Canadian Crude Oil at Record Discount

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cenovus Reports Second-Quarter 2020 Results Company Captures Value by Leveraging Flexibility of Its Operations Calgary, Alberta (July 23, 2020) – Cenovus Energy Inc

Cenovus reports second-quarter 2020 results Company captures value by leveraging flexibility of its operations Calgary, Alberta (July 23, 2020) – Cenovus Energy Inc. (TSX: CVE) (NYSE: CVE) remained focused on financial resilience in the second quarter of 2020 and used the flexibility of its assets and marketing strategy to adapt quickly to the changing external environment. This positioned the company to weather the sharp decline in benchmark crude oil prices in April by reducing volumes at its oil sands operations and storing the mobilized oil in its reservoirs for production in an improved price environment. While Cenovus’s financial results were impacted by the weak prices early in the quarter, the company captured value by quickly ramping up production when Western Canadian Select (WCS) prices increased almost tenfold from April to an average of C$46.03 per barrel (bbl) in June. As a result of this decision, Cenovus reached record volumes at its Christina Lake oil sands project in June and achieved free funds flow for the month of more than $290 million. “We view the second quarter as a period of transition, with April as the low point of the downturn and the first signs of recovery taking hold in May and June,” said Alex Pourbaix, Cenovus President & Chief Executive Officer. “That said, we expect the commodity price environment to remain volatile for some time. We believe the flexibility of our assets and our low cost structure position us to withstand a continued period of low prices if necessary. And we’re ready to play a significant -

Cenovus Energy Inc. (CVE) – Quality and Growth for the Patient Investor

Portfolio Advisory Group Cenovus Energy Inc. (CVE) – Quality and Growth For The Patient Investor Cenovus was created through the split of Calgary-based Primer on the Oil Sands and energy company EnCana into two separate organizations in late 2009. As a result of this split, many Canadian Steam-Assisted-Gravity-Drainage investors found themselves holding two very different (SAGD) investments: a pure-play natural gas company (EnCana) Including the oil sands, Canada’s oil reserves are the and an integrated oil & gas company (Cenovus). This second largest in the world. Oil sands are composed document aims to provide some insight into the nature primarily of sand, clay, bitumen and water. Bitumen and long-term potential of Cenovus. is the product of oil sands production – a thick oil Cenovus owns oil sands projects that have a tremendous embedded in sand. growth profile over the next decade and are widely Recovery of bitumen is typically achieved by one of viewed as some of the highest-quality assets in the two methods: mining in open pits or drilling. Bitumen industry. However, since inception, the shares of extraction using drilling is referred to as in situ recovery, Cenovus have largely traded within a range. One reason and is generally used for reservoirs that are too deep for is that the company has made a trade-off between near- surface mining techniques to work economically. It is term and future production by drawing cash flows from estimated that approximately 80% of the total bitumen its natural gas business to fund growth in its oil sands recoverable in Alberta can only be produced with in business. -

Cenovus Completes Acquisition of Assets in Western Canada from Conocophillips

Cenovus completes acquisition of assets in Western Canada from ConocoPhillips Calgary, Alberta (May 17, 2017) – Cenovus Energy Inc. (TSX: CVE) (NYSE: CVE) has closed its previously announced purchase of assets in Western Canada from ConocoPhillips after receiving all necessary regulatory approvals for the transaction. The acquired assets include ConocoPhillips’ 50% interest in the FCCL Partnership, the oil sands venture which was jointly owned with and operated by Cenovus, as well as the majority of ConocoPhillips’ Deep Basin conventional assets in Alberta and British Columbia. “With the completion of this transformational deal, we now have full control of our best-in- class oil sands projects and an exciting new growth platform in the Deep Basin that provides us with significant short-cycle development opportunities to complement our long-term oil sands growth portfolio,” said Brian Ferguson, Cenovus President & Chief Executive Officer. “As a result of this transaction, we’ve now doubled our production and reserves base.” In the coming months, Cenovus will remain firmly focused on: • Continuing to safely and reliably operate all of its assets • Efficiently integrating the Deep Basin assets and staff into the company • Deleveraging its balance sheet, including using the proceeds of planned divestitures, such as the sale of the company’s Pelican Lake and Suffield assets, which are currently being marketed. Cenovus intends to provide an update on its investment plans for its consolidated oil sands business and newly acquired Deep Basin -

