July Investment Companies Monthly Roundup

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

REAL ESTATE July 2020

LISTED MARKETS – REAL ESTATE July 2020 Leo Zielinski Partner Tel. +44 (0)7980 809031 [email protected] John Rodgers Partner Tel. +44 (0)7810 307422 [email protected] Will Strachan Partner Tel. +44 (0)7929 885859 [email protected] Lloyd Davies We track the share price movement and regulatory announcements Partner of 57 real estate owning listed entities (“Gerald Eve tracked index”). Tel. +44 (0)7767 311254 A summary of the Gerald Eve tracked index in terms of GAV, NAV, [email protected] LTV, Dividend, Share Price, Market Cap, Discount/Premium to NAV and their respective weekly movement is attached. Lorenzo Solazzo Data Analyst We provide a comparison to share price data from 3 February 2020 Tel. +44 (0)783 309 5582 [email protected] (pre-Covid-19 level) to present day to demonstrate the impact across certain entities as a direct result of Covid-19. James Brown Surveyor As at 30 of June, the Gerald Eve tracked index is currently down 30% to pre- Tel. +44 (0)7464 656563 Covid-19 level, under-performing the FTSE350 which is slowly recovering and is [email protected] now down 16%. The tracked listed REITs share price decreased on average 3% since 1 June 2020 (March: -25%, April: +6%, May: -3%). To provide context around the share price movement, the average discount to NAV is currently 31% against 3% pre-Covid-19. It is unsurprising to note that specialist sector entities across Industrial, Healthcare and Supermarkets have out-performed the REIT universe relative to other strategies within the Gerald Eve tracked index. -

Xtrackers Etfs

Xtrackers*/** Société d’investissement à capital variable R.C.S. Luxembourg N° B-119.899 Unaudited Semi-Annual Report For the period from 1 January 2018 to 30 June 2018 No subscription can be accepted on the basis of the financial reports. Subscriptions are only valid if they are made on the basis of the latest published prospectus of Xtrackers accompanied by the latest annual report and the most recent semi-annual report, if published thereafter. * Effective 16 February 2018, db x-trackers changed name to Xtrackers. **This includes synthetic ETFs. Xtrackers** Table of contents Page Organisation 4 Information for Hong Kong Residents 6 Statistics 7 Statement of Net Assets as at 30 June 2018 28 Statement of Investments as at 30 June 2018 50 Xtrackers MSCI WORLD SWAP UCITS ETF* 50 Xtrackers MSCI EUROPE UCITS ETF 56 Xtrackers MSCI JAPAN UCITS ETF 68 Xtrackers MSCI USA SWAP UCITS ETF* 75 Xtrackers EURO STOXX 50 UCITS ETF 80 Xtrackers DAX UCITS ETF 82 Xtrackers FTSE MIB UCITS ETF 83 Xtrackers SWITZERLAND UCITS ETF 85 Xtrackers FTSE 100 INCOME UCITS ETF 86 Xtrackers FTSE 250 UCITS ETF 89 Xtrackers FTSE ALL-SHARE UCITS ETF 96 Xtrackers MSCI EMERGING MARKETS SWAP UCITS ETF* 111 Xtrackers MSCI EM ASIA SWAP UCITS ETF* 115 Xtrackers MSCI EM LATIN AMERICA SWAP UCITS ETF* 117 Xtrackers MSCI EM EUROPE, MIDDLE EAST & AFRICA SWAP UCITS ETF* 118 Xtrackers MSCI TAIWAN UCITS ETF 120 Xtrackers MSCI BRAZIL UCITS ETF 123 Xtrackers NIFTY 50 SWAP UCITS ETF* 125 Xtrackers MSCI KOREA UCITS ETF 127 Xtrackers FTSE CHINA 50 UCITS ETF 130 Xtrackers EURO STOXX QUALITY -

