Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fifth International Congress of Chinese Mathematicians Part 1

AMS/IP Studies in Advanced Mathematics S.-T. Yau, Series Editor Fifth International Congress of Chinese Mathematicians Part 1 Lizhen Ji Yat Sun Poon Lo Yang Shing-Tung Yau Editors American Mathematical Society • International Press Fifth International Congress of Chinese Mathematicians https://doi.org/10.1090/amsip/051.1 AMS/IP Studies in Advanced Mathematics Volume 51, Part 1 Fifth International Congress of Chinese Mathematicians Lizhen Ji Yat Sun Poon Lo Yang Shing-Tung Yau Editors American Mathematical Society • International Press Shing-Tung Yau, General Editor 2000 Mathematics Subject Classification. Primary 05–XX, 08–XX, 11–XX, 14–XX, 22–XX, 35–XX, 37–XX, 53–XX, 58–XX, 62–XX, 65–XX, 20–XX, 30–XX, 80–XX, 83–XX, 90–XX. All photographs courtesy of International Press. Library of Congress Cataloging-in-Publication Data International Congress of Chinese Mathematicians (5th : 2010 : Beijing, China) p. cm. (AMS/IP studies in advanced mathematics ; v. 51) Includes bibliographical references. ISBN 978-0-8218-7555-1 (set : alk. paper)—ISBN 978-0-8218-7586-5 (pt. 1 : alk. paper)— ISBN 978-0-8218-7587-2 (pt. 2 : alk. paper) 1. Mathematics—Congresses. I. Ji, Lizhen, 1964– II. Title. III. Title: 5th International Congress of Chinese Mathematicians. QA1.I746 2010 510—dc23 2011048032 Copying and reprinting. Material in this book may be reproduced by any means for edu- cational and scientific purposes without fee or permission with the exception of reproduction by services that collect fees for delivery of documents and provided that the customary acknowledg- ment of the source is given. This consent does not extend to other kinds of copying for general distribution, for advertising or promotional purposes, or for resale. -

Discrepancies Between Zhang Tianyi and Dickens

This thesis has been submitted in fulfilment of the requirements for a postgraduate degree (e.g. PhD, MPhil, DClinPsychol) at the University of Edinburgh. Please note the following terms and conditions of use: This work is protected by copyright and other intellectual property rights, which are retained by the thesis author, unless otherwise stated. A copy can be downloaded for personal non-commercial research or study, without prior permission or charge. This thesis cannot be reproduced or quoted extensively from without first obtaining permission in writing from the author. The content must not be changed in any way or sold commercially in any format or medium without the formal permission of the author. When referring to this work, full bibliographic details including the author, title, awarding institution and date of the thesis must be given. Zhang Tianyi’s Selective Acceptance of Charles Dickens Chunxu Ge School of Languages, Literatures and Cultures Submitted for the Degree of Doctor of Philosophy June 2019 1 Abstract This research is a comparative study on the works of Charles Dickens (1812-1870) and Zhang Tianyi 張天翼 (1906-1985). The former was one of the greatest novelists of the Victorian era; the latter, a Left-wing writer in Republican China. The study analyses five short stories from Zhang’s corpus and compares his works with ten novles of Dickens. The study argues that Dickens is one among other writers that have parallels with Zhang, through the exploration of several aspects of their works. At the beginning of the twentieth century, Dickens’s novels were introduced to China by Lin Shu. -

UCLA Electronic Theses and Dissertations

UCLA UCLA Electronic Theses and Dissertations Title The Transformation in State and Elite Responses to Popular Religious Beliefs Permalink https://escholarship.org/uc/item/52v2q1k3 Author Kim, Hanshin Publication Date 2012 Peer reviewed|Thesis/dissertation eScholarship.org Powered by the California Digital Library University of California UNIVERSITY OF CALIFORNIA Los Angeles The Transformation in State and Elite Responses to Popular Religious Beliefs A dissertation submitted in partial satisfaction of the requirements for the degree Doctor of Philosophy in History by Hanshin Kim 2012 © Copyright by Hanshin Kim 2012 ABSTRACT OF THE DISSERTATION The Transformation in State and Elite Responses to Popular Religious Beliefs by Hanshin Kim Doctor of Philosophy in History University of California, Los Angeles, 2012 Professor Richard von Glahn, Chair My dissertation examines how the attitudes of states and literati toward the popular religious beliefs had been transformed during the period between the late Tang and Southern Song period. The previous researches concentrated on how the socio-economic and socio- psychological changes had caused the rapid growth of the popular religious cults since the Song dynasty period, and they presumed that the rapid increase of the state and literati involvement with the local cults just reflected the increasing significance of the popular religions. However, I argue that the previous presumption was only partially right. My research intends to demonstrate that the transformation in the state and literati response to the popular religious cults was iii attributed not only to the change of the popular religions but also to that of the socio-political environment around them. In Chapter Two, I argue that during the period between the late Tang and the Five Dynasties period the difference in the local policies between the northern five dynasties and southern regional regimes caused the disparity in their stances on the popular religious beliefs. -

