Payment Systems in Singapore

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FINANCE Offshore Finance.Pdf

This page intentionally left blank OFFSHORE FINANCE It is estimated that up to 60 per cent of the world’s money may be located oVshore, where half of all financial transactions are said to take place. Meanwhile, there is a perception that secrecy about oVshore is encouraged to obfuscate tax evasion and money laundering. Depending upon the criteria used to identify them, there are between forty and eighty oVshore finance centres spread around the world. The tax rules that apply in these jurisdictions are determined by the jurisdictions themselves and often are more benign than comparative rules that apply in the larger financial centres globally. This gives rise to potential for the development of tax mitigation strategies. McCann provides a detailed analysis of the global oVshore environment, outlining the extent of the information available and how that information might be used in assessing the quality of individual jurisdictions, as well as examining whether some of the perceptions about ‘OVshore’ are valid. He analyses the ongoing work of what have become known as the ‘standard setters’ – including the Financial Stability Forum, the Financial Action Task Force, the International Monetary Fund, the World Bank and the Organization for Economic Co-operation and Development. The book also oVers some suggestions as to what the future might hold for oVshore finance. HILTON Mc CANN was the Acting Chief Executive of the Financial Services Commission, Mauritius. He has held senior positions in the respective regulatory authorities in the Isle of Man, Malta and Mauritius. Having trained as a banker, he began his regulatory career supervising banks in the Isle of Man. -

Offshore Markets for the Domestic Currency: Monetary and Financial Stability Issues

BIS Working Papers No 320 Offshore markets for the domestic currency: monetary and financial stability issues by Dong He and Robert N McCauley Monetary and Economic Department September 2010 JEL classification: E51; E58; F33 Keywords: offshore markets; currency internationalisation; monetary stability; financial stability BIS Working Papers are written by members of the Monetary and Economic Department of the Bank for International Settlements, and from time to time by other economists, and are published by the Bank. The papers are on subjects of topical interest and are technical in character. The views expressed in them are those of their authors and not necessarily the views of the BIS. Copies of publications are available from: Bank for International Settlements Communications CH-4002 Basel, Switzerland E-mail: [email protected] Fax: +41 61 280 9100 and +41 61 280 8100 This publication is available on the BIS website (www.bis.org). © Bank for International Settlements 2010. All rights reserved. Brief excerpts may be reproduced or translated provided the source is stated. ISSN 1020-0959 (print) ISBN 1682-7678 (online) Abstract We show in this paper that offshore markets intermediate a large chunk of financial transactions in major reserve currencies such as the US dollar. We argue that, for emerging market economies that are interested in seeing some international use of their currencies, offshore markets can help to increase the recognition and acceptance of the currency while still allowing the authorities to retain a measure of control over the pace of capital account liberalisation. The development of offshore markets could pose risks to monetary and financial stability in the home economy which need to be prudently managed. -

Pa Perspectives on Nordic Financial Services

PA PERSPECTIVES ON NORDIC FINANCIAL SERVICES Autumn Edition 2017 CONTENTS The personal banking market 3 Interview with Jesper Nielsen, Head of Personal Banking at Danske bank Platform thinking 8 Why platform business models represent a double-edged sword for big banks What is a Neobank – really? 11 The term 'neobanking' gains increasing attention in the media – but what is a neobank? Is BankID positioned for the 14future? Interview with Jan Bjerved, CEO of the Norwegian identity scheme BankID The dance around the GAFA 16God Quarterly performance development 18 Latest trends in the Nordics Value map for financial institutions 21 Nordic Q2 2017 financial highlights 22 Factsheet 24 Contact us Chief editors and Nordic financial services experts Knut Erlend Vik Thomas Bjørnstad [email protected] [email protected] +47 913 61 525 +47 917 91 052 Nordic financial services experts Göran Engvall Magnus Krusberg [email protected] [email protected] +46 721 936 109 +46 721 936 110 Martin Tillisch Olaf Kjaer [email protected] [email protected] +45 409 94 642 +45 222 02 362 2 PA PERSPECTIVES ON NORDIC FINANCIAL SERVICES The personal BANKING MARKET We sat down with Jesper Nielsen, Head of Personal Banking at Danske Bank to hear his views on how the personal banking market is developing and what he forsees will be happening over the next few years. AUTHOR: REIAR NESS PA: To start with the personal banking market: losses are at an all time low. As interest rates rise, Banking has historically been a traditional industry, loss rates may change, and have to be watched. -

Interbank GIRO Is an Automated Payment Service Which Allows You to Make Monthly Payment to Your ICBC Credit Card Account from Your Designated Bank Account Directly

