Route 9A Promenade Project J

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

State of New York Court of Appeals

State of New York OPINION Court of Appeals This opinion is uncorrected and subject to revision before publication in the New York Reports. No. 50 John Kuzmich, et al., Appellants, v. 50 Murray Street Acquisition LLC, Respondent. -------------------------------------------- No. 51 William T. West, et al., Appellants, v. B.C.R.E. - 90 West Street, LLC, Respondent, Lee Rosen, Defendant. Case No. 50: Robert S. Smith, for appellants. James M. McGuire, for respondent. Metropolitan Council on Housing; The Real Estate Board of New York, amici curiae. Case No. 51: Robert S. Smith, for appellants. Magda L. Cruz, for respondent. STEIN, J.: The question presented on these appeals is whether plaintiffs’ apartments, which are located in buildings receiving tax benefits pursuant to Real Property Tax Law (RPTL) § 421-g, are subject to the luxury deregulation provisions of the Rent Stabilization Law - 1 - - 2 - Nos. 50, 51 (RSL) (see generally Rent Stabilization Law of 1969 [Administrative Code of City of New York § 26-504.1]). We conclude that they are not and, therefore, reverse. I In each of these cases, plaintiffs are individual tenants of rented apartments located in lower Manhattan, which are owned by defendants, 50 Murray Street Acquisition LLC or B.C.R.E. – 90 West Street, LLC.1 Defendants have received certain tax benefits pursuant to section 421-g of the RPTL in connection with the conversion of their buildings from office space to residential use. In these actions, plaintiffs seek, among other things, a declaration that their apartments are subject to rent stabilization. Plaintiffs allege that defendants failed to treat the apartments as rent stabilized even though the receipt of benefits under RPTL 421-g is expressly conditioned upon the regulation of rents in the subject buildings. -

Aroundmanhattan

Trump SoHo Hotel South Cove Statue of Liberty 3rd Avenue Peter J. Sharp Boat House Riverbank State Park Chelsea Piers One Madison Park Four Freedoms Park Eastwood Time Warner Center Butler Rogers Baskett Handel Architects and Mary Miss, Stanton Eckstut, F A Bartholdi, Richard M Hunt, 8 Spruce Street Rotation Bridge Robert A.M. Stern & Dattner Architects and 1 14 27 40 53 66 Cetra Ruddy 79 Louis Kahn 92 Sert, Jackson, & Assocs. 105 118 131 144 Skidmore, Owings & Merrill Marner Architecture Rockwell Group Susan Child Gustave Eiffel Frank Gehry Thomas C. Clark Armand LeGardeur Abel Bainnson Butz 23 East 22nd Street Roosevelt Island 510 Main St. Columbus Circle Warren & Wetmore 246 Spring Street Battery Park City Liberty Island 135th St Bronx to E 129th 555 W 218th Street Hudson River -137th to 145 Sts 100 Eleventh Avenue Zucotti Park/ Battery Park & East River Waterfront Queens West / NY Presbyterian Hospital Gould Memorial Library & IRT Powerhouse (Con Ed) Travelers Group Waterside 2009 Addition: Pei Cobb Freed Park Avenue Bridge West Harlem Piers Park Jean Nouvel with Occupy Wall St Castle Clinton SHoP Architects, Ken Smith Hunters Point South Hall of Fame McKim Mead & White 2 15 Kohn Pedersen Fox 28 41 54 67 Davis, Brody & Assocs. 80 93 and Ballinger 106 Albert Pancoast Boiler 119 132 Barbara Wilks, Archipelago 145 Beyer Blinder Belle Cooper, Robertson & Partners Battery Park Battery Maritime Building to Pelli, Arquitectonica, SHoP, McKim, Mead, & White W 58th - 59th St 388 Greenwich Street FDR Drive between East 25th & 525 E. 68th Street connects Bronx to Park Ave W127th St & the Hudson River 100 11th Avenue Rutgers Slip 30th Streets Gantry Plaza Park Bronx Community College on Eleventh Avenue IAC Headquarters Holland Tunnel World Trade Center Site Whitehall Building Hospital for Riverbend Houses Brooklyn Bridge Park Citicorp Building Queens River House Kingsbridge Veterans Grant’s Tomb Hearst Tower Frank Gehry, Adamson Ventilation Towers Daniel Libeskind, Norman Foster, Henry Hardenbergh and Special Surgery Davis, Brody & Assocs. -

