Pwc”) to Serve As Independent Auditor and Tax Compliance Services Provider for the Debtors, Effective As of February 18, 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

In the United States Bankruptcy Court for the Eastern District of Virginia Richmond Division

Case 20-32299-KLP Doc 304 Filed 06/09/20 Entered 06/09/20 21:09:06 Desc Main Document Page 1 of 128 Steven J. Reisman (pro hac vice admission pending) Donald C. Schultz (VSB No. 30531) Marc B. Roitman (pro hac vice admission pending) W. Ryan Snow (VSB No. 47423) KATTEN MUCHIN ROSENMAN LLP CRENSHAW, WARE & MARTIN, PLC 575 Madison Avenue 150 West Main Street, Suite 1500 New York, New York 10022 Norfolk, Virginia 23510 Telephone: (212) 940-8800 Telephone: (757) 623-3000 Facsimile: (212) 940-8776 Facsimile: (757) 623-5735 Geoffrey M. King (pro hac vice admission pending) KATTEN MUCHIN ROSENMAN LLP 525 West Monroe Street Chicago, Illinois 60661 Telephone: (312) 902-5200 Facsimile: (312) 902-1061 Proposed Co-Counsel to the Special Committee of the Board of Intelsat Envision Holdings LLC IN THE UNITED STATES BANKRUPTCY COURT FOR THE EASTERN DISTRICT OF VIRGINIA RICHMOND DIVISION ) In re: ) Chapter 11 ) INTELSAT S.A., et al.,1 ) Case No. 20-32299 (KLP) ) Debtors. ) (Jointly Administered) ) APPLICATION OF INTELSAT ENVISION HOLDINGS LLC FOR ENTRY OF AN ORDER AUTHORIZING THE EMPLOYMENT AND RETENTION OF KATTEN MUCHIN ROSENMAN LLP AS SPECIAL COUNSEL PURSUANT TO SECTIONS 327(e), 328(a), AND 1107(b) OF THE BANKRUPTCY CODE EFFECTIVE AS OF MAY 13, 2020 Intelsat Envision Holdings LLC (“Intelsat Envision” or the “Debtor”), one of the above- captioned debtors and debtors in possession (the “Debtors”), respectfully states as follows in support of this application (this “Application”):2 1 Due to the large number of Debtors in these chapter 11 cases, for which joint administration has been granted, a complete list of the Debtor entities and the last four digits of their federal tax identification numbers is not provided herein. -

Central Region Directory 2009—2010

CENTRAL REGION DIRECTORY 2009—2010 OFFICERS Regional President Regional Commissioner Regional Director Stephen B. King Brian P. Williams Jeffrie A. Herrmann King Capital, LLC Partner Central Region, BSA Founder, Partner Kahn, Dees, Donovan & Kahn, LLP 1325 W. Walnut Hill Lane 3508 N. Edgewood Dr. PO Box 3646 PO Box 152079 Janesville, WI 53545 Evansville, IN 47735-3646 Irvine, TX 75015-2079 Phone: 608.755.8162 Phone: 812.423.3183 Phone: Fax: 608.755.8163 Fax: 812.423.6066 [email protected] [email protected] [email protected] Vice President of Vice President Vice President Vice President Strategic Initiatives Finance & Endowment Outdoor Adventure Council Solutions Joseph T. Koch Ronald H. Yocum Steven McGowan Charles T. Walneck COO 9587 Palaestrum Rd. Steptoe & Johnson, PLLC Chairman, President & CEO Fellowes, Inc. Williamsburg, MI 49690 PO Box 1588 SubCon Manufacturing Corp. 1789 Norwood Ave. Phone: 231.267.9905 Chase Tower 8th Fl. 201 Berg St. Itasca, IL 60143-1095 Fax: 231.267.9905 Charleston, WV 25326 Algonquin, IL 60102 Phone: 630.671.8053 [email protected] Phone: 304.353.8114 Phone: 847.658.6525 Fax: 630.893.7426 (June-Oct.) Fax: 304.626.4701 Fax: 847.658.1981 [email protected] [email protected] steven.mcgowan [email protected] (Nov.-May) @steptoe-johnson.com Vice President Vice President Nominating Committee Appeals Committee Marketing LFL/Exploring Chairman Chairman Craig Fenneman Brad Haddock R. Ray Wood George F. Francis III President & CEO Haddock Law Office, LLC 1610 Shaw Woods Dr. Southern Bells, Inc. 19333 Greenwald Dr. 3500 North Rock Road, Building 1100 Rockford, IL 61107 5864 S. -

