Study of the North American MARC Records Marketplace

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Download on the AASL Website an Anonymous Funder Donated $170,000 Tee, and the Rainbow Round Table at Bit.Ly/AASL-Statements

May 2021 THE MAGAZINE OF THE AMERICAN LIBRARY ASSOCIATION MARSHALL BREEDING’S LIBRARY SYSTEMS REPORTp. 22 Library Jobs Landscape p. 34 NEWSMAKER: Isabel Allende p. 20 PLUS: Drive-In Storytimes, Rural Telehealth, Bike Tour Librarian This Summer! Join us online at the event created and curated for the library community. Event Highlights • Educational programming • COVID-19 information for libraries • News You Can Use sessions highlighting • Interactive Discussion Groups new research and advances in libraries • Presidents' Programs • Memorable and inspiring featured authors • Livestreamed and on-demand sessions and celebrity speakers • Networking opportunities to share and The Library Marketplace with more than • connect with peers 250 exhibitors, Presentation Stages, Swag-A-Palooza, and more • Event content access for a full year ALA Members who have been recently furloughed, REGISTER TODAY laid o, or are experiencing a reduction of paid alaannual.org work hours are invited to register at no cost. #alaac21 Thank you to our Sponsors May 2021 American Libraries | Volume 52 #5 | ISSN 0002-9769 COVER STORY 2021 LIBRARY SYSTEMS REPORT Advancing library technologies in challenging times | p. 22 BY Marshall Breeding FEATURES 38 JOBS REPORT 34 The Library Employment Landscape Job seekers navigate uncertain terrain BY Anne Ford 38 The Virtual Job Hunt Here’s how to stand out, both as an applicant and an employer BY Claire Zulkey 42 Serving the Community at All Times Cultural inclusivity programming during a pandemic BY Nicanor Diaz, Virginia Vassar -

Cost Summary/Proposal

The Library Corporation Proposal for Penitas Public Library Cost Summary for Penitas Public Library to join Hidalgo County Library System Library Sites 1 Technical Services Stations 1 Public Access Catalog Stations Unlimited Bibliographic Records 6,000 1st Year 2nd Year Costs Costs* Software: Library•Solution Integrated Software Package $ 3,500.00 $ 700.00 LS2 Staff Included Included LS2 PAC Included Included LS2 Kids Included Included LS2 Mobile Included Included Library•Z (Z39.50 server) Included Included Oracle Database Licensing Included Included Reports Manager (one user license per site) Included Included Services: Data Preparation ($.20/rec) $ 1,200.00 AuthorityWorks: Authority Control Processing and Automatic Updates Included Included Installation $ 1,200.00 Total 1st Year Costs$ 5,900.00 Total 2nd Year Costs $ 700.00 The costs in this proposal are guaranteed for 30 days. Additional costs may apply for installation if hardware is not purchased from TLC. Annual support after year 2 will not increase more than 5% per year. Payment terms are 25% at time of order with remainder due net 30 following installation. This summary is not derived from our GSA pricing as it is for the addition of a location to an existing GSA contracted system. The subsequent addition of a site is not part of our GSA pricing. Since this is an addition to an existing system, the software, installation and data prep services are only compatible with an existing TLC system and should therefore be considered as conforming to the requirements of a sole source purchase. TLC Proprietary/Confidential January 2, 2012 Page 1 The Library Corporation Proposal for Penitas Public Library Library#Solution® Software The Library#Solution Integrated Software Package includes: • Oracle database licensing • Integrated Authority Control with access to national authority files • Cataloging with Z39.50 client and Cataloger's Reference Shelf • Circulation with inventory control • Public Access Catalog with web access. -

Next Generation Integrated Library System (NGS/ILS) and Discovery Services (DS):System Equipment/Hardware

