Executive Remuneration Research Centre

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Historyeurex14e 08-03-28 Dezimalerweiterung

Contract Specifications for Futures Contracts and Eurex14 Options Contracts at Eurex Deutschland and Stand March 278, 2008 Eurex Zürich Seite 1 [….] Annex A in relation to subsection 1.6 of the contract specifications: Futures on Shares of Produkt- Group Cash Contract Minimum Price Currency ID ID** Market- Size Change* ID** AEGON N.V. AENF NL01 XAMS 100 0.00010.01 EUR Koninklijke Ahold N.V. AHOG NL01 XAMS 100 0.00010.01 EUR Akzo Nobel N.V. AKUF NL01 XAMS 100 0.00010.01 EUR ASML Holding N.V. ASMG NL01 XAMS 100 0.00010.01 EUR Koninklijke BAM Groep N.V. BGPF NL01 XAMS 100 0.00010.01 EUR Corporate Express N.V. BUHF NL01 XAMS 100 0.00010.01 EUR Corio N.V. CL6F NL01 XAMS 50 0.0010.01 EUR CSM N.V. CSMF NL01 XAMS 50 0.0010.01 EUR Koninklijke BAM Groep N.V. DSMF NL01 XAMS 100 0.00010.01 EUR Reed Elsevier ELVF NL01 XAMS 100 0.0010.01 EUR Reed Elsevier N.V. ELVG NL01 XAMS 100 0.00010.01 EUR Fortis N.V. FO4G NL01 XAMS 100 0.00010.01 EUR Fugro N.V. FUGF NL01 XAMS 100 0.0010.01 EUR Heineken Holding N.V. HEHF NL01 XAMS 100 0.00010.01 EUR Hagemeyer N.V. HMYF NL01 XAMS 100 0.00010.01 EUR Heineken N.V. HNKF NL01 XAMS 100 0.00010.01 EUR SBM Offshore N.V. IHCG NL01 XAMS 100 0.00010.01 EUR ING Groep N.V. INNF NL01 XAMS 100 0.00010.01 EUR Koninklijke KPN N.V. -

Contracts and Eurex14e Options Contracts at Eurex Deutschland and Eurex Zürich As of 22.01.2018 Page 1

Contract Specifications for Futures Contracts and Eurex14e Options Contracts at Eurex Deutschland and Eurex Zürich As of 22.01.2018 Page 1 ********************************************************************************** AMENDMENTS ARE MARKED AS FOLLOWS: INSERTIONS ARE UNDERLINED DELETIONS ARE CROSSED OUT ********************************************************************************** 1. Part: Contract Specifications for Futures Contracts […] 2. Subpart: Contract Specifications for Index Options […] 2.6.11 Price Gradations The price of a stock option or LEPO will generally be quoted with three or four decimal place. The smallest price change (Tick) shall be EUR 0.0005, EUR 0.001, EUR 0.01 or CHF 0.01 or GBX* 0.5, GBX 0.25 or USD 0.01. For stock options with group ID NL11, NL12 and NL13, the tick size will increase to EUR 0.05 for contracts with a premium above a predefined threshold stipulated in Annex B (Premium Threshold). The Management Boards of the Eurex Exchanges shall determine the relevant decimal place and the smallest price change (Tick) and shall notify all Exchange participation of any such decision. 3. Part: Contracts Off-Book […] Contract Specifications for Futures Contracts and Eurex14e Options Contracts at Eurex Deutschland and Eurex Zürich As of 22.01.2018 Page 2 3.3.4.2 Annex B: in relation to Subsection 2.6 of the Contract Specifications: […] Options on shares of Product-ID Group ID Minimum price Premium Minimum price change below Threshold change above threshold threshold Aalberts Industries N.V. AAI NL12 0.01 0.5 0.05 ABN AMRO Group AAR NL11 0.01 5 0.05 AEGON N.V. AEN NL11 0.01 5 0.05 Koninklijke Ahold NL11 Delhaize N.V. -