LXI REIT Plc Prospectus.Pdf

168594 Project Olympus - Prospectus Intro_168594 Project Olympus - Prospectus Intro 06/02/2017 10:43 Page 1 168594 Proof 3 Monday, February 6, 2017 10:43 THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. If you are in any doubt about the action you should take, you are recommended to seek your own financial advice immediately from an independent financial adviser who is authorised under the Financial Services and Markets Act 2000 (as amended) (“FSMA”) if you are in the United Kingdom, or from another appropriately authorised independent financial adviser if you are in a territory outside the United Kingdom. A copy of this document, which comprises a prospectus relating to LXI REIT plc (the “Company”) prepared in accordance with the Prospectus Rules of the UK Listing Authority made pursuant to section 73A of the FSMA, has been filed with the Financial Conduct Authority in accordance with Rule 3.2 of the Prospectus Rules. Applications will be made to the UK Listing Authority and the London Stock Exchange for the Ordinary Shares to be issued in connection with the Issue and each Subsequent Placing under the Placing Programme to be admitted to listing on the premium listing segment of the Official List and to trading on the premium segment of the main market for listed securities of the London Stock Exchange respectively. It is expected that First Admission will become effective and that dealings for normal settlement in the Ordinary Shares will commence on 27 February 2017. It is expected that any Subsequent Admission pursuant to Subsequent Placings under the Placing Programme will become effective and dealings will commence between 28 February 2017 and 5 February 2018. -

Description Iresscode Exchange Current Margin New Margin 3I

Description IRESSCode Exchange Current Margin New Margin 3I INFRASTRUCTURE PLC 3IN LSE 20 20 888 HOLDINGS PLC 888 LSE 20 20 ASSOCIATED BRITISH ABF LSE 10 10 ADMIRAL GROUP PLC ADM LSE 10 10 AGGREKO PLC AGK LSE 20 20 ASHTEAD GROUP PLC AHT LSE 10 10 ANTOFAGASTA PLC ANTO LSE 15 10 ASOS PLC ASC LSE 20 20 ASHMORE GROUP PLC ASHM LSE 20 20 ABERFORTH SMALLER COM ASL LSE 20 20 AVEVA GROUP PLC AVV LSE 20 20 AVIVA PLC AV LSE 10 10 ASTRAZENECA PLC AZN LSE 10 10 BABCOCK INTERNATIONAL BAB LSE 20 20 BARR PLC BAG LSE 25 20 BARCLAYS PLC BARC LSE 10 10 BRITISH AMERICAN TOBA BATS LSE 10 10 BAE SYSTEMS PLC BA LSE 10 10 BALFOUR BEATTY PLC BBY LSE 20 20 BARRATT DEVELOPMENTS BDEV LSE 10 10 BARING EMERGING EUROP BEE LSE 50 100 BEAZLEY PLC BEZ LSE 20 20 BH GLOBAL LIMITED BHGG LSE 30 100 BOWLEVEN PLC BLVN LSE 60 50 BANKERS INVESTMENT BNKR LSE 20 20 BUNZL PLC BNZL LSE 10 10 BODYCOTE PLC BOY LSE 20 20 BP PLC BP LSE 10 10 BURBERRY GROUP PLC BRBY LSE 10 10 BLACKROCK WORLD MININ BRWM LSE 20 65 BT GROUP PLC BT-A LSE 10 10 BRITVIC PLC BVIC LSE 20 20 BOVIS HOMES GROUP PLC BVS LSE 20 20 BROWN GROUP PLC BWNG LSE 25 20 BELLWAY PLC BWY LSE 20 20 BIG YELLOW GROUP PLC BYG LSE 20 20 CENTRAL ASIA METALS PLC CAML LSE 40 30 CLOSE BROTHERS GROUP CBG LSE 20 20 CARNIVAL PLC CCL LSE 10 10 CENTAMIN PLC CEY LSE 20 20 CHARIOT OIL & GAS LTD CHAR LSE 100 100 CHEMRING GROUP PLC CHG LSE 25 20 CONYGAR INVESTMENT CIC LSE 50 40 CALEDONIA INVESTMENTS CLDN LSE 25 20 CARILLION PLC CLLN LSE 100 100 COMMUNISIS PLC CMS LSE 50 100 CENTRICA PLC CNA LSE 10 10 CAIRN ENERGY PLC CNE LSE 30 30 COBHAM PLC -

