2019 Investor Day

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cenovus Reports Second-Quarter 2020 Results Company Captures Value by Leveraging Flexibility of Its Operations Calgary, Alberta (July 23, 2020) – Cenovus Energy Inc

Cenovus reports second-quarter 2020 results Company captures value by leveraging flexibility of its operations Calgary, Alberta (July 23, 2020) – Cenovus Energy Inc. (TSX: CVE) (NYSE: CVE) remained focused on financial resilience in the second quarter of 2020 and used the flexibility of its assets and marketing strategy to adapt quickly to the changing external environment. This positioned the company to weather the sharp decline in benchmark crude oil prices in April by reducing volumes at its oil sands operations and storing the mobilized oil in its reservoirs for production in an improved price environment. While Cenovus’s financial results were impacted by the weak prices early in the quarter, the company captured value by quickly ramping up production when Western Canadian Select (WCS) prices increased almost tenfold from April to an average of C$46.03 per barrel (bbl) in June. As a result of this decision, Cenovus reached record volumes at its Christina Lake oil sands project in June and achieved free funds flow for the month of more than $290 million. “We view the second quarter as a period of transition, with April as the low point of the downturn and the first signs of recovery taking hold in May and June,” said Alex Pourbaix, Cenovus President & Chief Executive Officer. “That said, we expect the commodity price environment to remain volatile for some time. We believe the flexibility of our assets and our low cost structure position us to withstand a continued period of low prices if necessary. And we’re ready to play a significant -

Appendix 4-I: Descriptions of the Life Stages and Habitat Requirements For

APPENDIX 4-I DESCRIPTIONS OF THE LIFE STAGES AND HABITAT REQUIREMENTS FOR FISH AND FISH HABITAT KEY INDICATOR RESOURCES MEG Energy Corp. - i - Fish and Fish Habitat KIRs Christina Lake Regional Project – Phase 3 Appendix 4-I April 2008 TABLE OF CONTENTS SECTION PAGE 1 INTRODUCTION.......................................................................................................1 1.1 ARCTIC GRAYLING........................................................................................................2 1.2 NORTHERN PIKE ...........................................................................................................3 1.3 WALLEYE........................................................................................................................4 1.4 WHITE SUCKER .............................................................................................................6 1.5 BROOK STICKLEBACK..................................................................................................7 1.6 BENTHIC INVERTEBRATES..........................................................................................7 2 REFERENCES..........................................................................................................9 2.1 PERSONAL COMMUNICATIONS ................................................................................11 LIST OF TABLES Table 1 Fish Life Cycle Stages and Habitat Components............................................................1 Volume 4 MEG Energy Corp. - 1 - Fish and Fish Habitat KIRs Christina -

Cenovus Energy Inc. (CVE) – Quality and Growth for the Patient Investor

Portfolio Advisory Group Cenovus Energy Inc. (CVE) – Quality and Growth For The Patient Investor Cenovus was created through the split of Calgary-based Primer on the Oil Sands and energy company EnCana into two separate organizations in late 2009. As a result of this split, many Canadian Steam-Assisted-Gravity-Drainage investors found themselves holding two very different (SAGD) investments: a pure-play natural gas company (EnCana) Including the oil sands, Canada’s oil reserves are the and an integrated oil & gas company (Cenovus). This second largest in the world. Oil sands are composed document aims to provide some insight into the nature primarily of sand, clay, bitumen and water. Bitumen and long-term potential of Cenovus. is the product of oil sands production – a thick oil Cenovus owns oil sands projects that have a tremendous embedded in sand. growth profile over the next decade and are widely Recovery of bitumen is typically achieved by one of viewed as some of the highest-quality assets in the two methods: mining in open pits or drilling. Bitumen industry. However, since inception, the shares of extraction using drilling is referred to as in situ recovery, Cenovus have largely traded within a range. One reason and is generally used for reservoirs that are too deep for is that the company has made a trade-off between near- surface mining techniques to work economically. It is term and future production by drawing cash flows from estimated that approximately 80% of the total bitumen its natural gas business to fund growth in its oil sands recoverable in Alberta can only be produced with in business. -

