Community Reinvestment Act Performance Evaluation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report for the As a Result of the National Financial Environment, Throughout 2009, US Congress Calendar Year 2009, Pursuant to Section 43 of the Banking Law

O R K Y S T W A E T E N 2009 B T A ANNUAL N N E K M REPORT I N T G R D E P A WWW.BANKING.STATE.NY.US 1-877-BANK NYS One State Street Plaza New York, NY 10004 (212) 709-3500 80 South Swan Street Albany, NY 12210 (518) 473-6160 333 East Washington Street Syracuse, NY 13202 (315) 428-4049 September 15, 2010 To the Honorable David A. Paterson and Members of the Legislature: I hereby submit the New York State Banking Department Annual Report for the As a result of the national financial environment, throughout 2009, US Congress calendar year 2009, pursuant to Section 43 of the Banking Law. debated financial regulatory reform legislation. While the regulatory debate developed on the national stage, the Banking Department forged ahead with In 2009, the New York State Banking Department regulated more than 2,700 developing and implementing new state legislation and regulations to address financial entities providing services in New York State, including both depository the immediate crisis and avoid a similar crisis in the future. and non-depository institutions. The total assets of the depository institutions supervised exceeded $2.2 trillion. State Regulation: During 2009, what began as a subprime mortgage crisis led to a global downturn As one of the first states to identify the mortgage crisis, New York was fast in economic activity, leading to decreased employment, decreased borrowing to act on developing solutions. Building on efforts from 2008, in December and spending, and a general contraction in the financial industry as a whole. -

Bank-Owned ATM Locations in New York State

Bank-Owned ATM Locations in New York State Name of Institution Street Address Wells Fargo ATM 234 West 33rd Street Bank of America N.A. GA1-006-15-40 Pinwlawn Road Bank of America N.A. GA1-006-15-40 130 North Country Shopping Center Berkshire Bank (Pittsfield, MA) 1925 Curry Road Capital One, N.A. Chelsea Piers Catskill Hudson Bank 1987 State Route 52 Citibank N. A. 717 Avenue of Americas Citibank N. A. 1445 East 82nd Street Community Bank, N.A. 311 North Comrie Ave, Route 30A Community Bank, N.A. 3140 West State Road Delta Employees Credit Union JFK Terminal 3 Elmira Savings Bank, FSB Route 17 & Chambers Road Empower Federal Credit Union State Street Evans National Bank 6840 Erie Road Five Star Bank 1940 Routes 5 & 20 Fulton Savings Bank Route 57 Greater Hudson Bank 485 Schutt Road Hudson United Bank Reade Place JPMorgan Chase Bank, National Association 333 Route 303 & Orangeburg Road Suffolk Federal Credit Union 850 North Country Road Drive, Route 39 Page 1 of 624 09/29/2021 Bank-Owned ATM Locations in New York State City ZIP Code County Georeference New YOrk 10119 New York Melville 11747 Suffolk Goldens Bridge 10526 Westchester Rotterdam 12303 Schenectady New York 10011 New York Liberty 12754 Sullivan New York 10010 New York New York 10028 New York Johnstown 12095 Fulton Allegany 14760 Cattaraugus Jamaica 11430 Queens Big Flats 14814 Chemung Phoenix 13135 Oswego Derby 14047 Erie POINT (-78.980166 42.701287) Waterloo 13165 Seneca Phoenix 13135 Oswego Middletown 10940 Orange Poughkeepsie 12601 Dutchess Orangeburg 10962 Rockland Southampton -

