View Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Part VII Transfers Pursuant to the UK Financial Services and Markets Act 2000

PART VII TRANSFERS EFFECTED PURSUANT TO THE UK FINANCIAL SERVICES AND MARKETS ACT 2000 www.sidley.com/partvii Sidley Austin LLP, London is able to provide legal advice in relation to insurance business transfer schemes under Part VII of the UK Financial Services and Markets Act 2000 (“FSMA”). This service extends to advising upon the applicability of FSMA to particular transfers (including transfers involving insurance business domiciled outside the UK), advising parties to transfers as well as those affected by them including reinsurers, liaising with the FSA and policyholders, and obtaining sanction of the transfer in the English High Court. For more information on Part VII transfers, please contact: Martin Membery at [email protected] or telephone + 44 (0) 20 7360 3614. If you would like details of a Part VII transfer added to this website, please email Martin Membery at the address above. Disclaimer for Part VII Transfers Web Page The information contained in the following tables contained in this webpage (the “Information”) has been collated by Sidley Austin LLP, London (together with Sidley Austin LLP, the “Firm”) using publicly-available sources. The Information is not intended to be, and does not constitute, legal advice. The posting of the Information onto the Firm's website is not intended by the Firm as an offer to provide legal advice or any other services to any person accessing the Firm's website; nor does it constitute an offer by the Firm to enter into any contractual relationship. The accessing of the Information by any person will not give rise to any lawyer-client relationship, or any contractual relationship, between that person and the Firm. -

Investment Stewardship 2020 Annual Report

Investment Stewardship 2020 Annual Report For institutional and sophisticated investors only. Not for public distribution. 2020 Annual Report An introduction from our chairman and CEO 1 Resilience and growth in a turbulent year 2 Our four principles 4 Our program 5 Investment Stewardship at a glance 6 Regional roundup 10 Engagement case studies Board composition 14 Oversight of strategy and risk 18 Proposals seek greater climate-change disclosure 22 Attention on diversity as social issues gain the spotlight 26 Executive compensation 30 Shareholder rights 34 Key votes 36 Proxy voting history 44 Company engagements 52 For institutional and sophisticated investors only. Not for public distribution. b An introduction from our chairman and CEO Tim Buckley Vanguard Chairman and Chief Executive Officer Investors come to Vanguard for many reasons. Some are drawn to our client-ownership structure. Others are attracted to our long-term, low-cost investment philosophy. And still others are looking for an investment firm with a strong track record of stability and outperformance. Regardless of your reason for selecting Vanguard, we deeply appreciate your trust and are committed to helping you achieve your financial goals. One of the clearest expressions of how we advocate on your behalf is our engagement with the companies in which we invest. Our Investment Stewardship team speaks with thousands of executives and board members each year to understand how they intend to deliver enduring value to investors. Our conversations delve into the strategic risks facing a portfolio company and how its leadership plans to manage those risks. Many of the issues we discuss are reflected in proxy ballot items, and Vanguard votes each fund’s shares in accordance with what will serve its investors best over a long time horizon. -

