Investor Presentation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Skills and Services Directory Achieve More from Your Property Property

Skills and Services Directory Achieve more from your property Property. It’s what we do every day – and we love it. When you experience the difference we can make, we think you’ll really appreciate what we do… So how can we help you exactly? Well, we offer you expert advice and a comprehensive range of services to cover all your property needs. We can help you make the very best property decisions to get the result you’re after. We are ready to help you make sure you achieve more from your property right now. Contact us today on 0333 772 1235 or [email protected] Asset Experience Academic, Health and Land Community Property and Institutional Airfields Public Realm Day care facilities Barns Community centres Doctors’ surgeries Brownfield sites County farm estates Extra care development Common land Leisure centres Primary care centres Contaminated land Libraries and information centres Respite and Residential Country parks, national parks Markets and small business centres care facilities and public open spaces Police, fire and ambulance stations Schools, colleges and Crown land Public access universities Development land Sports centres Student accommodation Entitlement Social housing Supported housing ESAs, AONBs and SSSIs Town halls and administrative Equestrian offices Historical Estates Ancient Monuments Farm and accommodation land Residential Churches Foreshores and rivers Country houses Church houses Glebe land Residential investments Listed buildings Greenfield sites Horticulture Retail Industrial Landfill sites Banks -

Taylor Woodrow Plc Report and Accounts 2006 Our Aim Is to Be the Homebuilder of Choice

Taylor Woodrow plc Report and Accounts 2006 Our aim is to be the homebuilder of choice. Our primary business is the development of sustainable communities of high-quality homes in selected markets in the UK, North America, Spain and Gibraltar. We seek to add shareholder value through the achievement of profitable growth and effective capital management. Contents 01 Group Financial Highlights 54 Consolidated Cash Flow 02 Chairman’s Statement Statement 05 Chief Executive’s Review 55 Notes to the Consolidated 28 Board of Directors Financial Statements 30 Report of the Directors 79 Independent Auditors’ Report 33 Corporate Governance Statement 80 Accounting Policies 37 Directors’ Remuneration Report 81 Company Balance Sheet 46 Directors’ Responsibilities 82 Notes to the Company Financial Statement Statements 47 Independent Auditors’ Report 87 Particulars of Principal Subsidiary 48 Accounting Policies Undertakings 51 Consolidated Income Statement 88 Five Year Review 52 Consolidated Statement of 90 Shareholder Facilities Recognised Income and Expense 92 Principal Taylor Woodrow Offices 53 Consolidated Balance Sheet Group Financial Highlights • Group revenues £3.68bn (2005: £3.56bn) • Housing profit from operations* £469m (2005: £456m) • Profit before tax £406m (2005: £411m) • Basic earnings per share 50.5 pence (2005: 50.6 pence) • Full year dividend 14.75 pence (2005: 13.4 pence) • Net gearing 18.6 per cent (2005: 23.7 per cent) • Equity shareholders’ funds per share 364.7 pence (2005: 338.4 pence) Profit before tax £m 2006 405.6 2005 411.0 2004 403.9 Full year dividend pence (Represents interim dividends declared and paid and final dividend for the year as declared by the Board) 2006 14.75 2005 13.4 2004 11.1 Equity shareholders’ funds per share pence 2006 364.7 2005 338.4 2004 303.8 * Profit from operations is before joint ventures’ interest and tax (see Note 3, page 56). -

City Investment Watch

UK Commercial – January 2021 MARKET IN City Investment MINUTES Savills Research Watch December records highest monthly volume of 2020 bringing the annual total to £4.48Bn. December is historically the busiest month of the year as and retail complex totals approximately 192,700 sq. ft. The investors look to close deals prior to year-end. Any concerns total rent passing is approximately £7.3 million per annum the typical flurry of activity would be impacted by the with approximately 40% of the income expiring in 2021. omnipresent political and economic disruption, principally December saw £1.18Bn focused around lengthy Brexit trade negotiations and the No new assets were marketed in December given the transact over 16 deals ever-evolving Covid-19 pandemic, were allayed swiftly. disruption associated with the November Lockdown and the The largest deal of the year exchanged early in the month Christmas / New Year break. Accordingly, with the rise in contributing to a monthly volume of £1.18Bn, a significant investment turnover there has been an expected fall in the increase on November (£404M) and the 2020 monthly average volume of stock under offer, which currently stands at £1.50Bn of £301.60M, but 31% below December 2019 (£1.69Bn). across 14 transactions. A comparatively strong December contributed to a total Q4 Unsurprisingly given the disruption across both investment volume of £2.14Bn, 34% down on Q4 2019 and 39% down on and occupational markets, investors were principally the Q4 10-year average. Total 2020 transactional volume seeking Core (54% of annual transactional volume over reached £4.48Bn, which is approximately 42.5% down on that 13 transactions) and Core Plus (29% over 29 transactions) achieved in 2019 (£8.18Bn) and 53% below the 10-year average. -

