ever produced by Kenworth • Predictive Cruise Control • Driver Performance Assistant • Front air dams, 19 inch side extenders and chassis fairing extenders, • Predictive Neutral -

Talking Tesla Elon Musk

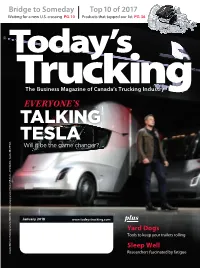

Bridge to Someday Top 10 of 2017 Waiting for a new U.S. crossing PG. 10 Products that topped our list PG. 36 The Business Magazine of Canada’s Trucking Industry EVERYONE’S TALKING TESLA W 5C4. Will it be the game changer? January 2018 www.todaystrucking.com plus Yard Dogs Tools to keep your trailers rolling Sleep Well Canadian Mail Sales Product Agreement #40063170. Return postage guaranteed. Newcom Media Inc., 451 Attwell Dr., Toronto, ON M9 Researchers fascinated by fatigue Contents January 2018 | VOLUME 32, NO.1 5 Letters 7 John G. Smith 10 16 9 Rolf Lockwood 31 Mike McCarron NEWS & NOTES Dispatches 13 MacKinnon Sold Ontario fleet sold to Contrans 22 Heard on the Street 32 36 23 Logbook 24 Truck Sales 25 Pulse Survey 26 Stat Pack 27 Trending 30 Truck of the Month In Gear 44 Yard Dogs Features Keep trailers moving in the yard with 10 Bridge to Someday specialized equipment Work on the Gordie Howe International 48 Southern Stars Bridge continues, but at a slow pace By Elizabeth Bate Cabovers gaining ground in Mexico 16 Talking Tesla 51 Product Watch Elon Musk (partially) unveils his electric truck. 52 Guess the location, Will it be the game changer he promises? By John G. Smith win a hat 32 Sleep Well Good health begins with proper sleep. Researchers want to know if drivers are getting what they need. By Elizabeth Bate 36 The Top 10 Here’s the tech that topped our editor’s list in 2017 By John G. Smith Cover Image: Courtesy of Tesla For more visit www.todaystrucking.com JANUARY 2018 3 BORN TO BE Designed with decades of experience BETTER. -

Holiday Last Day to Ship

2021 Shipping deadlines for holiday packages Last days to ship U.S. to U.S. Mon Tues Weds Thurs Fri Sat Sun Mon Tues Weds Thurs Fri Sat Sun Mon Tues Weds Thurs Fri FedEx Express® 12/6 12/7 12/8 12/9 12/10 12/11 12/12 12/13 12/14 12/15 12/16 12/17 12/18 12/19 12/20 12/21 12/22 12/23 12/24 FedEx Same Day® FO, PO, SO, Extra Hours 2Day & 2Day AM FedEx Express Saver® FedEx 1Day® Freight 12/19 FedEx 2Day® Freight FedEx 3Day® Freight FedEx Ground® 12/6 12/7 12/8 12/9 12/10 12/11 12/12 12/13 12/14 12/15 12/16 12/17 12/18 12/19 12/20 12/21 12/22 12/23 12/24 FedEx Ground® Contiguous US FedEx Ground® Alaska and Hawaii FedEx Home Delivery® Contiguous US FedEx Home Delivery® Alaska and Hawaii FedEx Ground® Economy FedEx Freight® 12/6 12/7 12/8 12/9 12/10 12/11 12/12 12/13 12/14 12/15 12/16 12/17 12/18 12/19 12/20 12/21 12/22 12/23 12/24 FedEx Freight® Priority FedEx Freight® Economy FedEx Freight® Direct International Mon Tues Weds Thurs Fri Sat Sun Mon Tues Weds Thurs Fri Sat Sun Mon Tues Weds Thurs Fri U.S. to Canada 12/6 12/7 12/8 12/9 12/10 12/11 12/12 12/13 12/14 12/15 12/16 12/17 12/18 12/19 12/20 12/21 12/22 12/23 12/24 FedEx® International Next Flight FedEx International First® FedEx International Priority® FedEx International Priority Distribution® FedEx International Economy® U.S. -

