A Practitioner's Guide to Cluster-Robust Inference

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Parable of the Tenants Matthew 21:33-43

Festival Update TheD St.u Michael/St.Bois Catherine Rom Labora Dayn FestivalCat hash beeno lcanceledic Fduea toi thet Coronah C Virus.ommunities The planning process for this event is delayed and large group gatherings are discouraged through the better part of the summer. Our hope is that next winter circumstances will be much more favorable for moving forward with a Festival in September, 2021. Our thanks to those who were part of the startup of the event and we hope we are able to count on your support next year! Pennsylvania Charitable Trusts The Parable of the Tenants Matthew 21:33-43 PARISH OFFICES SUNDAY MASS SCHEDULE Mailing Address Faith Family Friends St. Catherine of Siena 118 S. State St. 118 S. State St. DuBois, PA 15801 Mass of Anticipation: 4:30 p.m. Hours: 8 a.m. - 3 p.m., M-T Sunday Mass: 10 a.m. Phone: 814-371-8556 Daily Mass at 7 a.m., M-F Fax: 814-371-0592 St. Michael the Archangel Parish Email: 15 Robinson St. St. Catherine Sunday Mass: 9 a.m. [email protected] Daily Mass: M-F 8 a.m. St. Michael (Please check bulletin for any changes) [email protected] A Moms’ gathering will take Parish Website: place on Tuesday, RECONCILIATION www.stcathstmikedubois.org October 6, at St. Catherine’s St. Catherine - By appointment only. McGivney Hall from St. Michael - Wednesday: 7:15-7:45 a.m. Faith Formation: 814-371-4082 9 - 10:30 a.m. Anytime by appointment. Classes at DCC from Sept-May 11:30-12:45 See page 3 for details. -

Livability Court Records 1/1/1997 to 8/31/2021

Livability Court Records 1/1/1997 to 8/31/2021 Last First Middle Case Charge Disposition Disposition Date Judge 133 Cannon St Llc Rep JohnCompany Q Florence U43958 Minimum Standards For Vacant StructuresGuilty 8/13/18 Molony 148 St Phillips St Assoc.Company U32949 Improper Disposal of Garbage/Trash Guilty- Residential 10/17/11 Molony 18 Felix Llc Rep David BevonCompany U34794 Building Permits; Plat and Plans RequiredGuilty 8/13/18 Mendelsohn 258 Coming Street InvestmentCompany Llc Rep Donald Mitchum U42944 Public Nuisances Prohibited Guilty 12/18/17 Molony 276 King Street Llc C/O CompanyDiversified Corporate Services Int'l U45118 STR Failure to List Permit Number Guilty 2/25/19 Molony 60 And 60 1/2 Cannon St,Company Llc U33971 Improper Disposal of Garbage/Trash Guilty- Residential 8/29/11 Molony 60 Bull St Llc U31469 Improper Disposal of Garbage/Trash Guilty- Residential 8/29/11 Molony 70 Ashe St. Llc C/O StefanieCompany Lynn Huffer U45433 STR Failure to List Permit Number N/A 5/6/19 Molony 70 Ashe Street Llc C/O CompanyCobb Dill And Hammett U45425 STR Failure to List Permit Number N/A 5/6/19 Molony 78 Smith St. Llc C/O HarrisonCompany Malpass U45427 STR Failure to List Permit Number Guilty 3/25/19 Molony A Lkyon Art And Antiques U18167 Fail To Follow Putout Practices Guilty 1/22/04 Molony Aaron's Deli Rep Chad WalkesCompany U31773 False Alarms Guilty 9/14/16 Molony Abbott Harriet Caroline U79107 Loud & Unnecessary Noise Guilty 8/23/10 Molony Abdo David W U32943 Improper Disposal of Garbage/Trash Guilty- Residential 8/29/11 Molony Abdo David W U37109 Public Nuisances Prohibited Guilty 2/11/14 Pending Abkairian Sabina U41995 1st Offense - Failing to wear face coveringGuilty or mask. -

In the Lands of the Romanovs: an Annotated Bibliography of First-Hand English-Language Accounts of the Russian Empire