Quarterly Portfolio Disclosure

Schroders 29/05/2020 ASX Limited Schroders Investment Management Australia Limited ASX Market Announcements Office ABN:22 000 443 274 Exchange Centre Australian Financial Services Licence: 226473 20 Bridge Street Sydney NSW 2000 Level 20 Angel Place 123 Pitt Street Sydney NSW 2000 P: 1300 180 103 E: [email protected] W: www.schroders.com.au/GROW Schroder Real Return Fund (Managed Fund) Quarterly holdings disclosure for quarter ending 31 March 2020 Holdings on a full look through basis as at 31 March 2020 Weight Asset Name (%) 1&1 DRILLISCH AG 0.000% 1011778 BC / NEW RED FIN 4.25 15-MAY-2024 144a (SECURED) 0.002% 1011778 BC UNLIMITED LIABILITY CO 3.875 15-JAN-2028 144a (SECURED) 0.001% 1011778 BC UNLIMITED LIABILITY CO 4.375 15-JAN-2028 144a (SECURED) 0.001% 1011778 BC UNLIMITED LIABILITY CO 5.0 15-OCT-2025 144a (SECURED) 0.004% 1MDB GLOBAL INVESTMENTS LTD 4.4 09-MAR-2023 Reg-S (SENIOR) 0.011% 1ST SOURCE CORP 0.000% 21VIANET GROUP ADR REPRESENTING SI ADR 0.000% 2I RETE GAS SPA 1.608 31-OCT-2027 Reg-S (SENIOR) 0.001% 2I RETE GAS SPA 2.195 11-SEP-2025 Reg-S (SENIOR) 0.001% 2U INC 0.000% 360 SECURITY TECHNOLOGY INC A A 0.000% 360 SECURITY TECHNOLOGY INC A A 0.000% 361 DEGREES INTERNATIONAL LTD 0.000% 3D SYSTEMS CORP 0.000% 3I GROUP PLC 0.002% 3M 0.020% 3M CO 1.625 19-SEP-2021 (SENIOR) 0.001% 3M CO 1.75 14-FEB-2023 (SENIOR) 0.001% 3M CO 2.0 14-FEB-2025 (SENIOR) 0.001% 3M CO 2.0 26-JUN-2022 (SENIOR) 0.001% 3M CO 2.25 15-MAR-2023 (SENIOR) 0.001% 3M CO 2.75 01-MAR-2022 (SENIOR) 0.001% 3M CO 3.25 14-FEB-2024 (SENIOR) 0.002% -

Aston Martin Lagonda Da

ASTON MARTIN LAGONDA MARTIN LAGONDA ASTON PROSPECTUS SEPTEMBER 2018 ASTON MARTIN LAGONDA PROSPECTUS SEPTEMBER 2018 591176_AM_cover_PROSPECTUS.indd All Pages 14/09/2018 12:49:53 This document comprises a prospectus (the “Prospectus”) relating to Aston Martin Lagonda Global Holdings plc (the “Company”) prepared in accordance with the Prospectus Rules of the Financial Conduct Authority of the United Kingdom (the “FCA”) made under section 73A of the Financial Services and Markets Act 2000 (“FSMA”), which has been approved by the FCA in accordance with section 87A of FSMA and made available to the public as required by Rule 3.2 of the Prospectus Rules. This Prospectus has been prepared in connection with the offer of ordinary shares of the Company (the “Shares”) to certain institutional and other investors described in Part V (Details of the Offer) of this Prospectus (the “Offer”) and the admission of the Shares to the premium listing segment of the Official List of the UK Listing Authority and to the London Stock Exchange's main market for listed securities ("Admission"). This Prospectus updates and replaces in whole the Registration Document published by Aston Martin Holdings (UK) Limited on 29 August 2018. The Directors, whose names appear on page 96 of this Prospectus, and the Company accept responsibility for the information contained in this Prospectus. To the best of the knowledge of the Directors and the Company, who have taken all reasonable care to ensure that such is the case, the information contained in this Prospectus is in accordance with the facts and does not omit anything likely to affect the import of such information. -