Foreign Investment in the Oil Sands and British Columbia Shale Gas

Canadian Energy Research Institute Foreign Investment in the Oil Sands and British Columbia Shale Gas Jon Rozhon March 2012 Relevant • Independent • Objective Foreign Investment in the Oil Sands and British Columbia Shale Gas 1 Foreign Investment in the Oil Sands There has been a steady flow of foreign investment into the oil sands industry over the past decade in terms of merger and acquisition (M&A) activity. Out of a total CDN$61.5 billion in M&A’s, approximately half – or CDN$30.3 billion – involved foreign companies taking an ownership stake. These funds were invested in in situ projects, integrated projects, and land leases. As indicated in Figure 1, US and Chinese companies made the most concerted efforts to increase their profile in the oil sands, investing 2/3 of all foreign capital. The US and China both invested in a total of seven different projects. The French company, Total SA, has also spread its capital around several projects (four in total) while Royal Dutch Shell (UK), Statoil (Norway), and PTT (Thailand) each opted to take large positions in one project each. Table 1 provides a list of all foreign investments in the oil sands since 2004. Figure 1: Total Oil Sands Foreign Investment since 2003, Country of Origin Korea 1% Thailand Norway 6% UK 7% 2% US France 33% 18% China 33% Source: Canoils. Foreign Investment in the Oil Sands and British Columbia Shale Gas 2 Table 1: Oil Sands Foreign Investment Deals Year Country Acquirer Brief Description Total Acquisition Cost (000) 2012 China PetroChina 40% interest in MacKay River 680,000 project from AOSC 2011 China China National Offshore Acquisition of OPTI Canada 1,906,461 Oil Corporation 2010 France Total SA Alliance with Suncor. -

Climate and Energy Benchmark in Oil and Gas

Climate and Energy Benchmark in Oil and Gas Total score ACT rating Ranking out of 100 performance, narrative and trend 1 Neste 57.4 / 100 8.1 / 20 B 2 Engie 56.9 / 100 7.9 / 20 B 3 Naturgy Energy 44.8 / 100 6.8 / 20 C 4 Eni 43.6 / 100 7.3 / 20 C 5 bp 42.9 / 100 6.0 / 20 C 6 Total 40.7 / 100 6.1 / 20 C 7 Repsol 38.1 / 100 5.0 / 20 C 8 Equinor 37.9 / 100 4.9 / 20 C 9 Galp Energia 36.4 / 100 4.3 / 20 C 10 Royal Dutch Shell 34.3 / 100 3.4 / 20 C 11 ENEOS Holdings 32.4 / 100 2.6 / 20 C 12 Origin Energy 29.3 / 100 7.3 / 20 D 13 Marathon Petroleum Corporation 24.8 / 100 4.4 / 20 D 14 BHP Group 22.1 / 100 4.3 / 20 D 15 Hellenic Petroleum 20.7 / 100 3.7 / 20 D 15 OMV 20.7 / 100 3.7 / 20 D Total score ACT rating Ranking out of 100 performance, narrative and trend 17 MOL Magyar Olajes Gazipari Nyrt 20.2 / 100 2.5 / 20 D 18 Ampol Limited 18.8 / 100 0.9 / 20 D 19 SK Innovation 18.6 / 100 2.8 / 20 D 19 YPF 18.6 / 100 2.8 / 20 D 21 Compania Espanola de Petroleos SAU (CEPSA) 17.9 / 100 2.5 / 20 D 22 CPC Corporation, Taiwan 17.6 / 100 2.4 / 20 D 23 Ecopetrol 17.4 / 100 2.3 / 20 D 24 Formosa Petrochemical Corp 17.1 / 100 2.2 / 20 D 24 Cosmo Energy Holdings 17.1 / 100 2.2 / 20 D 26 California Resources Corporation 16.9 / 100 2.1 / 20 D 26 Polski Koncern Naftowy Orlen (PKN Orlen) 16.9 / 100 2.1 / 20 D 28 Reliance Industries 16.7 / 100 1.0 / 20 D 29 Bharat Petroleum Corporation 16.0 / 100 1.7 / 20 D 30 Santos 15.7 / 100 1.6 / 20 D 30 Inpex 15.7 / 100 1.6 / 20 D 32 Saras 15.2 / 100 1.4 / 20 D 33 Qatar Petroleum 14.5 / 100 1.1 / 20 D 34 Varo Energy 12.4 / 100 -