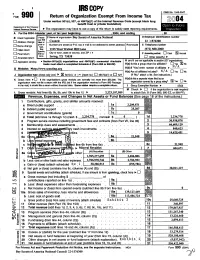

Srs Copy 2004

SRS COPY OMB No . 1545-0047 Fo,m 990 Return of Organization Exempt From Income Tax Under section 501(c), 52;x, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust w private foundation) 2004 Department of the Treasury Internal Revenue Samoa t The organization may have to use a copy of this return to satisfy state reporting requirements . A For the 2004 calendar year, or tax year beginning , 2004, and ending , 20 D Employer B Check if applicable : Please C Name of organization Boy Stoats of America National Identification number use :RS Address change label or Council 22 .1576300 print or Number and sweet (or P.O. box it mail is not delivered to street address) Room/suite E Telephone number D Name change D Initial return ~ 1325 West Walnut Hill Lane (972) 580-2000 Specific , city or town, state or count and ZIP + 4 0 Final return in~NC- y N~ F Accounting method: El Cash N Accrual tans. Irving, TX 75038 D Amended return D Other (specify) t H and 1 are not applicable to section 527 orga, nizafions. D Application pending " Section 501(e)(3) organizations end 4947(ax1) nonexempt charitable trusts must attach a completed Schedule A (Form 990 or 990-Q). H(a) IS this a group return for affiliates? El Y ~ No N ~A G Website: H(b) If 'Yes ; enter number of affiliates ~ , _ . .. .. H(c) Are all affiliates included? N / A E ]Yes E]No J Organization type (check only one) t IR 501(c) ( 3 ) ,4 (insert no .) 0 4947(a)(1) or [1 527 (If 'No,' attach a list. -

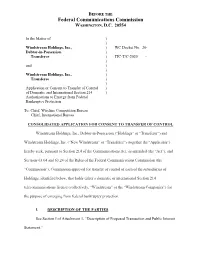

Federal Communications Commission WASHINGTON, D.C

BEFORE THE Federal Communications Commission WASHINGTON, D.C. 20554 In the Matter of ) ) Windstream Holdings, Inc., ) WC Docket No. 20-__ Debtor-in-Possession. ) Transferor ) ITC-T/C-2020____-_____ ) and ) ) Windstream Holdings, Inc., ) Transferee ) ) Application or Consent to Transfer of Control ) of Domestic and International Section 214 ) Authorizations to Emerge from Federal Bankruptcy Protection To: Chief, Wireline Competition Bureau Chief, International Bureau CONSOLIDATED APPLICATION FOR CONSENT TO TRANSFER OF CONTROL Windstream Holdings, Inc., Debtor-in-Possession (“Holdings” or “Transferor”) and Windstream Holdings, Inc. (“New Windstream” or “Transferee”) (together the “Applicants”) hereby seek, pursuant to Section 214 of the Communications Act, as amended (the “Act”), and Sections 63.04 and 63.24 of the Rules of the Federal Communications Commission (the “Commission”), Commission approval for transfer of control of each of the subsidiaries of Holdings, identified below, that holds either a domestic or international Section 214 telecommunications license (collectively, “Windstream” or the “Windstream Companies”) for the purpose of emerging from federal bankruptcy protection. I. DESCRIPTION OF THE PARTIES See Section I of Attachment 1, “Description of Proposed Transaction and Public Interest Statement.” - 2 - II. DESCRIPTION OF THE TRANSACTION See Section I.E. of Attachment 1, “Description of Proposed Transaction and Public Interest Statement.” As described therein, the Applicants seek FCC permission to accomplish this transaction in two steps, allowing the Windstream Companies to emerge more quickly from bankruptcy protection at Step One, and deferring consideration of the proposed final ownership structure to Step Two. III. APPROVAL OF THE REQUESTED TRANSFER OF CONTROL WILL PROVIDE SUBSTANTIAL PUBLIC INTEREST BENEFITS WITH NO COMPETITIVE OR OTHER HARMS See Section II of Attachment 1, “Description of Proposed Transaction and Public Interest Statement.” IV. -