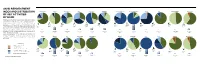

Anhd Reinvestment Index and Distribution of Key

COMMERCIAL BANKS SAVINGS BANKS WHOLESALE BANKS ANHD REINVESTMENT INDEX AND DISTRIBUTION JPMorgan Chase Citibank Bank of America HSBC Capital One Wells Fargo Sovereign / Santander NY Community Bank Astoria Apple Bank of NY Mellon* Goldman Sachs OF KEY ACTIVITIES BY BANK The 23 largest banks in New York City hold over $590 billion in depos- its and collectively devote only 1.35% of these deposits to lending and investments that benefit low- and moderate-income (LMI) New Yorkers. ANHD developed the Reinvestment Index to capture the percentage of local deposits each bank devoted to key reinvestment activities in NYC. Deposits: Deposits: Deposits: Deposits: Deposits: Deposits: The index includes (1) Community Development Lending, (2) CRA- Deposits: Deposits: Deposits: Deposits: Deposits: Deposits: 4.20% $11.6b $7.6b $5.1b 24.53% $4.3b $66b $32.3b Qualified Investments, and (3) CRA-eligible grants. For Commercial $256b $48.9b $43b $39.4b $17.8b $4b and Savings Banks, it also factors in (1) Multifamily lending in LMI 2.35% 2.28% 1.36% tracts, (2) Home purchase lending to LMI borrowers, and (3) Small 0.88% 1.19% 0.80% business lending in LMI tracts. The average reinvestment index among 0.36% 0.15% 0.75% 0.65% all banks is 3.1%, and when the highest and lowest percentages are re- Reinvestment Reinvestment Reinvestment Reinvestment Reinvestment Reinvestment Reinvestment Reinvestment Reinvestment Reinvestment Reinvestment Reinvestment moved, the average drops to 2.2%. Index Index Index Index Index Index Index Index Index Index Index Index The pie charts graphically represent each bank's distribution of these key reinvestment activities. -

Apple Bank Announces Mayra Tepan at Scarsdale NY Branch

News Release FOR IMMEDIATE RELEASE: Media Contact: Rick Anderson Connie Martin/Apple Bank (718) 986-1596 (212) 224-6455 [email protected] [email protected] APPLE BANK FOR SAVINGS NAMES MAYRA TEPAN ASSISTANT VICE PRESIDENT AND BRANCH MANAGER OF ITS SCARSDALE OFFICE SCARSDALE, NY – JULY 24, 2018 – Apple Bank for Savings has announced the appointment of Mayra Tepan as Assistant Vice President and Branch Manager at the Scarsdale, Westchester branch office located at 1075 Central Park Avenue. Ms. Tepan joins Apple Bank from Peoples United Bank, where she most recently served as Branch Manager of their Yonkers office. James Matera, Executive Vice President and Head of Apple Bank’s Consumer Banking Division, said, “We are very pleased that Mayra Tepan has joined the Apple Bank team in Westchester. She brings excellent retail banking experience and a strong familiarity with the local banking market, having served in branch management positions in the Westchester area with Peoples United Bank and J.P. Morgan Chase.” Ms. Tepan joined Peoples United Bank in 2012 in Massachusetts and then moved to Connecticut where she spent three years as Lead Financial Services Associate in their Greenwich office. Ms. Tepan then was promoted to Branch Manager of the Stamford, Connecticut office before moving on to head their Yonkers branch in Westchester. Mayra joined Peoples United Bank from TD Bank where she had been a Customer Service Representative for two years in Massachusetts. Previously, she worked for J.P. Morgan Chase as a Senior Teller in their Harrison, New York office beginning in 2004. Ms. Tepan joined J.P. -

Apple Bank Appoints Branch Manager in Jackson Heights, Queens

News Release FOR IMMEDIATE RELEASE: Media Contact: Rick Anderson (718) 986-1596 [email protected] APPLE BANK FOR SAVINGS APPOINTS ROHAN MADRAMOOTOO AS BRANCH MANAGER OF ITS NEWEST BRANCH OFFICE IN JACKSON HEIGHTS, QUEENS JACKSON HEIGHTS, NY – MAY 14, 2015 – Apple Bank for Savings has appointed Rohan Madramootoo as Branch Manager of its newest full-service branch office located at 78-01 37th Avenue in Jackson Heights, Queens. The opening of the bank’s sixth branch location in Queens is scheduled for Thursday, May 21, at 9:00 am. Branch hours are Monday through Thursday: 9:00 am to 4:00 pm, Friday: 9:00 am to 6:00 pm and Saturday: 9:00 am to 1:00 pm. Rohan currently serves as Assistant Vice President and Branch Manager for Apple Bank’s Scarsdale branch office in Westchester. James Matera, Executive Vice President and Head of Apple Bank’s Consumer Banking Division, said, “Rohan has been a valuable member of the bank’s branch management team for close to 25 years. He has built an impressive track record of success in business development, customer service and community outreach for the bank, and we look forward to his developing a strong following in the Jackson Heights community.” After holding sales and customer service positions at various New York City savings banks, Rohan joined Apple Bank in 1987 as a Customer Service Representative and became Assistant Branch Manager at the 2100 Broadway office in Manhattan in 1993. He then was promoted to Branch Manager of Apple’s Wall Street branch and served at this location from 1996 to 2005. -

