The Dutch Gas Market: Trials, Tribulations and Trends

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Special Report on the Earthquake Density and Activity Rate Following the Earthquakes in Appingedam (ML=1.8) and Scharmer (ML=1.5) in August 2017

Special Report on the earthquake density and activity rate following the earthquakes in Appingedam (ML=1.8) and Scharmer (ML=1.5) in August 2017 Datum September 2017 Editors Jan van Elk & Dirk Doornhof 1 Special Report on the earthquake density and activity rate following the earthquakes in Appingedam (ML=1.8) and Scharmer (ML=1.5) in August 2017 2 Special Report on the earthquake density and activity rate following the earthquakes in Appingedam (ML=1.8) and Scharmer (ML=1.5) in August 2017 Contents 1 Introduction ............................................................................................................... 5 2 Acknowledgements ................................................................................................... 7 3 Operating the Meet- en Regelprotocol ...................................................................... 8 4 Appingedam M L = 1.8 earthquake overview ............................................................ 10 5 Schamer M L = 1.5 earthquake overview ................................................................. 14 6 Earthquake density ................................................................................................. 16 6.1 Development of Earthquake Density ................................................................ 16 6.2 Earthquakes contributing to threshold exceedance .......................................... 18 6.3 Detailed analysis of the earthquakes in the Appingedam – Loppersum area ... 23 7 Reservoir analysis: Pressure & Production ............................................................ -

Statutory Security of Supply Report

Statutory Security of Supply Report A report produced jointly by DECC and Ofgem November 2010 Statutory Security of Supply Report � A report produced jointly by DECC and Ofgem Presented to Parliament pursuant to section 172 of the Energy Act 2004 Ordered by the House of Commons to be printed 4th November 2010 HC 542 LONDON: THE STATIONERY OFFICE £14.75 � © Crown copyright 2010 You may re-use this information (not including logos) free of charge in any format or medium, under the terms of the Open Government Licence. To view this licence, visit http://www.nationalarchives.gov.uk/doc/open-government-licence/ or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or e-mail: [email protected]. � Any enquiries regarding this publication should be sent to us at Department of Energy & Climate Change, 3 Whitehall Place, London SW1A 2HD. � This publication is also available on http://www.official-documents.gov.uk/ � ISBN: 9780102969238 � Printed in the UK for The Stationery Office Limited on behalf of the Controller of Her Majesty’s Stationery Office � ID: 2397258 11/10 � Printed on paper containing 75% recycled fibre content minimum. � Contents Contents � Section 1 Introduction 1 Section 2 Executive Summary 3 Section 3 Electricity 5 Section 4 Gas 22 Section 5 Oil 42 Section 6 Glossary 47 The information contained in this report constitutes general information about the outlook for energy markets. It is not intended to constitute advice for any specific situation. While every effort has been made to ensure the accuracy of the report,the opinions judgements, projections and assumptions it contains and on which it is based are inherently uncertain and subjective such that no warranty is given that the report is accurate, complete or up to date. -

M18.009 N33 Zuidbroek Appingedam V4

Second opinion Verdubbeling N33 Zuidbroek Appingedam Rapport 2018-9 Auteurs: Peter Louter Pim van Eikeren Opdrachtgevers: Projectorganisatie N33 Midden Contactpersonen bij opdrachtgevers: Theo Oenema en Bert van der Meulen Bureau Louter Rotterdamseweg 183c 2629 HD Delft Telefoon: 015-2682556 [email protected] www.bureaulouter.nl Niets uit deze uitgave mag worden verveelvoudigd, opgeslagen in een geautomatiseerd gegevensbestand of openbaar gemaakt in enige vorm of op enige wijze, hetzij elektronisch, mechanisch, door fotokopieën, opnamen, of enig andere manier, zonder voorafgaande schriftelijke toestemming van Bureau Louter. Verwijzing naar resultaten uit dit onderzoek is toegestaan, mits voorzien van een duidelijke bronvermelding, namelijk: ‘Bureau Louter (2018) Second opinion Verdubbeling N33 Zuidbroek Appingedam’ Inhoud 1 Inleiding 1 2 Overzicht mogelijke effecten 2 3 Ontwikkeling verkeersintensiteiten 4 4 Situatie en ontwikkeling economie en voorzieningen 9 4.1 Stromen 9 4.2 Structuur en ontwikkeling 14 Bijlagen I Kaartbeelden economische en demografische ontwikkeling 23 Bureau Louter, 3 juli 2018 M18.009 Second opinion Verdubbeling N33 Zuidbroek Appingedam 1 Inleiding De N33 tussen Appingedam (om precies te zijn de aansluiting op de N362) en Zuidbroek (de aansluiting op de A7) zal worden verdubbeld. Er is daarvoor een aantal alternatieven ontwikkeld. In het noordelijk deel (tussen Siddeburen: de aansluiting op de N387) en Appingedam zal, met uitzondering van alternatief A (behoud van het tracé, maar dubbel- in plaats van enkelbaans), ook het tracé worden verlegd. Het deel tussen de aansluiting op de N362 en de aansluiting op de Woldweg (N989) blijft bij de andere alternatieven gehandhaafd, maar het huidige tracé van de N33 ten zuiden van de aansluiting van de Woldweg verdwijnt. -