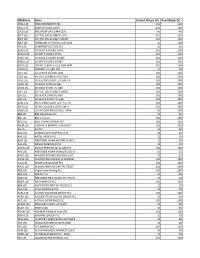

Description Holding Book Cost Market Price Market Value £000'S £000'S

DORSET COUNTY PENSION FUND VALUATION OF PORTFOLIO AT CLOSE OF BUSINESS 31 March 2017 Book Market Description Holding Market Value Cost Price £000's £000's UK EQUITIES MINING ACACIA MINING 33,000 147.93 4.502 148.57 ANGLO AMERICAN ORD USD0.54 270,390 2,804.18 12.27 3,317.69 ANTOFAGASTA ORD GBP0.05 74,500 151.50 8.355 622.45 BHP BILLITON ORD USD0.50 436,926 2,401.54 12.395 5,415.70 CENTAMIN EGYPT LTD 226,000 349.07 1.732 391.43 FRESNILLO 35,500 88.20 15.52 550.96 GLENCORE XSTRATA 2,412,543 5,662.91 3.141 7,577.80 HOCHSCHILD MINING ORD GBP0.25 49,000 108.90 2.765 135.49 KAZ MINERALS 53,600 89.80 4.551 243.93 PETRA DIAMONDS 106,900 169.67 1.329 142.07 POLYMETAL INT'L 53,800 514.30 9.945 535.04 RANDGOLD RESOURCES ORD USD0.05 19,250 485.32 69.7 1,341.73 RIO TINTO ORD GBP0.10 (REG) 250,150 2,876.49 32.185 8,051.08 VEDANTA RESOURCES ORD USD0.10 18,500 75.07 8.11 150.04 Total MINING 15,924.89 28,524.69 OIL & GAS PRODUCERS AFREN PLC 218,000 215.93 0 0.00 BP ORD USD0.25 3,948,100 13,177.95 4.5885 18,115.86 CAIRN ENERGY ORD GBP0.06153846153 119,207 236.32 2.048 244.14 NOSTRUM OIL & GAS 17,700 84.36 4.796 84.89 ROYAL DUTCH 'B' ORD EUR0.07 1,642,961 20,190.09 21.945 36,054.78 TULLOW OIL ORD GBP 0.10 188,500 789.92 1.99026 375.16 Total OIL & GAS PRODUCERS 34,694.58 54,658.45 CHEMICALS CRODA INTL ORD GBP0.10 26,995 211.15 35.77 965.61 ELEMENTIS 99,000 130.23 2.899 287.00 JOHNSON MATTHEY ORD GBP1.00 40,357 446.31 30.82 1,243.80 SYNTHOMER 57,665 118.87 4.751 273.97 VICTREX ORD GBP0.01 17,000 111.61 19.02 323.34 Total CHEMICALS 1,018.16 3,087.91 CONSTRUCTION -

Copy of Default Margin List

IRESSCode Name Current Margin (%) New Margin (%) 0HAL.LSE AEROVIRONMENT INC 100 100 0R22.LSE BARRICK GOLD CORP 100 100 17GK.LSE MEGAFON OAO-144A GDR 40 40 2LFT.LSE SG FTSE 100 X2 DAILY LONG 100 100 2SFT.LSE SG FTSE 100 X2 DAILY SHORT 100 100 38LF.LSE SBERBANK OF RUSSIA-GDR 144A 40 100 3IN.LSE 3I INFRASTRUCTURE PLC 20 20 3LAU.LSE SG GOLD X3 DAILY LONG 100 100 3LWO.LSE SG WTI X3 DAILY LONG 100 100 3SAU.LSE SG GOLD X3 DAILY SHORT 100 100 3SWO.LSE SG WTI X3 DAILY SHORT 100 100 42KU.LSE GRUPO CLARIN S-CL B GDR 144A 100 100 500U.LSE AMUNDI ETF S&P 500 20 20 51FL.LSE ELECTRICA SA-GDR-144A 100 100 53GI.LSE AFI DEVELOPMENT PLC-GDR 100 100 5DEL.LSE SG X5 LONG DAILY LEV DAX TR 100 100 5GOL.LSE SG GOLD LONG X5 GBP 100 100 5GOS.LSE SG GOLD SHORT X5 GBP 100 100 5SFT.LSE SG FTSE 100 X5 DAILY SHORT 100 100 5SIL.LSE SG SILVER LONG X5 GBP 100 100 5SIS.LSE SG SILVER SHORT X5 GBP 100 100 5UKL.LSE SG X5 LONG DAILY LEV FTSE TR 100 100 5WTI.LSE SG WTI X5 DAILY LONG GBP 2 100 100 66XD.LSE EDITA FOOD INDUSTRIES -144A 40 100 888.LSE 888 HOLDINGS PLC 20 30 88E.LSE 88 Energy Ltd 100 100 8PG.LSE EIGHT PEAKS GROUP PLC 100 100 98LM.LSE TURKIYE IS BANKASI-144A GDR 100 100 AA.LSE AA PLC 40 40 AA4.LSE AMEDEO AIR FOUR PLUS LTD 25 25 AAF.LSE AIRTEL AFRICA PLC 50 50 AAIF.LSE ABERDEEN ASIAN INCOME FUND L 25 30 AAL.LSE ANGLO AMERICAN PLC 15 10 AAOG.LSE ANGLO AFRICAN OIL & GAS PLC 100 100 AAS.LSE ABERDEEN ASIAN SMALLER COS-O 65 55 AASU.LSE AMUNDI ETF MSCI EM ASIA UCIT 20 25 AATG.LSE ALBION TECHNOLOGY & GENERAL 100 100 AAU.LSE ARIANA RESOURCES PLC 100 100 AAVC.LSE ALBION VENTURE -