ANTHONY CROSS In the Lands of the Romanovs An Annotated Bibliography of First-hand English-language Accounts of The Russian Empire (1613-1917) OpenBook Publishers To access digital resources including: blog posts videos online appendices and to purchase copies of this book in: hardback paperback ebook editions Go to: https://www.openbookpublishers.com/product/268 Open Book Publishers is a non-profit independent initiative. We rely on sales and donations to continue publishing high-quality academic works. In the Lands of the Romanovs An Annotated Bibliography of First-hand English-language Accounts of the Russian Empire (1613-1917) Anthony Cross http://www.openbookpublishers.com © 2014 Anthony Cross The text of this book is licensed under a Creative Commons Attribution 4.0 International license (CC BY 4.0). This license allows you to share, copy, distribute and transmit the text; to adapt it and to make commercial use of it providing that attribution is made to the author (but not in any way that suggests that he endorses you or your use of the work). Attribution should include the following information: Cross, Anthony, In the Land of the Romanovs: An Annotated Bibliography of First-hand English-language Accounts of the Russian Empire (1613-1917), Cambridge, UK: Open Book Publishers, 2014. http://dx.doi.org/10.11647/ OBP.0042 Please see the list of illustrations for attribution relating to individual images. Every effort has been made to identify and contact copyright holders and any omissions or errors will be corrected if notification is made to the publisher. As for the rights of the images from Wikimedia Commons, please refer to the Wikimedia website (for each image, the link to the relevant page can be found in the list of illustrations). -

First Honors Is Awarded at the End of Each Semester for Students Who Have Achieved an Average of 4.0 Or Above

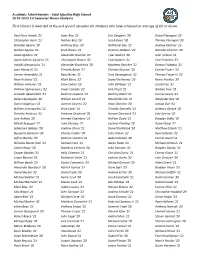

Academic Achievements – Saint Ignatius High School 2019-2020 1st Semester Honor Students First Honors is awarded at the end of each semester for students who have achieved an average of 4.0 or above. Paul Abou Haidar '22 Isaac Brej '21 Erik Daugenti '20 Daniel Flanagan '23 Christopher Aerni '22 Nathan Brej '20 Jacob Davis '20 Thomas Flanagan '20 Branden Agnew '20 Anthony Brey '20 Nathaniel Day '21 Andrew Fletcher '22 Nathan Agnew '23 Sean Brown '21 Dominic DeBlasis '22 Nicholas Fletcher '20 Jared Agoston '22 Alexander Bruncak '22 Tyler Dedrick '20 John Foliano '21 Aaron Aldrich Aguilera '23 Christopher Bruner '22 Evan Defloor '21 Cole Frabotta '23 Vassilis Alexopoulos '21 Alexander Brunkholz '20 Matthew Deucher '22 Damon Frabotta '22 Juan Alonso III '22 Timothy Bulan '21 Thomas Deucher '20 Connor Francz '20 Connor Amendola '21 Ryan Burke '21 Gino Devengencie '22 Thomas Fraser III '22 Ryan Anthony '21 Mark Burns '22 Daniel DeVenney '20 Henry Frawley '20 William Antonius '22 Evan Calton '23 John DiFilippo '21 Jacob Free '21 Andrew Apanasewicz '22 Javier Calzado '22 Jack Ditzel '21 Nathan Free '23 Aristotle Apostolakis '21 Dominic Caparso '21 Zachary Ditzel '22 Connor Geary '21 Robert Applegate '20 William Carroll '21 Maximilian Dix '21 Alexander Gee '20 Daniel Argalious '22 Carmen Caserio '22 Brian Donelon '20 Joshua Gee '23 William Armsworthy '22 Brice Cerar '21 Timothy Donnelly '21 Anthony Gerace '20 Timothy Atkinson '22 Anthony Chalhoub '20 Samuel Dornback '21 Kyle Gerrity '20 Jack Auletta '20 Emmett Chambers '22 William Doyle '21 Brayden -

Etapa 9 – Amostra

Amostra Instituto Cidade de Deus Etapa 9 – Amostra Editora Cidade de Deus FICHA CATALOGRÁFICA Instituto Cidade Deus Coleção Hypomoné: Etapa 9 / Instituto Cidade de Deus – São Carlos: Editora Cidade de Deus, 2019. 1. Material Didático 2. Religião Católica 3. Educação Católica I. Instituto Cidade de Deus II. Título III. Coleção. CDD – 200.71 Todos os direitos reservados. Proibida toda e qualquer reprodução desta edição por qualquer meio ou forma, seja ela eletrônica ou mecânica, fotocópia, gravação ou qualquer outro meio de reprodução, sem permissão expressa do Instituto Cidade de Deus Sobre a capa SANTO AGOSTINHO DE HIPONA, DOUTOR DA IGREJA (28 de agosto) Nasceu em Tagaste (África) no ano354. Depois de uma juventude perturbada, quer intelectualmente quer moralmente, converteu-se à fé e foi batizado em Milão por Santo Ambrósio no ano 387. Voltou à sua terra e aí levou uma vida de grande ascetismo. Eleito bispo de Hipona, durante trinta e quatro anos foi perfeito modelo do seu rebanho e deu-lhe uma sólida formação cristã por meio de numerosos sermões e escritos, com os quais combateu fortemente os erros do seu tempo e ilustrou sabiamente a fé católica. “Pai por excelência de todos os Padres da Igreja, Doutor da graça, monge, pastor, teólogo, autor de uma obra monumental e escritor de gênio, Agostinho permanece o símbolo vivo do convertido, não cessando de influenciar o espírito e o imaginário da civilização Ocidental”. Morreu no ano 430. Santo Agostinho, rogai por nós! 1 Sumário Estudo Sagrado .............................................................................................................................. -

