Activate Tech & Media Outlook 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Wanna Be a Star Unit 6

Unit Wanna be a star In this unit you are going to 6 talk about YouTube stars (Speaking A2) give advice (Speaking A2) write an argumentative text about the pros and cons of being a teenage millionaire (Writing B1) read biographies of different YouTube stars (Reading A2 / B1) listen to an interview with a teenage Yahoo millionaire (Listening B1) listen to three friends giving advice on feeling confident in a job interview (Listening A2 / B1) practise trouble-free grammar: Passive constructions (Language in use A2) boost your vocabulary: Engaging in small talk Warm-up Collocations with make, do, have Talking about teenage YouTube stars PewDiePie, Macbarbie07, LeFloid, Tyler Oakley and Sawyer Hartman are stars of a less traditional kind. They are part of the Generation YT (YouTube), attracting millions of subscribers and making lots of money. 1 Get in pairs and answer the following questions. Use the phrases from the LanguageBox. What do you use YouTube for? What are positive and negative aspects of YouTube? Who are YouTube stars and what do they do? How do they make money? Are you a subscriber of one or more YouTube channels? If yes, name them and say what you like about them. If not, what does a channel need to offer for you to subscribe? LanguageBox I use YouTube for listening / watching / getting … In my view the positive aspects of YouTube are … Talking about the negative aspects of YouTube, it can be said that … YouTube stars are … who … I have subscribed to … channels and my favourite is … because … I have not subscribed to any channel yet because … 2 Get in groups of three and answer the following questions. -

Sources & Data

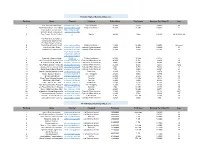

YouTube Highest Earning Influencers Ranking Name Channel Category Subscribers Total views Earnings Per Video ($) Age 1 JoJo https://www.youtube.com/channel/UCeV2O_6QmFaaKBZHY3bJgsASiwa (Its JoJo Siwa) Life / Vlogging 10.6M 2.8Bn 569112 16 2 Anastasia Radzinskayahttps://www.youtube.com/channel/UCJplp5SjeGSdVdwsfb9Q7lQ (Like Nastya Vlog) Children's channel 48.6M 26.9Bn 546549 6 Coby Cotton; Cory Cotton; https://www.youtube Garrett Hilbert; Cody Jones; .com/user/corycotto 3 Tyler Toney. (Dude Perfect) n Sports 49.4M 10Bn 186783 30,30,30,33,28 FunToys Collector Disney Toys ReviewToys Review ( FunToys Collector Disney 4 Toys ReviewToyshttps://www.youtube.com/user/DisneyCollectorBR Review) Children's channel 11.6M 14.9Bn 184506 Unknown 5 Jakehttps://www.youtube.com/channel/UCcgVECVN4OKV6DH1jLkqmcA Paul (Jake Paul) Comedy / Entertainment 19.8M 6.4Bn 180090 23 6 Loganhttps://www.youtube.com/channel/UCG8rbF3g2AMX70yOd8vqIZg Paul (Logan Paul) Comedy / Entertainment 20.5M 4.9Bn 171396 24 https://www.youtube .com/channel/UChG JGhZ9SOOHvBB0Y 7 Ryan Kaji (Ryan's World) 4DOO_w Children's channel 24.1M 36.7Bn 133377 8 8 Germán Alejandro Garmendiahttps://www.youtube.com/channel/UCZJ7m7EnCNodqnu5SAtg8eQ Aranis (German Garmendia) Comedy / Entertainment 40.4M 4.2Bn 81489 29 9 Felix Kjellberg (PewDiePie)https://www.youtube.com/user/PewDiePieComedy / Entertainment 103M 24.7Bn 80178 30 10 Anthony Padilla and Ian Hecoxhttps://www.youtube.com/user/smosh (Smosh) Comedy / Entertainment 25.1M 9.3Bn 72243 32,32 11 Olajide William Olatunjihttps://www.youtube.com/user/KSIOlajidebt -