Marketplace Sponsorship Opportunities Information Pack 2017

MarketPlace Sponsorship Opportunities Information Pack 2017 www.airmic.com/marketplace £ Sponsorship 950 plus VAT Annual Conference Website * 1 complimentary delegate pass for Monday www.airmic.com/marketplace only (worth £695)* A designated web page on the MarketPlace Advanced notification of the exhibition floor plan section of the website which will include your logo, contact details and opportunity to upload 20% discount off delegate places any PDF service information documents Advanced notification to book on-site meeting rooms Airmic Dinner Logo on conference banner Advanced notification to buy tickets for the Annual Dinner, 12th December 2017 Logo in conference brochure Access to pre-dinner hospitality tables Opportunity to receive venue branding opportunities Additional Opportunities * This discount is only valid for someone who have never attended an Airmic Conference Airmic can post updates/events for you on before Linked in/Twitter ERM Forum Opportunity to submit articles on technical subjects in Airmic News (subject to editor’s discretion) Opportunity to purchase a table stand at the ERM Forum Opportunity to promote MP content online via @ Airmic Twitter or the Airmic Linked In Group About Airmic Membership Airmic has a membership of about 1200 from about 480 companies. It represents the Insurance buyers for about 70% of the FTSE 100, as well as a very substantial representation in the mid-250 and other smaller companies. Membership continues to grow, and retention remains at 90%. Airmic members’ controls about £5 billion of annual insurance premium spend. A further £2 billion of premium spend is allocated to captive insurance companies within member organisations. Additionally, members are responsible for the payment of insurance claims from their business finances to the value of at least £2 billion per year. -

PAF Corporate Licence Holders - Listed Alphabetically PDF Created: 03 09 2020

PAF Licensing Centre PAF ® Corporate Licensees: PAF Corporate Licence Holders - Listed Alphabetically PDF created: 03 09 2020 Company Name. Corporate Licence Holder AGF Holdings UK Ltd Allianz Management Services Ltd Allianz Business Services Allianz Management Services Ltd Allianz Cornhill Engineering Inspection Services Limited Allianz Management Services Ltd Allianz Cornhill Equity Investments Limited Allianz Management Services Ltd Allianz Cornhill Holdings Limited Allianz Management Services Ltd Allianz Cornhill Insurance Company Pension Fund Trustees Allianz Management Services Ltd Limited Allianz Cornhill Insurance Plc Allianz Management Services Ltd Allianz Cornhill Management Services Limited Allianz Management Services Ltd Allianz Engineering Inspection Services Limited Allianz Management Services Ltd Allianz Equity Investments Ltd Allianz Management Services Ltd Allianz Holdings Allianz Management Services Ltd Allianz Insurance Plc Allianz Management Services Ltd Allianz International Limited Allianz Management Services Ltd Allianz Pension Fund Trustees Limited Allianz Management Services Ltd Allianz Properties Limited Allianz Management Services Ltd Allianz UK Ltd Allianz Management Services Ltd British Reserve Insurance Company Limited Allianz Management Services Ltd Buddies Enterprises Limited Allianz Management Services Ltd Domestic Insurance Services Limited Allianz Management Services Ltd Fairmead Distribution Services Limited Allianz Management Services Ltd Fairmead Insurance Limited Allianz Management Services Ltd Fairmead -