Interbank GIRO Frequently Asked Questions: 1. What is Interbank GIRO? Interbank GIRO is an automated payment service which allows you to make monthly payment to your ICBC Credit Card account from your designated bank account directly. The amount will be deducted from your designated bank account and paid to ICBC every month. All you need to do is to ensure that the designated bank account has sufficient funds every month. 2. What is the benefit of using Interbank GIRO? Interbank GIRO is a convenient, paperless and cashless payment method. It enables you to make hassle-free monthly payments to ICBC through your designated bank account. There are also no fees charged for the setup. 3. Are there any additional charges for signing up for Interbank GIRO? There are no fees charged for the setup of Interbank GIRO. 4. How can I apply for Interbank GIRO? Simply fill up the Interbank GIRO form, and submit to Credit Card Department. 5. Which banks can I use for Interbank GIRO? You can use any bank that supports Interbank GIRO. 6. How long is the Interbank GIRO application Processing Time? Interbank GIRO applications may take up to 60 days to process, including the processing time required by the deducting bank. We will notify you of your application status as soon as possible. 7. How do I submit the Interbank GIRO form to ICBC Credit Card Department? You can mail the duly signed Original Interbank GIRO form to ICBC Credit Card Department by using the Business Reply Service Envelope attached. Please do not fax the Interbank GIRO form or email the scanned copy of the Interbank GIRO form as the designated bank requires the original signature for verification. -

Gray Areas of Offshore Financial Centers

University of Tennessee, Knoxville TRACE: Tennessee Research and Creative Exchange Supervised Undergraduate Student Research Chancellor’s Honors Program Projects and Creative Work Spring 5-2008 Gray Areas of Offshore Financial Centers Matthew Benjamin Davis University of Tennessee - Knoxville Follow this and additional works at: https://trace.tennessee.edu/utk_chanhonoproj Recommended Citation Davis, Matthew Benjamin, "Gray Areas of Offshore Financial Centers" (2008). Chancellor’s Honors Program Projects. https://trace.tennessee.edu/utk_chanhonoproj/1167 This is brought to you for free and open access by the Supervised Undergraduate Student Research and Creative Work at TRACE: Tennessee Research and Creative Exchange. It has been accepted for inclusion in Chancellor’s Honors Program Projects by an authorized administrator of TRACE: Tennessee Research and Creative Exchange. For more information, please contact [email protected]. Gray Areas of Offshore Financial Centers Matthew Davis Chancellor's Honors Program Senior Project Introduction Offshore finance often brings to mind illegal activities such as money laundering and tax evasion. Over the years, these shady dealings have become associated with offshore banking due to its lax regulations and strict adherence to client secrecy. On the other hand, offshore financial centers can also be used for legitimate reasons such as setting up offshore hedge funds. Many motives drive the move of funds offshore and increase the activity of offshore financial centers. Some are completely legal, while others focus more on criminal activity. Often, the line between these legal and illegal activities is a very thin one. Specific regulations cannot be made to cover every single new situation, and taxpayers are forced to make decisions about how to interpret the law. -

Building a Customer-Centric Digital Bank in Singapore: It Takes an Ecosystem

White Paper Digital Banking EQUINIX AND KAPRONASIA BUILDING A CUSTOMER-CENTRIC DIGITAL BANK IN SINGAPORE: IT TAKES AN ECOSYSTEM Contents The dawn of digital banking in the Lion City Defining a value proposition . 2 No digital bank, in the purest sense of the term, Digital banking in Singapore amid COVID-19 . 4 currently exists in Singapore. While there are many fintechs, most provide only digital financial services The digital banking opportunity: that do not require a banking license: digital wallet retail and corporate . 5 services, cross-border payments and various virtual- asset-focused services. A digital bank (also known Key success factors for digital banks . 7 as a “neobank” or “virtual bank”) differs in that it is licensed to both accept customer deposits and issue 1. Digital agility to support a better loans, whether to retail customers, corporate customers customer experience. .7 or both. Singapore’s financial regulator, the Monetary 2. Favorable cost structure. .8 Authority of Singapore (MAS) plans to release five digital bank licenses in total and will announce the 3. Optimizing security .............................8 successful licensees in the second half of 2020. The licensed digital banks will likely then launch in mid-2021. Conclusion: The ecosystem opportunity . 10 While many less-developed Southeast Asian economies are leveraging digital banks to focus on financial inclusion, the role of digital banks in Singapore will be slightly different and focused on driving innovation. Bringing together traditional financial services firms, fintechs, other tech companies and even telecoms Singapore will become one of the firms, digital banks could act as a catalyst for financial focal points of Asia’s digital banking innovation in Singapore and help the city-state maintain evolution when the city-state awards its competitive advantage as a regional fintech hub. -