CMS.701S15 Final Paper Student Examples

Current Debates In Digital Media Undergraduate Students Final Papers Edited by Gabrielle Trépanier-Jobin August, 2015 1 Table of Content Introduction Gabrielle Trépanier-Jobin CHAPTER 1 YouTube’s Participatory Culture: Online Communities, Social Engagement, and the Value of Curiosity By an MIT student. Used with permission. CHAPTER 2 Exploring Online Anonymity: Enabler of Harassment or Valuable Community-Building Tool? By an MIT student. Used with permission. CHAPTER 3 When EleGiggle Met E-sports: Why Twitch-Based E-Sports Has Changed By an MIT student. Used with permission. CHAPTER 4 Negotiating Ideologies in E-Sports By Ryan Alexander CHAPTER 5 The Moral Grey Area of Manga Scanlations By an MIT student. Used with permission. CHAPTER 6 The Importance of Distinguishing Act from Actor: A Look into the the Culture and Operations of Anonymous By Hannah Wood 2 INTRODUCTION By Gabrielle Trépanier-Jobin, PhD At the end of the course CMS 701 Current Debates in Media, students were asked to submit a 15 pages dissertation on the current debate of their choice. They had to discuss this debate by using the thesis/antithesis/synthesis method and by referring to class materials or other reliable sources. Each paper had to include a clear thesis statement, supporting evidence, original ideas, counter-arguments, and examples that illustrate their point of view. The quality and the diversity of the papers were very impressive. The passion of the students for their topic was palpable and their knowledge on social networks, e-sports, copyright infringment and hacktivism was remarkable. The texts published in this virtual booklet all received the highest grade and very good comments. -

Table File Items for January 26, 2015, Regular School Board Meeting

NORTHFIELD PUBLIC SCHOOLS Office of the Superintendent Memorandum TO: Board of Education FROM: L. Chris Richardson, Ph.D., Superintendent RE: Table File Items for January 26, 2015, Regular School Board Meeting VII. Superintendent’s Report B. Items for Consent Grouping 2. Personnel Items. a. Appointments * 7. Pam Hanson (Swanson), GenEd Educational Assistant at die High School for 6 hours/day beginning 01/28/2015; Step 1, $13.21/hour. 8. Katrina Warner, GenEd Educational Assistant/Sibcare at the NCRC/ECFE for up to 8 hours/week beginning 01/28/2015; Step 1, $13.21/hour. 9. Community Sendees Fall/Winter/Spring Recreation positions beginning 01/24/2015 — 05/31/2015:_Savannah Dimick, Basketball Supervisor beginning 02/07/2015 - 05/31/2015; $10/hour; Michael Kopp - Birthday Party Staff beginning 01/24/2015 — 05/31/2015; $8/hour. b. Increase/Decrease/Cliange in Assignment 11. David Kurth, Evening Engineer/Security at the Middle School, change to Custodial Engineer (Day Shift) at the Middle School beginning 02/02/2015. c. Resignations/Retirements 7. Katie Bauernfeind, Building Nurse at Prairie Creek, Arcadia and St. Dominic’s, resignation effective 01/20/2015. 8. Robert McCarthy, Special Education Teacher at the High School, resignation effective 01/26/2015. * Conditional offers of employment arc subject to successful completion of a criminal background check. Northfield Charter Schools Arcadia«* Data Sheet CI H A R TE R S C H O O L J Minnesofii ('ompi'cliciishc Assessments Arcadia Charter School Mission 2014 MCA Scores It is the mission of Arcadia Charter School to prepare our stu 2012 2013 2014 dents to transition intellectually, emotionally, and ethically to — 70.7%| 67.7% higher education and future employment. -

Youtube Marketing: Legality of Sponsorship and Endorsement in Advertising Katrina Wu, University of San Diego