STOXX UK 180 Last Updated: 02.10.2017

STOXX UK 180 Last Updated: 02.10.2017 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) GB0005405286 0540528 HSBA.L 040054 HSBC GB GBP Y 171.2 1 1 GB0002875804 0287580 BATS.L 028758 BRITISH AMERICAN TOBACCO GB GBP Y 121.6 2 2 GB00B03MLX29 B09CBL4 RDSa.AS B09CBL ROYAL DUTCH SHELL A GB EUR Y 115.3 3 3 GB0007980591 0798059 BP.L 013849 BP GB GBP Y 107.0 4 4 GB0009252882 0925288 GSK.L 037178 GLAXOSMITHKLINE GB GBP Y 83.1 5 5 GB0009895292 0989529 AZN.L 098952 ASTRAZENECA GB GBP Y 71.2 6 9 GB0002374006 0237400 DGE.L 039600 DIAGEO GB GBP Y 70.1 7 6 GB00B10RZP78 B10RZP7 ULVR.L 091321 UNILEVER PLC GB GBP Y 64.2 8 7 GB00BH4HKS39 BH4HKS3 VOD.L 071921 VODAFONE GRP GB GBP Y 63.2 9 8 GB0008706128 0870612 LLOY.L 087061 LLOYDS BANKING GRP GB GBP Y 55.3 10 12 GB0007099541 0709954 PRU.L 070995 PRUDENTIAL GB GBP Y 52.4 11 11 GB00B24CGK77 B24CGK7 RB.L 072769 RECKITT BENCKISER GRP GB GBP Y 51.9 12 10 GB0007188757 0718875 RIO.L 071887 RIO TINTO GB GBP Y 47.4 13 13 JE00B4T3BW64 B4T3BW6 GLEN.L GB10B3 GLENCORE PLC GB GBP Y 47.0 14 14 JE00B2QKY057 B2QKY05 SHP.L 079980 SHIRE GB GBP Y 39.4 15 16 GB00BDR05C01 BDR05C0 NG.L 024282 NATIONAL GRID GB GBP Y 35.9 16 15 GB0031348658 3134865 BARC.L 007820 BARCLAYS GB GBP Y 35.1 17 19 GB0004544929 0454492 IMB.L 045449 IMPERIAL BRANDS GB GBP Y 34.6 18 18 GB0000566504 0056650 BLT.L 005666 BHP BILLITON GB GBP Y 31.5 19 17 GB00BD6K4575 BD6K457 CPG.L 053315 COMPASS GRP GB GBP Y 28.6 20 20 GB0030913577 3091357 BT.L 014084 BT GRP GB GBP Y 28.2 21 21 GB0002162385 0216238 AV.L -

Your European Breakdown Policy Booklet

Your European breakdown policy booklet RIV 90836312.indd 1 3/27/18 9:23 PM Generated at: Tue Mar 27 21:29:48 2018 Contents Welcome to Churchill breakdown services 1 General exclusions applying to this policy 9 Easy index 2 General conditions applying to this policy 10 Your European breakdown policy 3 Your privacy 12 Definitions 4 Important information about your breakdown policy 14 Churchill European Rescue Services (CERS) 6 What to do if your vehicle Section 1 Cover prior to departure 6 breaks down 16 Section 2 Roadside assistance and towing 6 Membership cards on flap Section 3 Loss of use of vehicle 6 Useful phone numbers back cover Section 4 Returning your vehicle to the United Kingdom 7 Section 5 Providing a chauffeur to return you home 7 Section 6 Delivering spare parts 7 Section 7 Legal defence expenses 7 90836312.indd 1 3/27/18 9:23 PM Generated at: Tue Mar 27 21:29:48 2018 Welcome to Churchill European breakdown services Dear Customer Welcome to Churchill breakdown services, provided by Green Flag and underwritten by U K Insurance Limited (all companies are part of the same group). We are passionate about insurance, and determined to make sure that you receive outstanding customer service at all times. We will do our best to make sure that buying breakdown services from us is as easy and trouble-free as possible. We hope that you stay our customer for many years to come. Happy motoring 1 90836312.indd 1 3/27/18 9:23 PM Generated at: Tue Mar 27 21:29:48 2018 Easy index Breakdown Cover What do I do if my vehicle breaks down? phone -

