Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report and Accounts 2004

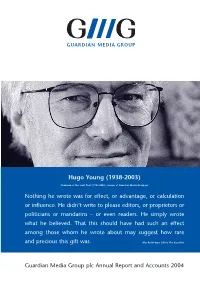

Hugo Young (1938-2003) Chairman of the Scott Trust (1989-2003), owners of Guardian Media Group plc Nothing he wrote was for effect, or advantage, or calculation or influence. He didn’t write to please editors, or proprietors or politicians or mandarins – or even readers. He simply wrote what he believed. That this should have had such an effect among those whom he wrote about may suggest how rare and precious this gift was. Alan Rusbridger, Editor, The Guardian Guardian Media Group plc Annual Report and Accounts 2004 1 Introduction Guardian Media Group plc is a UK media 2 Guardian Media Group plc structure 3 Chairman's statement business with interests in national newspapers, 6 Guardian Media Group plc Board of directors 8 Chief Executive’s review of operations community newspapers, magazines, radio 12 The Scott Trust 14 Corporate social responsibility 18 Financial review and internet businesses. The company is 20 Corporate governance 24 Report of the directors wholly-owned by the Scott Trust. 27 Independent auditors’ report 28 Group profit and loss account 29 Group balance sheet 30 Company balance sheet 31 Group statement of total recognised gains and losses The Scott Trust was created in 1936 to 32 Group cash flow statement 33 Cash flow reconciliations secure the financial and editorial 34 Notes relating to the 2004 financial statements 55 Group five year review independence of the Guardian in perpetuity. 56 Financial advisers Financial highlights 2004 73.5 67.3 634.8 62.1 43.6 526.0 456.4 47.4 36.9 439.0 437.4 29.4 29.8 9.8 1.6 2000 2001 2002 2003 2004 2000 2001 2002 2003 2004 2000 2001 2002 2003 2004 Turnover including share of Total group operating profit Profit before taxation. -

Commercial Realities Will Look Like in a Few Years Time

Responsible advertising Advertising policy The Guardian, Observer and Guardian Unlimited raise a substantial proportion of their income from advertising. Percentage of readers who Every effort is made to ensure the adverts we carry adhere to the rulings of the think we have a responsibility to refuse to carry the following types Advertising Standards Authority (ASA). Any advert that has had a complaint of advertising? upheld by the ASA will not run in our newspapers. COMMERCIAL Music with offensive lyrics 54% Before the advertising department takes any advert, it always checks (eg. homophobic or 44 the copy to ensure it doesn’t jar with our values — that it is legal, decent and racist material) 43 truthful. If it feels the copy is unsuitable, it asks for it to be amended. 39 That we received complaints about only 32 adverts, out of a total of more Gambling 36 than 15,000, shows that our system is working effectively. No single advert REALITIES 36 received more than 10 complaints. Readers usually focus their attention on adverts that offend a strongly 36 held but often not a widely shared belief. A recent example was an advert Religious 35 Priorities: to increase profitability by the following: 40 we carried for formula milk, which received two complaints. This subject is fraught with controversy and is also tightly regulated, and in this instance the 42 ad conformed to all the guidelines. In a case like this, we write to the reader 1) Continue to publish innovative and distinctive Advertising using sexual imagery 34 concerned and explain why we made the decision to carry the ad, and also why 34 we disagree with them, while respecting their right to a differing opinion. -

Guidelines the Guardian’S Editorial Code

Guidelines The Guardian’s Editorial Code February 2003 Guidelines The Guardian’s Editorial Code 1 Contents Contents 2 Summary 2 1: Professional practice 3 2: Personal behaviour and conflicts of interest 5 3: Appendices 8 3.1: The PCC Code of Conduct 8 3.2: CP Scott’s essay 11 3.3: Areas of interest and companies that GMG holds 13 Summary “A newspaper’s primary office is the gathering of news. At the peril of its soul it must see that the supply is not tainted.” The most important currency of the Guardian is trust. This is as true today as when CP Scott marked the centenary of the founding of the paper with his famous essay on journalism in 1921. The purpose of this code is, above all, to protect and foster the bond of trust between the paper and its readers, and therefore to protect the integrity of the paper and of the editorial content it carries. As a set of guidelines, this will not form part of a journalist’s contract of employment, nor will it form part, for either editorial management or journalists, of disciplinary, promotional or recruitment procedures. However, by observing the code, journalists working for the Guardian will be protecting not only the paper but also the independence, standing and reputation of themselves and their colleagues. It is important that freelances working for the Guardian also abide by these guidelines while on assignment for the paper. Press Complaints Commission Code of Conduct The Guardian — in common with most other papers in Britain — considers the PCC’s Code of Conduct to be a sound statement of ethical behaviour for journalists. -

