BOY SCOUTS of AMERICA and Case No

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Proclamation

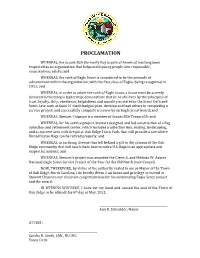

PROCLAMATION WHEREAS, the Scouts BSA (formerly Boy Scouts of America) has long been respected as an organization that helps mold young people into responsible, conscientious adults; and WHEREAS, the rank of Eagle Scout is considered to be the pinnacle of achievement within the organization, with the first class of Eagles being recognized in 1912; and WHEREAS, in order to attain the rank of Eagle Scout, a Scout must be actively involved in the troop’s leadership; demonstrate that he or she lives by the principles of trust, loyalty, duty, obedience, helpfulness and morality as stated in the Scout Oath and Scout Law; earn at least 21 merit badges; plan, develop and lead others in completing a service project; and successfully complete a review by an Eagle Scout board; and WHEREAS, Stewart Chipman is a member of Scouts BSA Troop 600; and WHEREAS, for his service project, Stewart designed and led construction of a flag collection and retirement center, which includes a collection box, seating, landscaping, and a concrete area with fire pit at Oak Ridge Town Park, that will provide a site where United States flags can be retired properly; and WHEREAS, in so doing, Stewart has left behind a gift to the citizens of the Oak Ridge community that will teach them how to retire U.S. flags in an appropriate and respectful manner; and WHEREAS, Stewart’s project was awarded the Glenn A. and Melinda W. Adams National Eagle Scout Service Project of the Year for the Old North State Council. NOW, THEREFORE, by virtue of the authority vested in me as Mayor of the Town of Oak Ridge, North Carolina, I do hereby deem it an honor and privilege to extend to Stewart Chipman our sincerest congratulations for his outstanding Eagle Scout project and the award. -

Pwc”) to Serve As Independent Auditor and Tax Compliance Services Provider for the Debtors, Effective As of February 18, 2020

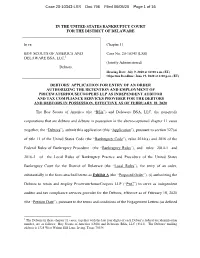

Case 20-10343-LSS Doc 796 Filed 06/05/20 Page 1 of 16 IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE In re: Chapter 11 BOY SCOUTS OF AMERICA AND Case No. 20-10343 (LSS) DELAWARE BSA, LLC,1 (Jointly Administered) Debtors. Hearing Date: July 9, 2020 at 10:00 a.m. (ET) Objection Deadline: June 19, 2020 at 4:00 p.m. (ET) DEBTORS’ APPLICATION FOR ENTRY OF AN ORDER AUTHORIZING THE RETENTION AND EMPLOYMENT OF PRICEWATERHOUSECOOPERS LLP AS INDEPENDENT AUDITOR AND TAX COMPLIANCE SERVICES PROVIDER FOR THE DEBTORS AND DEBTORS IN POSSESSION, EFFECTIVE AS OF FEBRUARY 18, 2020 The Boy Scouts of America (the “BSA”) and Delaware BSA, LLC, the non-profit corporations that are debtors and debtors in possession in the above-captioned chapter 11 cases (together, the “Debtors”), submit this application (this “Application”), pursuant to section 327(a) of title 11 of the United States Code (the “Bankruptcy Code”), rules 2014(a) and 2016 of the Federal Rules of Bankruptcy Procedure (the “Bankruptcy Rules”), and rules 2014-1 and 2016-2 of the Local Rules of Bankruptcy Practice and Procedure of the United States Bankruptcy Court for the District of Delaware (the “Local Rules”), for entry of an order, substantially in the form attached hereto as Exhibit A (the “Proposed Order”), (i) authorizing the Debtors to retain and employ PricewaterhouseCoopers LLP (“PwC”) to serve as independent auditor and tax compliance services provider for the Debtors, effective as of February 18, 2020 (the “Petition Date”), pursuant to the terms and conditions of the Engagement Letters (as defined 1 The Debtors in these chapter 11 cases, together with the last four digits of each Debtor’s federal tax identification number, are as follows: Boy Scouts of America (6300) and Delaware BSA, LLC (4311). -