Stoney Road out of Eden: the Struggle to Recover Insurance For

Scholarly Commons @ UNLV Boyd Law Scholarly Works Faculty Scholarship 2012 Stoney Road Out of Eden: The Struggle to Recover Insurance for Armenian Genocide Deaths and Its Implications for the Future of State Authority, Contract Rights, and Human Rights Jeffrey W. Stempel University of Nevada, Las Vegas -- William S. Boyd School of Law Sarig Armenian David McClure University of Nevada, Las Vegas -- William S. Boyd School of Law, [email protected] Follow this and additional works at: https://scholars.law.unlv.edu/facpub Part of the Contracts Commons, Human Rights Law Commons, Insurance Law Commons, Law and Politics Commons, National Security Law Commons, and the President/Executive Department Commons Recommended Citation Stempel, Jeffrey W.; Armenian, Sarig; and McClure, David, "Stoney Road Out of Eden: The Struggle to Recover Insurance for Armenian Genocide Deaths and Its Implications for the Future of State Authority, Contract Rights, and Human Rights" (2012). Scholarly Works. 851. https://scholars.law.unlv.edu/facpub/851 This Article is brought to you by the Scholarly Commons @ UNLV Boyd Law, an institutional repository administered by the Wiener-Rogers Law Library at the William S. Boyd School of Law. For more information, please contact [email protected]. STONEY ROAD OUT OF EDEN: THE STRUGGLE TO RECOVER INSURANCE FOR ARMENIAN GENOCIDE DEATHS AND ITS IMPLICATIONS FOR THE FUTURE OF STATE AUTHORITY, CONTRACT RIGHTS, AND HUMAN RIGHTS Je:jrev' W. Stempel Saris' ArInenian Davi' McClure* Intro d uctio n .................................................... 3 I. The Long Road to the Genocide Insurance Litigation ...... 7 A. The Millet System of Non-Geographic Ethno-Religious Administrative Autonomy ........................... -

Academic All-America All-Time List

Academic All-America All-Time List Year Sport Name Team Position Abilene Christian University 1963 Football Jack Griggs ‐‐‐ LB 1970 Football Jim Lindsey 1 QB 1973 Football Don Harrison 2 OT Football Greg Stirman 2 OE 1974 Football Don Harrison 2 OT Football Gregg Stirman 1 E 1975 Baseball Bill Whitaker ‐‐‐ ‐‐‐ Football Don Harrison 2 T Football Greg Stirman 2 E 1976 Football Bill Curbo 1 T 1977 Football Bill Curbo 1 T 1978 Football Kelly Kent 2 RB 1982 Football Grant Feasel 2 C 1984 Football Dan Remsberg 2 T Football Paul Wells 2 DL 1985 Football Paul Wells 2 DL 1986 Women's At‐Large Camille Coates HM Track & Field Women's Basketball Claudia Schleyer 1 F 1987 Football Bill Clayton 1 DL 1988 Football Bill Clayton 1 DL 1989 Football Bill Clayton 1 DL Football Sean Grady 2 WR Women's At‐Large Grady Bruce 3 Golf Women's At‐Large Donna Sykes 3 Tennis Women's Basketball Sheryl Johnson 1 G 1990 Football Sean Grady 1 WR Men's At‐Large Wendell Edwards 2 Track & Field 1991 Men's At‐Large Larry Bryan 1 Golf Men's At‐Large Wendell Edwards 1 Track & Field Women's At‐Large Candi Evans 3 Track & Field 1992 Women's At‐Large Candi Evans 1 Track & Field Women's Volleyball Cathe Crow 2 ‐‐‐ 1993 Baseball Bryan Frazier 3 UT Men's At‐Large Brian Amos 2 Track & Field Men's At‐Large Robby Scott 2 Tennis 1994 Men's At‐Large Robby Scott 1 Tennis Women's At‐Large Kim Bartee 1 Track & Field Women's At‐Large Keri Whitehead 3 Tennis 1995 Men's At‐Large John Cole 1 Tennis Men's At‐Large Darin Newhouse 3 Golf Men's At‐Large Robby Scott #1Tennis Women's At‐Large Kim -