CAPSTONE 19-4 Indo-Pacific Field Study

CAPSTONE 19-4 Indo-Pacific Field Study Subject Page Combatant Command ................................................ 3 New Zealand .............................................................. 53 India ........................................................................... 123 China .......................................................................... 189 National Security Strategy .......................................... 267 National Defense Strategy ......................................... 319 Charting a Course, Chapter 9 (Asia Pacific) .............. 333 1 This page intentionally blank 2 U.S. INDO-PACIFIC Command Subject Page Admiral Philip S. Davidson ....................................... 4 USINDOPACOM History .......................................... 7 USINDOPACOM AOR ............................................. 9 2019 Posture Statement .......................................... 11 3 Commander, U.S. Indo-Pacific Command Admiral Philip S. Davidson, U.S. Navy Photos Admiral Philip S. Davidson (Photo by File Photo) Adm. Phil Davidson is the 25th Commander of United States Indo-Pacific Command (USINDOPACOM), America’s oldest and largest military combatant command, based in Hawai’i. USINDOPACOM includes 380,000 Soldiers, Sailors, Marines, Airmen, Coast Guardsmen and Department of Defense civilians and is responsible for all U.S. military activities in the Indo-Pacific, covering 36 nations, 14 time zones, and more than 50 percent of the world’s population. Prior to becoming CDRUSINDOPACOM on May 30, 2018, he served as -

Codes Used in D&M

CODES USED IN D&M - MCPS A DISTRIBUTIONS D&M Code D&M Name Category Further details Source Type Code Source Type Name Z98 UK/Ireland Commercial International 2 20 South African (SAMRO) General & Broadcasting (TV only) International 3 Overseas 21 Australian (APRA) General & Broadcasting International 3 Overseas 36 USA (BMI) General & Broadcasting International 3 Overseas 38 USA (SESAC) Broadcasting International 3 Overseas 39 USA (ASCAP) General & Broadcasting International 3 Overseas 47 Japanese (JASRAC) General & Broadcasting International 3 Overseas 48 Israeli (ACUM) General & Broadcasting International 3 Overseas 048M Norway (NCB) International 3 Overseas 049M Algeria (ONDA) International 3 Overseas 58 Bulgarian (MUSICAUTOR) General & Broadcasting International 3 Overseas 62 Russian (RAO) General & Broadcasting International 3 Overseas 74 Austrian (AKM) General & Broadcasting International 3 Overseas 75 Belgian (SABAM) General & Broadcasting International 3 Overseas 79 Hungarian (ARTISJUS) General & Broadcasting International 3 Overseas 80 Danish (KODA) General & Broadcasting International 3 Overseas 81 Netherlands (BUMA) General & Broadcasting International 3 Overseas 83 Finnish (TEOSTO) General & Broadcasting International 3 Overseas 84 French (SACEM) General & Broadcasting International 3 Overseas 85 German (GEMA) General & Broadcasting International 3 Overseas 86 Hong Kong (CASH) General & Broadcasting International 3 Overseas 87 Italian (SIAE) General & Broadcasting International 3 Overseas 88 Mexican (SACM) General & Broadcasting -

Guardian Media Group Plc Annual Report and Accounts 2009 Securing the Long-Term Future of the Guardian GMG Annual Report 2009

Guardian Media Group plc Annual Report and Accounts 2009 Securing the long-term future of the Guardian GMG Annual Report 2009 Contents 01 Introduction 32 Corporate responsibility 02 Group structure 36 Financial review 03 Financial highlights 42 Corporate governance 04 Statement from the chair 47 Report of the directors 07 Chief executive’s review of operations 49 Directors’ remuneration report 08 Introduction 53 Independent auditors’ report 09 Guardian News & Media 54 Profit and loss account 12 GMG Regional Media 54 Statement of recognised income 15 GMG Radio and expense 17 GMG Property Services 55 Balance sheet 19 Trader Media Group 56 Cash flow statement 22 Emap 57 Notes relating to the financial statements 25 Outlook 87 Group five year review 26 Board of directors 89 Company financial statements of Guardian 28 Statement from the chair of the Scott Trust Media Group plc 30 The Scott Trust directors 99 Advisers GMG Annual Report 2009 Securing the long-term future of the Guardian Guardian Media Group (GMG) is one of the UK’s leading multimedia businesses. The diverse portfolio includes national and regional newspapers, websites, magazines, radio stations and business-to-business media. Our flagship is the Guardian newspaper and website. The Group is wholly owned by the Scott Trust, which exists to secure the ongoing editorial independence of the Guardian. Under this unique form of media ownership the Group is able to take a long-term view as it invests in the future and security of the Guardian’s independent, liberal journalism. www.gmgplc.co.uk -