Annual Report 2017

265 Henry Street New York, New York 10002-4808 212.766.9200 www.henrystreet.org HENRY STREET SETTLEMENT opens doors of opportunity to enrich lives and enhance human progress for Lower East Side residents and other New Yorkers through social services, arts and health care programs. ANNUAL REPORT 2017 Inside The cover features details of commissioned artists’ renderings of our iconic historic headquarters. MESSAGE FROM THE EXECUTIVE DIRECTOR FRONT COVER, CLOCKWISE FROM TOP: 2 H Spencer Young; Mark Palazzolo (markpalazzolo.com); Ed Cahill; 3 MESSAGE FROM THE BOARD OF DIRECTORS H Spencer Young; c. 1930 image of Henry Street. BACK COVER, CLOCKWISE FROM UPPER LEFT: Bob Rothstein; 4 CELEBRATING 125 YEARS OF HENRY STREET Ken Condon; Hedy Pagremanski; Mark Palazzolo; and Kit Maloney. WE BOUGHT A FIREHOUSE! CLOCKWISE FROM TOP LEFT: Early health 6 clinic at the Settlement; children in the Early Childhood Education Center; Abrons Arts Center dancers IT HAPPENED ON HENRY STREET 2017 at An Evening at Ludlow House; 8 1910 knitting class; and artist’s OUR PROGRAMS AND CLIENTS rendering of Henry Street. 10 16 TREASURES OF HENRY STREET 20 FINANCIAL REPORT FY2017 22 HENRY STREET DONORS 30 GALAS AND PARTIES 32 BOARD OF DIRECTORS AND SENIOR STAFF 33 MAP OF HENRY STREET LOCATIONS Messages FROM HENRY STREET FROM THE FROM THE Board of Directors Executive HENRY STREET’S SOLE MISSION is to serve our Director community, a course charted 125 years ago by our founder, AS HENRY STREET ENTERS its 125th year, our Lillian Wald. Originally serving neighbors through a visiting nurse service, she quickly realized that the needs of the Scott Swid Quasquicentennial, we have much to celebrate. -

Now Apple Bank for Savings

Landmark Preservation Commission December 21, 1993; Designation List 256A LP-1804 CENTRAL SAVINGS BANK (now Apple Bank for Savings), first floor interior consisting of the north, south, and west entrance vestibule and foyer, the main banking hall, and the two staircases leading from the first floor to the mezzanine floor level; the mezzanine floor interior consisting of the open passages above the north and south vestibules, the arcaded loggia with balustrade above the west entrance vestibule and foyer, the upper part of the banking hall, and the ceiling; and the fixtures and interior components of these spaces, including but not limited to, wall surfaces, ceiling surfaces, and marble floor surfaces, doors, stair and balcony railings, fixed counters, lighting fixtures, decorative ironwork, and attached decorative elements; 2100-2114 Broadway, Manhattan. Built 1926-28; York & Sawyer, architects. Landmark Site: Borough of Manhattan Tax Map Block 1165, Lot 36. On July 10, 1990, the Landmarks Preservation Commission held a public hearing on the proposed designation as an Interior Landmark of the Central Savings Bank, first floor interior consisting of the north, south, and west entrance vestibules, the main banking hall, and the two staircases leading from the first floor to the mezzanine level; the mezzanine floor interior consisting of balconies above the north and south vestibules, the main balcony above the west entrance vestibule, the upper part of the banking hall, and the ceiling; and the fixtures and interior components of these spaces, including but not limited to, wall, ceiling, and floor surfaces, doors, stair and balcony railings, lighting fixtures, fixed counters, decorative ironwork, and attached decorative elements; and the proposed designation of the related Landmark Site (Item No. -