Big Oil's Oily Grasp

Big Oil’s Oily Grasp The making of Canada as a Petro-State and how oil money is corrupting Canadian politics Daniel Cayley-Daoust and Richard Girard Polaris Institute December 2012 The Polaris Institute is a public interest research organization based in Canada. Since 1997 Polaris has been dedicated to developing tools and strategies to take action on major public policy issues, including the corporate power that lies behind public policy making, on issues of energy security, water rights, climate change, green economy and global trade. Polaris Institute 180 Metcalfe Street, Suite 500 Ottawa, ON K2P 1P5 Phone: 613-237-1717 Fax: 613-237-3359 Email: [email protected] www.polarisinstitute.org Cover image by Malkolm Boothroyd Table of Contents Introduction 1 1. Corporations and Industry Associations 3 2. Lobby Firms and Consultant Lobbyists 7 3. Transparency 9 4. Conclusion 11 Appendices Appendix A, Companies ranked by Revenue 13 Appendix B, Companies ranked by # of Communications 15 Appendix C, Industry Associations ranked by # of Communications 16 Appendix D, Consultant lobby firms and companies represented 17 Appendix E, List of individual petroleum industry consultant Lobbyists 18 Appendix F, Recurring topics from communications reports 21 References 22 ii Glossary of Acronyms AANDC Aboriginal Affairs and Northern Development Canada CAN Climate Action Network CAPP Canadian Association of Petroleum Producers CEAA Canadian Environmental Assessment Act CEPA Canadian Energy Pipelines Association CGA Canadian Gas Association DPOH -

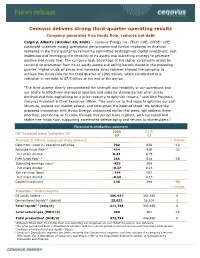

Cenovus Delivers Strong Third-Quarter Operating Results Company Generates Free Funds Flow, Reduces Net Debt Calgary, Alberta (October 29, 2020) – Cenovus Energy Inc

Cenovus delivers strong third-quarter operating results Company generates free funds flow, reduces net debt Calgary, Alberta (October 29, 2020) – Cenovus Energy Inc. (TSX: CVE) (NYSE: CVE) continued to deliver strong operational performance and further improved its financial resilience in the third quarter by remaining committed to disciplined capital investment, cost leadership and leveraging the flexibility of its assets and marketing strategy to generate positive free funds flow. The company took advantage of the higher commodity prices by ramping up production from its oil sands assets and selling barrels stored in the preceding quarter. Higher crude oil prices and increased sales volumes allowed the company to achieve free funds flow for the third quarter of $266 million, which contributed to a reduction in net debt to $7.5 billion at the end of the period. “The third quarter clearly demonstrated the strength and reliability of our operations and our ability to effectively manage production and sales by storing barrels when prices declined and then capitalizing on a price recovery to optimize returns,” said Alex Pourbaix, Cenovus President & Chief Executive Officer. “We continue to find ways to optimize our cost structure, expand our market access, and strengthen the balance sheet. We believe the proposed transaction with Husky Energy, announced earlier this week, will address these priorities, positioning us to come through this period more resilient, with increased and stable free funds flow, supporting accelerated deleveraging -