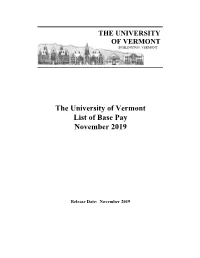

The University of Vermont List of Base Pay November 2019

THE UNIVERSITY OF VERMONT BURLINGTON, VERMONT The University of Vermont List of Base Pay November 2019 Release Date: November 2019 University of Vermont List of Base Pay, November 2019 Name Primary Job Title Base Pay Abaied,Jamie L. Associate Professor $67,200 Abair,Shirley Sam Office/Prgm Support Generalist $28,219 Abajian,Michael John Lecturer $53,612 Abbott,Lori M. Office/Prgm Support Generalist $45,766 Abdallah,Rany Talal Assistant Professor (COM) $30,000 Abdul-Karim,Yasmeen Assistant Professor (COM) $30,000 Abernathy,Karen E Assistant Professor (COM) $30,000 Abernathy,Mac Wilson Assistant Professor (COM) $30,000 Abiti,Pearl D. Early Childhood Teaching Ast $29,981 Abnet,Kevin R Associate Professor (COM) $19,800 Aboushousha,Reem M Lab Research Technician $40,641 Abu Alfa,Amer K Assistant Professor (COM) $40,500 AbuJaish,Wasef Associate Professor (COM) $35,000 Achenbach,Thomas Max Professor $63,050 Ackil,Daniel J. Assistant Professor (COM) $35,000 Acostamadiedo,Jose Maria Clinical Prac Phys-CVPH (COM) $30,000 Acquisto,Joseph T. Professor $118,256 Adair,Elizabeth Carol Associate Professor $83,786 Adam,Michael Anthony Facilities Repairperson $39,229 Adam,Wilfred Carl Maintenance Unit Supervisor $47,840 Adamczak,Christina L Office/Prgm Support Generalist $37,541 Adams,Alec L Business Oprtns Administrator $104,699 Adams,Clifford D. Custodial Maintenance Spec Sr $37,128 Adams,Elizabeth Jean Clinical Professor $96,794 Adams,Jane Lydia Researcher/Analyst $67,426 Adams,Zoe S Research Specialist $47,198 Adamson,Christine S.C. Lab Research Technician $49,140 Aden,Lule O Student Srvcs Professional $33,000 Aden,Mumina Hassan Custodial Maintenance Worker $29,390 Adeniyi,Aderonke Oluponle Assistant Professor (COM) $51,610 Ades,Philip A. -

OCTOBER TERM 1996 Reference Index Contents

JNL96$IND1Ð08-20-99 15:29:27 JNLINDPGT MILES OCTOBER TERM 1996 Reference Index Contents: Page Statistics ....................................................................................... II General .......................................................................................... III Appeals ......................................................................................... III Arguments ................................................................................... III Attorneys ...................................................................................... IV Briefs ............................................................................................. IV Certiorari ..................................................................................... IV Costs .............................................................................................. V Judgments and Opinions ........................................................... V Original Cases ............................................................................. V Parties ........................................................................................... V Rehearings ................................................................................... VI Rules ............................................................................................. VI Stays .............................................................................................. VI Conclusion ................................................................................... -

Share Their Story

SHARE JOY Walkthe with Francis ANNUAL REPORT 2014-2015 “Charity is born of the call of a God who continues to knock on our door, the door of all people, to invite us to love, to compassion, to service of one another. — Pope Francis, St. Patrick’s Parish 2 Dear Friends, It is a pleasure to present to you this annual report for Catholic Charities of the Archdiocese of Washington which highlights the efforts of this ministry to walk with Pope Francis in faith and charity on our pilgrim journey. The stories found in this report remind all of us that through the love we share, the Gospel faith still has the power to transform people’s lives. When our Holy Father met with some of the clients, staff and volunteers of Catholic Charities during his visit to Washington this year, he stressed that “Jesus wanted to show solidarity with every person. He wanted everyone to experience his companionship, his help, his love.” Thanks to your compassionate support, through Catholic Charities, our sisters and brothers in need are able to encounter that consolation and love of Christ every day. As a visible sign of Christ’s presence in the world today, this faith-filled ministry meets a myriad of material and spiritual needs in its 65 programs, including: housing, job training, legal aid, immigration and refugee assistance, mental health treatment, medical and dental care, life-long care for those with developmental disabilities, and food assistance, such as Saint Maria’s Meals, which served the lunch that was blessed during Pope Francis’ visit. -