SECURITIES and EXCHANGE COMMISSION Washington, D.C. 20549 ______FORM 8-K ______

SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 ______________ FORM 8-K ______________ Current Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event reported): August 2, 2019 Charter Communications, Inc. CCO Holdings, LLC CCO Holdings Capital Corp. (Exact name of registrant as specified in its charter) Delaware (State or other jurisdiction of incorporation or organization) 001-33664 84-1496755 001-37789 86-1067239 333-112593-01 20-0257904 (Commission File Number) (I.R.S. Employer Identification Number) 400 Atlantic Street Stamford, Connecticut 06901 (Address of principal executive offices including zip code) (203) 905-7801 (Registrant’s telephone number, including area code) Not Applicable (Former name or former address, if changed since last report) Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions: Written communications pursuant Rule 425 under the Securities Act (17 CFR 230.425) Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol(s) Name of each exchange on which registered Class A Common Stock, $.001 Par Value CHTR NASDAQ Global Select Market Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter). -

July 28 Golf Course

26TH ANNUAL JAMAR - BSA GOLF CLASSIC ENGER PARK JULY 28 GOLF COURSE 1801 W SKYLINE PKWY SHOTGUN START DULUTH, MN 55806 HOLE IN ONE - CLOSEST TO THE PIN - SCOUT PUP TENT MONEY HOLE - LONGEST PUTT - TOP 3 TEAMS SNACK BAG - DINNER - PROGRAM All proceeds benefit the Voyageurs Area Council, BSA to support development of youth Scouting programs in northern Minnesota, northern Wisconsin, and Gogebic County in Michigan, and provide a $2500 scholarship to a Council Eagle Scout. JAMAR - BSA GOLF CLASSIC SPONSORSHIP OPPORTUNITIES EAGLE LEVEL STAR LEVEL CART SPONSOR $2500 (1 Available) DRIVING RANGE $750 (1 Available) One foursome team Business logo on driving range signage Business logo on all carts Business logo and link on website Business logo and link on website Business logo on level sponsorship banner Mentions in social media posts Business logo on level sponsorship banner PLAYER BAG SPONSOR $500 (3 Available) Business logo on all printed marketing materials Business logo on player recognition items Business logo and link on website 2 Available) MEAL SPONSOR $1500 ( Business logo on level sponsorship banner Business logo on meal signage Business logo and link on website HOLE SPONSOR $250 (18 Available) Mentions in social media posts Business logo on tee box sign Business logo on level sponsorship banner Business logo and link on website Business logo on all printed marketing materials Business logo on level sponsorship banner Opportunity to be present at tee box LIFE LEVEL FOURSOME TEAM $600 FLAG SPONSOR $1250 (1 Available) Greens fees, 2 carts, snack bags, dinner, Business logo on flags and 2 beverages per player. -

2007 Fall Popcorn Sales a Huge

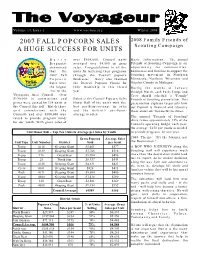

Volume 14, Issue 1 www.vac-bsa.org Winter 2008 2007 FALL POPCORN SALES 2008 Family Friends of Scouting Campaign A HUGE SUCCESS FOR UNITS Barry over $604,000, Council units Basic Information: The annual Bergquist averaged over $4,500 in gross Friends of Scouting Campaign is an announced sales. Congratulations to all the opportunity for communities, that the units for bettering their programs businesses and families to support the 2007 Fall through the Council popcorn Scouting movement in Northern Popcorn fundraiser. Barry also thanked Minnesota, Northern Wisconsin and Sales were the District Popcorn Chairs for Gogebic County in Michigan. the largest their leadership in this record During the months of January ever in the year. through March, each Pack, Troop, and Voyageurs Area Council. Over Crew should schedule a "Family" $190,000 in commissions and Below is the Council Popcorn Sales Friends of Scouting presentation. This prizes were earned by 134 units in Honor Roll of the unit’s with the presentation explains to parents how the Council this fall. Match those best per -Scout-average in sales our Council is financed and educates unit commissions with the and the district’s per-Scout- them about our wonderful facilities. Council’s and over $380,000 was average in sales: The annual "Friends of Scouting" raised to provide program funds drive raises approximately 15% of the for our youth. With gross sales of Council’s operating budget each year. On average, $150 per youth is needed Unit Honor Roll – Top Ten Units in Average per Sales by Youth to provide programs for one year. -