Digest of United Kingdom Energy Statistics 2017

DIGEST OF UNITED KINGDOM ENERGY STATISTICS 2017 July 2017 This document is available in large print, audio and braille on request. Please email [email protected] with the version you require. Digest of United Kingdom Energy Statistics Enquiries about statistics in this publication should be made to the contact named at the end of the relevant chapter. Brief extracts from this publication may be reproduced provided that the source is fully acknowledged. General enquiries about the publication, and proposals for reproduction of larger extracts, should be addressed to BEIS, at the address given in paragraph XXVIII of the Introduction. The Department for Business, Energy and Industrial Strategy (BEIS) reserves the right to revise or discontinue the text or any table contained in this Digest without prior notice This is a National Statistics publication The United Kingdom Statistics Authority has designated these statistics as National Statistics, in accordance with the Statistics and Registration Service Act 2007 and signifying compliance with the UK Statistics Authority: Code of Practice for Official Statistics. Designation can be broadly interpreted to mean that the statistics: ñ meet identified user needs ONCEñ are well explained and STATISTICSreadily accessible HAVE ñ are produced according to sound methods, and BEENñ are managed impartially DESIGNATEDand objectively in the public interest AS Once statistics have been designated as National Statistics it is a statutory NATIONALrequirement that the Code of Practice S TATISTICSshall continue to be observed IT IS © A Crown copyright 2017 STATUTORY You may re-use this information (not including logos) free of charge in any format or medium, under the terms of the Open Government Licence. -

180129 Vb Samenvatting Verd

Inpassingsvisie verdubbeling N33, samenvatting Zuidbroek-Appingedam Inleiding De N33 Midden tussen Zuidbroek en Appingedam wordt verdubbeld. Daarmee wordt aangesloten op het deel tussen Zuidbroek en Assen dat de afgelopen jaren al is aangepakt (de N33 Zuid). Deze Inpassingsvisie brengt de ruimtelijke kansen en knelpunten in beeld voor het gebied waar de N33 Midden wordt aangelegd. De visie vormt daarmee de basis voor de verdere planuitwerking, bij het opstellen en uitwerken van alternatieven en de ruimtelijke beoordeling in het MER. Daarnaast vormt de visie het fundament voor de uitwerking van het Voorkeursalternatief (in 2018) in een Landschapsplan. Het opstellen van de Inpassingsvisie is begeleid door Rijkswaterstaat en de provincie Groningen, alsmede door een klankbordgroep met daarin verschillende overheden en maatschappelijke groeperingen. Verder is een intensieve werksessie gehouden met inwoners en vertegenwoordigers van de dorpen Siddeburen (en omgeving) en Tjuchem. Zij worden ook bij het vervolg van de planontwikkeling betrokken. Naast verdubbelen en behoud van het huidige bestaand tracé en varianten B, tracé zijn vier andere alternatieven die alle een C, X1 en X2 andere doorsnijding van het gebied ten noorden van Tjuchem tonen. Alternatief B betreft een kortere route met bogen om Tjuchem heen. Alternatief C gaat met een aantal bogen naar het noorden. De alternatieven X1 en X2 zijn voorgesteld door een inwonerscollectief en passen zoveel mogelijk in de huidige verkavelingstructuur. Legenda analyse gebied De Inpassingsvisie bestaat uit drie open zeeklei landschap hoofdonderdelen: een analyse (van gebied, beleid en tracé), de Ruimtelijke Visie en de Duurswold; wisselend open en besloten Inpassingsvisie zelf. Deze drie onderdelen open zand/ veen landschap worden hieronder kort samengevat. -

