View Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Impacts of Future Sea Level Rise and High Water on Roads, Railways And

Master Thesis in Geographical Information Science nr 98 Impacts of future sea level rise and high water on roads, railways and environmental objects A GIS analysis of the potential effects of increasing sea levels and highest projected high water in Scania, Sweden Emilie Arnesten 2019 Department of Physical Geography and Ecosystem Science Centre for Geographical Information Systems Lund University Sölvegatan 12 S -223 62 Lund Sweden Emilie Arnesten (2019). Impacts of future sea level rise and high water on roads, railways and environmental objects: a GIS analysis of the potential effects of increasing sea levels and highest projected high water in Scania, Sweden. Master’s degree thesis, 30 credits in Geographical Information Systems (GIS) Department of Physical Geography and Ecosystem Science, Lund University ii Impacts of future sea level rise and high water on roads, railways and environmental objects A GIS analysis of the potential effects of increasing sea levels and highest projected high water in Scania, Sweden Emilie Arnesten Master thesis, 30 credits, in Geographical Information Systems (GIS) Autumn 2018 – Spring 2019 Supervisors: Andreas Persson Lund University Jan-Fredrik Wahlin & Peter Sieurin Swedish Transport Administration Department of Physical Geography and Ecosystem Science Centre for Geographical Information Systems Lund University iii Acknowledgements I would like to thank my supervisor at Lund University, Andreas Persson, for support and guidance in academic writing, geographical information systems and climate change adaptation. I would also like to thank my supervisors at the Swedish Transport Administration, Jan- Fredrik Wahlin and Peter Sieurin, for sharing their knowledge in the subjects handled within this study, and for enabling me to do the thesis I wished to do. -

Verksamheter Med Länsstyrelsen Skåne Som Tillsynsmyndighet Sida 1 Av 6

2021-09-01 Verksamheter med Länsstyrelsen Skåne som tillsynsmyndighet Sida 1 av 6 Nummer Anläggning Kommun 1260-101 Foodhills AB, Bjuv Bjuv 1260-129 Sven Jönssons Cykelaffär AB Bjuv 1272-50-001 Bromölla avloppsreningsverk Bromölla 1272-125 G. Larsson Starch Technology AB Bromölla 1272-102 Geberit Production AB Bromölla 1272-101 Stora Enso Paper AB Bromölla 1272-118 Ytbehandlingsteknik i Näsum AB Bromölla 1272-60-004 Åsens Avfallsanläggning Bromölla 1272-20-011 Östad Bromölla 1272-20-001 Östad Norr Bromölla 1278-20-017 Förslöv grustäkt Båstad 1278-101 LINDAB VENTILATION AB Båstad 1278-60-001 NSR återvinningsanläggning Bås Båstad 1278-50-004 Torekovs avloppsreningsverk Båstad 1285-50-001 Ellinge Avloppsreningsverk Eslöv 1285-144 O. Kavli AB Eslöv 1285-101 Orkla Foods Sverige AB Eslöv 1285-20-006 Rönneholms mosse Eslöv 1285-91-804 Skibaröd Eslöv 1285-158 Örtofta Kraftvärmeverk Eslöv 1285-105 Örtofta Sockerbruk Eslöv 1283-109H Filborna Kraftvärmeverk Helsingborg 1283-109A Fjärrvärmecentral, Israel (FCI) Helsingborg 1283-75-001 Helsingborgs Hamn AB Helsingborg 1283-101 KEMIRA KEMI AB Helsingborg 1283-60-001 NSR återvinningsanläggning Hel Helsingborg 1283-60-002 RÖKILLE AVFALLSUPPLAG Helsingborg 1283-102 Solenis Sweden AB Helsingborg 1283-109B Västhamnsverket, (VHV) Helsingborg 1283-50-001 Öresundsverket, AVR Helsingborg 1293-60-001 Hässleholms Kretsloppscenter Hässleholm 1293-20-910 Vinne mosse Hässleholm 1293-20-901 Åbuamossen Hässleholm 1284-50-001 Höganäs avloppsreningsverk Höganäs 1284-101B Höganäs Hetvattencentral 1 Höganäs 1284-101 Höganäs -