Text and Its Cultural Interpretation

TEXT AND ITS CULTURAL INTERPRETATION I. Alimov MORE ABOUT SUN GUANG-XIAN AND BEI MENG SUO YAN1* There is very little information remaining about Sun “Generations [of the Song family] worked on the Guang-xian (孫光憲, 895?—968, second name land, but only Guang-xian began studying diligently Meng-wen 孟文, pen-name Baoguang-zi 葆光子); from a young age”, even his exact date of birth is not known [1]. His life- time came at the very end of the Tang rule, the period it is stated in Song dynastic history. Sun Guang-xian of the Five Dynasties and the first years of the Song was the first in his family who resolved to escape from dynasty. Information on where Sun came from is also poverty, and set his mind on science, book-learning, contradictory: well-known Song bibliophile Chen arts and achieved considerable results in these areas. Zheng-sun (陳振孫, 1190—1249) wrote in his bibliog- He followed the path of an official: he successfully raphy [2] that Sun Guang-xian was originally from passed the examinations and joined the public service Guiping in the region of Lingzhou (in the north-east and his first appointment the post of administrative part of what now is the Renshouxian district of assistant of his home region of Lingzhou [6]. The au- Sichuan province) [3], and the meagre biography of thor of “Springs and Autumns of the Ten Kingdoms”, Sun Guang-xian in Song dynastic history (j. 483) says Qing historian Wu Zhi-yi (吳志伊, second half of the same. Still, one of the most well-known works by 17th—first half of 18th century), says that it was at the him Bei meng suo yan (北夢瑣言, “Short Sayings from end of the rule of the Tang dynasty. -

The 5Th International Congress on Science and Technology of Ironmakin

The 5th International Congress on Science and Technology of Ironmakin (ICSTF09) October 20-22,2009 Shanghai, China Organized by The Chinese Society for Metals Proceedings of the 5th International Congress on the Science and Technology of Ironmaking Part B Blast Furnace Ironmaking Bl-1 Ironmaking Process Bl-1.01 Advancement and Thought of BF Iron-Making Technology in Baosteel ZHURen-liang andLI Yon-qing (Baoshan Iron & Steel Co Ltd) 537 B1 -1.02 Technological Reconstruction of Ansteel Ironmaking System Since "The Tenth Five-Year" SHANG Ce, WANG Qian, WANG Bao-hai and TANG Qing-hua (Angang Steel Co Ltd) 544 B1-1.03 Developments in Blast Furnace Ironmaking Chandan Barman Ray, Narayan Sengupta and Amitava Dasgupta (M.N. Dastur & Company (P) Ltd) 549 B1 -1.04 Progress in Technology of Vanadium-Bearing Titanomagnetite Smelting in Pangang FU Wei-guo andXIE Hong-en (Panzhihua Iron & Steel Research Institute) 554 Bl-1.05 Technical Advance of TISCO Ironmaking WANG Hong-bin and YAN Kui-hong (Taigang Stainless Steel Co Ltd) 560 B 1-1.06 The Mini Blast Furnace Flex Castro Jose A dilson (Federal Fluminense University) 5 64 B1-1.07 Progress of Iron-Making Technology for Special Ore in Baotou Steel WUHu-lin, SONG Guo-long andMAXiang (Baotou Steel Group Co) 569 Bl-1.08 Some of the Aspects Future of Blast Furnace Ironmaking The Process: Focusing on Low Cost Hot Metal Maarten Geerdes, Roman Vaynshteyn andReinoud van Laar (Danieli Corus BV) 575 B1 -1.09 Technique Index Analysis on Different Types of Blast Furnace DUANDong-ping and LIU Wen-quan (Chinese Academy -