NB4 - Rivers, Creeks and Streams Waterbody Waterbody Detail Season Bait WALL NRPK YLPR LKWH BURB GOLD MNWH L = Bait Allowed Athabasca River Mainstem OPEN APR

Legend: As examples, ‘3 over 63 cm’ indicates a possession and size limit of ‘3 fish each over 63 cm’ or ‘10 fish’ indicates a possession limit of 10 for that species of any size. An empty cell indicates the species is not likely present at that waterbody; however, if caught the default regulations for the Watershed Unit apply. SHL=Special Harvest Licence, BKTR = Brook Trout, BNTR=Brown Trout, BURB = Burbot, CISC = Cisco, CTTR = Cutthroat Trout, DLVR = Dolly Varden, GOLD = Goldeye, LKTR = Lake Trout, LKWH = Lake Whitefish, MNWH = Mountain Whitefish, NRPK = Northern Pike, RNTR = Rainbow Trout, SAUG = Sauger, TGTR = Tiger Trout, WALL = Walleye, YLPR = Yellow Perch. Regulation changes are highlighted blue. Waterbodies closed to angling are highlighted grey. NB4 - Rivers, Creeks and Streams Waterbody Waterbody Detail Season Bait WALL NRPK YLPR LKWH BURB GOLD MNWH l = Bait allowed Athabasca River Mainstem OPEN APR. 1 to MAY 31 l 0 fish 3 over 63 cm 10 fish 10 fish 5 over 30 cm Mainstem OPEN JUNE 1 to MAR. 31 l 3 over 3 over 63 cm 10 fish 10 fish 5 over 43 cm 30 cm Tributaries except Clearwater and Hangingstone rivers OPEN JUNE 1 to OCT. 31 l 3 over 3 over 63 cm 10 fish 10 fish 10 fish 5 over 43 cm 30 cm Birch Creek Beyond 10 km of Christina Lake OPEN JUNE 1 to OCT. 31 l 0 fish 3 over 63 cm Christina Lake Tributaries and Includes all tributaries and outflows within 10km of OPEN JUNE 1 to OCT. 31 l 0 fish 0 fish 15 fish 10 fish 10 fish Outflows Christina Lake including Jackfish River, Birch, Sunday and Monday Creeks Clearwater River Snye Channel OPEN JUNE 1 to OCT. -

Cenovus Completes Acquisition of Assets in Western Canada from Conocophillips

Cenovus completes acquisition of assets in Western Canada from ConocoPhillips Calgary, Alberta (May 17, 2017) – Cenovus Energy Inc. (TSX: CVE) (NYSE: CVE) has closed its previously announced purchase of assets in Western Canada from ConocoPhillips after receiving all necessary regulatory approvals for the transaction. The acquired assets include ConocoPhillips’ 50% interest in the FCCL Partnership, the oil sands venture which was jointly owned with and operated by Cenovus, as well as the majority of ConocoPhillips’ Deep Basin conventional assets in Alberta and British Columbia. “With the completion of this transformational deal, we now have full control of our best-in- class oil sands projects and an exciting new growth platform in the Deep Basin that provides us with significant short-cycle development opportunities to complement our long-term oil sands growth portfolio,” said Brian Ferguson, Cenovus President & Chief Executive Officer. “As a result of this transaction, we’ve now doubled our production and reserves base.” In the coming months, Cenovus will remain firmly focused on: • Continuing to safely and reliably operate all of its assets • Efficiently integrating the Deep Basin assets and staff into the company • Deleveraging its balance sheet, including using the proceeds of planned divestitures, such as the sale of the company’s Pelican Lake and Suffield assets, which are currently being marketed. Cenovus intends to provide an update on its investment plans for its consolidated oil sands business and newly acquired Deep Basin -