General Insurance: the Digital Experience

General Insurance: The Digital Experience How did the insurers we tested rank? RANK Insurer Quote Claim Renewal MTA Online Telematics Webchat Dedicated Score Documents Offered Mobile App 1 Aviva 96.0 2= Hastings Direct 87.5 2= Quote me Happy 87.5 4 Swift Cover 83.5 5 More Th>n 76.0 6 Direct Line 68.0 7= Admiral 67.0 7= Allianz 67.0 9 AXA 62.5 10= Elephant/Diamond 50.5 10= LV= 50.5 12= Co-op 50.0 12= esure 50.0 14 Privilege 46.0 15 Legal & General 38.0 16= Home Protect NA 37.5 16= RIAS 37.5 18 Zurich 34.0 19 Lloyds/Halifax/BoS 29.5 20= Churchill 25.0 20= Hiscox 25.0 20= People’s Choice 25.0 20= Sheila’s Wheels 25.0 24 NFU 0.0 Supported Mostly supported Partially supported Not supported 1 Altus Consulting research 2017, covering digital services altus.co.uk/consulting for home and motor insurance products. General Insurance: Beyond quote and buy, digital capabilities are lacking1 The Digital Overall % of leading insurers offering services digitally Experience Quote MTAs Renewal Claim Key to Questions: 1: Quote 2: Claim 8 1 3: Renewal 4: MTA 7 Rank 2 5: Online Documents 6 # 3 6: Telematics 96% 42% 21% 4% 5 4 7: Webchat Offered 8: Dedicated Mobile App How did the insurers we tested rank? Rank Rank Rank Rank 1 2= 2= 4 Rank Rank Rank Rank 5 6 7= 7= Rank Rank Rank Rank 9 10= 10= 12= Rank Rank Rank Rank 12= 14 15 NA 16= Rank Rank Rank Rank 16= 18 19 20= Rank Rank Rank Rank 20= 20= 20= 24 Supported Mostly supported Partially supported Not supported 1 Altus Consulting research 2017, covering digital services altus.co.uk/consulting for home and motor insurance products. -

Charlotte Eborall

3 Verulam Buildings WC1R 5NT DX: LDE 331 Gray’s Inn, London. Telephone: +44(0)20 7831 8441 Barristers regulated by the Bar Standards Board Charlotte Eborall Email Address: [email protected] Year Of Call: 2004 Charlotte is an experienced commercial senior junior specialising in complex and high value litigation in the fields of banking, financial services, civil fraud and general commercial disputes. Described in the directories as “steeped in banking law” and “strong in banking and finance cases”, Charlotte has extensive experience of cases involving banks and other financial institutions. She is known for being “very personable” and “extremely client-friendly” with “a good eye for detail…who’s rated by banks as well as solicitors.” Charlotte is regularly instructed as sole counsel and is “tenacious in fighting for her client”, often appearing against silks. She “gets to grips well with cases quickly and efficiently” and is “really impressive and noted for her rigorous analysis of cases” her advisory work being described as “clear, measured and methodical” and “her written work output is excellent.” During 2019 and 2020, Charlotte was instructed in one of the leading banking litigation cases, PCP Capital Partners LLP v Barclays Bank plc, led by David Quest QC and working together with Jeffery Onions QC, Alex Polley and Oliver Butler of One Essex Court), on behalf of Barclays Bank, to defend the £1.6 billion claim for fraudulent misrepresentation alleged by Ms Staveley (the principal of PCP) concerning the bank’s capital raising during Autumn 2008 at the height of the financial crisis. Charlotte is currently acting in a number of her own commercial and banking cases (noted below).