Ac Compressors

A/C COMPRESSORS 2019 PARTS GUIDE allianceparts.com INTRODUCTION INTRODUCTION ALL-MAKES HEAVY-DUTY A/C COMPRESSORS With parts and accessories for all makes and models1, Alliance Parts is the smartest choice for value on the road. Readily available, easily affordable and assured in quality, Alliance has everything you need to deliver. PARTS NUMBERING SYSTEM All part numbers in this program contain the prefix ABP and N83 (the company-assigned code for this program). The remaining digits are based on part and design. Example – ABP N83 304QP7H154417 All Alliance Parts products in the catalog are set up with an Alliance part number. In the back of this catalog, you will find an extensive cross-reference list. This will help link another manufacturer’s part to an Alliance ABP number. WARRANTY Alliance products are backed by a 1-year/unlimited-mile standard warranty. Additional warranty coverage may apply where specified. Illustrations and photographs used in this catalog may vary slightly from the actual product. Prototype samples are sometimes used for photography. The production parts may vary slightly. Availability of products shown in this catalog is subject to change without notice. 1For nearly all heavy-duty truck makes and models. 2019 | ALLIANCE PARTS A/C COMPRESSORS 2 TABLE OF CONTENTS TABLE OF CONTENTS TABLE WOBBLE PLATE COMPRESSORS 1 SPECIFICATIONS ...............................................................................................................................................5 PARTS LIST .........................................................................................................................................................6 -

Trp Parts Catalog

Parts for Trucks, Trailers & Buses ® BUS PARTS 5 CAB Proven, reliable and always innovative. TRP® offers reliable aftermarket products that are designed and tested to exceed customers’ expectations regardless of the vehicle make, model or age. GLASS • BUMPERS • MIRRORS • MIRROR HARDWARE • WIPER BLADES TABLE OF CONTENTS Tested. Reliable. Guaranteed. CAB BUS GLASS Cab Amtran ...........................5-7 Blue Bird .........................5-8 Choosing the right replacement part or service for Carpenter .......................5-10 your vehicle—whether you own Navistar .........................5-10 one, or a fleet—is one of the most important decisions you Thomas .........................5-11 can make for your business. And, with tested TRP® parts Ward ...........................5-14 it’s an easy decision. Wayne ..........................5-14 Regardless of the make you drive, TRP® quality CABOVER GLASS replacement parts are Ford ............................5-15 engineered to fit your truck, trailer or bus. Choose the Freightliner ......................5-15 parts that give you the best Hino ............................5-16 value for your business. Check them out at an approved Isuzu ...........................5-17 TRP® retailer near you. Mack ...........................5-18 Mitsubishi .......................5-19 Navistar .........................5-20 Nissan ..........................5-21 The cross reference information in this catalog is based upon data provided Peterbilt .........................5-21 by several industry sources and our partners. While every attempt is made to ensure the information presented Volvo ...........................5-22 is accurate, we bear no liability due to incorrect or incomplete information. Product Availability Due to export restrictions and market ® demands, not all products are TRP North America always available in every location. 750 Houser Way N. Check for availability in your area with your local TRP® Distributor. -

Driving Prosperity Driving Prosperity Through Transport Solutions

VOLVO GROUP ANNUAL AND SUSTAINABILITY REPORT 2018 Driving prosperity Driving prosperity through transport solutions The Volvo Group’s mission statement expresses a broad ambition – to drive prosperity. Our customers provide modern logistics as the base for our economic welfare. Transport supports growth, provides access for people and goods and helps combat poverty. Modern transport solutions facilitate the increasing urbanization in a more sustainableainable way. Transport is not an end in itself, but ratherher a means allowing people to access what theyhey need, economically and socially. A GLOBAL GROUP 2018 OVERVIEW Our customers make societies work The Volvo Group’s products and services contribute to much of what Volvo Group’s customers are companies within the transportation we all expect of a well-functioning society. Our trucks, buses, engines, or infrastructure industries. The reliability and productivity of the construction equipment and financial services are involved in many products are important and in many cases crucial to our customers’ of the functions that most of us rely on every day. The majority of the success and profitability. ON THE ROAD OFF ROAD IN THE CITY AT SEA Our products help ensure that Engines, machines and vehicles Our products are part of daily Our products and services people have food on the table, from the Volvo Group can be life. They take people to work, are there, regardless of whether can travel to their destination found at construction sites, in collect rubbish and keep lights someone is at work on a ship, and have roads to drive on. mines and in the middle of shining. -

In the United States District Court for the District of Connecticut

Case 3:15-cv-01550-JAM Document 120 Filed 06/27/17 Page 1 of 45 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF CONNECTICUT CARLOS TAVERAS, individually and on behalf of all others similarly situated, Plaintiff, C.A. No. 3:15-cv-01550-JAM v. XPO LAST MILE, INC. Defendant. XPO LAST MILE, INC. Third-Party Plaintiff, v. EXPEDITED TRANSPORT SERVICES, LLC. Third-Party Defendant. PLAINTIFF’S ASSENTED-TO MOTION FOR FINAL APPROVAL OF A CLASS ACTION SETTLEMENT Plaintiff filed this lawsuit on behalf of himself and a class of similarly situated delivery drivers who performed delivery services for Defendant XPO Last Mile, Inc. in Connecticut pursuant to standard contracts under which they were classified as independent contractors. Plaintiff alleges that XPO’s delivery contractors were actually employees, and based on this misclassification, XPO’s practice of making deductions from its delivery drivers’ pay for such things as damage claims and worker’s compensation violates the Connecticut wage payments laws. Conn. Gen. Stat. Sec. 31-71e. The parties have reached a non-reversionary class action settlement for $950,000. 1 Case 3:15-cv-01550-JAM Document 120 Filed 06/27/17 Page 2 of 45 On March 17, 2017, the Court granted preliminary approval of the proposed settlement, certified a class of individuals who performed delivery services for Defendant XPO Last Mile, Inc. in Connecticut pursuant to contracts that class them as independent contractors, and authorized notice to the class. ECF No. 115. Plaintiff now seeks the Court’s final approval of the proposed class action settlement at the final settlement approval hearing scheduled for July 7, 2017. -