Northwest Territories Territoires Du Nord-Ouest British Columbia

122° 121° 120° 119° 118° 117° 116° 115° 114° 113° 112° 111° 110° 109° n a Northwest Territories i d i Cr r eighton L. T e 126 erritoires du Nord-Oues Th t M urston L. h t n r a i u d o i Bea F tty L. r Hi l l s e on n 60° M 12 6 a r Bistcho Lake e i 12 h Thabach 4 d a Tsu Tue 196G t m a i 126 x r K'I Tue 196D i C Nare 196A e S )*+,-35 125 Charles M s Andre 123 e w Lake 225 e k Jack h Li Deze 196C f k is a Lake h Point 214 t 125 L a f r i L d e s v F Thebathi 196 n i 1 e B 24 l istcho R a l r 2 y e a a Tthe Jere Gh L Lake 2 2 aili 196B h 13 H . 124 1 C Tsu K'Adhe L s t Snake L. t Tue 196F o St.Agnes L. P 1 121 2 Tultue Lake Hokedhe Tue 196E 3 Conibear L. Collin Cornwall L 0 ll Lake 223 2 Lake 224 a 122 1 w n r o C 119 Robertson L. Colin Lake 121 59° 120 30th Mountains r Bas Caribou e e L 118 v ine i 120 R e v Burstall L. a 119 l Mer S 117 ryweather L. 119 Wood A 118 Buffalo Na Wylie L. m tional b e 116 Up P 118 r per Hay R ark of R iver 212 Canada iv e r Meander 117 5 River Amber Rive 1 Peace r 211 1 Point 222 117 M Wentzel L. -

Canadian Crude Oil at Record Discount

Canadian crude oil at record discount Hilliard MacBeth Hilliard’s Weekend Notebook – Friday October 19, 2018 Richardson GMP World oil prices are at cycle highs recently with the benchmark Brent at US$80 and 10180 101 Street, Suite 3360 the North American West Texas Intermediate (WTI) at US$70. Edmonton, AB T5J 3S4 Tel. 1.780.409.7735 But in Canada, the Western Canada Select (WCS) price is below US$20. Fax 780.409.7777 www.TheMacBethGroup.com This gap of US$50 to WTI is shocking. Hilliard MacBeth Will the price for a key Canadian energy export recover soon enough to save the Director, Wealth Management industry? Portfolio Manager Tel. 780.409.7740 Source: Bloomberg Rising production from oil sands along with a lack of pipeline capacity to move that product to the US market gets the blame for this extremely low price. On October 12, the price for WCS fell to US$15.97, as of yesterday the price has returned to US$19.75. Source: OilPrice.com One solution that should have been in place by now is the Keystone XL pipeline that was approved years ago but keeps hitting new roadblocks. This pipeline is the 4th phase of an existing pipeline system that moves crude to the US refineries that are well-suited to handle Alberta’s heavy crude. The new XL phase would handle an additional 830,000 barrels per day but won’t be on line until 2021, if it goes ahead. Nebraska’s highest court has yet to rule on another legal challenge to the route. -

In Situ Report Card

Drilling DEEPERTHE IN SITU OIL SANDS REPORT CARD JEREMY MOORHOUSE • MARC HUOT • SIMON DYER March 2010 Oil SANDSFever SERIES Drilling Deeper The In Situ Oil Sands Report Card Jeremy Moorhouse Marc Huot Simon Dyer March 2010 The In Situ Oil Sands Report Card About the Pembina Institute The Pembina Institute The Pembina Institute is a national The Pembina Institute provides policy Box 7558 non-profit think tank that advances research leadership and education on Drayton Valley, Alberta, T7A 1S7 sustainable energy solutions through climate change, energy issues, green Phone: 780-542-6272 research, education, consulting and economics, energy efficiency and advocacy. It promotes environmental, conservation, renewable energy, and E-mail: [email protected] social and economic sustainability in environmental governance. For more the public interest by developing information about the Pembina practical solutions for communities, Institute, visit www.pembina.org or individuals, governments and businesses. contact info @pembina.org. Acknowledgements The Pembina Institute thanks the graciously reviewed and commented William and Flora Hewlett Foundation on the data the Pembina Institute for its support of this work. The had collected for this analysis. Their Pembina Institute would also like to comments and insights improved acknowledge the support of Cenovus, the quality of this report and the Shell and Husky for participating in this Pembina Institute’s understanding process. Each of these companies of in situ operations. ii DRILLING DEEPER: THE IN SITU OIL SANDS REPORT CARD The Pembina Institute The In Situ Oil Sands Report Card About the Authors Jeremy Moorhouse of Alberta, and a Master of Arts in Technical Analyst natural sciences Jeremy is a Technical Analyst with the from Cambridge Pembina Institute’s Corporate University. -