Last Name First Name Company Name Job Title Country Kennedy

Last Name First Name Company Name Job Title Country Kennedy Matthew 1CSI CEO United Kingdom Brown Tom 2H OFFSHORE ENGINEERING LTD Senior Engineer United Kingdom Roos Jan 2MOFFSHORE BV Advisor Netherlands Hardon Maarten 2MOFFSHORE BV Advisor Netherlands Roos Jan 2MOFFSHORE BV Advisor Netherlands Hardon Maarten 2MOFFSHORE BV Advisor Netherlands PETERS Luc 3B-THE FIBREGLASS COMPANY Technical Service Manager Belgium Palmers Geert 3E CEO Belgium Coppye Werner 3E CTO Belgium Pianta Martina 3E Product Manager Belgium Mertiris Vasilis 3E Technical Account Manager Belgium Lead Consultant International Business Estrada Santiago 3E Development Belgium Fripiat Michel 3E Technical Account Manager Belgium De Vylder Thomas 3E CEO Belgium Anderson Lauren 4C Offshore United Kingdom RUSSELL Tom 4C Offshore Press Coordinator United Kingdom ANDERSON Chris 4C OFFSHROE CEO United Kingdom Brown Julian 8.2 AARUFIELD LTD Director United Kingdom Dugué Charles 8.2 CONSULTING AG CEO Germany 't Hooft Jaap 8WINDS Head Netherlands Heap Richard A WORD ABOUT WIND Editor United Kingdom Nielsen Gina A2SEA A/S Senior Marketing Coordinator Denmark Siddiqui Mo. AACTIO GMBH Managing Director Germany Slot René M. M. AALBORG UNIVERSITY PhD candidate Denmark Nielsen Jannie Sønderkær AALBORG UNIVERSITY Assistant Professor Denmark LASOTA Michal ABB Area Sales Manager - Transformer Service Poland Global Marketing & Sales Manager - PRYLINSKI Pawel ABB Renewables Poland Pacheco Ramos Pablo ABB Shell Transformer Product Manager Spain Gracia Abad Juan Pedro ABB Account Manager Spain -

Euronext Options and Futures Traded at the Amsterdam Derivatives Markets

Euronext Options and Futures traded at the Amsterdam Derivatives Markets Last change: Added new Spotlight option contracts AFU & HAL Date: Effective per 07-06-2021 STANDARD EXPIRY CYCLE Trading American style equity options Serial Quarterly HY Annual symbol 1 2 3 6 9 12 18 24 36 48 60 ABN AMRO Bank ABN x x x x x x x x x x x AEGON AGN x x x x x x x x x x x Koninklijke Ahold Delhaize AH x x x x x x x x x x x Akzo Nobel AKZ x x x x x x x x x x x ASML Holding ASL x x x x x x x x x x x Koninklijke DSM DSM x x x x x x x x x x x Heineken HEI x x x x x x x x x x x ING Groep ING x x x x x x x x x x x Koninklijke KPN KPN x x x x x x x x x x x ArcelorMittal MT x x x x x x x x x x x Koninklijke Philips Electronics PHI x x x x x x x x x x x Royal Dutch Shell (A-shares) RD x x x x x x x x x x x RELX PLC (EUR) REN x x x x x x x x x x x Unilever UN x x x x x x x x x x x ASM International ASM x x x x x x x x x Prosus PRX x x x x x x x x x Adyen (contract size 10) ADY x x x x x x x x Air France-KLM AFA x x x x x x x x Ageas AGA x x x x x x x x Koninklijke BAM Groep BAM x x x x x x x x Fugro FUR x x x x x x x x Just Eat Takeaway.com TKW x x x x x x x x Koninklijke PostNL PNL x x x x x x x x Randstad RND x x x x x x x x SBM Offshore SBM x x x x x x x x TomTom TTM x x x x x x x x Unibail-Rodamco-Westfield UBL x x x x x x x x Wolters Kluwer WKL x x x x x x x x Alfen ALF x x x x x x AMG AMG x x x x x x Aperam AP x x x x x x BE Semiconductor Industries BES x x x x x x Koninklijke Boskalis westminster BOS x x x x x x Klépierre CIO x x x x x x JDE Peet's JDE x -