From the SelectedWorks of Katrina Wu Spring 2016 YouTube Marketing: Legality of Sponsorship and Endorsement in Advertising Katrina Wu, University of San Diego Available at: http://works.bepress.com/katrina_wu/2/ YOUTUBE MARKETING: LEGALITY OF SPONSORSHIP AND ENDORSEMENTS IN ADVERTISING Katrina Wua1 Abstract YouTube endorsement marketing, sometimes referred to as native advertising, is a form of marketing where advertisements are seamlessly incorporated into the video content unlike traditional commercials. This paper categorizes YouTube endorsement marketing into three forms: (1) direct sponsorship where the content creator partners with the sponsor to create videos, (2) affiliated links where the content creator gets a commission resulting from purchases attributable to the content creator, and (3) free product sampling where products are sent to content creators for free to be featured in a video. Examples in each of the three forms of YouTube marketing can be observed across virtually all genres of video, such as beauty/fashion, gaming, culinary, and comedy. There are four major stakeholder interests at play—the YouTube content creators, viewers, YouTube, and the companies—and a close examination upon the interplay of these interests supports this paper’s argument that YouTube marketing is trending and effective but urgently needs transparency. The effectiveness of YouTube marketing is demonstrated through a hypothetical example in the paper involving a cosmetics company providing free product sampling for a YouTube content creator. Calculations in the hypothetical example show impressive return on investment for such marketing maneuver. Companies and YouTube content creators are subject to disclosure requirements under Federal law if the content is an endorsement as defined by the Federal Trade Commission (“FTC”). -

![Youtube Brandcast [2012-Present]](https://docslib.b-cdn.net/cover/0648/youtube-brandcast-2012-present-1650648.webp)

Youtube Brandcast [2012-Present]

goodsense.nyc CREATIVE & PRODUCTION SERVICES makes good sense. We love to create and execute events. We're all about big ideas, and creative collaboration. We create events that tell stories, market brands, position new products, and resonate with target audiences. GOOD SENSE & COMPANY is a creative and production agency that designs and manages live events for some We’re a full-service agency that provides whatever kind of service our of the biggest corporate and nonprofit entities in the clients need, from simple AV for a single event to a full-scale, world. multi-million dollar production. From the start, we've been tasked with large-scale, visionary projects, and we refined our craft, working on high-stakes, high-profile events: award shows, A-list concerts and GOOD SENSE & COMPANY is founded on the multi-venue festivals. complementary partnership of Jared Siegel and Joshua Cicerone. The company model is based on their own We love design that has meaning and purpose. We approach each archetypal dynamic: diplomat and agitator, dreamer and project as an exploration into the goals and aesthetics of the technician. For over a decade they have produced live company, brand, or product in need. We love new technology and events together, leading a team of talented individuals bring it in when and where it makes sense within a design. Our core that love to put on a good show. philosophy is focused on making our clients look good. We take one-off projects but where we truly thrive is in our long-term relationships. Regardless of project scope, we support all our clients with the same level of creativity, attention, and thought. -

Thornridge High School 15000 Cottage Grove Avenue Dolton, IL Volume 56 Issue 4 THORNRIDGE

Thornridge High School 15000 Cottage Grove Avenue Dolton, IL Volume 56 Issue 4 THORNRIDGE bAGPIPE MAY 2016 mR. dunn forever in our hearts to help our young people enjoy Never Forgotten: some of those same successes. Mr. Otis Dunn He will be dearly missed. By Kashleigh Redd He was a fantastic gentleman, friend, colleague, and Thorn- In March of 2016, Thorn- ridge High School is definitely ridge High School suffered all the worse for wear because a great loss. One of our long of his untimely passing. May standing staff members sud- he Rest in Peace.” denly passed away. Mr. Otis Dunn, had been a staff mem- Mr. Wafford- “What I miss ber since 2000. His last posi- about Mr. Dunn is being able tion was that of the Truancy to just sit there and talk family, Officer. The staff who knew occasionally sports but mainly him best had this to say when family.” asked, “What is your most cherished memory of Mr. Ms. Ousley- “I liked that Mr. Dunn?”: Dunn is very personable and down to earth. Makes you Mr. Broom - “I am the truan- feel comfortable talking to cy officer that has the task of taking over for Mr. Dunn after him. He would relate differ- his untimely passing. I knew ent things to real life stories. Mr. Dunn for probably, almost He was just very personable. twenty years. We worked to- I will miss his stories and gether over at Thornton. What talking to him about every- I remember most about him was his uplifting spirit and he thing. -