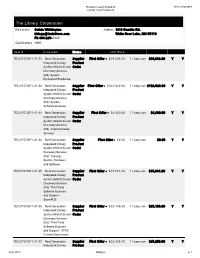

%URZDUG&RXQW\%RDUGRI 7(&3 &RXQW\&RPPLVVLRQHUV 7KH/LEUDU\&RUSRUDWLRQ %LG&RQWDFW Calvin Whittington $GGUHVV 1818 Buerkle Rd. [email protected] White Bear Lake, MN 55110 Ph 304-229 - 4XDOLILFDWLRQV :%( ,WHP /LQH,WHP Notes 8QLW3ULFH 4W\8QLW 7RWDO3ULFH $WWFK 'RFV 7(&3--01- 1H[W*HQHUDWLRQ Supplier First Offer - OXPSVXP $39,808.00 Y Y Integrated Library Product System (NGS/ILS) and Code: Discovery Services (DS): System (TXLSPHQW+DUGZDUH 7(&3--01- 1H[W*HQHUDWLRQ Supplier First Offer - OXPSVXP $102,920.00 Y Y Integrated Library Product System (NGS/ILS) and Code: Discovery Services (DS): System 6RIWZDUH/LFHQVHV 7(&3--01- 1H[W*HQHUDWLRQ Supplier First Offer - OXPSVXP $4,800.00 Y Y Integrated Library Product System (NGS/ILS) and Code: Discovery Services (DS): Implementation 6HUYLFHV 7(&3--01- 1H[W*HQHUDWLRQ Supplier First Offer - OXPSVXP $0.00 Y Y Integrated Library Product System (NGS/ILS) and Code: Discovery Services (DS): Training - System Hardware DQG6RIWZDUH 7(&3--01- 1H[W*HQHUDWLRQ Supplier First Offer - OXPSVXP $15,881.00 Y Y Integrated Library Product System (NGS/ILS) and Code: Discovery Services (DS): Third - Party Software Licenses and Support - 6Z\HU326 7(&3--01- 1H[W*HQHUDWLRQ Supplier First Offer - OXPSVXP $25,159.00 Y Y Integrated Library Product System (NGS/ILS) and Code: Discovery Services (DS): Third - Party Software Licenses and Support - OPAC &RQWHQW(QULFKPHQW 7(&3--01- 1H[W*HQHUDWLRQ Supplier First Offer - OXPSVXP $25,256.00 Y Y Integrated Library Product %LG6\QF S %URZDUG&RXQW\%RDUGRI 7(&3 g y &RXQW\&RPPLVVLRQHUV System -

RFP Response

Region 10 ESC RFP #R10-1118 Submitted by: TLC & Tech Logic Research Park Inwood, WV USA 25428 Toll-Free: 800.325.7759 Fax: 304.229.0295 Contents COVER LETTER ............................................................................. 4 PROPOSAL FORM 1: ATTACHMENT B - PRICING ...................... 6 PROPOSAL FORM 2: QUESTIONNAIRE ...................................... 7 COMPANY PROFILE .................................................................................. 7 PRICING/PRODUCTS/SERVICES OFFERED .............................................. 11 PERFORMANCE CAPABILITIES: ............................................................... 21 PROPOSAL FORM 3: DIVERSITY VENDOR CERTIFICATION PARTICIPATION ........................................................................... 34 PROPOSAL FORM 4: MANAGEMENT PERSONNEL ................. 35 PROPOSAL FORM 5: REFERENCES AND EXPERIENCE QUESTIONNAIRE ......................................................................... 39 QUESTIONS:.......................................................................................... 41 PROPOSAL FORM 6: VALUE ADD QUESTIONNAIRE ............... 42 PROPOSAL FORM 7: CLEAN AIR WATER ACT ......................... 45 PROPSAL FORM 8: DEBAREMENT NOTICE .............................. 46 PROPOSAL FORM 9: LOBBYING CERTIFICATION ................... 47 PROPOSAL FORM 10: CONTRACTOR CERTIFICATION REQUIREMENTS .......................................................................... 48 PROPOSAL FORM 11: ANTITRUST CERTIFICATION STATEMENTS ............................................................................. -

Interlocal Services Agreement Between the City of Sedro-Woolley and the Central Skagit Rural Partial County Library District

