Procedure and Requirements for the Listing of New Companies on Oslo Stock Exchange's Main List, SMSB List, and the Primary Capital Certificates List

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Norway – United States

NORWAY – UNITED STATES Overview of requirements for listing shares on Oslo Børs vs NYSE Euronext / NASDAQ April 2014 Overview ∙ This presentation has been prepared with respect to listing of shares on the regulated markets operated by the Oslo Stock Exchange and NYSE Euronext and NASDAQ − In Norway: Oslo Børs and Oslo Axess − In the United States (US): New York Stock Exchange Euronext (NYSE) and NASDAQ Stock Market (NASDAQ) ∙ This presentation has been prepared by Advokatfirmaet Selmer DA for matters pertaining to Norwegian law and by Akin Gump Straus Hauer & Feld LLP for matters pertaining to US law, based on their experience for Norway and US transactions respectively, to provide an overview with respect to certain listing requirements and obligations in relation to listing on Oslo Børs / Oslo Axess vs NYSE / Nasdaq ∙ This presentation comprises only general information on certain Norwegian and US regulations related to listing, and registration of securities, and the continuing obligations of companies listed on Oslo Børs / Oslo Axess and NYSE / Nasdaq, and is not a complete nor exhaustive description of such obligations or other matters that could impact the regulations or application of such regulations. This presentation is prepared for information purposes only as of the date hereof, and shall not be considered nor construed as legal advice in any respect. No liability or responsibility are accepted as a result of this presentation 2 Main features for listing in Norway and the US 03 Listing in Norway 05 Listing in the US 10 Listing comparisons - fees and continuing obligations 16 Prospectus and registration requirements 20 American Depository Receipts, FPIs and EGCs 24 Contact persons 31 Main features for listing in Norway vs US Norway United States Time listing process Formal listing process takes minimum 8 weeks (fast Varies. -

Base Prospectus Dated 21 November 2019

BASE PROSPECTUS DATED 21 NOVEMBER 2019 Heimstaden Bostad AB (publ) (incorporated with limited liability in Sweden) €4,000,000,000 Euro Medium Term Note Programme Under this €4,000,000,000 Euro Medium Term Note Programme (the "Programme"), Heimstaden Bostad AB (publ) (the "Issuer") may from time to time issue notes (the "Notes") denominated in any currency agreed between the Issuer and the relevant Dealers (as defined below). Notes may be issued in bearer or registered form (respectively "Bearer Notes" and "Registered Notes") or in uncertificated book entry form ("VPS Notes") settled through the Norwegian Central Securities Depositary, Verdipapirsentralen ASA (the "VPS"). The maximum aggregate nominal amount of all Notes from time to time outstanding under the Programme will not exceed €4,000,000,000 (or its equivalent in other currencies calculated as described in the Programme Agreement described herein), subject to increase as described herein. The Notes may be issued on a continuing basis to one or more of the Dealers specified under "Overview of the Programme" and any additional Dealer appointed under the Programme from time to time by the Issuer (each a "Dealer" and together the "Dealers"), which appointment may be for a specific issue or on an ongoing basis. References in this Base Prospectus to the "relevant Dealer" shall, in the case of an issue of Notes being (or intended to be) subscribed by more than one Dealer, be to all Dealers agreeing to subscribe such Notes. An investment in Notes issued under the Programme involves certain risks. For a discussion of these risks see "Risk Factors". -

Msci Index Calculation Methodology

INDEX METHODOLOGY MSCI INDEX CALCULATION METHODOLOGY Index Calculation Methodology for the MSCI Equity Indexes Esquivel, Carlos July 2018 JULY 2018 MSCI INDEX CALCULATION METHODOLOGY | JULY 2018 CONTENTS Introduction ....................................................................................... 4 MSCI Equity Indexes........................................................................... 5 1 MSCI Price Index Methodology ................................................... 6 1.1 Price Index Level ....................................................................................... 6 1.2 Price Index Level (Alternative Calculation Formula – Contribution Method) ............................................................................................................ 10 1.3 Next Day Initial Security Weight ............................................................ 15 1.4 Closing Index Market Capitalization Today USD (Unadjusted Market Cap Today USD) ........................................................................................................ 16 1.5 Security Index Of Price In Local .............................................................. 17 1.6 Note on Index Calculation In Local Currency ......................................... 19 1.7 Conversion of Indexes Into Another Currency ....................................... 19 2 MSCI Daily Total Return (DTR) Index Methodology ................... 21 2.1 Calculation Methodology ....................................................................... 21 2.2 Reinvestment -

Bermuda to Oslo (And Beyond?): Still an Attractive Route to Growth by Guy Cooper, Conyers Dill & Pearman