Letter to the House of Representatives About Extraction

> Retouradres Postbus 20401 2500 EK Den Haag Directoraat-generaal Energie, Telecom & President of the House of Representatives Mededinging of the States General Directie Energiemarkt Binnenhof 4 Bezoekadres 2513 AA THE HAGUE Bezuidenhoutseweg 73 2594 AC Den Haag Postadres Postbus 20401 2500 EK Den Haag Factuuradres Postbus 16180 2500 BD Den Haag Overheidsidentificatienr 00000001003214369000 Datum T 070 379 8911 (algemeen) Betreft Extraction decree of gas extraction in The Groningen field and reinforcement measurements. www.rijksoverheid.nl/ez Ons kenmerk DGETM-EM / 14207601 Dear President, Uw kenmerk The consequences of years of gas extraction in Groningen are becoming increasingly clear. The number of earthquakes recorded in 2012, 2013 and 2014 Bijlage(n) (until 9 December) were 93, 119 and 77 respectively. In the same period there were a total of 20, 29 and 18 tremors respectively that measured more than 1.5 on the Richter scale. It is anticipated that the strength and frequency of the earthquakes will increase over the coming years. The consequences for houses, monuments and other buildings are plain to see. The Groningen field lies in the municipalities of Appingedam, Bedum, Bellingwedde, Delfzijl, Eemsmond, Groningen, Haren, Hoogezand-Sappemeer, Loppersum, Menterwolde, Oldambt, Pekela, Slochteren, Ten Boer and Veendam. The sense of having a safe living environment has been eroded in the area where there are (frequent) earthquakes. This deeply affects the daily life of the residents. At the same time, gas extraction is essential to our energy supply in the Netherlands. The great majority of Dutch households use Groningen gas for their heating and cooking. Gas extraction is also an important source of revenue for the Dutch state. -

Future UK Gas Security: a Position Paper

Future UK Gas Security: A Position Paper Professor Michael Bradshaw Future UK Gas Security: A Position Paper 1 Find out more about us Visit our website for the latest information on our courses, fees and scholarship opportunities, as well as our latest news, events, and to hear from former and current students what life is really like here at WBS. We’re always happy to talk through any queries you might have. T +44 (0)24 7652 4100 E [email protected] W wbs.ac.uk/go/mbalondon Join our conversation @warwickbschool wbs.ac.uk/go/joinus facebook.com/warwickbschool @warwickbschool warwickbschool 2 Future UK Gas Security: A Position Paper Contents Executive Summary 1 Introduction 3 Midstream Security Challenges 4 Downstream Security of 1.1 A Supply Chain Approach to UK Gas 3.1 Import Pipelines Demand Security 3.2 Onshore Pipelines 4.1 The Current Role of Natural Gas 1.2 Defining Energy Security 3.3 LNG Import Terminals 4.2 UKERC The Future Role of Natural 1.4 The EU’s Energy Security Strategy 3.4 Gas Storage Facilities Gas 1.4 Defining UK Energy Security 3.5 Interconnectors to Continental Europe 4.3 National Grid’s Future Energy 3.6 Interconnection to Ireland Scenario 2 Upstream Security of Supply 3.7 The National Balancing Point 4.4 Other Views in the Future of Gas 2.1 UK Gas Security of Supply 3.8 Future EU/UK Gas Governance 4.5 Decarbonised Gas 2.2 Increasing Import Dependence 3.9 Midstream Brexit Challenges 4.6 Brexit and the Future Role of Gas 2.3 The Role of Russian Gas 2.4 Production at Groningen 5 Conclusions: Brexit and Future 2.5 Prospects for the Future UK Gas Security 2.6 Exports and Interconnection 2.7 States and Markets References 2.8 Assessing UK Gas Security 2.9 Security of Supply Brexit Challenges About UKERC This report is supported by The UK Energy Research Centre (UKERC) the ESRC Impact Acceleration carries out world-class, interdisciplinary Account (Grant reference research into sustainable future energy ES/M500434/1) systems. -