Time to Touch up the CV? Beeb Launches Search for New Director General

BUSINESS WITH PERSONALITY PLOUGHING AHEAD 30 YEARS LATER THE WIMBLEDON LOOK LAND ROVER DISCOVERY TO HEAD BACK TO HITS A LANDMARK P24 MERTON HOME P26 TUESDAY 11 FEBRUARY 2020 ISSUE 3,553 CITYAM.COM FREE HACKED OFF US ramps up China TREASURY TO spat with fresh Equifax charges SET OUT CITY BREXIT PLAN EXCLUSIVE Beyond Brexit, it will also consider “But there will be differences, not CATHERINE NEILAN the industry’s future in relation to least because as a global financial cen- worldwide challenges such as emerg- tre the UK needs to keep pace with @CatNeilan ing technologies and climate change. and drive international standards. THE GOVERNMENT will insist on the Javid sets out the government’s Our starting point will be what’s right right to diverge from EU financial plans to retain regulatory autonomy for the UK.” services regulation as part of a post- while seeking a “reliable equivalence He also re-committed to concluding Brexit trade deal with Brussels. process”, on which a “durable rela- “a full range of equivalence assess- Writing exclusively in City A.M. today, tionship” can be built. ments” by June of this year, in order to chancellor Sajid Javid says the “Of course, each side will only give the system sufficient stability City “will no longer be a rule- grant equivalence if it believes ahead of the end of transition. taker” and reveals that the other’s regulations are One senior industry figure told City ministers are working on compatible,” the chancel- A.M. that while a white paper was EMILY NICOLLE Zhiyong, Wang Qian, Xu Ke and Liu Le, a white paper setting lor writes. -

Consultation Statement Submission Version

Consultation Statement (Submission) November 2019 2 Consultation Statement (Submission) November 2019 Table of contents 1 Introduction ............................................................................................................................... 4 2 Regulation 19 consultation process ........................................................................................... 6 2.1 Notification ................................................................................................................................ 6 Website .................................................................................................................................... 6 Emails ...................................................................................................................................... 6 Social media ............................................................................................................................ 6 Hard copies ............................................................................................................................. 7 2.2 Coverage .................................................................................................................................. 7 Media coverage ....................................................................................................................... 7 Scrutiny Committee ................................................................................................................ 8 Petitions.................................................................................................................................. -

Proptech 3.0: the Future of Real Estate

University of Oxford Research PropTech 3.0: the future of real estate PROPTECH 3.0: THE FUTURE OF REAL ESTATE WWW.SBS.OXFORD.EDU PROPTECH 3.0: THE FUTURE OF REAL ESTATE PropTech 3.0: the future of real estate Right now, thousands of extremely clever people backed by billions of dollars of often expert investment are working very hard to change the way real estate is traded, used and operated. It would be surprising, to say the least, if this burst of activity – let’s call it PropTech 2.0 - does not lead to some significant change. No doubt many PropTech firms will fail and a lot of money will be lost, but there will be some very successful survivors who will in time have a radical impact on what has been a slow-moving, conservative industry. How, and where, will this happen? Underlying this huge capitalist and social endeavour is a clash of generations. Many of the startups are driven by, and aimed at, millennials, but they often look to babyboomers for money - and sometimes for advice. PropTech 2.0 is also engineering a much-needed boost to property market diversity. Unlike many traditional real estate businesses, PropTech is attracting a diversified pool of talent that has a strong female component, representation from different regions of the world and entrepreneurs from a highly diverse career and education background. Given the difference in background between the establishment and the drivers of the PropTech wave, it is not surprising that there is some disagreement about the level of disruption that PropTech 2.0 will create. -

Retail Is Not Dead and Regionally Dominant Shopping Centres Offer an Attractive Value Play