Route 9A Promenade Project PROJECT UPDATE World Financial Center

Route 9A Promenade Project PROJECT UPDATE World Financial Center World Trade Center Site Presentation to the WTC Committee of CB#1 December 13, 2010 NEW YORK STATE STATE OF NEW YORK DEPARTMENT OF TRANSPORTATION David A. Paterson Stanley Gee Phillip Eng, P.E. Marie A. Corrado, Esq. Joseph T. Brown, P.E. Governor Acting Commissioner Regional Director Director, Major Projects Project Director, 9A 1 Presentation Outline . Route 9A at the World Trade Center Site . NYSDOT Pending Work adjacent to the WTC & WFC Site - Cedar to Vesey Street Eastside Frontage - Memorial Access & Egress on Route 9A on 9/11/2011 - Pedestrian Bridges (West Thames & Vesey Street) - WTC Project Impact Zones - Traffic Shifts for WTC Projects . Current Route 9A and WTC Site Schedule . The Two Components of the Route 9A Promenade Project . World Financial Center Frontage . NYSDOT Completed Work South of Liberty Street - South Promenade - West Thames Park - Temporary Liberty Street Pedestrian Bridge Extension - 90 West Street Frontage . NYSDOT Completed Work North of Vesey Street . NYSDOT Pending Work North & South of WTC Site . Route 9A Promenade Project Status NEW YORK STATE DEPARTMENT OF TRANSPORTATION 2 12/13/2010 Route 9A at the World Trade Center Site Aerial Photo 1 WFC 2 WFC 3 WFC GOLDMAN SACHS ROUTE 9A SB ROUTE 9A NB VSC NATIONAL SEPTEMBER 11 MEMORIAL & MUSEUM VERIZON 1 WTC NEW YORK STATE DEPARTMENT OF TRANSPORTATION 3 12/13/2010 Route 9A at the World Trade Center Site Pending Route 9A Curblines with Permanent & Temporary Pavement 1 WFC 2 WFC 3 WFC GOLDMAN ROUTE 9A SB SACHS ROUTE 9A NB 90 WEST ST. -

TM 3.1 Inventory of Affected Businesses

N E W Y O R K M E T R O P O L I T A N T R A N S P O R T A T I O N C O U N C I L D E M O G R A P H I C A N D S O C I O E C O N O M I C F O R E C A S T I N G POST SEPTEMBER 11TH IMPACTS T E C H N I C A L M E M O R A N D U M NO. 3.1 INVENTORY OF AFFECTED BUSINESSES: THEIR CHARACTERISTICS AND AFTERMATH This study is funded by a matching grant from the Federal Highway Administration, under NYSDOT PIN PT 1949911. PRIME CONSULTANT: URBANOMICS 115 5TH AVENUE 3RD FLOOR NEW YORK, NEW YORK 10003 The preparation of this report was financed in part through funds from the Federal Highway Administration and FTA. This document is disseminated under the sponsorship of the U.S. Department of Transportation in the interest of information exchange. The contents of this report reflect the views of the author who is responsible for the facts and the accuracy of the data presented herein. The contents do no necessarily reflect the official views or policies of the Federal Highway Administration, FTA, nor of the New York Metropolitan Transportation Council. This report does not constitute a standard, specification or regulation. T E C H N I C A L M E M O R A N D U M NO. -

Survey of Rent Stabilized Apartment Units in Lower Manhattan

Survey of Rent Stabilized Apartment Units in Lower Manhattan Prepared by Manhattan Community Board 1 January 21, 2015 Contents Executive Summary ................................................................................................. 2 Background of Survey ............................................................................................. 3 Why Care About Rent Stabilized Apartments? .................................................... 3 What Tenants Should Know About Rent Stabilized Apartments ........................ 4 What Should I Know Before Signing a Lease? .................................................... 5 Deregulation Due to Tenant Income Level or Vacancy ....................................... 5 List of Rent Stabilized Units in Lower Manhattan .................................................. 6 Map with Locations of Stabilized Units .................................................................. 9 Acknowledgments .................................................................................................. 10 1 Executive Summary This report is intended as a resource for anyone seeking a rent stabilized apartment in the district. It is also intended to serve as a brief primer about rent stabilization. We hope that it will help tenants take advantage of opportunities to move into regulated apartments. By making this information available, CB1 seeks to encourage a stable population of long-term residents. Community Board 1 (CB1) enjoys considerable affordable and rent stabilized housing. Nevertheless, -