An Exploratory Thematic Analysis on Viewers’ Involvement with Haul Video Personaes---Taking Bethany Mota As a Case Study

AN EXPLORATORY THEMATIC ANALYSIS ON VIEWERS’ INVOLVEMENT WITH HAUL VIDEO PERSONAES---TAKING BETHANY MOTA AS A CASE STUDY BY LEI WANG A Thesis Submitted to the Graduate Faculty of WAKE FOREST UNIVERSITY GRADUATE SCHOOL OF ARTS AND SCIENCES in Partial Fulfillment of the Requirements for the Degree of MASTER OF ARTS Communication December, 2015 Winston-Salem, North Carolina Approved By: Michael Hazen, Ph.D., Advisor Ananda Mitra, Ph.D., Chair James Narus, Ph.D. ACKNOWLEDGEMENT To my family: Thank you very much for your love, motivation and constant support. I am beyond grateful for having you as my parents and always trusting me and allowing me to chase my dreams. Also thanks to my husband who helped me to better balance between work, family and this project and to his generous help of pulling the data by using his coding skills. To my advisor, Dr. Michael Hazen, It has been such an honor to have worked alongside you throughout my entire program. Thank you for being such an incredible teacher while I took your classes for three semesters and worked on projects with you. I have never been so stretched to see the world through a new lens. Thank you for mentoring me and molding me into a better thinker, and also for all your help and guidance concerning the literature review, the method, the dataset, the sample, and the analysis. To my committee: Dr. Ananda Mitra and Dr. Jim Narus, thank you very much for your mentorship, support, and guidance throughout my completion of the thesis. Thank you very much again for sacrificing your time to help me make this project possible. -

Global Perspectives Podcast Trends and Issues in Australia and Beyond: Global Perspectives

PODCAST TRENDS AND ISSUES IN AUSTRALIA AND BEYOND: GLOBAL PERSPECTIVES PODCAST TRENDS AND ISSUES IN AUSTRALIA AND BEYOND: GLOBAL PERSPECTIVES Yoonmo Sang Jee Young Lee Sora Park For further information, please contact [email protected] Published by the News & Media Research Centre, Canberra, Australia. © 2020 by News & Media Research Centre ISBN: 978-1-74088-510-2 DOI: 10.25916/sgv0-qh32 Cite as: Sang, Y., Lee, J.Y., & Park, S. (2020). Podcast Trends and Issues in Australia and Beyond: Global Perspectives. Canberra: News & Media Research Centre, University of Canberra. Report designed by Zita Leung DIGITAL NEWS REPORT: AUSTRALIA Digital News Report (DNR): Australia is an annual report published by the News and Media Research Centre at the University of Canberra. The N&MRC is the Australian partner institute of the Reuters Institute for the Study of Journalism, University of Oxford. This report is the first of N&MRC DNR Special Report Series in 2020. REUTERS INSTITUTE DIGITAL NEWS REPORT The Reuters Institute Digital News Report is an annual report about digital news consumption based on a YouGov survey of over 80,000 online news consumers in 40 markets. The News & Media Research Centre is the Australian partner of this study. NEWS & MEDIA RESEARCH CENTRE The N&MRC advances understanding of the changing media environment. Our research focuses on digital news consumption and the impacts of digital technology on journalism, politics, and society. Research occurs in three hubs: the Digital News+ Lab; the Critical Conversations Lab; and the Media Cultures Lab. The Centre conducts both critical and applied research projects with partners and institutions in Australia and internationally. -