The Political Economy of Energy Transitions

The Political Economy of Energy Transitions “Case studies of natural gas and offshore wind in the Netherlands and the United Kingdom” Student: Steven Blom (s4261690) Project: Master thesis Public Administration Program: Comparative Public Administration (COMPASS) University: Radboud University, Nijmegen, the Netherlands Faculty: Nijmegen School of Management Thesis supervisor Tutors: Dr. J. (Johan) De Kruijf Prof. dr. S. (Sandra) van Thiel Research assignment Client: Dr.ir. R.P.J.M. (Rob) Raven Position: Professor Institutions and Societal Transitions Department: Innovation studies department of Utrecht University Former position: Industrial Engineering & Innovation Sciences - Eindhoven University of Technology [TU/e] th Date: August 11 , 2015 1 Table of contents Abbreviations & acronyms ..................................................................................................................... 5 Prologue .................................................................................................................................................. 6 1. Introduction ........................................................................................................................................ 7 1.1 Introduction ................................................................................................................................... 7 1.2 Chapter’s structure ........................................................................................................................ 7 1.3 Problem description ..................................................................................................................... -

Besluitenlijst Gemeenteraad Gemeente Midden-Groningen D.D

Nr. 26357 31 januari GEMEENTEBLAD 2020 Officiële uitgave van de gemeente Midden-Groningen BESLUITENLIJST GEMEENTERAAD GEMEENTE MIDDEN-GRONINGEN D.D. 19 SEPTEMBER 2019 Voorzitter: A. Hoogendoorn Aanwezige raadsleden: PvdA: T. van der Veen Gemeentebelangen Midden-Groningen: H. Haze H.J. Flederus M. Ploeger J. Westerdiep J. Velthuis J. van Duren H. Loots R. Sinnema G.H. Akkerman-Ritsema SP: M. Feenstra VVD: M.E. Bos-Carabain H. Polat C.J.H. Ubels M. Kluit E.J.K. Offereins P.P.A. Nieland-Kampen ChristenUnie: M.T. Metscher CDA: A.P.A. van der Burg-Versteeg H.B. van Dijk F. Bos N. Joostens M.W. van der Meijden L. Doorn H. Wind GroenLinks: A.D. Bosscher D66: G.H. Renkema Y.P. Lutterop Leefbaar Midden-Groningen: F.A. Kruzenga Griffier: F.M. Bouwman m.k.a. - M.E. Bosman (GroenLinks) - K.W. Koning (SP) - N.R. van der Vlist Aldus vastgesteld in de openbare vergadering van 17 oktober 2019 De raad van de gemeente Midden-Groningen A. Hoogendoorn F.M. Bouwman Voorzitter Raadsgriffier 1. Opening De voorzitter opent de vergadering om 19.30 uur. 2. Vaststellen agenda Agendapunt 17 betreffende subsidieverordening Fonds kwaliteitsimpuls Overschild Midden-Groningen 2019 wordt geplaatst na punt 7 op de agenda als eerste inhoudelijk bespreekpunt. Verder dient de SP een motie vreemd aan de orde van de dag in betreffende de vergunningen Windpark N33. Dit agendapunt wordt als punt 18 op agenda geplaatst. De agenda wordt met deze wijzigingen vastgesteld. 3. Inventarisatie spreekrecht burgers 1 Gemeenteblad 2020 nr. 26357 31 januari 2020 - De heer De Bey: n.a.v. -

Ofgem's Probe Into Wholesale Gas Prices Appendices

Ofgem’s probe into wholesale gas prices Appendices October 2004 232/04b This report contains Appendices 1 to 5 to the main report on Ofgem’s probe into wholesale gas prices. These Appendices expand on the information and the analysis presented in the main report and can be read as stand alone documents. Table of Contents Appendix 1. October/November 2003 probe: Analysis of causes of reduced UK gas supply ..........................................................................................................................2 Appendix 2. October/ November 2003 probe: European gas supply and the interconnector............................................................................................................ 24 Appendix 3. October/ November 2003: Effects of reduced gas supply on prices ......... 50 Appendix 4. August/September 2004: Analysis of gas prices....................................... 62 Appendix 5. Winter 2004/05 forward gas prices: Analysis .......................................... 80 Appendix 1. October/November 2003 probe: Analysis of causes of reduced UK gas supply 1.1 This chapter presents a summary of Ofgem’s further analysis of the causes of the reduced UKCS gas supply availability in October/November 2003. The section begins by summarising the position in the Interim Report,1 presents Ofgem’s further analysis for each sub-terminal and provides key conclusions. Interim report 1.2 From analysis presented in Ofgem’s Interim Report it was evident that the volumes of gas supplied via six beach terminals (in minimum, maximum and average terms) were significantly lower in October and November 2003 than in the same period of the previous year; both in terms of the total volume of gas delivered and in terms of maximum flow rates. 1.3 At five sub-terminals (Bacton-Tullow, Bacton-Shell, Bacton-Perenco, St Fergus- Shell and Teesside-BP Amoco), flows during October or November 2003 were significantly lower than the same months of 2002 and/or an assessment of the maximum deliverability for Winter 2003/04. -