FREIGHTLINER Ecascadia the FUTURE of COMMERCE

Insider ELECTRIC CAR Buyers Guide Buyers COMMERCIAL VEHICLES ELECTRIC TRUCK COMPLETE REVIEWS Mobile App REBATES GUIDE REBATES FREIGHTLINER eCASCADIA THE FUTURE OF COMMERCE BYD Class 6 PROTERRA Catalyst US: $9.45 CA: $11.45 EV Educational Pillars Displays for Electric Vehicle Exhibitions and Educational Events Get answers to the most common EV questions, including: • How do I charge my truck? • How far can electric trucks drive? • What incentives and rebates are available? • Are electric trucks really cheaper to operate? • How green are electric trucks? Set up throughout an event space: • Provide educational exhibits at intervals along the walking loop. • Create consistent visual appeal throughout the exhibit area. • When displayed together, the ten exhibits provide a complete introductory knowledge to owning and driving electric vehicles. Fully customizable with your logo, local pricing data and other information. Call us for more information and pricing www.electric-car-insider.com/edu-exhibits.html 619-335-7102 Buyers Guide Contents 2020 Q3 TRUCKS & VANS 8 FEATURES Tesla Semi 7 From the Editor Nikola TWO 8 Electric Crossovers Here, Trucks Coming 3 Freightliner eCascadia 9 Volvo VNR Electric 10 XOS ET-One 11 ELECTRIC VEHICLE BUYERS GUIDE Peterbilt 579EV 12 16 Commercial Electric Vehicles Freightliner eM2 13 Profiles and Specifications 6 Peterbilt 220EV 14 XOS Medium Duty 15 Lion 8 16 BYD Class 8 17 Mitsubishi Fuso eCanter 18 SEA Electric Hino 195 EV 19 34 25 BYD Class 6 20 Phoenix Zeus 500 21 Motiv Power Systems Epic 22 Cummins PowerDrive -

India Leaps Ahead: Transformative Mobility Solutions for All

M OUN KY T C A I O N R I N E STIT U T INDIA LEAPS AHEAD: TRANSFORMATIVE MOBILITY SOLUTIONS FOR ALL MAY 2017 AUTHORS & ACKNOWLEDGMENTS AUTHORS SUGGESTED CITATION NITI Aayog: NITI Aayog and Rocky Mountain Institute. India Leaps Ahead: Transformative mobility solutions for all. Amit Bhardwaj 2017. https://www.rmi.org/insights/reports/transformative_mobility_solutions_india Shikha Juyal Sarbojit Pal ACKNOWLEDGMENTS Dr. Manoj Singh Shashvat Singh The authors would like to thank the following individuals for their contribution. Rocky Mountain Institute: Adnan Ansari, Albright Stonebridge Group Marshall Abramczyk Manuel Esquivel, Independent Consultant Aman Chitkara Jules Kortenhorst, Rocky Mountain Institute Ryan Laemel Amory Lovins, Rocky Mountain Institute James Newcomb Robert McIntosh, Rocky Mountain Institute Clay Stranger Jesse Morris, Rocky Mountain Institute Greg Rucks, Rocky Mountain Institute * Authors listed alphabetically Anand Shah, Albright Stonebridge Group Samhita Shiledar, Independent Consultant Vindhya Tripathi, BTC Productions Art Director: Romy Purshouse Jonathan Walker, Rocky Mountain Institute Designer: Michelle Fox Jeruld Weiland, Rocky Mountain Institute Designer: Laine Nickl Supporters: Editorial Director: Cindie Baker The authors would also like to thank ClimateWorks Foundation, the Grantham Foundation for the Editor: David Labrador Protection of the Environment, George Krumme, and Wiancko Charitable Foundation for their generous support that made this report possible. Marketing Manager: Todd Zeranski CONTACTS The views and opinions expressed in this document are those of the authors and do not necessarily reflect the For more information, please contact: positions of the institutions or governments. The specific solutions listed in chapter five were generated by a group of 75 stakeholders during the NITI Aayog and RMI Transformative Mobility Solutions Charrette in New Delhi in February Shikha Juyal, [email protected] 2017. -