Community Based Organizations

Community Based Organizations Alliance for Progress Allianza Dominicana 1070 Ogden Avenue 1257 Ogden Avenue Bronx, New York 10452 Bronx, New York 10452 Ms. Antonia Diaz, Chairperson Ms. Maria Stroud, Director (718) 992-6448 (718) 590-0101 Anderson Avenue HDFC Andrew Freeman Home 1185 Anderson Avenue 1125 Grand Concourse Bronx, New York 10452 Bronx, New York 10452 Ms. Katherina McMilian, Pres Mr. Elbert Courtneay, Adm. (718) 588-0614 (718) 293-8100 Apple Bank for Savings Alliance for Community Services 44 East 161st Street 110 E. Burnside Avenue Bronx, New York 10451 Bronx, New York 10453 Mrs. Rene Cross, Branch Mgr. Mr. Leo Martinez, Director (718) 537-2500 (718) 583-8011 Albert Einstein College of Medicine Bronx Campaign for Peace & Quiet Melrose 9 Clinic 141 Marcy Place Division of Substance Abuse Bronx, New York 10452 260 East 161st Street Mr. John E. Dallas, President Bronx, New York 10451 (212) 802-4964 Ms. Felice Bradford, Adm. (718) 292-6622 Bronx General Post Office Bronx Lebanon Hospital Center 558 Grand Concourse 1276 Fulton Avenue Bronx, New York 10451 Bronx, New York 10456 Mr. Tony Rosario, Postmaster Mr. Miguel Fuentes, President (718) 402-1459 (718) 901-8800 Bronx Lebanon Hospital Center Bronx Defenders 1650 Selwyn Avenue-8E 890 Grant Avenue Bronx, New York 10457 Bronx, New York 10452 Mr. Robert Sancho, V.P. of Development M s. Denise King, Client Advocate And External Affairs (718) 838-7878/7860 (718) 960-4490 BRONX COMMUNITY BOARD #4 COMMUNITY BASED ORGANIZATIONS PAGE-2- NYC Department of Education Crime Victims Assistant Unit Instructional Division #1 98 East 161 Street-5th Floor One Fordham Plaza Bronx, New York 10451 Bronx, New York 10464 Ms. -

3.8 Neighborhood Character (FEIS)

125th Street Corridor Rezoning and Related Actions EIS New York City Department of City Planning 3.8 NEIGHBORHOOD CHARACTER INTRODUCTION As defined in the CEQR Technical Manual, neighborhood character is considered to be an amalgam of the various elements that give a neighborhood its distinct personality. These elements can include land use, urban design, visual resources, historic resources, socioeconomic conditions, traffic, and noise, as well as any other physical or social characteristics that help to distinguish the community in question from another. The proposed action is anticipated to result in changes to the neighborhood character of the 125th Street corridor. These changes are considered to be beneficial to the overall character of the corridor and would not constitute significant adverse impacts to neighborhood character. According to the CEQR Technical Manual, an assessment of neighborhood character is generally needed when the action would exceed preliminary thresholds in any one of the following areas of technical analysis: land use, urban design and visual resources, historic resources, socioeconomic conditions, transportation, or noise. An assessment is also appropriate when the action would have moderate effects on several of the aforementioned areas. Potential effects on neighborhood character may include: Land Use. Development resulting from a proposed action could alter neighborhood character if it introduces new land uses, conflicts with land use policy or other public plans for the area, changes land use character, or generates significant land use impacts. Socioeconomic Conditions. Changes in socioeconomic conditions have the potential to affect neighborhood character when they result in substantial direct or indirect displacement or addition of population, employment, or businesses; or substantial differences in population or employment density. -