Väg E6 Trelleborg-Vellinge

UV SYD RAPPORT 2006:15 MALMÖ KULTURMILJÖ, ENHETEN FÖR ARKEOLOGI, RAPPORT 2006:6 ARKEOLOGISK UTREDNING STEG 1 Väg E6 Trelleborg-Vellinge Skåne, Trelleborgs och Vellinge kommuner, Maglarp, Skegrie, Håslöv och Vellinge socknar. Dnr 421-18921-05 Bengt Jacobsson och Mats Riddersporre Väg E6 Trelleborg–Vellinge 1 Riksantikvarieämbetet Malmö Kulturmiljö Avdelningen för arkeologiska undersökningar Box 406 UV Syd 201 24 Malmö Odlarevägen 5, Tel. 040-34 44 75 226 60 Lund Fax 040-34 42 45 Tel. 046-32 95 00 www.malmo.se Fax 046-32 95 39 www.raa.se/uv © 2006 Riksantikvarieämbetet UV Syd Rapport 2006:15 Malmö Kulturmiljö, Enheten för arkeologi, rapport 2006:6 ISSN 1104-7526 ISSN 1653-4948 Kart- och ritmaterial Henrik Pihl Layout Henrik Pihl Utskrift UV Syd Lund, 2006 Kartor ur allmänt kartmaterial, © Lantmäteriverket, 801 82 Gävle. Dnr L 1999/3 Innehåll Sammanfattning 5 Inledning 5 Det förhistoriska landskapet 7 Det historiska landskapet 9 Utredningen 10 Arbetets upplägg 10 Resultat 12 Utvalda områden 13 Utvärdering och förslag till åtgärd 28 Bilagor 29 Referenser 30 Administrativa uppgifter 31 Fig. 1. Utsnitt ur GSD-Röda kartan, Skåne län, med vägsträckningen markerad. Skala 1:250 000. 4 UV Syd Rapport 2006:15 Väg E6 Trelleborg – Vellinge Bengt Jacobsson och Mats Riddersporre Sammanfattning Vägverket planerar att bygga om väg E6, delen Trelleborg – Vellinge, till motorvägsstandard. Sträckan är ca 13 kilometer lång. Som ett led i att klargöra fornlämningssituationen utmed vägsträckan har Riks- antikvarieämbetet, avdelningen för arkeologiska undersökningar UV Syd, på uppdrag av länsstyrelsen i Skåne län, och i samarbete med Malmö Kulturmiljö, utfört en arkeologisk utredning steg 1. -

1 Globala Målen

GLOBALA MÅLEN | BAKGRUND 1 FÖR KÄVLINGE, LOMMA, SIMRISHAMN, SJÖBO, SKURUP, SVEDALA, TOMELILLA, TRELLEBORG, VELLINGE OCH YSTAD 2 BAKGRUND | GLOBALA MÅLEN Remiss Remiss GLOBALA MÅLEN | BAKGRUND 3 Tänk att du bor i ett hus och helt plötsligt inte kan göra dig av med dina sopor. Vad skulle du göra? Du kanske börjar lägga dem i källaren. Sen fyller du vinden. Boendemiljön blir sämre och sämre. Antagligen skulle du vilja flytta. Planeten är vårt gemensamma hem. Här ska våra barn bo och deras barn i all evighet. Eller? Vilket hem får de? Allt vi köper gör att det uppstår avfall, även när det tillverkas. Oftast i andra delar av världen. Hur mycket avfall rymmer vår planet? Vart kan vi flytta? Remiss Vi harRemiss en enda planet. Ett enda hem. 4 FÖRORD | VAD ÄR AVFALL FÖR DIG? VAD ÄR AVFALL för dig? Vad tänker du på när du hör ordet avfall? Kanske tänker du på soporna under diskbänken, på din halvgamla fåtölj, eller din omoderna mobiltelefon? Eller så tänker du att din soffa är ett kap för någon annan och säljer den vidare? Eller så tänker du efter innan du handlar nya saker och lagar det som är trasigt, innan du ger dem till återbruk? En privatperson i Sverige ger upphov till nästan 500 kg sopor per år. För 100 år sedan var samma siffra cirka 30 kg per person. En sak är säker, allt vi handlar och i stort sett allt som produceras kommer att bli avfall i framtiden. I Sverige kommer befolkningen att fortsätta öka under perioden fram till år 2030. -