Skyscrapers and District Heating, an Inter-Related History 1876-1933

Skyscrapers and District Heating, an inter-related History 1876-1933. Introduction: The aim of this article is to examine the relationship between a new urban and architectural form, the skyscraper, and an equally new urban infrastructure, district heating, both of witch were born in the north-east United States during the late nineteenth century and then developed in tandem through the 1920s and 1930s. These developments will then be compared with those in Europe, where the context was comparatively conservative as regards such innovations, which virtually never occurred together there. I will argue that, the finest example in Europe of skyscrapers and district heating planned together, at Villeurbanne near Lyons, is shown to be the direct consequence of American influence. Whilst central heating had appeared in the United Kingdom in the late eighteenth and the early nineteenth centuries, district heating, which developed the same concept at an urban scale, was realized in Lockport (on the Erie Canal, in New York State) in the 1880s. In United States were born the two important scientists in the fields of heating and energy, Benjamin Franklin (1706-1790) and Benjamin Thompson Rumford (1753-1814). Standard radiators and boilers - heating surfaces which could be connected to central or district heating - were also first patented in the United States in the late 1850s.1 A district heating system produces energy in a boiler plant - steam or high-pressure hot water - with pumps delivering the heated fluid to distant buildings, sometimes a few kilometers away. Heat is therefore used just as in other urban networks, such as those for gas and electricity. -

Chapter 5. Historic Resources 5.1 Introduction

CHAPTER 5. HISTORIC RESOURCES 5.1 INTRODUCTION 5.1.1 CONTEXT Lower Manhattan is home to many of New York City’s most important historic resources and some of its finest architecture. It is the oldest and one of the most culturally rich sections of the city. Thus numerous buildings, street fixtures and other structures have been identified as historically significant. Officially recognized resources include National Historic Landmarks, other individual properties and historic districts listed on the State and National Registers of Historic Places, properties eligible for such listing, New York City Landmarks and Historic Districts, and properties pending such designation. National Historic Landmarks (NHL) are nationally significant historic places designated by the Secretary of the Interior because they possess exceptional value or quality in illustrating or interpreting the heritage of the United States. All NHLs are included on the National Register, which is the nation’s official list of historic properties worthy of preservation. Historic resources include both standing structures and archaeological resources. Historically, Lower Manhattan’s skyline was developed with the most technologically advanced buildings of the time. As skyscraper technology allowed taller buildings to be built, many pioneering buildings were erected in Lower Manhattan, several of which were intended to be— and were—the tallest building in the world, such as the Woolworth Building. These modern skyscrapers were often constructed alongside older low buildings. By the mid 20th-century, the Lower Manhattan skyline was a mix of historic and modern, low and hi-rise structures, demonstrating the evolution of building technology, as well as New York City’s changing and growing streetscapes. -