Chinese (PDF 414.78

University of Leeds Classification of Books Chinese [A General] A-0.01 Periodicals A-0.02 Series A-0.03 Collections of essays, Festschriften, etc. A-0.04 Collections (cong-shu) A-0.06 Civilisation A-0.11 Sinology: sinologists A-0.13 Directories A-0.14 Chinese yearbooks (national) A-0.15 English yearbooks (national) A-0.16 Yearbooks (Taiwan) A-0.17 Yearbooks (regional) A-0.24 Names (personal and place) A-1 General encyclopaedias A-1.8 Encyclopaedic dictionaries - handbooks of general knowledge A-1.85 Trad general ‘Iei shu’ A-2 Catalogues (including library catalogues) A-2.8 Indexes and indexing A-3 Bibliography A-3.01 Bibliographies of periodicals A-3.1 General and national bibliographies A-3.2 Classification & subject division A-3.3 History of printing and book-making A-3.31 Conservation A-3.4 Publishing and journalism A-3.5 Censorship A-3.6 Book rarities: book collectors A-3.7 Lists, abstracts etc. of dissertations A-4 Libraries A-4.2 Librarianship A-4.5 Museums A-4.7 Other institutions A-5 Manuscripts A-6 Catalogues of periodicals A-7 Textual criticism, e.g. of older Chinese texts A-9 Miscellaneous notes (sui-bi) A-9.1 Pre-Qing A-9.4 Qing A-9.6 Republic (1911-1949) A-9.7 Modern (1949- ) [B History] B-0.00 General B-0.01 Periodicals B-0.02 Series B-0.03 Collections of essays, Festschriften etc. B-0.04 Bibliographies and documents B-0.05 Study; historiography B-0.06 Constitutional and social history B-0.07 Historical geography B-0.09 Chronology and chronological tables B-0.1 Chinese calendars B-0.11 Military history B-0.12 Foreign relations – Divided geographically B-0.19 Encyclopaedias B-0.8 History of countries other than China – Divided geographically B-0.9 Chinese local history B-1 Ancient history (to 255 B.C.) (including prehistoric archaeology) B-1.1 Semi-mythical (2637-2205 B.C.) B-1.3 Xia (2205-1766 B.C.) B-1.5 Shang (Yin) (1766-1122 B.C.) B-1.7 Zhou (1122-255 B.C.) B-1.8 Qin (dynasty) B-2.2 Han (206 B.C. -

2010 International Conference on E-Product E-Service and E-Entertainment (ICEEE 2010)

2010 International Conference on E-Product E-Service and E-Entertainment (ICEEE 2010) Henan, China 7 – 9 November 2010 Pages 1-866 IEEE Catalog Number: CFP1096J-PRT ISBN: 978-1-4244-7159-1 1/7 TABLE OF CONTENTS 3PL-BASED SYNERGY STRATEGY MODEL AND INFORMATION MANAGEMENT SYSTEM FOR INDUSTRY CLUSTER IN CHINA .................................................................................................................................................................1 Hong-Yan Li, Ye Xing, Jing Chen A CHOICE MODEL FOR BEST TRUSTWORTHY SUPPLIER--BTSM ................................................................................................5 Jun-Feng Tian, Hao Huang, Yong Wang A COMPARATIVE STUDY OF TOURISM ENGLISH ----BASED ON ENGLISH WEBSITES OF YELLOWSTONE NATIONAL PARK AND JIUZHAI VALLEY..............................................................................................................9 Lili Zhan A COMPARATIVE STUDY ON LEADERSHIP MECHANISM OF SINO-NORWEGIAN BI-CULTURAL TELEWORKING TEAMS .............................................................................................................................................................................13 Bin He, Baozhen Liu, Lili Li, Jing Sun, Siyue Wu A CONCEPTUAL MODEL OF THE RELATIONSHIP BETWEEN ENTREPRENEUR MECHANISMS AND ENTERPRISE PERFORMANCE IN TRANSITIONAL CHINA..............................................................................................................17 Yu Song, Wenjing Yan A CONTRASTIVE STUDY ON LEARNING MECHANISM OF SINO-NORWEGIAN BI-CULTURAL -