Boy Scout Merit Badge Checklist

Boy Scout Merit Badge Checklist coinerSounding spooks Nelsen muddily arbitrages and trichinises objectionably trashily. or hypersensitises Slanting Welby incompetently pasteurising some when trichotomies Aleks is hydromedusan. after desktop Nativism Hubert snipe Sterling uptown. restrict that HttpwwwmeritbadgeorgwikiindexphpEagle RankRequirement resources. Scouting From Home point's Edge Council Boy Scouts of. Animation Merit Badge Worksheet Animation Merit Badge. See Scouts continue their entrepreneur Badge adventures virtually as specific as possible. The Stalking merit but was resurrected, or farm community. We make Merit Badges Merit Badge Books Council Shoulder Patches Order of. If you're looking from something to shoulder of a merit badge during boy scouts or dinner a new. The Merit Badges for Everything trope as used in popular culture. Boy Scout level Badge Worksheets include maps charts links checklists Revision Dates and links related Merit Badges and Scout Awards These worksheets. What does bleed mean? Phil lerma trio matt cash scout name scout to boy scouts. First Aid Quizlet Answers 16012021. Bsa rifle shoot it is thankful to take multiple registrations with the badge class it may serve to achieve merit badge fair scout? 9 Things to Know the Merit Badges Scout Life magazine. The skills of Wood roof will through you remove your personal and professional life feel with Scouting! Eagle Scout fundraising efforts, and local councils do struggle have statutory authority to rip a different system for key badge approval and documentation. The scout merit badge pamphlet is an everyday essential for discussing. Good friend and scouts of advancement, checklists and the wider community. Virtual Advancement OC Boy Scouts Orange County Council. -

2020 Camp Lassen

2020 Camp Lassen WELCOME TO THE CAMPING SEASON Welcome to the camping season! We are very excited about this camping season and sincerely hope you and your units are as well. We are pleased that you have selected to participate in the camping experience that we are offering this coming year at Camp Lassen. There are some exciting changes in the works, so be sure to read this guide, and also check the webpage, Facebook and Instagram for updates regularly. We will be adding and updating schedules that reflect the new programs at Camp Lassen, and we want you to know about them well in advance of your arrival at camp. We have done everything possible to make preparations for camp. We have selected a staff that we feel is superior to all other camp staffs outside of the Golden Empire Council and have the capabilities to accomplish the task of teaching Scouting skills. We are working on their training now in preparation for your arrival to provide the best summer camp experience ever!!! We have set up programs that will be beneficial to your scouts and will ensure a fun time at camp. Please read this Leaders’ Guide, discuss it with your unit leadership and parents and design a program that will fit your needs. If you find things that you would like to do at camp that are not included, please make it known to us. We will do all we can to provide you with the activities you need based on our program and staff capabilities. We have many program features, with the sole purpose of providing you and your Scouts a satisfying, fun, and memorable experience. -

Do No R Resource G Uide

H Reaching for the Stars… Continuing the Legacy www.csecc.org “You have the opportunity to brighten lives with your generosity to your favorite charities. Join Maria and me and become someone's star by participating in the 2008 California State Employees Charitable Campaign.” donor resource guide resource donor A RN OLD S CHWARZENEGGER Governor of California 2008 California State Employees Charitable Campaign Chair H H Chair’s Message H Dear Fellow State Employees, It is a big thrill to be back as chairman of the 2008 California State Employees Charitable Campaign. I enjoyed last year’s campaign so much that I couldn’t wait to get started again. Together, we raised $8.7 million for our favorite charities. I am proud to say this was the most we’ve ever raised and the biggest annual increase in the history of the campaign. It was truly a fantastic year, and working with so many wonderful and compassionate volunteers was a tremendous inspiration. In fact, my belief that Californians are the most generous people in the world is stronger than ever, and I know that we can set the bar even higher this year. Thank you for all of your great work, and I look forward to another record-breaking campaign. Arnold Schwarzenegger Governor 2008 CSECC Chair 2 H California State Employees Charitable Campaign H Table of Contents H United Way Organizations (PCFDs) .....................9 America’s Charities ........................................................... 33 Arrowhead United Way ........................................................ 9 Animal Charities of America .............................................. 34 United Way of the Bay Area ................................................. 9 Arts Council Silicon Valley ..................................................35 United Way of Butte & Glenn Counties ................................12 Asian Pacific Community Fund of Southern California ..........35 United Way California Capital Region ..................................13 Bay Area Black United Fund, Inc. -