The VT Redlands Portfolios

The VT Redlands Portfolios What are the VT Redlands Portfolios? The VT Redlands Portfolio funds each invest in one of four defined “asset classes” namely the Equity, Multi-Asset, Property and Fixed Income categories. Each fund carries a prescribed Risk Profile on a scale of 1 to 7 – with for example Equity being the highest at a factor 5. Each one is used as a building block in the creation of bespoke risk rated investment portfolios for clients of David Williams IFA. By combining the four VT Redlands funds with other asset classes such as With Profits/ Smoothed Managed and Structured Equity funds, our clients can enjoy the benefits of a very wide level of diversification within their portfolios. This reduces volatility and creates the potential for rewarding rates of return year after year. Each Portfolio fund is constructed as a Fund of Funds providing access to the “best of the best” sector funds from a huge investment universe. The Portfolios are designed to meet their objectives as efficiently as possible whilst keeping costs to a minimum and are run according to a strict risk-control criteria. Typically, 15 to 25 different funds are held in each portfolio, with each one in turn managed by leading investment houses such as Fundsmith, Fidelity and Invesco as well as specialist boutiques including Ruffer, Fulcrum and Somerset. Underlying funds have exposure to a great many shares, bonds and other assets, Therefore, a single investment into one of the Redlands Portfolios gives a spread across a myriad of different holdings, countries and investment styles. -

Annual Report of Proxy Voting Record Date Of

ANNUAL REPORT OF PROXY VOTING RECORD DATE OF REPORTING PERIOD: JULY 1, 2018 - JUNE 30, 2019 FUND: VANGUARD FTSE 250 UCITS ETF --------------------------------------------------------------------------------------------------------------------------------------------------------------------------------- ISSUER: 3i Infrastructure plc TICKER: 3IN CUSIP: ADPV41555 MEETING DATE: 7/5/2018 FOR/AGAINST PROPOSAL: PROPOSED BY VOTED? VOTE CAST MGMT PROPOSAL #1: ACCEPT FINANCIAL STATEMENTS AND ISSUER YES FOR FOR STATUTORY REPORTS PROPOSAL #2: APPROVE REMUNERATION REPORT ISSUER YES FOR FOR PROPOSAL #3: APPROVE FINAL DIVIDEND ISSUER YES FOR FOR PROPOSAL #4: RE-ELECT RICHARD LAING AS DIRECTOR ISSUER YES FOR FOR PROPOSAL #5: RE-ELECT IAN LOBLEY AS DIRECTOR ISSUER YES FOR FOR PROPOSAL #6: RE-ELECT PAUL MASTERTON AS DIRECTOR ISSUER YES FOR FOR PROPOSAL #7: RE-ELECT DOUG BANNISTER AS DIRECTOR ISSUER YES FOR FOR PROPOSAL #8: RE-ELECT WENDY DORMAN AS DIRECTOR ISSUER YES FOR FOR PROPOSAL #9: ELECT ROBERT JENNINGS AS DIRECTOR ISSUER YES FOR FOR PROPOSAL #10: RATIFY DELOITTE LLP AS AUDITORS ISSUER YES FOR FOR PROPOSAL #11: AUTHORISE BOARD TO FIX REMUNERATION OF ISSUER YES FOR FOR AUDITORS PROPOSAL #12: APPROVE SCRIP DIVIDEND SCHEME ISSUER YES FOR FOR PROPOSAL #13: AUTHORISE CAPITALISATION OF THE ISSUER YES FOR FOR APPROPRIATE AMOUNTS OF NEW ORDINARY SHARES TO BE ALLOTTED UNDER THE SCRIP DIVIDEND SCHEME PROPOSAL #14: AUTHORISE ISSUE OF EQUITY WITHOUT PRE- ISSUER YES FOR FOR EMPTIVE RIGHTS PROPOSAL #15: AUTHORISE MARKET PURCHASE OF ORDINARY ISSUER YES FOR FOR -