Expiry Months Listed Per Class

Euronext Options and Futures traded at the Amsterdam Derivatives Markets Last change: Adding new options classes Alfen (ALF) and Eurocommercial Properties (ECM) Date: 25-Sep-20 STANDARD EXPIRY CYCLE Trading American style equity options Serial Quarterly HY Annual symbol 1 2 3 6 9 12 18 24 36 48 60 ABN AMRO Bank ABN x x x x x x x x x x x AEGON AGN x x x x x x x x x x x Koninklijke Ahold Delhaize AH x x x x x x x x x x x Akzo Nobel AKZ x x x x x x x x x x x ASML Holding ASL x x x x x x x x x x x Koninklijke DSM DSM x x x x x x x x x x x Heineken HEI x x x x x x x x x x x ING Groep ING x x x x x x x x x x x Koninklijke KPN KPN x x x x x x x x x x x ArcelorMittal MT x x x x x x x x x x x Koninklijke Philips Electronics PHI x x x x x x x x x x x Royal Dutch Shell (A-shares) RD x x x x x x x x x x x RELX PLC (EUR) REN x x x x x x x x x x x Unilever UN x x x x x x x x x x x Adyen (contract size 10) ADY x x x x x x x x Air France-KLM AFA x x x x x x x x ASM International ASM x x x x x x x x Ageas AGA x x x x x x x x Koninklijke BAM Groep BAM x x x x x x x x Fugro FUR x x x x x x x x Koninklijke PostNL PNL x x x x x x x x Prosus PRX x x x x x x x x Randstad RND x x x x x x x x SBM Offshore SBM x x x x x x x x TomTom TTM x x x x x x x x Wolters Kluwer WKL x x x x x x x x Altice Europe ATC x x x x x x Aperam AP x x x x x x BE Semiconductor Industries BES x x x x x x Koninklijke Boskalis westminster BOS x x x x x x Klépierre CIO x x x x x x JDE Peet's JDE x x x x x x NN Group NN x x x x x x Unibail-Rodamco-Westfield UBL x x x x x x Koninklijke Vopak -

Euronext Options and Futures Traded at the Amsterdam Derivatives Markets

Euronext Options and Futures traded at the Amsterdam Derivatives Markets Last change: Removal of contract ATC (takeover), added 12-month maturity to contract ALF and changed name for contract CCE (corporate action: name change) Date: Effective per 26-05-2021 STANDARD EXPIRY CYCLE Trading American style equity options Serial Quarterly HY Annual symbol 1 2 3 6 9 12 18 24 36 48 60 ABN AMRO Bank ABN x x x x x x x x x x x AEGON AGN x x x x x x x x x x x Koninklijke Ahold Delhaize AH x x x x x x x x x x x Akzo Nobel AKZ x x x x x x x x x x x ASML Holding ASL x x x x x x x x x x x Koninklijke DSM DSM x x x x x x x x x x x Heineken HEI x x x x x x x x x x x ING Groep ING x x x x x x x x x x x Koninklijke KPN KPN x x x x x x x x x x x ArcelorMittal MT x x x x x x x x x x x Koninklijke Philips Electronics PHI x x x x x x x x x x x Royal Dutch Shell (A-shares) RD x x x x x x x x x x x RELX PLC (EUR) REN x x x x x x x x x x x Unilever UN x x x x x x x x x x x ASM International ASM x x x x x x x x x Prosus PRX x x x x x x x x x Adyen (contract size 10) ADY x x x x x x x x Air France-KLM AFA x x x x x x x x Ageas AGA x x x x x x x x Koninklijke BAM Groep BAM x x x x x x x x Fugro FUR x x x x x x x x Just Eat Takeaway.com TKW x x x x x x x x Koninklijke PostNL PNL x x x x x x x x Randstad RND x x x x x x x x SBM Offshore SBM x x x x x x x x TomTom TTM x x x x x x x x Unibail-Rodamco-Westfield UBL x x x x x x x x Wolters Kluwer WKL x x x x x x x x Alfen ALF x x x x x x AMG AMG x x x x x x Aperam AP x x x x x x BE Semiconductor Industries BES x x x x -