REAL ASSETS Research & Strategy For professional clients only January 2019 Retail is not dead and regionally dominant shopping centres offer anattractive value play Executive summary: ■ The consumer has taken control of the retail relationship which is putting pressure on retailers’ margins, as they face increased competition and a need to invest in a full reconfiguration of their supply chain to offer an “Omni-channel” distribution model ■ This pressure on retailers’ margins is likely to limit rental value growth Justin Curlow prospects over the short-term, as traditional bricks and mortar retailers’ Global Head of Research & Strategy space consolidations leave more voids than online pure play retailers establishing a physical presence absorb ■ In our view, regionally dominant shopping centres and second-tier tourist- oriented city high streets represent an attractive “value play” for investors, as we feel the entire sector is being tainted by the same doomsday brush despite the fact that the operational performance of these schemes remains strong ■ The sector is not without risks, as highlighted by the continued raft of Vanessa Moleiro retailer failures and bankruptcies which could be exacerbated if an economic Research Analyst downturn materialised over the short term. In addition, for those schemes that remain viable and in demand, the retailer-landlord relationship has to respond to a shorter retail life cycle and increased ambiguity across ultimate sales channels ■ Ultimately, we do not think the developed world will stop consuming -

Annex 1: Parker Review Survey Results As at 2 November 2020

Annex 1: Parker Review survey results as at 2 November 2020 The data included in this table is a representation of the survey results as at 2 November 2020, which were self-declared by the FTSE 100 companies. As at March 2021, a further seven FTSE 100 companies have appointed directors from a minority ethnic group, effective in the early months of this year. These companies have been identified through an * in the table below. 3 3 4 4 2 2 Company Company 1 1 (source: BoardEx) Met Not Met Did Not Submit Data Respond Not Did Met Not Met Did Not Submit Data Respond Not Did 1 Admiral Group PLC a 27 Hargreaves Lansdown PLC a 2 Anglo American PLC a 28 Hikma Pharmaceuticals PLC a 3 Antofagasta PLC a 29 HSBC Holdings PLC a InterContinental Hotels 30 a 4 AstraZeneca PLC a Group PLC 5 Avast PLC a 31 Intermediate Capital Group PLC a 6 Aveva PLC a 32 Intertek Group PLC a 7 B&M European Value Retail S.A. a 33 J Sainsbury PLC a 8 Barclays PLC a 34 Johnson Matthey PLC a 9 Barratt Developments PLC a 35 Kingfisher PLC a 10 Berkeley Group Holdings PLC a 36 Legal & General Group PLC a 11 BHP Group PLC a 37 Lloyds Banking Group PLC a 12 BP PLC a 38 Melrose Industries PLC a 13 British American Tobacco PLC a 39 Mondi PLC a 14 British Land Company PLC a 40 National Grid PLC a 15 BT Group PLC a 41 NatWest Group PLC a 16 Bunzl PLC a 42 Ocado Group PLC a 17 Burberry Group PLC a 43 Pearson PLC a 18 Coca-Cola HBC AG a 44 Pennon Group PLC a 19 Compass Group PLC a 45 Phoenix Group Holdings PLC a 20 Diageo PLC a 46 Polymetal International PLC a 21 Experian PLC a 47 -

What's the Best Way to Get in Touch with My Banks?

INVESTIGATION | CONTACTING BANKS What’s the best way to get in touch with my bank? With more than 2,000 branches closing over the past decade, In part, banks and building societies have been cutting costs as a result of the financial has it become harder to access your bank, or do new contact crisis, or prioritising investment in technology methods compensate for the decline in face-to-face service? to get people banking in other ways. To better understand this shift in banking decade ago, if you wanted to pay in a The rapid rate of branch closure is a cause access, we surveyed 14 of the biggest current cheque or withdraw some money, all for concern for 57% of Which? members, account providers to find out how many A it would take was a short walk to your according to our survey of 1,356 people in branches they’d closed or opened between local high street bank branch. But today, the January 2014. However, with 89% of those we 2003 and 2013. We also asked about their same transaction at your nearest branch surveyed having access to online banking and branch network plans for 2014 and beyond. might require a 20-mile drive. 76% using telephone banking, it’s perhaps no HSBC closed the largest percentage – almost Given that the number of bank branches surprise that 42% believe that branch banking 30% were shut between the start of 2003 and on our high streets has almost halved since is becoming obsolete. But do the alternatives the end of 2013 – 458 branches in areas where the late 1980s, that’s hardly surprising. -