CONTENTS Folk Life in Sweden 1871 by AH

(ISSN 0275-9314) CONTENTS Folk Life in Sweden 1871 65 by A.H Guernsey Mathias Bernard Pederson Found 85 by Elisabeth Thorsell Finding Surprising Ties to Halland Swedes 87 by Carl O. Helstrom, Jr. Using the Demographic Database for S. Sweden 96 by Dean Wood Old Issue Revisited 109 fry Carol J. Bern Swenson Center Serendipity 114 by Jill Seaholm The Poor Y ou Always Have with You 124 by Elisabeth Thorsell Genealogical Queries 126 Vol. XXIII June 2003 No. 2 Copyright ©2003 (ISSN 0275-9314) Swedish American Genealogist Publisher: Swenson Swedish Immigration Research Center Augustana College Rock Island, IL 61201-2296 Telephone: 309-794-7204 Fax: 309-794-7443 E-mail: [email protected] Web address: http://www.augustana.edu/administration/swenson/ Editor: Harold L. Bern, Jr. 2341 E. Lynnwood Dr., Longview, WA 98632 E-mail: [email protected] Editor Emeritus: Nils William Olsson, Ph.D., F.A.S.G., Winter Park, FL Contributing Editor: Peter Stebbins Craig. J.D., F.A.S.G., Washington, D.C. Technical editor: Elisabeth Thorsell, Järfälla, Sweden Editorial Committee: Dag Blanck, Uppsala, Sweden Ronald J. Johnson, Madison, WI Christopher Olsson, Stockton Springs, ME Ted Rosvall, Enasen-Falekvarna. Sweden Priscilla Jönsson Sorknes, Minneapolis, MN Swedish American Genealogist, its publisher, editors, and editorial committee assume neither responsibility nor liability for statements of opinion or fact made by contributors. Correspondence. Please direct editorial correspondence such as manuscripts, queries, book reviews, announcements, and ahnentafeln to the editor in Longview. Correspondence regarding change of address, back issues (price and availa• bility), and advertising should be directed to the publisher in Rock Island. -

Konsekvensutredning För Lokala Trafikföreskrifter Om Förbud Mot

KONSEKVENSUTREDNING 1(8) 2018-10-31 Dnr 258-31356-2018 Kontaktperson Förvaltningsjuridiska enheten Ida Persson [email protected] 010-224 17 28 Telefontid 09.00-12.00 Konsekvensutredning för lokala trafikföreskrifter om förbud mot omkörning med tung lastbil på väg E6, Velllinge, Malmö, Burlövs, Lomma, Kävlinge, Landskrona och Helsingborgs kommuner; 1. Vad är problemet och vad ska uppnås? Idag finns fem olika förbud mot omkörning med tung lastbil på väg E6 i Skåne enligt följande; mellan trafikplats 19 (Alnarp), Burlövs och Lomma kommuner, och trafikplats 26 (Landskrona Norra), Landskrona kommun vilket gäller vardagar utom vardag före sön- och helgdag klockan 6.00-9.00 och 16.00-18.00, Länsstyrelsens lokala trafikföreskrifter 12TFS 2010:18- 20, på väg E6 i norrgående körriktning mellan 1250 meter söder om väg 1370 och 650 meter norr om väg 1370, Helsingborgs kommun, förbudet är inte tidsbegränsat, Länsstyrelsens lokala trafikföreskrifter 12FS 2002:1867, och på väg E6 i södergående körriktning mellan 900 meter norr om väg 1370 och 1300 meter söder om väg 1370, Helsingborgs kommun, förbudet är inte tidsbegränsat, Länsstyrelsens lokala trafikföreskrifter 12FS 2002:1867. Väghållningsmyndigheten, Trafikverket Region Syd, har ansökt om en utökning av befintliga lokala trafikföreskrifter att gälla på hela vägsträckan mellan trafikplats 8 (Vellinge S), Vellinge kommun, och trafikplats 30, (Kropp), Helsingborgs kommun, med undantag från sträckorna vid rastplats Glumslöv Ö, Landskrona kommun, med stigningsfält (tre körfält i färdriktningen). -