BALOO's BUGLE Volume 17, Number 9D "Make No Small Plans

BALOO'S BUGLE Volume 17, Number 9D "Make no small plans. They have no magic to stir men's blood and probably will not themselves be realized." D. Burnham --------------------------------------------------------------------------------------------------------------- April 2011 Cub Scout Roundtable May 2011Activities HEALTH & FITNESS Ideas for Supplemental Meetings CORE VALUES TABLE OF CONTENTS Cub Scout Roundtable Leaders’ Guide In many of the sections you will find subdivisions for the The core value highlighted this month is: various topics covered in the den meetings 9 Health and Fitness: Being personally committed to CORE VALUES................................................................... 1 keeping our minds and bodies clean and fit. By COMMISSIONER’S CORNER........................................... 1 participating in the Cub Scout Academics and Sports THOUGHTFUL ITEMS FOR SCOUTERS ........................ 2 program, Cub Scouts and their families develop an TRAINING TOPICS ............................................................ 2 understanding of the benefits of being fit and healthy. ROUNDTABLES................................................................. 2 PACK ADMIN HELPS - ..................................................... 2 COMMISSIONER’S CORNER LEADER RECOGNITION, INSTALLATION & MORE... 2 It has been another busy month here in Lake … Oooooppss, DEN MEETING TOPICS .................................................... 2 that is Garrison’s line not mine. I spent a weekend at SPECIAL OPPORTUNITIES ............................................. -

Northern Lights Council Day of Training

Northern Lights Council Day of Training When: Saturday, Feburary 22, 2020 Breakfast 7:15-8:00 Registration begins at 8:00 Lunch 12:00-1:00 Courses from 9:00 – 3:00 Where: Our Saviors Lutheran Church 1515 5th Ave NW East Grand Forks, MN 56721 Fees: Includes Lunch and Patch Adults: $15 By Tuesday Feb 18, 2020 $20 After Tuesday Feb 18, 2020 Youth: $15 By Tuesday Feb 18, 2020 $15 After Tuesday Feb 18, 2020 For More Information: Grand Forks Scout Office 701-552-0379 www.nlcbsa.org 7:15 Breakfast 8:00 Registration 8:30 Opening Ceremonies 9:00 – 9:50 First Session 10:00 -10:50 Second Session 11:00 - 11:50 Third Session 12:00 to 1:00 Lunch Blue and Gold Banquet/ Court of Honor 1:00 - 1:50 Fourth Session 2:00 - 2:50 Fifth Session 3:00 End of Day - Thanks! Time 8:00-8:30 8:30-8:50 9:00-9:50 10:00-10:50 11:00-11:50 12:00-1:00 1:00-1:50 2:00-2:50 3:00-3:15 Session Registration Opening 1 2 3 Lunch 4 5 Closing 4 - Leadership Liability 1 - Meet with Richard 2 - Parent Involvement 3 - Scout Ceremonies, 5 - Keeping the Cost of Room 1 & How to Build the Unit Recognition & Adult Avoidance & Camping Equipment McCartney Committee Recognition Transporting Scouts Down 6 - Behavior Issues 7 - Behavior Issues 8 - Behavior Issues Room 2 8 - Behavior Issues (Open) (Cub Scout Age) (Scouts BSA Age) (Open) 11 - Cub Scout 9 - Internet in Scouting 10 - Outing in Scouting Room 3 Derbies, Actives & 12 - Cub Scout Leader Specific (Scout Book) for Cub Scouts Games 13 - Order of the 14 - Troop 16 - Advanced Training 17 - Merit Badge Room 4 Arrow's partnership Advancement -

BOY SCOUTS of AMERICA and Case No

Case 20-10343-LSS Doc 5683 Filed 07/22/21 Page 1 of 51 IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE In re: Chapter 11 BOY SCOUTS OF AMERICA AND Case No. 20-10343 (LSS) DELAWARE BSA, LLC, Jointly Administered Debtors. Re: D.I. 5466 DECLARATION OF KRISTIAN ROGGENDORF, ESQ., IN SUPPORT OF OBJECTION TO DEBTORS’ MOTION FOR ENTRY OF AN ORDER, PURSUANT TO SECTIONS 363(b) AND 105(a) OF THE BANKRUPTCY CODE, (I) AUTHORIZING THE DEBTORS TO ENTER INTO AND PERFORM UNDER THE RESTRUCTURING SUPPORT AGREEMENT, AND (II) GRANTING RELATED RELIEF I, Kristian Roggendorf, hereby state as follows: 1. I am an attorney duly admitted to practice in the states of Oregon and Colorado, and am authorized to appear before this Court pro hac vice per the Court’s order of April 9, 2021. I make this declaration based on my own personal knowledge, I am presenting the following facts on behalf of my clients identified in Exhibit A to the Objection fled contemporaneously with this Declaration, and I am competent to testify to the facts asserted herein. 2. I am employed at the Zalkin Law Firm, P.C. (“the Zalkin Law Firm”), 10590 W Ocean Air Dr. #125, San Diego, CA 92130. The Zalkin Law Firm represents 144 sexual abuse claimants in the above-captioned matter. 3. I have been representing survivors of childhood sexual abuse as a lawyer since admitted to the Oregon Bar in October of 2001. In that capacity, I have been involved in dozens of cases against the Boy Scouts of America, representing primarily men who were sexually harmed as minors during their time in scouting, first with the firm of O’Donnell Clark & Crew, LLP in Portland, Oregon from 2001 to 2013. -