A Homemade Treat Goes Big Time Town Council

This Weekend FRIDAY 50% Chance of Snow MILL 38/25 SATURDAY 70% Chance of Snow 27/16 SUNDAY Clear 36/20 Inside this issue! carrborocitizen.com JANUARY 28, 2010 u LOCALLY OWNED AND OPERATED u VOLUME III VNO. XL I FREE Three years in, Carrboro High hits a winning stride BY BETH MECHUM Staff Writer An atmosphere of success has taken hold on the Carrboro High School cam- pus. The field hockey team now plays more competitively with both East Chapel Hill and Chapel Hill, the women’s golf team helped start a high school women’s golf league in the area and the men’s soccer team beat conference rival Cedar Ridge for the first time ever. Students, teachers and parents walked the halls and fields of Carrboro High School three years ago not knowing what was ahead. It was tough going in the be- ginning, and it’s still no easy ride. But with cohesion, camaraderie and a sense of community from all, things just keep get- ting better. Three years ago, in the school’s first year of operation, the football team couldn’t as much as sniff a win, even when at home Common catbriers occasionally display remarkable colors. on its brand-new field. Fortunately, there PHOTO BY GILES BLUNDEN weren’t many people in the stands to wit- ness those weekly beatings. A full women’s golf team was just a pie-in-the-sky dream for the few golf enthusiasts on campus. FLORA BY KEN MOORE There was no senior leadership on any team, because there were no seniors. -

During This Week You Will: NYLT Is

During this week you will: NYLT is presented by: • Learn the latest modern leadership skills • Make new friends • Learn about goal setting • Camp out • Learn problem solving techniques • Learn more about yourself • Cook outside • Learn conflict resolution • Have fun! • And much more! Voyageurs Area Council Boy Scouts of America The skills you will learn at NYLT are taught using modern corporate National Youth Leadership Training leadership skills that will help you 3877 Stebner Road wherever you are: home, school, work Hermantown, MN 55811 and, of course, Scouts! Phone: 218-729-5811 Fax: 218-729-6559 NYLT Scoutmaster: Mara Spaeth Email: [email protected] Phone: 218-966-7596 Camp Horace Johnson June 13-19, 2021 Be part of the most advanced leadership training for Scouts! REGISTER AT WWW.VAC-BSA.ORG or National Youth Leadership Training SUBMIT THIS APPLICATION NYLT is an exciting, action-packed program designed to provide all 13- to 17-year-old Name: ________________________________ youth members of the Boy Scouts of America Street Address: ________________________ with leadership skills and experiences they City: __________________________________ can use in their home units and in other State: __________________ Zip: __________ situations demanding leadership of self and Phone: ________________________________ others. Email: _________________________________ Unit/District: __________________________ A trained and dedicated staff of youth leaders Current Unit Position: ___________________ This intense six-day training course is held -

Jitasa Client Councils

Jitasa Client Councils Council Name City Start Date Council Name City Start Date Alabama-Florida Council Dothan, AL 5/27/2013 Mobile Area Council Mobile, AL 7/17/2012 Andrew Jackson Council Jackson, MS 3/1/2013 Mountain West Council Boise, ID 4/13/2020 Blue Mountain Council Kennewick, WA 7/23/2018 Mountaineer Area Council Fairmont, WV 10/1/2012 Blue Ridge Mountains Council Roanoke, VA 4/4/2014 Nevada Area Council Reno, NV 3/1/2018 Buckeye Council Canton, OH 10/30/2020 Northeast Illinois Council Highland Park, IL 7/15/2013 Buckskin Council Charleston, WV 3/15/2015 Northeast Georgia Council Jefferson, GA 8/1/2018 Buffalo Trail Council Midland, TX 10/18/2011 Northwest Georgia Council Rome, GA 4/21/2016 California Inland Empire Cncl Redlands, CA 9/26/2012 Northwest Texas Council Wichita Falls, TX 5/29/2015 Cape Cod & Islands Council Yarmouth Port, MA 3/18/2016 Norwela Council Shreveport, LA 5/9/2016 Catalina Council Tucson, AZ 10/14/2015 Occoneechee Council Raleigh, NC 5/1/2020 Central Georgia Council Macon, GA 12/1/2020 Old Hickory Council Winston-Salem, NC 8/27/2020 Chattahoochee Council Columbus, GA 7/1/2015 Orange County Council Santa Ana, CA 10/15/2018 Cherokee Area Council Chattanooga, TN 2/1/2021 Pacific Skyline Council Foster City, CA 10/19/2011 Chester County Council Exton,PA 6/15/2020 Palmetto Council Spartanburg, SC 8/1/2018 Chickasaw Council Memphis, TN 6/20/2014 Patriots’ Path Council Cedar Knolls, NJ 8/1/2019 Choctaw Area Council Meridian, MS 10/14/2013 Pennsylvania Dutch Council Lancaster, PA 7/1/2020 Coastal Georgia Council -