ASML Holding NV Remuneration Report

ASML Holding N.V. Remuneration Report Contents 6 Message of the Supervisory Board 7 The Remuneration Committee 8 Remuneration Policy - Board of Management 14 2015 Remuneration - Board of Management 18 2015 Remuneration - Supervisory Board ASML HOLDING N.V. - REMUNERATION REPORT 2015 Message of the Supervisory Board Dear Shareholders, dear Stakeholders, We are pleased to present the Remuneration Report over the financial year 2015 ("the Report"). In this report you will find information on the remuneration of the Board of Management and the Supervisory Board of ASML Holding N.V. ("ASML" or "the Company"), based on the remuneration policy for the Board of Management, as adopted by the General Meeting of Shareholders on April 24, 2013, and which became effective per January 1, 2014 (the "Remuneration Policy"). Some adjustments to the Remuneration Policy were adopted by the General Meeting of Shareholders on April 23, 2014, and on April 22, 2015, and are applicable retro-actively as from January 1, 2014, and January 1, 2015, respectively. The Remuneration Policy builds on the core principles that have served us for more than ten years: • Transparency: the policy and its execution need to be clear and practical; • Alignment: the remuneration policy is aligned with the ASML business needs and the remuneration policies for ASML’s senior management and other ASML employees; • Long-term orientation: the incentives to management need to focus on long-term value creation; • Compliance: ASML adopts the highest standards of good corporate governance, and • Simplicity: the policy and its execution are as simple as possible and easily understandable for all stakeholders. -

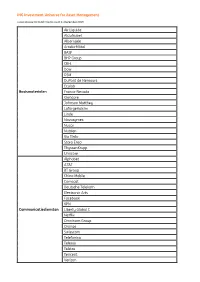

ING Investment Universe for Asset Management Basismaterialen Air

ING Investment Universe for Asset Management Listed shares for Dutch Clients as at 31 December 2019 Air Liquide AkzoNobel Albemarle ArcelorMittal BASF BHP Group CRH Dow DSM DuPont de Nemours Ecolab Basismaterialen Franco-Nevada Glencore Johnson Matthey LafargeHolcim Linde Novozymes Nucor Nutrien Rio Tinto Stora Enso ThyssenKrupp Umicore Alphabet AT&T BT Group China Mobile Comcast Deutsche Telekom Electronic Arts Facebook KPN Communicatiediensten Liberty Global C Netflix Omnicom Group Orange Swisscom Telefonica Telenor Telstra Tencent Verizon Vodafone Group Walt Disney WPP Ahold Delhaize Anheuser-Busch InBev Carrefour Coca-Cola Colgate-Palmolive Danone Diageo Estee Lauder Companies Heineken Henkel Kraft Heinz Company Dagelijkse L'Oreal consumentengoederen METRO Mondelez International Nestle PepsiCo Pernod-Ricard Procter & Gamble Reckitt Benckiser Group Tesco Unilever Walgreens Boots Alliance Wal-Mart Stores WM Morrison Supermarkets Accor Adidas Alibaba Group Holding Amazon.com BMW Booking Holdings CECONOMY Continental Duurzame Daimler consumentengoederen EssilorLuxottica Ford Motor Garmin Hennes & Mauritz Home Depot Inditex Intercontinental Hotels Group Kingfisher Lowe's Companies LVMH Marks & Spencer Group McDonald's Nike Peugeot Prosus Richemont Sodexo Starbucks Swatch Group Target Tesla Motors Toyota Motor YUM! Brands Baker Hughes BP Chevron ENI EOG Resources Equinor ExxonMobil Marathon Petroleum National Oilwell Varco Energie Occidental Petroleum Philips 66 Repsol Royal Dutch Shell SBM Offshore Schlumberger TechnipFMC Total Valero Energy -