Livro Do Animador

LIVRO DO ANIMADOR ANO 1 LIVRO DO ANIMADOR – ANO 1 Itinerário de preparação para a JMJ Lisboa 2023 Ficha técnica Nada obsta 01 de novembro de 2020, Solenidade de Todos os Santos D. Joaquim Mendes, Bispo Auxiliar do Patriarcado de Lisboa Textos bíblicos CEP, Bíblia, Os Quatro Evangelhos e os Salmos, 2019 Edição litúrgica dos textos bíblicos Elaboração Direção de Pastoral e Eventos Centrais da Jornada Mundial da Juventude Lisboa 2023 Ilustrações Mário Linhares Fotografias Vatican Media Design Gráfico Douglas Azevedo Leila Ferreira Fundação Salesianos Propriedade Fundação JMJ Lisboa 2023 Equipa de redação Alice Neto (Paróquia de Alcochete, Diocese de Setúbal); Pe. André Batista (Secretariado Diocesano da Pastoral Juvenil, Diocese de Leiria – Fátima); Pe. Bruno Dinis (Missionários Passionistas); Carlota Cardoso (Paróquia de S. Julião do Tojal,Patriarcado de Lisboa); Júlio Torres (Paróquia de Vialonga, Patriarcado de Lisboa); Liliana Maia (Leigos Missionários Combonianos); Ir. Linda Vieira (Filhas de Maria Auxiliadora, Salesianas); Ir. Lisete da Natividade (Irmãs Doroteias); Pe. Luís Rafael Azevedo (Departamento Diocesano da Pastoral Juvenil, Diocese de Lamego); Maria Lopes (Paróquia da Póvoa de Santa Iria, Patriarcado de Lisboa); Ir. Marta Mendes (Aliança de Santa Maria †); Pedro Feliciano (Serviço da Juventude, Patriarcado de Lisboa); Romana Esteves (Paróquia de Olhalvo, Patriarcado de Lisboa); Rui Lourenço Teixeira (Corpo Nacional de Escutas); Ir. Sandra Bartolomeu (Servas de Nossa Senhora de Fátima); Pe. Tiago Neto (Patriarcado de Lisboa). Revisão teológica D. Vitorino José Pereira Soares (Bispo Auxiliar da Diocese do Porto) Cón. Luís Miguel Figueiredo Rodrigues (Arquidiocese de Braga) Pe. Mário José Rodrigues de Sousa (Diocese do Algarve) RISE UP | LIVRO DO ANIMADOR 3 UM ENCONTRO QUE NOS APRESSA Saúdo estas catequeses preparatórias da JMJ 2023. -

Guido Schäffer

QUINTA-FEIRA • 07 DE DEZEMBRO DE 2017 Diário do Minho Este suplemento faz parte da edição n.º 31605 de 07 de Dezembro de 2017, do jornal Diário do Minho, não podendo ser vendido separadamente. O "santo" surfista obra e vida de guido schäffer reportagem p. 4-5 2 INTERNACIONAL IGREJA VIVA “AIGREJA mudança UNIVERSAL mais urgente na Igreja é a renovação do clero” à vista de todos. É importante e que têm atende várias outras semelhantes, mas relacionadas José María Castillo urgente actualizar a Liturgia, o paróquias, que podem estar distantes com o mesmo problema de fundo. teólogo espanhol Direito Canónico, a vida religiosa, a umas das outras. Esse problema, que (no seu âmbito) Teologia, a participação dos leigos na E para isso deve haver – e em breve afecta o mundo inteiro, não pode gestão das paróquias, nas dioceses, – alguma solução. Essa mudança depender do que pensam ou é na cúria romana e muitas outras está a ser preparada? Em que vai conveniente a alguns homens em questões que estão aí e que todos consistir? Não seria conveniente Roma e “redondezas”. Teremos logo É evidente que o Papa Francisco vêem. Por mais que haja gente informar a Igreja sobre o que se está uma resposta? E se parece indiscreto, está a mudar, em coisas muito relutante em ver o que é impossível a fazer para resolver esse problema? inclusive, perguntar isso e contá-lo sérias, o exercício do papado. Todos esconder. Não exagero. Nem invento É uma questão que diz respeito a aos outros, então será preciso pensar vêem isso.