Time Travelers Camporee a Compilation of Resources

1 Time Travelers Camporee A Compilation of Resources Scouts, Ventures, Leaders & Parents…. This is a rather large file (over 80 pages). We have included a “Table of Contents” page to let you know the page numbers of each topic for quick reference. The purpose of this resources to aid the patrols, crews (& adults) in their selection of “Patrol Time Period” Themes. There are numerous amounts of valuable information that can be used to pinpoint a period of time or a specific theme /subject matter (or individual).Of course, ideas are endless, but we just hope that your unit can benefit from the resources below…… This file also goes along with the “Time Traveler” theme as it gives you all a look into a wide variety of subjects, people throughout history. The Scouts & Ventures could possibly use some of this information while working on some of their Think Tank entries. There are more events/topics that are not covered than covered in this file. However, due to time constraints & well, we had to get busy on the actual Camporee planning itself, we weren’t able to cover every event during time. Who knows ? You might just learn a thing or two ! 2 TIME TRAVELERS CAMPOREE PATROL & VENTURE CREW TIME PERIOD SELECTION “RESOURCES” Page Contents 4 Chronological Timeline of A Short History of Earth 5-17 World Timeline (1492- Present) 18 Pre-Historic Times 18 Fall of the Roman Empire/ Fall of Rome 18 Middle Ages (5th-15th Century) 19 The Renaissance (14-17th Century) 19 Industrial Revolution (1760-1820/1840) 19 The American Revolutionary War (1775-1783) 19 Rocky Mountain Rendezvous (1825-1840) 20 American Civil War (1861-1865) 20 The Great Depression (1929-1939) 20 History of Scouting Timeline 20-23 World Scouting (Feb. -

Charitable Solicitation Licensing Section Annual Report

Charitable Solicitation Licensing Section Annual Report July 1, 2006 through June 30, 2007 North Carolina Department of the Secretary of State Elaine F. Marshall, Secretary Charitable Solicitation Licensing Section P.O. Box 29622 Raleigh, NC 27626-0622 Phone: 888-830-4989 or 919-807-2214 Email: [email protected] www.sosnc.com 2007 Charitable Solicitation Licensing Annual Report North Carolina Department of the Secretary of State Table of Contents Introduction: Message from the Secretary Mission Statement and Contact Information Section One: Executive Summary of Professional Solicitor Activities 1A: Sorted By Charity or Sponsor Name 1B: Sorted By Solicitor Name Section Two: Charitable/Sponsor Organizations Current Registry Section Three: Exempt Organizations Registry Section Four: Professional Fundraisers Current Registry 4A: Fundraising Consultants Registry 4B: Solicitors Registry Section Five: Solicitors Contract Report Section Six: Charitable/Sponsor Organizations Audited Financial Statements Section Seven: Investigation Statistics Report Complaints with Violations Report Enforcement Actions Report Appendices: Appendix A: North Carolina General Statute 131F Appendix B: Charitable/Sponsor Organization Initial Application Appendix C: Fundraising Consultant Application Appendix D: Solicitor Application Appendix E: Enforcement Complaint Form and Instructions State of North Carolina Department of the Secretary of State Each December, the Department of the Secretary of State releases the Annual Report of the Charitable Solicitation Licensing Section. There is no better time of year than this season of giving to provide the public with the information included in this Report. Throughout my private and public life, I have been a strong supporter of charitable organizations. As this Report shows, I am certainly not alone in my charitable giving.