The Virgin UK Index Tracking Trust

The Virgin UK Index Tracking Trust Final Report and Financial Statements For the year ended 15 March 2021 2 The Virgin UK Index Tracking Trust Contents Manager's report 3 Management and professional services 3 Manager's investment report 4 Comparative tables 11 Portfolio statement 12 Top purchases and sales of investments 30 Securities Financing Transactions (SFTs) 32 Statement of total return 36 Statement of change in net assets attributable to unitholders 37 Balance sheet 38 Notes to the financial statements 39 Distribution tables 53 Statement of the Manager’s responsibilities 54 Independent auditor’s report to the unitholders of the Virgin UK Index Tracking Trust 55 Manager’s remuneration 58 Statement of the Trustee’s responsibilities in respect of the Scheme and Report of the Trustee to the Unitholders of the Virgin UK Index Tracking Trust 59 The Virgin UK Index Tracking Trust 3 Management and professional services For the year ended 15 March 2021 Manager (the ‘Manager’) Virgin Money Unit Trust Managers Limited Jubilee House Directors: S. Bruce (appointed 29 September 2020) Gosforth J. Byrne (appointed 24 May 2021) Newcastle upon Tyne H. Chater NE3 4PL S. Fennessy (resigned 29 September 2020) F. Murphy (appointed 19 October 2020) M. Phibbs J. Scott (resigned 4 December 2020) I. Smith (resigned 19 October 2020) D. Taylor (appointed 29 September 2020) N. L. Tu (resigned 24 May 2021) S. Wemyss (appointed 8 December 2020) Telephone 03456 10 20 30* Authorised and regulated by the Financial Conduct Authority. Investment adviser Aberdeen Asset Managers Limited 10 Queen’s Terrace Aberdeen Aberdeenshire AB10 1XL Authorised and regulated by the Financial Conduct Authority. -

EPRA Nareit UK

2 FTSE Russell Publications 19 August 2021 FTSE EPRA Nareit UK Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) Aberdeen Standard European Logistics 0.47 UNITED Great Portland Estates 2.87 UNITED Schroder Real Estate Investment Trust 0.38 UNITED Income KINGDOM KINGDOM KINGDOM Assura 3.11 UNITED Hammerson 2.41 UNITED Segro 20.93 UNITED KINGDOM KINGDOM KINGDOM Big Yellow Group 3.37 UNITED Helical 0.7 UNITED Shaftesbury 2.53 UNITED KINGDOM KINGDOM KINGDOM BMO Commercial Property Trust 0.76 UNITED Impact Healthcare REIT 0.46 UNITED Sirius Real Estate 1.71 UNITED KINGDOM KINGDOM KINGDOM BMO Real Estate Investments 0.27 UNITED Land Securities Group 7.69 UNITED Standard Life Inv Prop Inc Trust 0.44 UNITED KINGDOM KINGDOM KINGDOM British Land Co 7.31 UNITED LondonMetric Property 3.25 UNITED Target Healthcare REIT 0.94 UNITED KINGDOM KINGDOM KINGDOM Capital & Counties Properties 1.89 UNITED LXI REIT 1.32 UNITED Triple Point Social Housing REIT 0.61 UNITED KINGDOM KINGDOM KINGDOM Civitas Social Housing 1.15 UNITED NewRiver REIT 0.42 UNITED Tritax Big Box REIT 5.39 UNITED KINGDOM KINGDOM KINGDOM CLS Holdings 0.6 UNITED Phoenix Spree Deutschland 0.53 UNITED Tritax EuroBox GBP 1.06 UNITED KINGDOM KINGDOM KINGDOM Custodian REIT 0.6 UNITED Picton Property Income 0.76 UNITED UK Commercial Property REIT Limited 0.9 UNITED KINGDOM KINGDOM KINGDOM Derwent London 5.34 UNITED Primary Health Prop. 3.22 UNITED Unite Group 5.46 UNITED KINGDOM KINGDOM KINGDOM Empiric Student Property 0.81 UNITED PRS REIT (The) 0.76 UNITED Workspace Group 1.78 UNITED KINGDOM KINGDOM KINGDOM GCP Student Living 1.17 UNITED Regional REIT 0.5 UNITED KINGDOM KINGDOM Grainger 3.01 UNITED Safestore Holdings 3.1 UNITED KINGDOM KINGDOM Source: FTSE Russell 1 of 2 19 August 2021 Data Explanation Weights Weights data is indicative, as values have been rounded up or down to two decimal points. -