Annual Report 2017 in Brief 2 Sysav 2017

ANNUAL REPORT 2017 IN BRIEF 2 SYSAV 2017 This report is an extract from Sysavs annual- and sustainability report 2017. The complete report is only avaliable in Swedish. For questions concerning the report, contact [email protected] Group sales for the year KSEK 915,100 Profit after financial items KSEK 71,000 Visits to recycling centres 2 ,111, 8 0 0 Facebook post with the most views: a love song about the new recycling container 37,000 We recovered 97.2% of the waste we received into new materials and energy 97.2% We kept warm with recovered energy – 60% of the district heating in Malmö and Burlöv 60% comes from Sysav SYSAV 2017 3 Our Sysav Sysav is owned by 14 municipalities in Skåne – and ultimately BUSINESS CONCEPT the residents of those municipalities. Sysav offers safe, secure waste management, where These municipalities are Burlöv, Kävlinge, Lomma, Lund, reuse and recovery of materials and energy are Malmö, Simrishamn, Sjöbo, Skurup, Staffanstorp, Svedala, maximised in a cost-effective way, focusing on the Tomelilla, Trelleborg, Vellinge and Ystad. environment and resource management. In co-operation with the owner municipalities, Sysav is responsible for ensuring that waste from the region’s households CORE VALUES is dealt with, recycled and treated in the best possible way. Delighted customers through quality and service. Waste from companies and from other regions and countries is managed by the subsidiary Sysav Industri AB. Thanks to its core business and its training and information initiatives, Sysav is a strong player on the market that contributes to a more sustainable society. -

Bitillsynmän I Skåne 2020

Bitillsynare i Skåne 2021 dnr: 605-1861-2021 Kommun Bitillsynsman Adress Ort Telefon E-mail Båstad Björn Berndtsson Fornåkersväg 14 269 73 Förslöv 070-344 33 47 [email protected] Båstad Jonas Berndtsson Kroken 205 269 73 Förslöv 070-656 76 38 [email protected] Ängelholm Christel Gustavsson Farhultsvägen 205 263 95 Farhult 070-592 76 38 [email protected] Ängelholm Fahrudin Cehajic Odalgatan 1 262 53 Ängelholm 070-496 31 62 [email protected] Åstorp Lars Åke Eriksson Ö.Fjärestadsväg 180 253 42 Vållåkra 070-433 35 82 [email protected] Klippan Kent Tofft Rögnaröd 4628 264 54 Ljungbyhed 070-813 00 26 [email protected] Klippan Karl-Henrik Jansson Bladgatan 14C 264 36 Klippan 072-734 87 32 [email protected] Perstorp Kent Tofft Rögnaröd 4628 264 54 Ljungbyhed 070-813 00 26 [email protected] Perstorp Karl-Henrik Jansson Bladgatan 14C 264 36 Klippan 072-734 87 32 [email protected] Örkelljunga Fahrudin Cehajic Odalgatan 1 262 53 Ängelholm 070-496 31 62 [email protected] Hässleholm Erling Andersson M P Nilssons väg 4 281 97 Ballingslöv 0451-313 86; 070-631 38 66 [email protected] Hässleholm Stig Hansson Snorresväg 8 281 43 Hässleholm 070-960 91 23 [email protected] Osby Tolfte Carlsson Smedjegatan 6 287 72 Traryd 070-244 05 95 Osby Roy Quarton Tosthult 1195 280 70 Lönsboda 076-039 00 71 [email protected] Östra Göinge Göran Håkansson Högsma 1039 289 72 Sibbhult 070-575 32 62 [email protected] Bromölla Anders Jansson Bygdegårdsvägen 27 297 72 Everöd 076-139 06 24 [email protected] Kristianstad -