Foreign Investment in the Oil Sands and British Columbia Shale Gas

Canadian Energy Research Institute Foreign Investment in the Oil Sands and British Columbia Shale Gas Jon Rozhon March 2012 Relevant • Independent • Objective Foreign Investment in the Oil Sands and British Columbia Shale Gas 1 Foreign Investment in the Oil Sands There has been a steady flow of foreign investment into the oil sands industry over the past decade in terms of merger and acquisition (M&A) activity. Out of a total CDN$61.5 billion in M&A’s, approximately half – or CDN$30.3 billion – involved foreign companies taking an ownership stake. These funds were invested in in situ projects, integrated projects, and land leases. As indicated in Figure 1, US and Chinese companies made the most concerted efforts to increase their profile in the oil sands, investing 2/3 of all foreign capital. The US and China both invested in a total of seven different projects. The French company, Total SA, has also spread its capital around several projects (four in total) while Royal Dutch Shell (UK), Statoil (Norway), and PTT (Thailand) each opted to take large positions in one project each. Table 1 provides a list of all foreign investments in the oil sands since 2004. Figure 1: Total Oil Sands Foreign Investment since 2003, Country of Origin Korea 1% Thailand Norway 6% UK 7% 2% US France 33% 18% China 33% Source: Canoils. Foreign Investment in the Oil Sands and British Columbia Shale Gas 2 Table 1: Oil Sands Foreign Investment Deals Year Country Acquirer Brief Description Total Acquisition Cost (000) 2012 China PetroChina 40% interest in MacKay River 680,000 project from AOSC 2011 China China National Offshore Acquisition of OPTI Canada 1,906,461 Oil Corporation 2010 France Total SA Alliance with Suncor. -

Climate and Energy Benchmark in Oil and Gas

Climate and Energy Benchmark in Oil and Gas Total score ACT rating Ranking out of 100 performance, narrative and trend 1 Neste 57.4 / 100 8.1 / 20 B 2 Engie 56.9 / 100 7.9 / 20 B 3 Naturgy Energy 44.8 / 100 6.8 / 20 C 4 Eni 43.6 / 100 7.3 / 20 C 5 bp 42.9 / 100 6.0 / 20 C 6 Total 40.7 / 100 6.1 / 20 C 7 Repsol 38.1 / 100 5.0 / 20 C 8 Equinor 37.9 / 100 4.9 / 20 C 9 Galp Energia 36.4 / 100 4.3 / 20 C 10 Royal Dutch Shell 34.3 / 100 3.4 / 20 C 11 ENEOS Holdings 32.4 / 100 2.6 / 20 C 12 Origin Energy 29.3 / 100 7.3 / 20 D 13 Marathon Petroleum Corporation 24.8 / 100 4.4 / 20 D 14 BHP Group 22.1 / 100 4.3 / 20 D 15 Hellenic Petroleum 20.7 / 100 3.7 / 20 D 15 OMV 20.7 / 100 3.7 / 20 D Total score ACT rating Ranking out of 100 performance, narrative and trend 17 MOL Magyar Olajes Gazipari Nyrt 20.2 / 100 2.5 / 20 D 18 Ampol Limited 18.8 / 100 0.9 / 20 D 19 SK Innovation 18.6 / 100 2.8 / 20 D 19 YPF 18.6 / 100 2.8 / 20 D 21 Compania Espanola de Petroleos SAU (CEPSA) 17.9 / 100 2.5 / 20 D 22 CPC Corporation, Taiwan 17.6 / 100 2.4 / 20 D 23 Ecopetrol 17.4 / 100 2.3 / 20 D 24 Formosa Petrochemical Corp 17.1 / 100 2.2 / 20 D 24 Cosmo Energy Holdings 17.1 / 100 2.2 / 20 D 26 California Resources Corporation 16.9 / 100 2.1 / 20 D 26 Polski Koncern Naftowy Orlen (PKN Orlen) 16.9 / 100 2.1 / 20 D 28 Reliance Industries 16.7 / 100 1.0 / 20 D 29 Bharat Petroleum Corporation 16.0 / 100 1.7 / 20 D 30 Santos 15.7 / 100 1.6 / 20 D 30 Inpex 15.7 / 100 1.6 / 20 D 32 Saras 15.2 / 100 1.4 / 20 D 33 Qatar Petroleum 14.5 / 100 1.1 / 20 D 34 Varo Energy 12.4 / 100 -