Bfm:978-1-56898-652-4/1.Pdf

Manhattan Skyscrapers Manhattan Skyscrapers REVISED AND EXPANDED EDITION Eric P. Nash PHOTOGRAPHS BY Norman McGrath INTRODUCTION BY Carol Willis PRINCETON ARCHITECTURAL PRESS NEW YORK PUBLISHED BY Princeton Architectural Press 37 East 7th Street New York, NY 10003 For a free catalog of books, call 1.800.722.6657 Visit our website at www.papress.com © 2005 Princeton Architectural Press All rights reserved Printed and bound in China 08 07 06 05 4 3 2 1 No part of this book may be used or reproduced in any manner without written permission from the publisher, except in the context of reviews. The publisher gratefully acknowledges all of the individuals and organizations that provided photographs for this publi- cation. Every effort has been made to contact the owners of copyright for the photographs herein. Any omissions will be corrected in subsequent printings. FIRST EDITION DESIGNER: Sara E. Stemen PROJECT EDITOR: Beth Harrison PHOTO RESEARCHERS: Eugenia Bell and Beth Harrison REVISED AND UPDATED EDITION PROJECT EDITOR: Clare Jacobson ASSISTANTS: John McGill, Lauren Nelson, and Dorothy Ball SPECIAL THANKS TO: Nettie Aljian, Nicola Bednarek, Janet Behning, Penny (Yuen Pik) Chu, Russell Fernandez, Jan Haux, Clare Jacobson, John King, Mark Lamster, Nancy Eklund Later, Linda Lee, Katharine Myers, Jane Sheinman, Scott Tennent, Jennifer Thompson, Paul G. Wagner, Joe Weston, and Deb Wood of Princeton Architectural Press —Kevin Lippert, Publisher LIBRARY OF CONGRESS CATALOGING-IN-PUBLICATION DATA Nash, Eric Peter. Manhattan skyscrapers / Eric P. Nash ; photographs by Norman McGrath ; introduction by Carol Willis.—Rev. and expanded ed. p. cm. Includes bibliographical references. ISBN 1-56898-545-2 (alk. -

Principles and Revised Preliminary Blueprint for the Future of Lower Manhattan

Lower Manhattan Development Corporation 1 Liberty Plaza, 20th Floor New York, NY 10006 Phone: (212) 962-2300 Fax: (212) 962-2431 PRINCIPLES AND REVISED PRELIMINARY BLUEPRINT FOR THE FUTURE OF LOWER MANHATTAN When New York City was attacked on September 11, 2001, the United States and the democratic ideals upon which it was founded were also attacked. The physical damage New York City sustained was devastating and the human toll was immeasurable. But New York does not bear the loss alone. In the aftermath of September 11, the entire nation has embraced New York, and we have responded by vowing to rebuild our City – not as it was, but better than it was before. Although we can never replace what was lost, we must remember those who perished, rebuild what was destroyed, and renew Lower Manhattan as a symbol of our nation’s resilience. This is the mission of the Lower Manhattan Development Corporation. The LMDC, a subsidiary of Empire State Development, was formed by the Governor and Mayor as a joint State-City Corporation to oversee the revitalization of Lower Manhattan south of Houston Street. LMDC works in cooperation with the Port Authority and all stakeholders to coordinate long-term planning for Lower Manhattan while concurrently pursuing initiatives to improve the quality of life. The task before us is immense. Our most important priority is to create a permanent memorial on the World Trade Center site that appropriately honors those who were lost, while reaffirming the democratic ideals that came under attack on September 11. Millions of people will journey to Lower Manhattan each year to visit what will be a world-class memorial in an area steeped in historical significance and filled with cultural treasures – including the Statute of Liberty and Ellis Island. -

Crown of Gold: Roof Gleams Anew Atop N.Y. Landmark

Durability + Design - Crown of Gold: Roof Gleams Anew Atop N.Y. Landmark The Journal of Architectural Coatings A Product of Technology Publishing JPCL/PaintSquare | D+D | PWC | Paint BidTracker Crown of Gold: Roof Gleams Anew Atop N.Y. Landmark From D+D, September 2010 By Joe Maty Editor, Durability + Design New York Life Insurance Company has successfully built an indelible brand identity by calling itself “The Company You Keep.” Perhaps equally firmly etched into public consciousness of the venerable Empire State-based concern is its landmark headquarters building on Madison Avenue, a Gothic- revival, Indiana limestone edifice designed in 1926 by the legendary Cass Gilbert. The towering structure has loomed large in the company’s media imagery for many years. No doubt it’s the building the company will keep, considering its intimate connection with the corporate identity. Recently, the company also demonstrated that the building’s roof it is surely determined to keep—intact in all its gold-gilt glory, a gem glittering amid Gotham’s steel, stone, and concrete canyons. New York Life summoned The Gilders’ Studio Inc., based in Olney, Md., to formulate and execute a restoration and regilding program for the pyramidal, lantern-topped roof, composed of 25,000 gilded tiles. The job entailed an in- depth evaluation of materials and methods to return the roof and lantern to their former, glittering appearance. The company also serves as construction manager for the project. The upper section of the building, showing the gilded roof following restoration Michael Kramer, president of The Gilders Studio, said the roof is the largest exterior gold-leaf structure in the Photos courtesy of The Gilders’ Studio. -