Översiktsplan 2018 DEL 1: PLANSTRATEGI OCH MARKANVÄNDNING

Översiktsplan 2018 DEL 1: PLANSTRATEGI OCH MARKANVÄNDNING ANTAGEN AV KOMMUNFULLMÄKTIGE 28 NOVEMBER 2018 Beställare Bilder och foto framsida Kommunstyrelsen Sandellsandberg arkitekter AB Istockphoto Styrgrupp Scandnav bildbyrå, Anders Andersson Scandnav bildbyrå, Jens Lindström Linda Allansson Wester, Kommunstyrelsens ordförande (M) Scandnav bildbyrå, Jörgen Wiklund Ambjörn Hardenstedt, Kommunstyrelsens vice ordförande (S) Leif Öst Per Olof Lindgren, Tekniska nämndens ordförande (L) Ingimage Björn Jönsson, Tekniska nämndens 2:e vice ordförande (S) Billy Lindberg Sverker Nordgren, Bygg- och miljönämndens ordförande (M) Geir Hansen, Bygg- och miljönämndens 2:e vice ordförande (S) Övriga bilder och foto Medverkande Svedala kommun om inget annat anges Lena Gerdtsson, samhällsbyggnadschef, Bygg och miljö (t.o.m. utställning) Jeanette Widén Gabrielsson, planarkitekt, Bygg och miljö Kartor Karin Gullberg, stadsarkitekt, Bygg och miljö Bygg och Miljö Fredrik Löfqvist, teknisk chef, Miljö och teknik Geodata har hämtats från nedanstående myndig- Bengt Nilsson, kanslichef, Kommunkansliet (t.o.m. 2016) heter och sammanställts av personal på Bygg och Thomas Carlsson, näringslivs och turismutvecklare, Kommunkansliet miljö. Linda Wolski, miljöstrateg, Bygg och miljö Med upphovsrätt ©: Lowe Kisiel, planarkitekt, Bygg och miljö Lantmäteriet Geodatasamverkan, Sveriges geo- Lisa Norfall, planarkitekt, Bygg och miljö (t.o.m. utställning) logiska undersökningar (SGU), Försvarsmakten, Anne-Marie Pedersen, VA chef, Miljö och teknik Skogsstyrelsen, Naturvårdsverket -

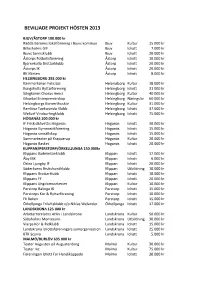

Beviljade Projekt Hösten 2013

BEVILJADE PROJEKT HÖSTEN 2013 BJUV/ÅSTORP 100.000 kr Rädda Barnens lokalförening i Bjuvs kommun Bjuv Kultur 15.000 kr Billesholms GIF Bjuv Idrott 7.000 kr Bjuvs tennisklubb Bjuv Idrott 20.000 kr Åstorps Fotbollsförening Åstorp Idrott 10.000 kr Björnekulla Brottarklubb Åstorp Idrott 20.000 kr Åstorps IK Åstorp Idrott 20.000 kr BK Klinten Åstorp Idrott 8.000 kr HELSINGBORG 292.000 kr Kammarkören Felicitas Helsingborg Kultur 18.000 kr Kungshults Ryttarförening Helsingborg Idrott 31 000 kr Sångkören Chorus Amici Helsingborg Kultur 40 000 kr Glowbal Entreprenörskap Helsingborg Näringsliv 60 000 kr Helsingborgs Konserthuskör Helsingborg Kultur 31.000 kr Ramlösa Taekwondo Klubb Helsingborg Idrott 37.000 kr WeSurf Vindsurfingklubb Helsingborg Idrott 75.000 kr HÖGANÄS 100.000 kr IF Friskis&Svettis Höganäs Höganäs Idrott 30.000 kr Höganäs Gymnastikförening Höganäs Idrott 15.000 kr Höganäs simsällskap Höganäs Idrott 15.000 kr Sommarteater på Krapperup Höganäs Kultur 20.000 kr Höganäs Basket Höganäs Idrott 20.000 kr KLIPPAN/PERSTORP/ÖRKELLJUNGA 150.000kr Klippans Badmintonklubb Klippan Idrott 17.000 kr Åby IBK Klippan Idrott 6.000 kr Östra Ljungby IF Klippan Idrott 20.000 kr Söderåsens Brukshundklubb Klippan Utbildning 10.000 kr Klippans Brottarklubb Klippan Idrott 10.000 kr Klippans FF Klippan Idrott 20.000 kr Klippans Ungdomsorkester Klippan Kultur 10.000 kr Perstorp Bälinge IK Perstorp Idrott 15.000 kr Perstorps Kör & Ryttarförening Perstorp Idrott 10.000 kr Fk Boken Perstorp Idrott 15.000 kr Örkelljunga Friluftsklubb c/o Niklas Welander Örkelljunga -