Big Oil's Oily Grasp

Big Oil’s Oily Grasp The making of Canada as a Petro-State and how oil money is corrupting Canadian politics Daniel Cayley-Daoust and Richard Girard Polaris Institute December 2012 The Polaris Institute is a public interest research organization based in Canada. Since 1997 Polaris has been dedicated to developing tools and strategies to take action on major public policy issues, including the corporate power that lies behind public policy making, on issues of energy security, water rights, climate change, green economy and global trade. Polaris Institute 180 Metcalfe Street, Suite 500 Ottawa, ON K2P 1P5 Phone: 613-237-1717 Fax: 613-237-3359 Email: [email protected] www.polarisinstitute.org Cover image by Malkolm Boothroyd Table of Contents Introduction 1 1. Corporations and Industry Associations 3 2. Lobby Firms and Consultant Lobbyists 7 3. Transparency 9 4. Conclusion 11 Appendices Appendix A, Companies ranked by Revenue 13 Appendix B, Companies ranked by # of Communications 15 Appendix C, Industry Associations ranked by # of Communications 16 Appendix D, Consultant lobby firms and companies represented 17 Appendix E, List of individual petroleum industry consultant Lobbyists 18 Appendix F, Recurring topics from communications reports 21 References 22 ii Glossary of Acronyms AANDC Aboriginal Affairs and Northern Development Canada CAN Climate Action Network CAPP Canadian Association of Petroleum Producers CEAA Canadian Environmental Assessment Act CEPA Canadian Energy Pipelines Association CGA Canadian Gas Association DPOH -

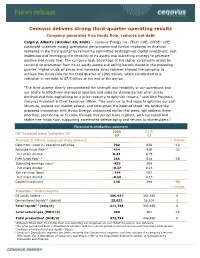

Cenovus Delivers Strong Third-Quarter Operating Results Company Generates Free Funds Flow, Reduces Net Debt Calgary, Alberta (October 29, 2020) – Cenovus Energy Inc

Cenovus delivers strong third-quarter operating results Company generates free funds flow, reduces net debt Calgary, Alberta (October 29, 2020) – Cenovus Energy Inc. (TSX: CVE) (NYSE: CVE) continued to deliver strong operational performance and further improved its financial resilience in the third quarter by remaining committed to disciplined capital investment, cost leadership and leveraging the flexibility of its assets and marketing strategy to generate positive free funds flow. The company took advantage of the higher commodity prices by ramping up production from its oil sands assets and selling barrels stored in the preceding quarter. Higher crude oil prices and increased sales volumes allowed the company to achieve free funds flow for the third quarter of $266 million, which contributed to a reduction in net debt to $7.5 billion at the end of the period. “The third quarter clearly demonstrated the strength and reliability of our operations and our ability to effectively manage production and sales by storing barrels when prices declined and then capitalizing on a price recovery to optimize returns,” said Alex Pourbaix, Cenovus President & Chief Executive Officer. “We continue to find ways to optimize our cost structure, expand our market access, and strengthen the balance sheet. We believe the proposed transaction with Husky Energy, announced earlier this week, will address these priorities, positioning us to come through this period more resilient, with increased and stable free funds flow, supporting accelerated deleveraging