Federal Home Loan Bank of New York Members Selected for Community Support Review

Federal Home Loan Bank of New York Members Selected for Community Support Review Member Address City State Zip 1st Bank of Sea Isle City 4301 Landis Avenue Sea Isle City NJ 08243 1st Colonial Community Bank 1040 Haddon Avenue Collingswood NJ 08108 1st Constitution Bank 2650 Route 130 Cranbury NJ 08512 Abacus Federal Savings Bank Six Bowery New York NY 10013-1596 Adirondack Bank 185 Genesee Street Utica NY 13501 Advantage Federal Credit Union 1975 Buffalo Road Rochester NY 14624 Affinity Federal Credit Union 73 Mountainview Boulevard Basking Ridge NJ 07920 Alden State Bank 13216 Broadway Alden NY 14004 Alma Bank 28-31 31st Street Astoria NY 11102 Alpine Capital Bank 680 Fifth Avenue, 15th Floor New York NY 10019 Alternatives Federal Credit Union 125 North Fulton Street Ithaca NY 14850-3301 Amalgamated Bank 275 Seventh Avenue, 14th Fl. New York NY 10001 Amboy Bank 3590 U.S. Highway No. 9 Old Bridge NJ 08857 Amerasia Bank 41-06 Main Street Flushing NY 11355 American Community Bank 300 Glenn Street Glen Cove NY 11542 American Home Assurance Company 175 Water Street, 18th fl. New York NY 10038 AmeriCU Credit Union 1916 Black River Boulevard Rome NY 13440 Apple Bank for Savings 1395 Northern Boulevard Manhasset NY 11030 ARBC Insurance Company, LLC 445 South Street #210 Morristown NJ 07960 Aspire Federal Credit Union 67 Walnut Avenue, Ste. 401 Clark NJ 07066 Astoria Bank One Astoria Bank Plaza Lake Success NY 11042-1085 Atlantic Stewardship Bank 630 Godwin Avenue Midland Park NJ 07432 Audubon Savings Bank 515 South White Horse Pike Audubon NJ -

Banking in the Bronx: Evaluating Options in a Historically Redlined

Banking in the Bronx Assessing Options in a Historically Redlined and Underbanked Borough April 2012 A report by University Neighborhood Housing Program Banking in the Bronx: Assessing Options in a Historically Redlined and Underbanked Borough Historical Context Much of the economic decline in the Bronx in the 1960s and 1970s was due to redlining and disinvestment by the financial industry and the government. Federal Housing Authority (FHA) and Veterans Administration (VA) mortgage underwriting criteria discriminated against both borrowers of color and dense urban neighborhoods, setting the stage for increased racial and ethnic segregation and the devaluation of properties in cities. A shift in federal investment away from public transportation and into highways and suburban development, along with urban renewal projects that demolished thriving neighborhoods in favor of expressways and public housing uprooted hundreds of thousands and created every incentive for a mass exodus from places like the Bronx. Many of those who could depart, did so. The absence of manufacturing jobs for newcomers, mostly black and Latino, increased a need for social services while shrinking the tax base. Budget restraints by the City led to a loss of municipal services, and struggling neighborhoods such as those in the south Bronx bore the brunt of many of these cuts – most significantly to the fire department. In the depths of the ensuing devastation which began in southern part of the borough and headed north in a wave taking out neighborhood after neighborhood, many Bronx residents joined together to fight back. In the northwest part of the borough, a coalition of neighborhood associations and local clergy was formed in 1974. -

Heights Planning Initiative

Heights Planning Initiative A survey of Washington Heights and Morningside Heights in Manhattan, New York City. Convened by: Community League of the Heights Report Prepared by: Warnke Community Consulting JANUARY 2005 Copies of the executive summary (English/Spanish), the report, or other information can be requested from: Copias del resumen ejecutivo en español pueden ser solicitadas a la Community League of the Heights (Asociación Comunitaria de la Zona Heights en el alto Manhattan). Community League of the Heights 500 West 159th Street, New York, NY 10032 T (212) 795 4779 | [email protected] For Information about the Community Survey data or other inquiries about neighborhood planning contact: Warnke Community Consulting 198 Broadway, Suite 1100, New York, NY 10038 T (212) 566 8805 | F (212) 566 8806 | [email protected] | www.warnkecc.com TABLE OF CONTENTS Acknowledgements..................................................................................................................... iv Forward...................................................................................................................................... vii Executive Summary......................................................................................................................x Background and Methodology......................................................................................................1 Community Survey Data...............................................................................................................3 Demographics