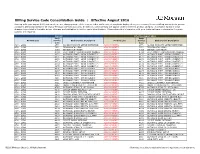

Billing Service Code Consolidation Guide | Effective August 2016

Billing Service Code Consolidation Guide | Effective August 2016 Starting with your August 2016 statement, we are changing some of the service codes and service descriptions displayed on your Treasury Services Billing statement to provide consistent billing standards for all of your Treasury Services accounts. In addition, some services will appear under a different product category. A complete listing of these changes is provided in the table below. Changes are highlighted in red for easier identification. Please share this information with your technical team to determine if system updates are required. Current Effective August 2016 Bank Bank Product Line Service Bank Service Description Product Line Service Bank Service Description Code Code ACH - GIRO 2770 ACHDD MANDATE SETUP(INITIATOR) ACH PAYMENTS 2770 ACHDD MANDATE SETUP(INITIATOR) ACH - GIRO 3971 ZENGIN ACH (LOW) ACH PAYMENTS 3971 ZENGIN ACH (LOW) ACH - GIRO 4093 ZENGIN ACH (HIGH) ACH PAYMENTS 4093 ZENGIN ACH (HIGH) ACH - GIRO 4094 ELECTRONIC TRANSMISSION CHARGE ACH PAYMENTS 4094 ELECTRONIC TRANSMISSION CHARGE ACH - GIRO 4170 OUTWARD PYMT - GIRO (URGENT) 1 ACH PAYMENTS 4170 OUTWARD PYMT - GIRO (URGENT) 1 ACH - GIRO 4171 OUTWARD PYMT - GIRO (URGENT) 2 ACH PAYMENTS 4171 OUTWARD PYMT - GIRO (URGENT) 2 ACH - GIRO 4172 OUTWARD PYMT - GIRO (URGENT) 3 ACH PAYMENTS 4172 OUTWARD PYMT - GIRO (URGENT) 3 ACH - GIRO 4173 OUTWARD PYMT - GIRO (URGENT) 4 ACH PAYMENTS 4173 OUTWARD PYMT - GIRO (URGENT) 4 ACH - GIRO 4174 OUTWARD PYMT - GIRO (URGENT) 5 ACH PAYMENTS 4174 OUTWARD PYMT - GIRO (URGENT) -

Payment Services Guide

CitiDirect® Online Banking Payments Services Guide March 2004 Proprietary and Confidential These materials are proprietary and confidential to Citibank, N.A., and are intended for the exclusive use of CitiDirect ® Online Banking customers. The foregoing statement shall appear on all copies of these materials made by you in whatever form and by whatever means, electronic or mechanical, including photocopying or in any information storage system. In addition, no copy of these materials shall be disclosed to third parties without express written authorization of Citibank, N.A. Table of Contents Overview .......................................................................................................................................1 Payments Services....................................................................................................................1 Creating Service Requests From Transaction Lookup..............................................................2 Creating Service Requests From Transaction Details ..............................................................9 Modifying Service Requests....................................................................................................14 Authorizing or Deleting Service Requests...............................................................................16 Viewing Service Request Transactions...................................................................................18 Disclaimer ...................................................................................................................................20 -

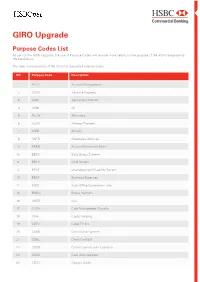

GIRO Upgrade Purpose Codes List

GIRO Upgrade Purpose Codes List As part of the GIRO Upgrade, the use of Purpose Codes will provide more details on the purpose of the ACH transaction to the beneficiary. The table below consists of the full list of supported purpose codes. SN Purpose Code Description 1 ACCT Account Management 2 ADVA Advance Payment 3 AGRT Agricultural Transfer 4 AIRB Air 5 ALLW Allowance 6 ALMY Alimony Payment 7 ANNI Annuity 8 ANTS Anesthesia Services 9 AREN Account Receivable Entry 10 BBSC Baby Bonus Scheme 11 BECH Child Benefit 12 BENE Unemployment Disability Benefit 13 BEXP Business Expenses 14 BOCE Back Office Conversion Entry 15 BONU Bonus Payment 16 BUSB Bus 17 CASH Cash Management Transfer 18 CBFF Capital Building 19 CBTV Cable TV Bill 20 CCRD Credit Card Payment 21 CDBL Credit Card Bill 22 CDCB Credit Payment with Cashback 23 CDCD Cash Disbursement 24 CDOC Original Credit SN Purpose Code Description 25 CDQC Quasi cash 26 CFEE Cancellation Fee 27 CHAR Charity Payment 28 CLPR Car Loan Principal Repayment 29 CMDT Commodity Transfer 30 COLL Collection Payment 31 COMC Commericial Payment 32 COMM Commission 33 COMT Consumer Third Party Consolidate Payment 34 COST Costs 35 CPKC Carpark Charges 36 CPYR Copyright 37 CSDB Cash Disbursement 38 CSLP Company Social Loan Payment To Bank 39 CVCF Convalescent Care facility 40 DBTC Debit Collection Payment 41 DCRD Debit Card Payment 42 DEPT Deposit 43 DERI Derivatives 44 DIVD Dividend 45 DMEQ Durable Medical Equipment 46 DNTS Dental Services 47 EDUC Education 48 ELEC Electricity Bill 49 ENRG Energies 50 ESTX Estate -