Cenovus Reports 2020 Fourth-Quarter and Full-Year Results

Cenovus reports 2020 fourth-quarter and full-year results Calgary, Alberta (February 9, 2021) – Cenovus Energy Inc. (TSX: CVE) (NYSE: CVE) responded to extreme oil price volatility in 2020 by quickly reducing capital spending as well as strategically managing oil sands production and purchasing curtailment credits to achieve increased output when prices were more favourable. The company generated positive free funds flow in the fourth quarter, partially offsetting the impact of low oil prices on its full- year results. Cenovus’s planned combination with Husky Energy, announced in the fourth quarter, closed January 1, 2021. The company exited 2020 with net debt of $7.2 billion. “In a year of unprecedented challenges for our industry, we demonstrated the flexibility, strength and reliability of our operations by adapting our capital and operating plans, including leveraging the dynamic storage capabilities of our oil sands reservoirs, transportation optionality and marketing activities to help preserve liquidity,” said Alex Pourbaix, Cenovus President & Chief Executive Officer. “We believe our compelling combination with Husky will provide even greater ability to reduce free funds flow volatility and accelerate debt reduction and returns to shareholders.” Cenovus released its 2021 budget in late January. The budget includes sustaining capital of approximately $2.1 billion to deliver upstream production of approximately 755,000 barrels of oil equivalent per day (BOE/d) and downstream throughput of approximately 525,000 barrels per day (bbls/d). The company also expects to achieve nearly $1 billion of synergies this year as a result of the recent transaction with Husky, putting Cenovus firmly on track to reach its planned $1.2 billion in annual run-rate synergies by the end of 2021. -

Canada's Natural Gas and Oil Emissions

CANADA’S NATURAL GAS AND OIL EMISSIONS: Ongoing Reductions, Demonstrable Improvement GREENHOUSE GAS EMISSIONS AND CANADA’S NATURAL GAS AND OIL INDUSTRY Canada’s Natural Gas and Oil Emissions: Ongoing Reductions, Demonstrable Improvement Contents Emissions: Ongoing Reductions, Demonstrable Improvement . E3 Industry Overview . E5 Technology Overview: The Path to Emissions Reduction . E7 Technology Performance to Date . E9 Near-Term / Potential Technologies . E22 Ongoing Collaboration and Research . E26 Emissions Intensity Performance Data . E29 Natural Gas, Natural Gas Liquids and Condensate . E30 Oil Sands In Situ . E31 Oil Sands Mining. E32 Offshore . E33 Comparable Emissions Performance and Data Quality . E34 E METHODOLOGY IN SITU OIL MINED OIL NATURAL GAS OFFSHORE TECHNOLOGY RESEARCH 2 Emissions: Ongoing Reductions, Demonstrable Improvement E METHODOLOGY IN SITU OIL MINED OIL NATURAL GAS OFFSHORE TECHNOLOGY RESEARCH 3 il and natural gas will continue to be an important part of the world’s energy mix for the foreseeable future . Supplying affordable, reliable and cleaner energy to a Supplying affordable, Ogrowing global population will continue to be the goal of Canada’s upstream energy industry . reliable and cleaner Climate change is a global challenge that requires global energy to a growing perspectives and solutions . Advancing greenhouse gas (GHG) emissions reduction is critical to realizing the vision for Canada global population will to be a global natural gas and oil supplier of choice . continue to be the goal Emissions reduction performance, including emission intensity, is increasingly the basis for policies such as low-carbon of Canada’s upstream fuel regulations, carbon pricing, specific reduction targets energy industry. and emission caps . It’s used to inform funding decisions by governments, funding agencies and investors . -