Portfolio of Investments

PORTFOLIO OF INVESTMENTS Variable Portfolio – Partners International Value Fund, September 30, 2020 (Unaudited) (Percentages represent value of investments compared to net assets) Investments in securities Common Stocks 97.9% Common Stocks (continued) Issuer Shares Value ($) Issuer Shares Value ($) Australia 4.2% UCB SA 3,232 367,070 AMP Ltd. 247,119 232,705 Total 13,350,657 Aurizon Holdings Ltd. 64,744 199,177 China 0.6% Australia & New Zealand Banking Group Ltd. 340,950 4,253,691 Baidu, Inc., ADR(a) 15,000 1,898,850 Bendigo & Adelaide Bank Ltd. 30,812 134,198 China Mobile Ltd. 658,000 4,223,890 BlueScope Steel Ltd. 132,090 1,217,053 Total 6,122,740 Boral Ltd. 177,752 587,387 Denmark 1.9% Challenger Ltd. 802,400 2,232,907 AP Moller - Maersk A/S, Class A 160 234,206 Cleanaway Waste Management Ltd. 273,032 412,273 AP Moller - Maersk A/S, Class B 3,945 6,236,577 Crown Resorts Ltd. 31,489 200,032 Carlsberg A/S, Class B 12,199 1,643,476 Fortescue Metals Group Ltd. 194,057 2,279,787 Danske Bank A/S(a) 35,892 485,479 Harvey Norman Holdings Ltd. 144,797 471,278 Demant A/S(a) 8,210 257,475 Incitec Pivot Ltd. 377,247 552,746 Drilling Co. of 1972 A/S (The)(a) 40,700 879,052 LendLease Group 485,961 3,882,083 DSV PANALPINA A/S 15,851 2,571,083 Macquarie Group Ltd. 65,800 5,703,825 Genmab A/S(a) 1,071 388,672 National Australia Bank Ltd. -

Annual Report and Accounts 2012 2012 8493 1 Report 2012 Report 2012 01 to 96 31/05/2012 14:41 Page 3

8493 1 Report 2012_Report 2012 01 to 96 31/05/2012 14:41 Page 2 The British Land Company DELIVERING PERFORMANCE PLC Annual Report and Accounts Annual Report and Accounts Annual Report and Accounts 2012 2012 8493 1 Report 2012_Report 2012 01 to 96 31/05/2012 14:41 Page 3 BRITISH LAND IS ONE OF EUROPE’S LARGEST REAL ESTATE INVESTMENT TRUSTS (REITs) AND OUR VISION IS TO BE THE BEST. We provide investors with access to a diverse range of quality property assets which we actively manage, finance and develop. We focus mainly on prime UK retail and London office properties and have a reputation for delivering industry-leading customer service. Our properties and our approach attracts high-quality occupiers committed to long leases, so we can provide shareholders with security of income as well as capital growth. Our size and substance demands a responsible approach to business. We believe achieving leading levels of efficiency and sustainability in our buildings helps drive our performance. This is also of increasing importance to occupiers and central to our aim to create environments in which businesses and local communities can thrive. Corporate responsibility information is integrated throughout our Annual Report and Accounts. This reflects how managing our environmental, economic and social impacts is central to the way we do business. It also provides readers with insights into the critical linkages in our thinking and activity, and greater clarity on the relationship between our financial and non-financial key performance indicators. Why go online? For more information Our corporate website contains detailed information You’ll find links throughout this Report, about the Company and is frequently updated as to guide you with further reading or relevant additional details become available. -

FTSE Factsheet

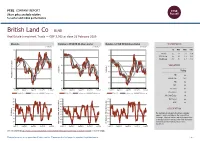

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Data as at: 21 February 2020 British Land Co BLND Real Estate Investment Trusts — GBP 5.562 at close 21 February 2020 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 21-Feb-2020 21-Feb-2020 21-Feb-2020 6.5 105 115 1D WTD MTD YTD Absolute -2.0 -5.4 0.3 -12.9 110 Rel.Sector -2.0 -4.0 -1.8 -12.3 100 Rel.Market -1.6 -5.3 -1.5 -11.6 6 105 95 VALUATION 100 5.5 Trailing 95 RelativePrice RelativePrice 90 PE -ve Absolute Price (local (local Absolute currency)Price 90 5 EV/EBITDA 28.1 85 85 PB 0.6 PCF 8.4 4.5 80 80 Div Yield 5.0 Feb-2019 May-2019 Aug-2019 Nov-2019 Feb-2020 Feb-2019 May-2019 Aug-2019 Nov-2019 Feb-2020 Feb-2019 May-2019 Aug-2019 Nov-2019 Feb-2020 Price/Sales 5.8 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.4 90 100 90 Div Payout -ve 80 90 80 ROE -ve 70 80 70 70 Index) Share Share Sector) Share - 60 - 60 60 DESCRIPTION 50 50 50 40 40 The Company is a property investment company 40 RSI RSI (Absolute) 30 30 based in London and listed on the London Stock 30 Exchange.