Evaluating Fedex Express Hybrid-Electric Delivery Trucks

VEHICLE TECHNOLOGIES PROGRAM Project Results: Evaluating FedEx Express Hybrid-Electric Delivery Trucks The National Renewable Energy Laboratory’s (NREL’s) Fleet Test and Evaluation Team evaluated the 12-month, in-service performance of three Class 4 gasoline hybrid-electric delivery trucks and three comparable conventional diesel trucks operated by FedEx Express in Southern California. In addition, the tailpipe emissions and fuel economy of one of the gasoline hybrid-electric vehicles (gHEVs) and one diesel truck were tested on a chassis dynamometer. The gHEVs were equipped with a parallel hybrid system manufactured by Azure FedEx Express’s gasoline hybrid-electric delivery trucks Dynamics, including a 100-kW alternating current induction demonstrated lower tailpipe emissions compared with conventional motor, regenerative braking, and a 2.45-kWh nickel-metal- diesel delivery trucks. Courtesy of Sam Snyder, FedEx Express hydride battery pack. This fact sheet summarizes the results of the evaluation of the gHEVs. This technology evaluation was part of a collaborative effort In-Service Testing co-funded by the U.S. Department of Energy’s (DOE’s) Three routes served by gHEVs and three served by Vehicle Technologies Program and the South Coast Air conventional diesel trucks were selected for the evaluation, Quality Management District (SCAQMD) via CALSTART. which took place from April 2009 to April 2010. The gHEVs The in-use technology evaluation was conducted by NREL were moved to the initial diesel routes after 6 months of and primarily sponsored by DOE. The chassis dynamometer evaluation, while the diesel trucks were moved to the initial testing was conducted by NREL and primarily funded by gHEV routes. -

AGM Notice 2021

FIFTH GEAR VENTURES LIMITED CIN: U74999MH2015PLC357932 Regd. Office: Mahindra Towers, P. K. Kurne Chowk, Worli, Mumbai – 400018 Telephone No. 022 – 24901411 Fax No: 2490 0833 Website: www.carandbike.com ========================================================== NOTICE NOTICE IS HEREBY GIVEN THAT THE SIXTH ANNUAL GENERAL MEETING OF FIFTH GEAR VENTURES LIMITED WILL BE HELD, THROUGH VIDEO CONFERENCING (“VC”)/OTHER AUDIO VISUAL MEANS (“OAVM”), AT MAHINDRA TOWERS, P. K. KURNE CHOWK, WORLI, MUMBAI-400018 (DEEMED VENUE OF THE AGM) ON WEDNESDAY, 21ST JULY, 2021 AT 12.30 P.M. TO TRANSACT THE FOLLOWING BUSINESSES: The proceedings of the Annual General Meeting (“AGM”) shall be deemed to be conducted at the Registered Office of the Company which shall be the deemed venue of the AGM. ORDINARY BUSINESS 1. To receive, consider and adopt the Audited Financial Statements of the Company for the financial year ended 31st March, 2021, including the Audited Balance Sheet as at 31st March, 2021 and the Statement of Profit and Loss for the year ended on that date and the Reports of the Board of Directors and Auditors thereon. 2. To appoint a Director in place of Mr. Rajeev Dubey (DIN: 00104817) who retires by rotation and, being eligible, offers himself for re-appointment. 3. To appoint Statutory Auditors of the Company and fix their remuneration: “RESOLVED that pursuant to Section 139 and other applicable provisions, if any, of the Companies Act, 2013 read with the Companies (Audit and Auditors) Rules, 2014 as amended from time to time (“Act”), M/s. BSR & Co LLP, Chartered Accountants, (ICAI FRN 101248W/W100022) be and they are hereby appointed as the Statutory Auditors of the Company for a term of 5 (five) years to hold office from the conclusion of this 6th Annual General Meeting until the conclusion of the 11th Annual General Meeting of the Company to be held in the year 2026 at such remuneration as may be fixed by Board of Directors. -

Electric Vehicle Market Status - Update Manufacturer Commitments to Future Electric Mobility in the U.S

Electric Vehicle Market Status - Update Manufacturer Commitments to Future Electric Mobility in the U.S. and Worldwide September 2020 Contents Acknowledgements ....................................................................................................................................... 2 Executive Summary ...................................................................................................................................... 3 Drivers of Global Electric Vehicle Growth – Global Goals to Phase out Internal Combustion Engines ..... 6 Policy Drivers of U.S. Electric Vehicle Growth ........................................................................................... 8 Manufacturer Commitments ....................................................................................................................... 10 Job Creation ................................................................................................................................................ 13 Charging Network Investments .................................................................................................................. 15 Commercial Fleet Electrification Commitments ........................................................................................ 17 Sales Forecast.............................................................................................................................................. 19 Battery Pack Cost Projections and EV Price Parity ...................................................................................