Life After Lockdown

www.whatinvestment.co.uk Issue 460 | July 2021 | £4.50 LIFE AFTER LOCKDOWN A growing concern Are you switched on? A high stakes game Investing in trees could How artifi cial intelligence Peter Elston on why be the antidote to some of is transforming life as infl ation is far more Earth’s biggest challenges we know it complex than it appears Pages 34-35 Pages 50-52 Page 82 001_WI_0721.indd 1 17/06/2021 10:42 ad template.indd 1 17/06/2021 12:02 First word 3 July 2021 On life and investing www.whatinvestment.co.uk Issue 460 | July 2021 | £4.50 LIFE AFTER LOCKDOWN after the pandemic A growing concern Are you switched on? A high stakes game Investing in trees could How artificial intelligence Peter Elston on why be the antidote to some of is transforming life as inflation is far more Earth’s biggest challenges we know it complex than it appears Pages 34-35 Pages 50-52 Page 82 elcome to the July issue As you will learn in this month’s Editorial of What Investment, which issue, some investment trust Editor-in-chief comes at a time when it managers believe there will be a Lawrence Gosling 020 7250 7027 W [email protected] looks like the economy is on the very strong recovery, particularly verge of opening up for the fi rst in areas like consumer spending, Subscriptions Lara Rossett 020 7250 7011 time since March of last year. housebuilding and specialist [email protected] How we view this situation industrial businesses; others don’t Advertising depends largely on what kind of Lawrence Gosling think things will be so simple. -

Annual Report and Accounts 2018 01 Overview Performance Highlights for the Year to 31 March 2018

3i Group plc Overview Governance Introduction 01 Chairman’s introduction 58 Performance highlights 02 Board of Directors and Executive Committee 60 Chairman’s statement 02 Nominations Committee report 65 Chief Executive’s statement 04 Audit and Compliance Committee report 66 Action 08 Valuations Committee report 70 Directors’ remuneration report 73 Our business Relations with shareholders 83 Our business at a glance 10 Additional statutory and corporate governance information 84 Our business model 12 Our strategic objectives 14 Audited financial statements Key performance indicators 16 Private Equity 18 Consolidated statement of comprehensive income 92 Infrastructure 25 Consolidated statement of financial position 93 Performance, risk and sustainability Consolidated statement of changes in equity 94 Consolidated cash flow statement 95 Financial review 29 Company statement of financial position 96 Investment basis 35 Company statement of changes in equity 97 Reconciliation of Investment basis and IFRS 39 Company cash flow statement 98 Alternative Performance Measures 43 Significant accounting policies 99 Risk management 44 Notes to the accounts 104 Principal risks and mitigations 47 Independent Auditor’s report 139 Sustainability 52 Portfolio and other information 20 Large investments 148 Strategic report: Portfolio valuation – an explanation 150 pages 2 to 56. Information for shareholders 152 Directors’ report: pages Glossary 154 58 to 72 and 83 to 90. For definitions of our financial terms, used throughout this report, please see Directors’ remuneration our glossary on pages 154 to 156. report: pages 73 to 82. Consistent with our approach since the introduction of IFRS 10 in 2014, the financial data presented in the Overview and Strategic report is taken from the Investment basis financial statements. -