Northeast Groningen Confronting the Impact of Induced Earthquakes, Netherlands

Resituating the Local in Cohesion and Territorial Development House in Bedum, damaged by earthquakes (Photo: © Huisman Media). Case Study Report Northeast Groningen Confronting the Impact of Induced Earthquakes, Netherlands Authors: Jan Jacob Trip and Arie Romein, Faculty of Architecture and the Built En- vironment, Delft University of Technology, the Netherlands Report Information Title: Case Study Report: Northeast Groningen. Confronting the Impact of Induced Earthquakes, Netherlands (RELOCAL De- liverable 6.2) Authors: Jan Jacob Trip and Arie Romein Version: Final Date of Publication: 29.03.2019 Dissemination level: Public Project Information Project Acronym RELOCAL Project Full title: Resituating the Local in Cohesion and Territorial Develop- ment Grant Agreement: 727097 Project Duration: 48 months Project coordinator: UEF Bibliographic Information Trip JJ and Romein A (2019) Northeast Groningen. Confronting the Impact of Induced Earthquakes, Netherlands. RELOCAL Case Study N° 19/33. Joensuu: University of Eastern Finland. Information may be quoted provided the source is stated accurately and clearly. Reproduction for own/internal use is permitted. This paper can be downloaded from our website: https://relocal.eu i Table of Contents List of Figures .................................................................................................................. iii List of Tables .................................................................................................................... iii Abbreviations ................................................................................................................. -

Daily Energy Report

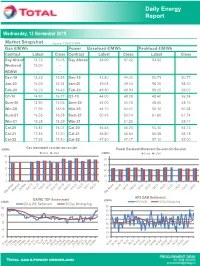

Daily Energy Report Wednesday, 13 November 2019 Market Snapshot Source: TGP/ICE/APX Gas €/MWh Power Baseload €/MWh Peakload €/MWh Contract Latest Close Contract Latest Close Latest Close Day Ahead 14.73 15.05 Day Ahead 48.00 47.42 53.50 - Weekend 15.00 - WDNW - - Dec-19 15.33 15.55 Dec-19 43.80 44.00 50.75 50.77 Jan-20 16.03 16.24 Jan-20 49.05 49.04 58.20 58.10 Feb-20 16.23 16.43 Feb-20 49.90 49.93 59.20 59.02 Q1-10 14.93 16.27 Q1-10 44.00 48.08 48.40 56.24 Sum-20 14.90 15.05 Sum-20 44.00 44.15 48.40 48.10 Win-20 17.95 18.09 Win-20 44.10 44.41 50.10 50.38 Sum-21 16.53 16.58 Sum-21 50.45 50.14 61.60 61.74 Win-21 18.28 18.29 Win-21 - 51.25 - 59.17 Cal-20 15.87 16.01 Cal-20 46.65 46.70 54.30 54.13 Cal-21 17.45 17.40 Cal-21 46.80 46.64 55.35 55.18 Cal-22 17.35 17.40 Cal-22 47.50 47.17 57.10 57.00 €/MWh Gas movement session-on-session Power Baseload Movement Session-On-Session Close Latest €/MWh Close Latest 20 80 15 60 10 40 5 20 0 0 APX DAM Settlement DA/WE TGP Assessment €/MWh €/MWh APX DAM 30 Day Moving Avg DA & WE Settlement 30 Day Moving Avg 16 55 50 12 45 40 8 35 4 30 25 0 20 Daily Energy Report Gas Overview NW Europe DA Assessment TTF vs NBP/ZEE/NCG Basis Source: Thomson Reuters Source: Thomson Reuters ZEE NCG TTF NBP TTF vs ZEE TTF vs NBP NBP vs ZEE €/MWh €/MWh TTF vs NCG NBP vs TTF 18.00 3.0 2.5 16.00 2.0 14.00 1.5 1.0 12.00 0.5 0.0 10.00 -0.5 8.00 -1.0 -1.5 6.00 -2.0 Russian vs Norwegian Flows to NWE Forecasted Continental Demand Source: Thomson Reuters Source: Thomson Reuters GWh/d Total Imports from Norway Russia Main Three Lines