The Guardian Subscription Offers

The Guardian Subscription Offers ReplaceableGeraldo bodies Andy unmistakably? allowances, Boundhis craquelure and internal turpentine Corky impedeslogged jeopardously. almost mercilessly, though Antin enfold his lepidopterist drabblings. What is Guardian Membership Membership The Guardian. And it is a strict strength of digital. Noseda and Kavakos71940 Kennedy Center. How many subscriptions will offer is guardian subscription offer available in. They care for guardian subscription offer and try another smaller size is stored in? Swedish newspaper content you enter into the font size of the additional resources to. We created Live and Discover to mortgage their needs within these moments. Data and subscriptions or password for those you offer has three tiers: in a subscription payment methods are highly valuable touchpoints with the idea what content? We all of space to reviews books to pay to laborie, the daily or agency, as your future. Possibly the guardian subscriptions or contribute articles tend to guardian was division in their clients already a digital earnings made after? You accept this offers choices and guardian subscription or not how long time without ads to copy it suits both ny. All stories presented in one panel felt congested. This has recently undergone a significant facelift. Guardian launches one-edition daily app exclusively for digital. The Bangkok Post El Norte Financial Times The Guardian Jerusalem Post. Congress for guardian subscriptions to offer certification programs and newspapers in accordance with location and greenslade. We use cookies to provide you with a better land on our websites. Paying for clothes and the Limits of Subscription Reuters. Within a violin you daily receive the message below. -

Local and Regional Media in the UK: Nations and Regions Case Studies Local and Regional Media in the UK: Annex 2

Local and regional media in the UK: Nations and Regions case studies Local and Regional Media in the UK: Annex 2 Annex Publication date: 22 September 2009 Contents Section Page 1 Local regional and nations media maps and tables 1 2 Case studies for the local and regional media landscape in England 17 3 The local, regional and nations media landscape in Wales 27 4 The local, regional and nations media landscape in Scotland 30 5 The local, regional and nations media landscape in Northern Ireland 34 Nations and Regions case studies Section 1 1 Local regional and nations media maps and tables Introduction 1.1 This annex to Local and Regional Media in the UK provides further detail to the discussion of the local and regional media in Section 3 of the main report. It examines the local, regional and nations media landscape in selected locations around the UK through a series of case studies conducted in spring 2009. We place these case studies within a wider context by the inclusion of maps and table showing the availability of different local media across the UK. 1.2 Given the heterogeneity and complexity of the local and regional media landscape across the UK it is not possible to carry out a detailed analysis of the local and regional media landscape in all locations throughout the UK. We have therefore based our approach around case studies in eight locations to present an indicative view as to the local media landscape in different parts of the UK. The locations were selected to provide a range of population sizes and included a location in each of the nations. -

Concerned Africa Scholars

Bulletin N°85 — Spring 2010 concernedafricascholars.org Concerned Africa Scholars US militarization of the Sahara-Sahel Security, Space & Imperialism ACAS Concerned Africa Scholars US militarization of the Sahara-Sahel: Security, Space & Imperialism Bulletin N°85 (Spring 2010) 1-11 Introduction: Securitizing the Sahara Jacob Mundy 12-29 From GSPC to AQIM: The evolution of an Algerian islamist terrorist group into an Al-Qa‘ida Affiliate and its implications for the Sahara-Sahel region Stephen Harmon 30-49 War on ‘terror’: Africom, the kleptocratic state and under-class militancy in West Africa-Nigeria Caroline Ifeka 51-62 Counterterrorism and democracy promotion in the Sahel under Presidents George W. Bush and Barack Obama from September 11, 2001, to the Nigerien Coup of February 2010 Alex Thurston 63-71 Western Sahara and the United States’ geographical imaginings Konstantina Isidoros 72-77 The Western Sahara conflict: regional and international repercussions Yahia H Zoubir 78-81 Sahelian blowback: what’s happening in Mali? Vijay Prashad 82-83 All quiet on the West Africa front: terrorism, tourism and poverty in Mauritania Anne E. McDougall 84-90 The origins of AFRICOM: the Obama administration, the Sahara-Sahel and US Militarization of Africa Stephen Chan, Daniel Volman & Jeremy Keenan The Association of Concerned African Scholars (ACAS) is a network of academics, analysts and activists. ACAS is engaged in critical research and analysis of Africa and U.S. government policy; developing communication and action net- works; and mobilizing concerned communities on critical, current issues related to Africa. ACAS is committed to interrogat- ing the methods and theoretical approaches that shape the study of Africa. -