Euro Stoxx® Multi Premia Index

EURO STOXX® MULTI PREMIA INDEX Components1 Company Supersector Country Weight (%) BOLSAS Y MERCADOS ESPANOLES Financial Services ES 1.27 SNAM RETE GAS Oil & Gas IT 1.21 CARL ZEISS MEDITEC Health Care DE 1.20 EURONEXT Financial Services FR 1.18 TAG IMMOBILIEN AG Real Estate DE 1.09 SANOFI Health Care FR 1.06 ORION B Health Care FI 1.04 SUEZ ENVIRONNEMENT Utilities FR 1.03 ASM INTERNATIONAL Technology NL 0.98 PUMA Personal & Household Goods DE 0.97 ESSILORLUXOTTICA Health Care FR 0.97 ENAGAS Utilities ES 0.95 SCOUT24 Technology DE 0.92 VOPAK Industrial Goods & Services NL 0.91 L'OREAL Personal & Household Goods FR 0.89 UCB Health Care BE 0.88 GERRESHEIMER Health Care DE 0.86 TERNA Utilities IT 0.86 SARTORIUS STEDIM BIOTECH Health Care FR 0.85 EUTELSAT COMMUNICATION Media FR 0.82 HERA Utilities IT 0.80 HERMES INTERNATIONAL Personal & Household Goods FR 0.80 RECORDATI Health Care IT 0.79 DANONE Food & Beverage FR 0.79 MERCK Health Care DE 0.78 UNILEVER NV Personal & Household Goods NL 0.78 COFINIMMO Real Estate BE 0.77 HANNOVER RUECK Insurance DE 0.74 HUHTAMAKI Industrial Goods & Services FI 0.73 ADIDAS Personal & Household Goods DE 0.72 INGENICO Technology FR 0.72 ICADE Real Estate FR 0.70 WDP Real Estate BE 0.69 FERROVIAL Construction & Materials ES 0.68 SIGNIFY Industrial Goods & Services NL 0.68 BEIERSDORF Personal & Household Goods DE 0.67 SODEXO Travel & Leisure FR 0.65 ENGIE Utilities FR 0.63 SYMRISE Chemicals DE 0.62 WOLTERS KLUWER Media NL 0.62 AENA SME Industrial Goods & Services ES 0.60 SCHNEIDER ELECTRIC Industrial Goods & Services FR 0.60 DIASORIN Health Care IT 0.59 VEOLIA ENVIRONNEMENT Utilities FR 0.59 SIEMENS GAMESA Oil & Gas ES 0.58 FREENET Telecommunications DE 0.58 KINGSPAN GRP Construction & Materials IE 0.58 UNIBAIL-RODAMCO-WESTFIELD Real Estate FR 0.57 ILIAD Telecommunications FR 0.57 ALSTRIA OFFICE REIT Real Estate DE 0.56 ALTEN Technology FR 0.56 OSRAM LICHT Industrial Goods & Services DE 0.55 SARTORIUS PREF. -

Corbion Remuneration Policy Board of Management

Corbion Remuneration Policy Board of Management The objectives of the remuneration policy In order to ensure that Corbion can develop itself as a successful bio-based ingredients and bio- technology company, the first objective of the policy is to enable competitive remuneration and employment conditions to create the best environment for attracting and retaining international talent in this global industry. Secondly, the policy must create a clear and distinct alignment of the interests of the Board of Management with the strategic direction and horizon of the Company. Thirdly, this policy is used as a reference framework for the remuneration policy of Corbion’s senior management to align all interests throughout the organization. Effectiveness This remuneration policy shall be effective from 1 January 2015. Remuneration reference levels Total compensation levels (base salary, STIP, LTIP and the pay mix) are based on a combined reference group of European biotechnology companies and Dutch general industry companies (AMX and smaller AEX). Every two (2) years a reference check will be performed to align the total compensation levels with market levels. The reference groups may be adjusted at that moment in time, as determined by the Supervisory Board and as disclosed on the Company's website. Within these two reference groups, Corbion qualifies around the median in terms of market capitalization, revenue and number of employees. The reference groups used for this remuneration policy consist of the following companies: Dutch reference group European biotechnology Aalberts Industries N.V. Koninklijke Ten Cate N.V. Novozymes (Denmark) Aperam SBM Offshore N.V. Galapagos (Belgium) ASM International N.V. -