Long-Form Improv Practices in US Comedy Podcast Culture Smith, AN

Achieving a depth of character : long-form improv practices in US comedy podcast culture Smith, AN http://dx.doi.org/10.1080/2040610X.2019.1623500 Title Achieving a depth of character : long-form improv practices in US comedy podcast culture Authors Smith, AN Type Article URL This version is available at: http://usir.salford.ac.uk/id/eprint/51264/ Published Date 2019 USIR is a digital collection of the research output of the University of Salford. Where copyright permits, full text material held in the repository is made freely available online and can be read, downloaded and copied for non-commercial private study or research purposes. Please check the manuscript for any further copyright restrictions. For more information, including our policy and submission procedure, please contact the Repository Team at: [email protected]. Achieving a depth of character: Long-form improv practices in US comedy podcast culture Anthony N. Smith Long-form improvised comedy – or long-form improv – has been enduringly significant across media cultures since its development in 20th Century North American theatrical contexts. The comedic mode has been formative to the early development of various successful and influential comedy performers, writers and producers in recent decades, including Mike Myers, Tina Fey, Amy Poehler and Adam McKay (Fotis 2014, 7). It has influenced the scripting and performance processes of many US film comedies, including Anchorman and Knocked Up, and US television sitcoms, such as 30 Rock and Curb Your Enthusiasm.1 It has furthermore recently spread into podcast culture, underpinning various popular podcast series, including Comedy Bang! Bang!, which garners upwards of two million episode downloads per month (Wilstein, 2017). -

Senators Sample Letter

May 6, 2019 The Honorable Richard Blumenthal U.S. Senate 706 Hart Senate Office Building Washington, DC 20510 The Honorable Edward Markey U.S. Senate 255 Dirksen Senate Office Building Washington, DC 20510 The Honorable Chris Van Hollen U.S. Senate 110 Hart Senate Office Building Washington, DC 20510 Senator Blumenthal, Senator Markey, and Senator Van Hollen, Thank you for your April 1, 2019 letter regarding tobacco imagery in Amazon’s video content. Amazon is a customer-obsessed company and we appreciate your interest in the important topic of underage tobacco use. Below we have highlighted the tools that we provide customers to select appropriate content for their households. We are available to discuss these issues further with your offices if you have any questions. Today, the Amazon Prime Video catalog available to customers in the United States contains tens of thousands of titles, including Amazon Originals as well as third-party licensed movies and television series from content providers around the world. Our content selection is always changing; due to the size and dynamic nature of our catalog and the lack of an industry standard mechanism for identifying tobacco-specific data within content, we are unable to provide a title by title assessment on the presence of tobacco imagery or dialogue. However, individual maturity ratings are displayed on the detail page for the title within the catalog. Amazon Prime Video’s goal is to deliver the broadest selection of premium content to our customers to stream, purchase, or rent while also ensuring that we provide the information necessary to allow customers to make informed decisions about what content is appropriate for them and their households. -

Seven Podcasts Join Earwolf As It Celebrates 500Th Episode of “Comedy Bang! Bang!”

Seven podcasts join Earwolf as it celebrates 500th episode of “Comedy Bang! Bang!” July 24, 2017 NEW YORK CITY – Podcast industry leader Midroll Media has unveiled its late-summer lineup of new programming for comedy network Earwolf, including a first-of-its-kind improvised musical podcast, a dating tell-all and a radio favorite available for the first time to podcast listeners. The expanded roster reflects Earwolf’s commitment to building a network that’s home to a diverse group of both established and up-and-coming comedic talent. The announcement comes as Earwolf and host Scott Aukerman celebrate the 500th episode of “Comedy Bang! Bang!”, the network’s flagship podcast and one of the industry’s longest-running and most popular comedy shows. The podcast has long served as an incubator for comedy talent, with regular guests including Lauren Lapkus, Paul Rust, Jessica St. Clair and Lennon Parham having boosted their early careers through appearances on the show. The 500th episode of “Comedy Bang! Bang!” is available July 24 and features special guests Lapkus, Jon Gabrus, Nick Kroll, Jason Mantzoukas, Mary Holland and Paul F. Tompkins. “We’re excited to celebrate ‘Comedy Bang! Bang!’, the show that created the world of comedy podcasting and is still going strong at 500 episodes,” said Chris Bannon, chief content officer for Midroll Media. “And I’m delighted that, after seven years, Earwolf is still working with the best performers in comedy to create brand new shows for all the listeners coming into podcasting today.” The Earwolf summer launches include: • “Off Book” is the first-ever improvised musical podcast, featuring rising improvisational comedy stars Jessica McKenna (a regular “Comedy Bang! Bang!” guest) and Zach Reino (co-star and co- writer of numerous UCB productions).