DOKUMENTATION Der Städtepartnerschaftlichen Und Internationalen Kontakte

DOKUMENTATION der städtepartnerschaftlichen und internationalen Kontakte STADT BErgEN AUf rügEN in den Jahren 1990 – 2009 DOKUMENTATION der städtepartnerschaftlichen und internationalen Kontakte der Stadt BErgen auf rügen in den Jahren 1990 – 2009 DOKUMENTATION Vorwort Sehr geehrte Damen und Herren! Die Ihnen vorliegende Dokumentation beinhaltet eindrucksvoll die städ- tepartnerschaftlichen Beziehungen und die internationalen Aktivitäten der Stadt Bergen auf Rügen. Neben den seit 1990 möglichen innerdeutschen Kontakten entstanden aufrichtige Freundschaften über die Ostsee nach Skandinavien und zum polnischen Nachbarland. So besteht seit 20 Jahren eine intensive Partnerschaft zur Stadt Oldenburg in Holstein und später eine im Drei- erverbund funktionierende Freundschaft mit der schwedischen Stadt Svedala und der polnischen Stadt Goleniow. Diese Kontakte werden nicht nur von den politisch Verantwortlichen gepflegt, sondern waren und sind vor allem Begegnungen unserer Bürgerinnen und Bürger, unserer Kinder und Jugendlichen und der Mitglieder von Vereinen aller gesellschaftlicher Bereiche. Darüber hinaus ist die Stadt Bergen auf Rügen durch ihre territoriale Lage und ihre Stellung als Mit- telzentrum der Insel Rügen oft Austragungsort überregionaler, nationaler und europäischer Veranstal- tungen und ist dabei immer an weiteren internationalen Kontakten auf wirtschaftlichen oder kulturellen Gebieten interessiert. Bergen auf Rügen profiliert sich aber auch als Stadt der Zukunft für Bildung und Gesundheit. Dafür wurden bereits wichtige Voraussetzungen -

LUCSUS Lund University Centre for Sustainability Studies

A Tale of Three Cities A comparative analysis of climate policy formulation in Swedish municipalities Emily Norford Master Thesis Series in Environmental Studies and Sustainability Science, No 2015:016 A thesis submitted in partial fulfillment of the requirements of Lund University International Master’s Programme in Environmental Studies and Sustainability Science (30hp/credits) LUCSUS Lund University Centre for Sustainability Studies A Tale of Three Cities A comparative analysis of climate policy formulation in Swedish municipalities Emily Norford A thesis submitted in partial fulfillment of the requirements of Lund University International Master’s Programme in Environmental Studies and Sustainability Science Submitted May 13, 2015 Supervisor: Henner Busch, LUCSUS, Lund University Abstract The adage “think global, act local” can be a fitting description of how to address climate change. Municipalities are often responsible for implementing the measures required to reduce greenhouse gas emissions and shift to a more climate-neutral development trajectory. However, there is a vast spectrum of municipal ambition regarding climate, and not all municipalities manage to have robust and ambitious climate policies. Sweden is a country that both has ambitious climate goals and affords a high amount of autonomy to local-level governing bodies. This thesis investigates how municipalities in Skåne, Sweden develop policies to address climate change, with a focus on how they approach the national “reduced climate impact” environmental quality objective. It seeks to unveil the conditions that enable ambitious climate policy at the municipal level by comparing Hässleholm, Vellinge, and Kristianstad, which exhibit many similar characteristics but have varying levels of climate policy success – which I define as having in place an ambitious and robust program to reduce climate impact.