Euro Stoxx® Momentum Premium Index

EURO STOXX® MOMENTUM PREMIUM INDEX Components1 Company Supersector Country Weight (%) PUMA Personal & Household Goods DE 2.51 HERMES INTERNATIONAL Personal & Household Goods FR 1.94 Getlink Industrial Goods & Services FR 1.90 HANNOVER RUECK Insurance DE 1.88 CARL ZEISS MEDITEC Health Care DE 1.88 Vonovia SE Real Estate DE 1.85 PERNOD RICARD Food & Beverage FR 1.83 LEG IMMOBILIEN Real Estate DE 1.68 MTU AERO ENGINES Industrial Goods & Services DE 1.67 MUENCHENER RUECK Insurance DE 1.61 IMCD Chemicals NL 1.61 CHRISTIAN DIOR Personal & Household Goods FR 1.59 KERRY GRP Food & Beverage IE 1.58 TELEPERFORMANCE Industrial Goods & Services FR 1.56 SAFRAN Industrial Goods & Services FR 1.47 UNILEVER NV Personal & Household Goods NL 1.43 FERROVIAL Construction & Materials ES 1.42 CELLNEX TELECOM Telecommunications ES 1.42 L'OREAL Personal & Household Goods FR 1.40 ALTEN Technology FR 1.38 POSTE ITALIANE Insurance IT 1.33 ALLIANZ Insurance DE 1.31 SNAM RETE GAS Oil & Gas IT 1.31 NESTE Oil & Gas FI 1.31 ARGENX Health Care BE 1.28 SOFINA Financial Services BE 1.27 SYMRISE Chemicals DE 1.26 WOLTERS KLUWER Media NL 1.22 AIRBUS Industrial Goods & Services FR 1.17 VERBUND Utilities AT 1.17 RWE Utilities DE 1.16 EDENRED Industrial Goods & Services FR 1.15 ENDESA Utilities ES 1.09 HEINEKEN Food & Beverage NL 1.08 HEINEKEN HLDG Food & Beverage NL 1.07 SARTORIUS STEDIM BIOTECH Health Care FR 1.06 DAVIDE CAMPARI Food & Beverage IT 1.05 Naturgy Energy Group Utilities ES 1.04 DASSAULT SYSTEMS Technology FR 1.04 IBERDROLA Utilities ES 1.03 ASM INTERNATIONAL Technology NL 1.03 SBM OFFSHORE Oil & Gas NL 1.02 LVMH MOET HENNESSY Personal & Household Goods FR 1.02 DEUTSCHE BOERSE Financial Services DE 1.00 VEOLIA ENVIRONNEMENT Utilities FR 0.98 RECORDATI Health Care IT 0.94 NEMETSCHEK Technology DE 0.93 KONINKLIJKE DSM Chemicals NL 0.92 ADIDAS Personal & Household Goods DE 0.91 SARTORIUS PREF. -

Indelta Nederland Index Fonds

Year To Date overview of 31/Jul/21 InDelta InDelta Nederland Index Fonds The InDelta Nederland Index Fonds invests in shares of the largest and most traded companies, listed on the Amsterdam stock exchange. In principle, the Fund Data sub-fund has a passive investment policy. The portfolio is constructed with a Assets under mgmt € 7,432,752 minimum of 40 stocks and aims for 50 stocks, with stocks being equally Last Price € 26.1354 x weighted. Units 284394.44 x Fund Information x Sub-Fund of InDelta x x Fund Manager FundShare Fund x Total Performance Including all costs Management x Portfolio Manager InDelta x Fund Benchmark x ISIN Code NL0010066221 x Currency EUR x Category Stock x 8.6 x mrt-12 jul-13 nov-14 apr-16 aug-17 jan-19 mei-20 Benchmark Stoxx Netherlands x 1M 3M 12M Ytd 3Y (p/y) 5Y (p/y) Start (p/y) x Fund Returns 1.73% 3.29% 49.57% 18.77% 12.77% 13.63% 10.74% Start Fund 02-03-2012 x Benchmark Returns 4.57% 7.76% 48.16% 27.75% 17.94% 16.18% 13.42% Trading frequency Daily x Standard deviation 16.88% 13.37% 15.15% 12.97% 19.54% 16.46% 16.92% Min. Initial Purchase € 1 x Sharp Ratio 1.31 1.10 2.77 2.42 0.73 0.88 0.70 Custodian DeGiro x Operating Fees* 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% Depository Caceis x Management Fees* 0.00% -0.17% -0.24% -0.15% -0.43% -0.46% -0.40% Accountant Mazars x Trading Fees* -0.02% 0.00% -0.03% 0.00% -0.08% -0.10% -0.14% Administrator FundShare Fund x Withholding tax* -0.22% -0.72% -0.38% -0.39% -0.42% -0.45% -0.37% Administration x Turnover* 0% 0% 28% 7% 47% 53% 51% Regulator AFM x *Annualized Website www.fundshare.nl x Fund Returns (net) x Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Total Cum.