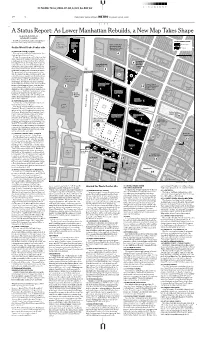

As Lower Manhattan Rebuilds, a New Map Takes Shape

ID NAME: Nxxx,2004-07-04,A,024,Bs-BW,E2 3 7 15 25 50 75 85 93 97 24 Ø N THE NEW YORK TIMES METRO SUNDAY, JULY 4, 2004 CITY A Status Report: As Lower Manhattan Rebuilds, a New Map Takes Shape By DAVID W. DUNLAP and GLENN COLLINS Below are projects in and around ground DEVELOPMENT PLAN zero and where they stood as of Friday. Embassy Goldman Suites Hotel/ Sachs Bank of New York BUILDINGS UA Battery Park Building Technology and On the World Trade Center site City theater site 125 Operations Center PARKS GREENWICH ST. 75 Park Place Barclay St. 101 Barclay St. (A) FREEDOM TOWER / TOWER 1 2 MURRAY ST. Former site of 6 World Trade Center, the 6 United States Custom House 0Feet 200 Today, the cornerstone will be laid for this WEST BROADWAY skyscraper, with about 60,000 square feet of retail space at its base, followed by 2.6 mil- Fiterman Hall, lion square feet of office space on 70 stories, 9 Borough of topped by three stories including an obser- Verizon Building Manhattan PARK PL. vation deck and restaurants. Above the en- 4 World 140 West St. Community College closed portion will be an open-air structure Financial 3 5 with wind turbines and television antennas. Center 7 World The governor’s office is a prospective ten- VESEY ST. BRIDGE Trade Center 100 Church St. ant. Occupancy is expected in late 2008. The WASHINGTON ST. 7 cost of the tower, apart from the infrastruc- 3 World 8 BARCLAY ST. ture below, is estimated at $1 billion to $1.3 Financial Center billion. -

The Exterior Restoration of 90 West Street

THE EXTERIOR RESTORATION OF 90 WEST STREET, NYC RICHARD W. LEFEVER, PE, AND MARK ANDERSON, AIA FAÇADE MAINTENANCE DESIGN, PC, NEW YORK, NY B UILDING E NVELOPE T ECHNOLOGY S YMPOSIUM • O CTOBER 2 0 0 6 L EFEVER AND A NDERSON • 2 9 ABSTRACT 90 West Street is a New York City landmark whose very survival was in doubt after heavy damage from the terrorist attack of September 11, 2001. Located at the south end of the World Trade Center site, this early skyscraper, designed in 1907 by Cass Gilbert, lay vacant for two years until a restoration effort described as “heroic” in size was undertaken by new owners who transformed the building into residential rental apartments. Façade Maintenance Design was the Professional of Record for the exterior restoration, which included the restoration of the copperclad mansard roof, terra cotta façade, granite base, and windows. FMD’s work began in the winter of 2003 and was completed in the fall of 2005. The project scope was reviewed by the National Park Service, the New York State Historic Preservation Office, and the New York City Landmarks Preservation Commission. SPEAKERS RICHARD W. LEFEVER, PE, AND MARK ANDERSON, AIA FAÇADE MAINTENANCE DESIGN, PC – NEW YORK, NY Rick Lefever and Mark Anderson together have over 35 years of experience in the design of exterior restoration projects. As founders of Façade Maintenance Design, an awardwin ning architectural and engineering firm based in New York City, they have performed design services throughout the eastern half of the U.S. 3 0 • L EFEVER AND A NDERSON B UILDING E NVELOPE T ECHNOLOGY S YMPOSIUM • O CTOBER 2 0 0 6 THE EXTERIOR RESTORATION OF 90 WEST STREET, NYC PROJECT SUMMARY terra cotta with polychrome terra cotta as it National Register of Historic Places while in The exterior of 90 West Street has been gets closer to the top, and then topped off a state of disrepair after the attacks of 9/11.