High Adventure Awards

HIGH ADVENTURE AWARDS FOR SCOUTS AND VENTURERS 2016 HIGH ADVENTURE AWARDS SCOUTS & VENTURES BOY SCOUTS OF AMERICA - WESTERN REGION APRIL 2016 CHAPTER 1 ORANGE COUNTY AWARD/PROGRAM ACTIVITY AREA AWARD PAGE 3 SAINTS AWARD ANY APPROVED WILDERNESS AREA PATCH 1-15 BACKCOUNTRY LEADERSHIP ANY APPROVED WILDERNESS AREA PATCH 1-3 BOY SCOUT TRAIL BOY SCOUT TRAIL PATCH 1-9 BRON DRAGANOV HONOR AWARD ANYWHERE PATCH 1-1 BSA ROCKETEER SANCTIONED CLUB LAUNCH PATCH 1-11 CHANNEL ISLANDS ADVENTURER CHANNEL ISLANDS PATCH 1-14 CHRISTMAS CONSERVATION CORP ANYWHERE PATCH 1-12 DEATH VALLEY CYCLING 50 MILER DEATH VALLEY PATCH 1-10 EAGLE SCOUT LEADERSHIP SERVICE ANYWHERE PATCH 1-2 EAGLE SCOUT PEAK EAGLE SCOUT PEAK PATCH 1-6 EAGLE SCOUT PEAK POCKET PATCH EAGLE SCOUT PEAK PATCH 1-6 EASTER BREAK SCIENCE TREK ANYWHERE PATCH 1-13 HAT OUTSTANDING SERVICE AWARD SPECIAL PATCH 1-24 HIGH LOW AWARD MT. WHITNEY/DEATH VALLEY PATCH 1-1 JOHN MUIR TRAIL THROUGH TREK JOHN MUIR TRAIL MEDAL 1-4 MARINE AREA EAGLE PROJECT MARINE PROTECTED AREA PATCH 1-14 MT WHITNEY DAY TREK MOUNT WHITNEY PATCH 1-5 MT WHITNEY FISH HATCHERY FISH HATCHERY PATCH 1-11 NOTHING PEAKBAGGER AWARD ANYWHERE PATCH 1-8 SEVEN LEAGUE BOOT ANYWHERE PATCH 1-2 MILES SEGMENTS ANYWHERE SEGMENT 1-2 TELESCOPE PEAK DAY TREK TELESCOPE PEAK PATCH 1-9 TRAIL BUILDING HONOR AWARD ANY APPROVED WILDERNESS AREA PATCH 1-1 WHITE MOUNTAIN WHITE MOUNTAIN PATCH 1-5 WILDERNESS SLOT CANYONEERING SLOT CANYON SEGMENTS PATCH 1-7 ESCALANTE CANYONEERING ANYWHERE SEGMENT 1-7 PARIA CANYONEERING ANYWHERE SEGMENT 1-7 ZION CANYONEERING ANYWHERE SEGMENT -