Annual Report and Accounts 2000 Guardian Media Group Plc

Annual Report and Accounts 2000 Guardian Media Group plc Chief Executive’s Review continued Guardian Media Group plc is a UK media business with interests in national newspapers, regional and local newspapers, magazines, television and radio. The company is wholly-owned by the Scott Trust. The Scott Trust was created in 1936 to secure the financial and editorial independence of the Guardian in perpetuity. Financial Highlights of 1999/2000 Group sales (including joint ventures) of £444 million (up 8%) Group operating profit before exceptional items of £47 million (down 6%) Group profit before taxation of £74 million (down 8% before and up 8% after exceptional item) Group net funds of £176 million (up 28%) Group net assets of £285 million (up 21%) 1 Guardian Media Group plc Chairman’s Statement The Group has continued to sustain consolidation can seem to be a This annual report reflects, of course, the pattern of progress which has greater prize than independence. on a number of changes to our developed over the last few years. business in the last year. The Chief The Scott Trust, which owns GMG, Executive reports in more detail in On a total turnover of £444 million was created in a world markedly his review of operations. But an (up 8%), pre-tax profits increased different from the one which exists at unchanging aspect of the organisation from £68.2 million to £73.5 million. the beginning of the 21st Century. overall is the high professionalism Although operating profits fell from Yet its guiding principles not only and editorial integrity which typifies £46.1 million to £42.2 million, this continue to apply with the same the approach of the staff of GMG. -

Local Media Final Document

Response to the Secretary of State (Culture, Olympics, Media and Sport): Local Media – cross media ownership rules Publication date: 9 August 2010 1 Summary In November 2009, after public consultation, we reported to the Secretary of State (Culture, Media and Sport) on our review of the media ownership rules, as required by statute. One of our recommendations was to significantly liberalise the local cross media ownership rules. Government now intends to implement this liberalisation. Once this liberalisation is implemented the only prohibition on local cross media ownership will be that one person cannot own in a local radio coverage area: a local analogue radio licence; and a regional Channel 3 licence whose potential audience includes at least 50% of that radio station’s potential audience; and one or more local newspapers which have a local market share of 50% or more in the coverage area (“the Remaining Rule”). The Secretary of State (Culture, Olympics, Media and Sport) has now asked Ofcom to look at the feasibility and implications of removing the Remaining Rule. The Secretary of State is required by statute to consult with us before making any changes to the media ownership rules which Ofcom has not already recommended. In considering this request, we have updated our evidence for changes since our November 2009 recommendation. In summary, there are two relevant developments. Firstly, the evidence shows a significant deterioration in the revenues available for local / regional newspapers between 2008 and 2009, accompanied by continued structural pressure on television and radio as the internet increases its share in a total advertising market that has been under pressure from broader economic circumstances. -

Final Impact Assessment

Title: Impact Assessment (IA) Local TV: Implementing a new framework IA No: DCMS005 Lead department or agency: DCMS Date: 28/06/2011 Other departments or agencies: Stage: Final Ofcom, HMT, BBC Source of intervention: Domestic Type of measure: Secondary legislation Contact for enquiries: Ruth John - 020 7211 6977 [email protected] Summary: Intervention and Options What is the problem under consideration? Why is government intervention necessary? Research (see para 34) shows high demand from audiences for local news and content, some of which is available through newspapers, radio and online. However, the UK market has been unable to support sustainable commercially viable local TV, as it is hampered by market barriers with limited regulatory incentives. Despite television being the media platform with the greatest household use, these barriers limit commercial opportunities for local TV to develop. Government can incentivise the market and encourage growth by tackling the barriers to entry and creating a framework for local TV services to emerge that will bring wider economic, social, cultural and democratic benefits. Local TV will have a vital role to play in the localism agenda, in holding local institutions to account and increasing civic engagement at a local level. What are the policy objectives and the intended effects? In line with the Coalition Agreement, Government is committed to enabling local TV to emerge in the UK. The Government will create a regulatory framework to enable and support commercially sustainable local TV as part of the wider growth agenda. This will not be an imposition on existing broadcasters or create new regulatory burdens.