Capture Project (CCP) – Phase 3 Results

CO2 Capture Project (CCP) – Phase 3 Results 2015 CSLF Mid-Year Meeting – 16th June 2015 Presented by: Mark Crombie – CCP Program Manager BP Group Technology, UK CCP Overview CCP3 Capture Program CCP3 Storage Program CCP3 Comms/P&I Programs CCP4 CCP Conclusions This presentation has been prepared for informational purposes only. All statements of opinion and/or belief contained in this document and all views expressed and all projections, forecasts or statements relating to expectations regarding future events represent the CCP’s own assessment and interpretation of information available to it as at the date of this document. CCP Overview CCP3 Capture Program CCP3 Storage Program CCP3 Comms/P&I Programs CCP4 CCP Conclusions CCP – A brief history The CCP was founded in 2000. As a partnership of several major energy companies, it provides a unique, collaborative forum for those companies to develop practical CCS knowledge and solutions that relate specifically to the oil and gas industry. Since 2000 the CCP’s expert Technical Teams, made up of engineers, scientists and geologists from member companies, have undertaken well over 150 projects to increase understanding of the science, economics and engineering applications of CCS. In that time, the CCP has worked closely with government organizations - including the US Department of Energy and the European Commission – and more than 60 academic bodies and global research institutes. It has been recognised by the Carbon Sequestration Leadership Forum (CSLF) for its contribution to the advancement of CCS. Its activities are monitored and reviewed by an independent Technical Advisory Board made up of CCS industry experts. -

April 7, 2021 This Note Is Provided to Analysts and Associates That Cover Cenovus and Will Be Posted on the Cenovus Website Unde

April 7, 2021 This note is provided to analysts and associates that cover Cenovus and will be posted on the Cenovus website under Quarterly results in the Investors section. The company will announce its first quarter 2021 results on Friday, May 7th, at 4:00AM MT (6:00AM ET) with a conference call to follow at 9:00AM MT (11:00AM ET). We’d like to remind you of the following items that have been previously disclosed by Cenovus or are a summation of public information. Please note that all such information and statements were made as at the dates of the disclosure documents or conference calls specifically noted below, and this document is not intended to be an update of any such information or statements. Any updates on the prior statements and information summarized in this document will be provided in the company’s announcement of its first quarter results. Corporate: • Cenovus posted a presentation outlining further detail on its planned go forward segmentation and reporting in preparation for our 2021 first quarter results. • “2021 budget to achieve nearly $1 billion of synergies in first year… The budget includes sustaining capital of approximately $2.1 billion to deliver upstream production of approximately 755,000 barrels of oil equivalent per day (BOE/d) and downstream throughput of approximately 525,000 barrels per day (bbls/d).” (Cenovus News Release, January 28, 2021) • “The company expects between $500 million and $550 million of one-time integration related costs such as consultation and legal fees, transfer of licensed seismic data, integration of IT systems, severance associated with workforce reductions and change of control obligations.” (Cenovus News Release, January 28, 2021) - 1 - • Cenovus provides Adjusted Funds Flow sensitivities to benchmark commodity prices for 2021 in its 2021 guidance document. -

Insert Text Here

Cenovus to double production and reserves in Canada $17.7 billion acquisition establishes anchor position in two of Canada’s most attractive oil and gas plays Calgary, Alberta (March 29, 2017) – Cenovus Energy Inc. (TSX: CVE) (NYSE: CVE) has agreed to acquire ConocoPhillips’ 50% interest in the FCCL Partnership, the companies’ jointly owned oil sands venture operated by Cenovus. Cenovus is also purchasing the majority of ConocoPhillips’ Deep Basin conventional assets in Alberta and British Columbia. Combined, these assets have forecast 2017 production of approximately 298,000 barrels of oil equivalent per day (BOE/d). The acquisition is immediately accretive to key metrics, and, assuming the successful completion of a planned divestiture program, is expected to result in an 18% increase in 2018 adjusted funds flow per share compared with Cenovus’s original 2018 forecast. Total consideration for the purchase is $17.7 billion, including $14.1 billion in cash and 208 million Cenovus common shares. The cash component is fully financed with a portion of cash on hand, existing credit facility capacity and committed bridge loans. As part of the transaction, Cenovus has also agreed, in certain circumstances, to make contingent payments to ConocoPhillips. The transaction is expected to close in the second quarter of 2017, subject to customary conditions, including the receipt of necessary regulatory approvals, and has an effective date of January 1, 2017. Concurrent with the acquisition, Cenovus has launched a bought-deal offering of common shares for expected gross proceeds of approximately $3 billion. The bought-deal offering is detailed in a separate news release issued by Cenovus today.