THE AML JARGON-BUSTER Your Guide to Anti-Money Laundering Definitions

THE AML JARGON-BUSTER Your guide to Anti-Money Laundering definitions TERM DEFINITION TERM DEFINITION AML See Anti-Money Laundering Enhanced Due An enhanced form of customer due Diligence (EDD) diligence (CDD) that must be adopted Anti-Money The systems and controls that regulated when the firm has ascertained that the Laundering (AML) firms are required to put in place in customer poses a higher risk of money order to prevent, detect and report laundering. It typically requires the money laundering. collection of additional documentation, or further verification checks. Anonymous An anonymous account is one for which Account the financial institution holds no records FATF See Financial Action Task Force concerning the identity of the account holder. Most jurisdictions now prohibit Financial Action An inter-governmental organisation the use of anonymous accounts Task Force (FATF) founded by the G7 in 1989 to develop although numerous ‘anonymous’ a global set of standards to combat accounts and facilities are still offered money laundering. FATF is based in via the Internet. Paris, France and the latest version of its 40 recommendations were published Beneficial Owner The person who ultimately owns in February 2012. They focus on the (BO) an asset and on whom AML checks importance of taking a risk-based need to be carried out. On occasions, approach to combatting money particularly with offshore entities, the laundering and terrorist financing. identity of the beneficial owner may not be disclosed in the public domain. Financial The Financial Action Task Force Sufficient KYC checks will not be Intelligence Unit recommends that each country should deemed to have been carried out if the (FIU) establish a financial intelligence unit identity of the beneficial owner(s) is not (FIU) – a national central authority to established, and then verified as per the receive, analyse and act upon suspicious risk-based approach. -

Global Financial Services Regulatory Guide

Global Financial Services Regulatory Guide Baker McKenzie’s Global Financial Services Regulatory Guide Baker McKenzie’s Global Financial Services Regulatory Guide Table of Contents Introduction .......................................................................................... 1 Argentina .............................................................................................. 3 Australia ............................................................................................. 10 Austria ................................................................................................ 22 Azerbaijan .......................................................................................... 34 Belgium .............................................................................................. 40 Brazil .................................................................................................. 52 Canada ................................................................................................ 64 Chile ................................................................................................... 74 People’s Republic of China ................................................................ 78 Colombia ............................................................................................ 85 Czech Republic ................................................................................... 96 France ............................................................................................... 108 Germany -

Offshore Banking and the Prospects for the Ghanaian Economy

GHAN F A O K N 7 A B 5 9 1 EST. OFFSHORE BANKING AND THE PROSPECTS FOR THE GHANAIAN ECONOMY RESEARCH DEPARTMENT BANK OF GHANA OCTOBER 2008 The Sector Study reports are prepared by the Research Department of Bank of Ghana for the deliberations of the Bank’s Board of Directors. The reports are subsequently made available as public information. This Study Report was prepared under the general direction of Dr. Ernest Addison. Primary contributors were Dr. Johnson Asiama and Ibrahim Abdulai. Further information may be obtained from: The Head Research Department Bank of Ghana P. O. Box GP 2674 Accra, Ghana. Tel: 233-21-666902-8 ISBN: 0855-658X TabLE of Contents 1.0 IntrodUction 1 1.1 History and Size 2 2.0 OVerVieW of Offshore FinanciaL Centres 4 2.1 Definitional Issues and Uses of Offshore Financial Centres 4 2.2 The Potential Risks from Offshore Operations and Country Experiences 7 3.0 FinanciaL SerVices Centre And Offshore Banking in Ghana 11 3.1 Background 11 3.2 Prospects and Benefits to the Ghanaian Economy 12 3.3 Channel of Influence between Offshore Banks and Domestic Banking Institutions 14 4.0 RegULation of Offshore Banks in Ghana 16 4.1 Why regulate 16 4.2 The Banking (Amendment) Act, 2007 (Act 738) and offshore banking 16 5.0 ConcLUsion and POLicy Recommendations 18 AppendiX 19 References 20 1.0 IntrodUction One of the key developments in the world economy during the last few decades has been the growing international mobility of capital. An element in this process has been the growth of offshore finance.