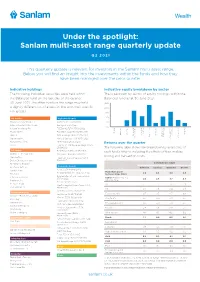

Sanlam Multi-Asset Range Quarterly Update

Under the spotlight: Sanlam multi-asset range quarterly update Q2 2021 This quarterly update is relevant for investors in the Sanlam multi-asset range. Below you will find an insight into the investments within the funds and how they have been managed over the prior quarter. Indicative holdings Indicative equity breakdown by sector The following individual securities were held within The breakdown by sector of equity holdings within the the Balanced fund on the last day of the quarter, Balanced fund as at 30 June 2021. 30 June 2021. The other funds in the range may hold 25% a slightly different list of assets, in line with their specific 20% risk grades. 15% 10% UK equity High yield bonds Howden Joinery Group Plc AA Bond 6.5% 31/01/2026 5% Intercontinental Hotels Group Barclays 6.375% Perp 0% s s s s s e y re Integrafin Holdings Plc FCE Bank 2.727% 03/06/2022 ty gy on ion ti rial rial Ca vice umer umer aple onar Prudential Plc Fidelidade SA 4.25% 04/09/2031 te oper ti Ener ructur St rmat Ser Ma alth Pr re chnology fo Financial Indust Cons Relx Plc GKN Holdings 4.625% 12/05/2032 Cons sc In He Te frast Di Rightmove Plc Marks & Spencer 4.5% 10/07/2027 In Communica Taylor Wimpey Plc MPT 3.692% 05/06/2028 Returns over the quarter Unilever Plc Permanent TSB Group Holdings 2.125% 26/09/2024 The following table shows the breakdown by asset class of US equity Rolls-Royce 3.375% 18/06/2026 each fund’s returns, including the effects of fees, midday Akamai Technologies Inc Sainsbury’s Bank 6% 23/11/2027 pricing and transaction costs. -

Chrysalis Investments Limited

THIS PROSPECTUS IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. If you are in any doubt as to what action you should take you are recommended to seek your own financial advice immediately from your stockbroker, bank, solicitor, accountant or other independent financial adviser who is authorised under the Financial Services and Markets Act 2000 (the “FSMA”) if you are in the United Kingdom, or from another appropriately authorised independent financial adviser if you are in a territory outside the United Kingdom. This Prospectus comprises a prospectus relating to Chrysalis Investments Limited (the “Company”) in connection with the issue of Shares, prepared in accordance with the Prospectus Regulation Rules of the Financial Conduct Authority made pursuant to section 73A of the FSMA. This Prospectus has been approved by the Financial Conduct Authority for the purposes of the UK version of Regulation (EU) 2017/1129 (the “EU Prospectus Regulation”) which forms part of UK law by virtue of the European Union (Withdrawal) Act 2018 (the “UK Prospectus Regulation”). The Financial Conduct Authority only approves this Prospectus, as the competent authority under the Prospectus Regulation Rules, as meeting the standards of completeness, comprehensibility and consistency imposed by the UK Prospectus Regulation. Such approval should not be considered as an endorsement of the Company that is the subject of this Prospectus or of the quality of the Shares. This Prospectus has been drawn up and published in accordance with the UK Prospectus Regulation. Investors should make their own assessment as to the suitability of investing in the Shares. The Shares are only suitable for investors: (i) who understand and are willing to assume the potential risks of capital loss and that there may be limited liquidity in the underlying investments of the Company; (ii) for whom an investment in the Shares is part of a diversified investment programme; and (iii) who fully understand and are willing to assume the risks involved in such an investment.