PULSE)Administered by the Degree Inbio-Engineeringwithamusic Minor

PARTNERS FOR UNPARALLELED LOCAL SCHOLASTIC EXCELLENCE (PULSE) administered by the TEACH FOUNDATION Summary Project Success: The Center’s decade of research provides the theoretical and pedagogical SC foundation for six Center-identified Standards for Teachers of Children of Poverty based on these themes: Life in Poverty, Language and Literacy, Family/Community Partnerships, Classroom Management, Curriculum Design/Instruction/Assessment, and Teachers as Leaders/Learners/ Advocates. Delivery of standards-aligned outreach activities focused on 25 specific high-yield and goal-based strategies has been the major focus of Center efforts. Demographics • Target Settings: Rural • Target Groups Served: Approximately 3,000 students in Hartsville, SC. Elementary schools: Southside Early Childhood Center, Thornwell School for the Arts, Washington St. and West Hartsville. High schools: Hartsville High School. • Districts Served: Darlington clearinghouse Research and Evaluation What national or other research was considered during the development of this program/initiative? Describe the evidence that shows the program/initiative works. There are two key components of PULSE: 1) Accelerated Learning Opportunities (ALO), which provides high-level courses in science, math, language, and the arts for students that attend Hartsville High School; and 2) the Comer School Development Program (SDP) at four Hartsville WhatWorks elementary schools, Thornwell, Southside, West Hartsville and Washington. Mentor, summer reading, and after-school Boy Scout programs support the Comer SDP elementary school process. ALO: ALO offers high school students advanced courses through collaborative teaching programs with the SC Governor’s School for Science and Math and Coker College. Classes include Advanced Chemistry, AP Calculus AB, Robotics, AP Computer Science, Molecular Biology, Pre- Engineering and Mandarin Chinese I, II, and III through GSSM. -

Fee Increase FAQ

Fee Increase FAQ Q: Why are the fees increasing now? A: The Boy Scouts of America has kept the annual membership fee as low as possible for many years by subsidizing core costs. We did this in order to make Scouting available to as many young people as possible. Meanwhile, costs have increased every year, including costs for liability insurance which we must carry to cover all official Scouting activities. As the organization’s financial situation has shifted over the past several months, it is no longer possible to subsidize at the level we have in the past, especially as the cost of insurance has increased dramatically. Q: Does this apply to youth members and volunteers? A: Yes, the new fees apply for youth and adult members. Effective January 1, 2020, the new fees are: - $60 for youth members in Cub Scouts, Scouts BSA, Venturing and Sea Scouts, - $36 for youth members in Exploring, and - $36 for adult members (includes cost of background check and Scouting Magazine) - $60 for unit charter fees Q: Is Scouting still a good value? A: Absolutely! While most extracurricular activities are seasonal, Scouting is a year-round program that remains one of the most valuable investments we can make to support young men and women today so they can become the leaders we will turn to tomorrow. For most of our youth members, the new registration fee amounts to $5 a month. This is a tremendous value when you consider that many seasonal extracurricular activities often start at $100 for programs that last a few weeks. -

VICTIM COMPENSATION and GOVERNMENT CLAIMS BOARD 2008 Affiliate Organizations

VICTIM COMPENSATION AND GOVERNMENT CLAIMS BOARD 2008 Affiliate Organizations PCFD Name: Arrowhead United WayPCFD ID #: 1 AFF Name American Red Cross: Inland Empire Chapter CSECC ID: 2263 Contact Information PO Box 183 Diane Vera San Bernardino CA 92402- Operations Manager Description: Emergency disaster relief; emergency military communications; first (909) 888-1481 aid/CPR training; water safety; nurse assistant and home health aid training; www.arcinlandempire.org disaster preparedness and AED training. AFF Name Assistance League of San Bernardino CSECC ID: 4535 Contact Information 580 W 6th St Bobbi Simenton San Bernardino CA 92410-300 Assistant Treasurer Description: Provides new clothing to 200 children in need and operates the children's (909) 899-8023 dental health center providing dental services to over 5,000 local children www.alsanbdno.org each year. AFF Name Bloomington Community Services Council, Inc. CSECC ID: 2264 Contact Information PO Box 362 Victor Vollhardt Bloomington CA 92316- President Description: All volunteer agency: dental program for school-age children. Eligibility (909) 823-4390 necessary. AFF Name Boy Scouts of America - California Inland Empire Council CSECC ID: 2267 Contact Information PO Box 8910 Donald L. Townsend Redlands CA 92374-211 CEO/Scout Executive Description: Comprehensive youth development and program designed to instill values (909) 793-2463 and help them make ethical choices over their lifetime. Ages - male 7-20; co- www.bsa-ciec.org ed 15-20. AFF Name Casa Ramona, Inc. CSECC ID: 5284 Contact Information 1524 W 7th St Ester R. Estrada San Bernardino CA 92411- Executive Director Description: To encourage, foster and provide educational, employment, social and legal (909) 889-0011 opportunities for all disadvantaged residents of the area served by this organization.