INTERLOCAL SERVICES AGREEMENT BETWEEN THE CITY OF SEDRO-WOOLLEY AND THE CENTRAL SKAGIT RURAL PARTIAL COUNTY LIBRARY DISTRICT This Interlocal Services Agreement (the "Agreement"), is by and between the City of Sedro-Woolley, (hereinafter "City") and the Central Skagit Rural Partial County Library District (hereinafter "District"). A. RECITALS WHEREAS, the parties find that it will be mutually beneficial for the City to purchase certain services for the benefit of both the City and the District; and WHEREAS, the parties agree that the City's provision of such services will result in more efficient, effective, and less costly services for citizens within both entities' service areas, thereby better serving the public: and WHEREAS, the parties are currently engaged in a partnership formalized through a series of three Interlocal Agreements that will ultimately result in the construction of a New Library to be operated by the District for the benefit of both parties' residents; and WHEREAS, the parties are currently signatories to an interlocal agreement that provides for reciprocal library borrowing; and WHEREAS, the City has the technical ability and is qualified to provide the services described in this Agreement, and WHEREAS. both parties are authorized by law to provide the services set forth in this Agreement.. and WHEREAS, the Interlocal Cooperation Act, RCW 39.34, specifically authorizes public entities to work together to better serve the public; NOW, THEREFORE, in consideration of the mutual promises, covenants and provisions contained in this Agreement and the mutual benefits to be derived therefrom, the parties agree as follows: B. DEFINITIONS 1. City means the City of Sedro-Woolley. -

Library Resources Technical Services&

Library Resources Technical Services& ISSN 0024-2527 January 2004 Volume 48, No. 1 Editorial 3 Peggy Johnson ARTICLES Association for Library Collections and Technical Services 4 Annual Report 2002/2003 Olivia M. A. Madison, ALCTS President Cataloging Electronic Books 12 Robert Bothmann About the cover: Sherman, Nathan. Paper to PDF 20 “Young and Old Visit the Making License Agreements Accessible through the OPAC Library on the Parkway.” March 27, 1937. Work Marie R. Kennedy, Michele J. Crump, and Douglas Kiker Projects Administration Poster Collection (Library Collection Development and Maintenance across 26 of Congress). [cph Libraries, Archives, and Museums 3b51496] (12/17/03). A Novel Collaborative Approach This cover is available through the Library of Phillip M. Edwards Congress American Memories, Historical The Administration and Management of Integrated 34 Collection of the Library Systems National Digital Library at http://memory.loc. A Survey and Results gov/. Rosann Bazirjian An omission from LRTS Evaluative Study of Catalog Department Web Pages 48 47, no. 4: About the Kavita Mundle, Lisa Zhao, and Nirmala S. Bangalore Cover: Artwork by Keith D. Skeen and used Cataloging and Metadata in North American LIS Programs 59 with permission of ALA Graphics, from the Ingrid Hsieh-Yee Library Art CD, a royalty- free art resource for libraries available at www.alastore.ala.org. NOTES FROM OPERATIONS © 2003 American Library Association Gold Rush 69 Integrated Access to Aggregated Journal Text through the OPAC Association for Library Elizabeth S. Meagher and Christopher C. Brown Collections and Technical Services Visit LRTS online at www. ala.org/alcts/lrts. FEATURES For current news and reports on ALCTS Book Reviews 78 activities, see the ALCTS Newsletter Online at Edward Swanson, Interim Editor www.ala.org/alcts/ alcts_news. -

TLC Final Response for HCPSS

Howard County Public School System Request for Proposal No. 042.18.B5 For Online School Library Automation and Circulation Solution Submitted by: The Library Corporation Research Park Inwood, WV USA 25428 Federal Identification No.: 52-1043428 Toll-Free: 800.325.7759 Fax: 304.229.0295 Visit us online at: TLCdelivers.com 2 The Library Corporation TABLE OF CONTENTS Proposal Contents Phone:Phone: (800) (800) 325- 3257759-7759 | Email | E:- [email protected]: [email protected] | www.TLCdelivers.com | www.TLCdelivers.com The Library Corporation 3 ABOUT US 24/7/365 UNPARALLELED SERVICE WHO WE ARE TLC provides you with advanced technological solutions supported by an outstanding and unexpected level of service. Our customer service is unmatched in the automation The Library Corporation industry. Call TLC for information or assistance. A person – (TLC) was established in not a machine – will answer. You’ll get what you want without 1974 with one purpose: To wandering through a voicemail labyrinth. That’s service you serve libraries with can depend on. advanced automation solutions. We stand out in A VERY DEDICATED TEAM today’s market of vendor TLC libraries benefit from an uncompromising knowledge takeovers because our base in a resource of people that care. Seventy percent of founders still own and TLC employees have been with the company for at least five years, while over 60 percent have logged a decade or more of operate TLC. service! You get a knowledge base unsurpassed in the industry. You get a core group of TLC staff that knows you When you partner with and cares about you.