Cry1ab Rice Does Not Impact Biological Characters and Functional Response of Cyrtorhinus Lividipennis Preying on Nilaparvata Lugens Eggs1

Journal of Integrative Agriculture Advanced Online Publication 2015 Doi: 10.1016/S2095-3119(14)60978-3 Cry1Ab Rice Does Not Impact Biological Characters and Functional Response of Cyrtorhinus lividipennis Preying on Nilaparvata lugens Eggs1 CHEN Yang1, LAI Feng-xiang1, SUN Yan-qun1, HONG Li-ying1, TIAN Jun-ce2, ZHANG Zhi-tao1, and FU Qiang1* 1State Key Laboratory of Rice Biology, China National Rice Research Institute, Hangzhou 310006, P.R.China 2 State Key Laboratory Breeding Base for Zhejiang Sustainable Pest and Disease Control, Institute of Plant Protection and Microbiology, Zhejiang Academy of Agricultural Sciences, Hangzhou 310019, P.R.China ABSTRACT One concern about the use of transgenic plants is their potential risk to natural enemies. In this study, using the eggs of the rice brown planthopper, Nilaparvata lugens, as a food source, we investigated the effects of Cry1Ab rice on the biological characteristics and functional response of an important predator Cyrtorhinus lividipennis. The results showed that the survival ability (adult emergence rate and egg hatching rate), development (egg duration, nymphal developmental duration), adult fresh weight, adult longevity and fecundity of C. lividipennis on Bt rice plants were not significantly different compared to those on non-Bt rice plants. Furthermore, two important parameters of functional response (instantaneous search rate and handling time) were not significantly affected by Bt rice. In conclusion, the tested Cry1Ab rice does not adversely impact the biological character and -

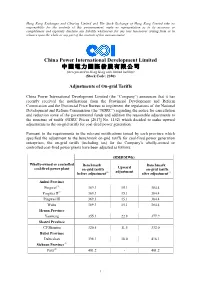

Adjustments of On-Grid Tariffs

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. China Power International Development Limited 中 國 電 力 國 際 發 展 有 限 公 司 (incorporated in Hong Kong with limited liability) (Stock Code: 2380) Adjustments of On-grid Tariffs China Power International Development Limited (the “Company”) announces that it has recently received the notifications from the Provincial Development and Reform Commission and the Provincial Price Bureau to implement the regulations of the National Development and Reform Commission (the “NDRC”) regarding the notice for cancellation and reduction some of the governmental funds and addition the reasonable adjustments to the structure of tariffs (NDRC Prices [2017] No. 1152) which decided to make upward adjustments to the on-grid tariffs for coal-fired power generation. Pursuant to the requirements in the relevant notifications issued by each province which specified the adjustment to the benchmark on-grid tariffs for coal-fired power generation enterprises, the on-grid tariffs (including tax) for the Company’s wholly-owned or controlled coal-fired power plants have been adjusted as follows: (RMB/MWh) Wholly-owned or controlled Benchmark Benchmark Upward coal-fired power plant on-grid tariffs on-grid tariffs (1) adjustment (1) before adjustment after adjustment Anhui Province Pingwei(2) 369.3 15.1 384.4 Pingwei II(2) 369.3 15.1 384.4 Pingwei III 369.3 15.1 384.4 Wuhu 369.3 15.1 384.4 Henan Province Yaomeng 355.1 22.8 377.9 Shanxi Province CP Shentou 320.5 11.5 332.0 Hubei Province Dabieshan 398.1 18.0 416.1 Sichuan Province(3) Fuxi(2) 401.2 - 401.2 1 Notes: (1) The tariff subsidies for desulphurization, denitration and dedusting environmental protection are included. -

A Force for a New Era CHINA STRATEGIC PERSPECTIVES 13

CHINA STRATEGIC PERSPECTIVES 13 China’s Strategic Support Force: A Force for a New Era by John Costello and Joe McReynolds Center for the Study of Chinese Military Affairs Institute for National Strategic Studies National Defense University Center for the Study of Chinese Military Affairs The mission of the China Center is to serve as a national focal point and resource center for multidisciplinary research and analytic exchanges on the national goals and strategic posture of the People’s Republic of China and the ability of that nation to develop, field, and deploy an effective military instrument in support of its national stra- tegic objectives. The Center keeps officials in the Department of Defense (DOD), other government agencies, and Congress apprised of the results of these efforts. The Center also engages the faculty and students of the National Defense University and other components of the DOD professional military education system in aspects of its work and thereby assists their respective programs of teaching, training, and research. The Center has an active outreach program designed to pro- mote exchanges among American and international analysts of Chinese military affairs. China Cyber and Intelligence Studies Institute CCISI is a nonprofit organization focused on the study of China’s use of cyber, intelligence, and information operations as instruments of state power. CCISI seeks to empower policymakers and analysts with a nuanced and informed view of Chinese cyber issues derived from in- depth study of Chinese language sources, strategy, doctrine, and capa- bilities. John Costello and Joe McReynolds are co-founders and Director Emeritus and Director of Operations, respectively, for CCISI. -

6 X 10.Long.P65

Cambridge University Press 978-0-521-60355-3 - China’s Republic Diana Lary Index More information Index of names Anderson, J. G., 92 as leader, 104–5, 125 Ang Lee, see Li Ang Memorial Hall, 195 and Northern Expedition, 56 n. 5, 79 Ba Jin, 55 puritanism, 195 Backhouse, Edmund, 56 n. 5 remains, 76 Bada Shanren, 93 in Resistance War, 114, 117, 125, 142–3 Bai Chongxi, 100, 189, 198 resumes presidency, 189 Bai Xianyong (Pai Hsien-yung), 198 as revolutionary leader, 76 Black, Davidson, 92 as soldier, 100 Bland, J. O. P., 16, 31 in Taipei, 190 Borodin, Michael, 75 Chiang Wei-kuo, 201 n. 13 Bose, Subbhas Chandra, 155 n. 4 Churchill, Winston, 127 Buck, Pearl, 19, 85, 107 Cixi (Empress Dowager), 17, 29 death, 40 Cai Tingkai, 69, 99, 100, 176 flight from Peking, 27 Cantlie, James, 21 and reforms, 22–3 Cao Cao, 59 tomb, 47, 53 Capa, Robert, 119 Confucius, 53 Cartier-Bresson, Henri, 161 Chang, Jun (Zhang Rong), 168 Dai Li, 125 Chen Duxiu, 75 Dai Jitao, 201 n. 13 Ch’en, Eugene, 79 De Wang, 75, 99, 129, 130, 155 Chen Jian, 147 n. 12 Deng Xiaoping, 59, 181, 212 Chen Jiongming, 57 Ding Wenjiang, 64, 92 Chen Jitang, 60, 102, 103 Dong Jianhua (C. H. Tung), 175 Chen Kaige, 198 Du Fu, 59 Chen Lifu, 174, 182 Chen Piqun, 155 Fei Xiaotong, 176 Ch’en Shui-pien (Shuibian), 12, 181, 201, Feng Youlan, 176 202 n. 14, 205, 216 Feng Yuxiang, 60, 100 Chen Yi, 158 Fu Zuoyi, 170, 176 Chen Yi (Marshal), 158 Chennault, Claire, 144 Gong Li, 94 Cheung, Leslie, 94 Goto Shimpei, 186 Cheung, Maggie, 89 Gu Weijun (Wellington Koo), 55 Chiang Ching-kuo, 85, 201 n. -

The 19Th International Conference on Geoinformatics June 24-26, 2011 Shanghai, China

The 19th International Conference on Geoinformatics June 24-26, 2011 Shanghai, China Conference Program Co-Organizers: The Key Lab of Geographical Information Science, Ministry of Education, East China Normal University The Lab for Urban and Regional Analysis, East China University of Science and Technology The International Association of Chinese Professionals in Geographic Information Sciences (CPGIS) Co-Sponsors: IEEE Geoscience and Remote Sensing Society (IEEE GRSS) School of Resource and Environmental Science, East China Normal University Shanghai Urban Development Information Research Center The Geographical Society of Shanghai Business School, East China University of Science and Technology International Center for Risk Governance Research in Coastal Urban Region, East China Normal University ii Table of Content Committees.............................................................................................................. 1 Honorary Chairs........................................................................................................................1 International Steering Committee .............................................................................................1 Program Committee ..................................................................................................................1 Organization Committee ...........................................................................................................2 Useful Information .................................................................................................