Bermuda to Oslo (and beyond?): still an attractive route to growth By Guy Cooper, Conyers Dill & Pearman T he last five years have seen Shipping industry participants Potential investors are more incorporated – second only to several shipping and ship- choose to incorporate in likely to show interest in an Norwegian companies. The ping-related companies incor- Bermuda because investors are equity offering where there is most recent examples of porate in Bermuda and go on to comfortable with the island’s some immediate liquidity for Bermuda companies listing on list on the Oslo Stock reputation as one of the world’s their investment. Norway, the N-OTC are GoodBulk in Exchange. A key step along the premier offshore jurisdictions where shipping is in the April 2017 and 2020 Bulkers in route for a number of them has and an established international country’s DNA, is the obvious December 2017. been the use of the Norwegian finance centre. Bermuda offers place to turn to raise funds over-the-counter market as a a tax-neutral, business-friendly quickly. One option is a private Oslo listing fast-track way to access fresh environment, with a robust placement of shares to Many companies have used the capital. Avance Gas, Flex LNG, regulatory framework that investors, whilst simultaneously N-OTC as a stepping stone to a and Borr Drilling all took this full listing on the Oslo Stock route prior to an Oslo listing, Shipping industry participants choose Exchange or elsewhere. Over whilst GoodBulk and 2020 the past five years, several Bulkers listed on Norway’s to incorporate in Bermuda because Bermuda companies have OTC just last year, highlighting investors are comfortable with the island’s followed this route, including the enduring appeal of the reputation as one of the world’s premier Avance Gas in 2014, Flex LNG O c Bermuda-Oslo nexus. -

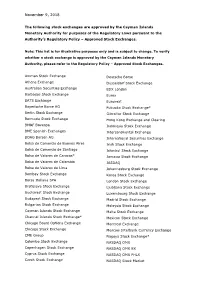

The List of Approved Stock Exchanges

November 9, 2018 The following stock exchanges are approved by the Cayman Islands Monetary Authority for purposes of the Regulatory Laws pursuant to the Authority’s Regulatory Policy – Approved Stock Exchanges. Note: This list is for illustrative purposes only and is subject to change. To verify whether a stock exchange is approved by the Cayman Islands Monetary Authority, please refer to the Regulatory Policy – Approved Stock Exchanges. Amman Stock Exchange Deutsche Borse Athens Exchange Dusseldorf Stock Exchange Australian Securities Exchange EDX London Barbados Stock Exchange Eurex BATS Exchange Euronext Bayerische Borse AG Fukuoka Stock Exchange* Berlin Stock Exchange Gibraltar Stock Exchange Bermuda Stock Exchange Hong Kong Exchange and Clearing BM&F Bovespa Indonesia Stock Exchange BME Spanish Exchanges Intercontinental Exchange BOAG Borsen AG International Securities Exchange Bolsa de Comercio de Buenos Aires Irish Stock Exchange Bolsa de Comercio de Santiago Istanbul Stock Exchange Bolsa de Valores de Caracas* Jamaica Stock Exchange Bolsa de Valores de Colombia JASDAQ Bolsa de Valores de Lima Johannesburg Stock Exchange Bombay Stock Exchange Korea Stock Exchange Borsa Italiana SPA London Stock Exchange Bratislava Stock Exchange Ljubljana Stock Exchange Bucharest Stock Exchange Luxembourg Stock Exchange Budapest Stock Exchange Madrid Stock Exchange Bulgarian Stock Exchange Malaysia Stock Exchange Cayman Islands Stock Exchange Malta Stock Exchange Channel Islands Stock Exchange* Mexican Stock Exchange Chicago Board Options Exchange -

World Markets 5

MARKET5 final 2019_Layout 1 2/15/19 5:19 PM Page 25 Lisette WORLD Van Doorn Ruchir “Sentiment is more negative on cities fac- Sharma's ing geopolitical risks” Markets Top 10 Economic Financial Markets Insights Trends To Watch p.02 Out For in 2019 Distributed Freely Monthly Edition ⎥ Volume II ⎥ Issue 05 ⎥ January 2019 P. 07 John Bogle East & SE Europe Equities The life and legacy of Vanguard’s Monthly performance reports and Analysts give their 2019 outlook on FUNDS founder p.06 statistics from the region p.02 world markets p.03 SEE STOCK EXCHANGES FORECAST GREAT TRADERS David Alan Tepper A specialist in distressed debt investing David A.Tepper was born on 11 Sep- Bond Funds. He also worked in the treasury tember 1957 in Pittsburgh, Pennsylva- department of Republic Steel. In 1985 Tepper nia, USA. He is the founder and was recruited by Goldman Sachs as a Credit D president of the wildly successful hedge Analyst. His primary focus was bankruptcies “The point is, fund Appaloosa Management which is based and special situations at the firm. Within six in Miami Beach, Florida and now manages months he became its head trader, remaining markets adapt, $15 billion. Tepper earned a Bachelor of Arts at Goldman till December 1992. He founded people adapt. with honors in economics from the University Appaloosa Management in early 1993. A 2010 Don’t listen to of Pittsburgh in 1978 and an M.B.A. from profile in New York Magazine described him Carnegie Mellon University in 1982. During as the object of “a certain amount of hero wor- all the crap college, he began small scale investing in var- ship inside the industry.” Forbes listed him as out there.” ious markets. -

RAFI™ Global Equity Universe: Methodology

This Version: March, 2021 RAFI™ Global Equity Universe: Methodology Introduction The RAFI Global Equity Investable Universe (GEIU) is the starting point for all index strategies available through RAFI Indices. These include RAFI Fundamental Index Series, RAFI Multi- Factor Index Series, RAFI ESG Index Series, and RAFI Diversity & Governance Index Series. Data Source The data source for the GEIU is derived from Bloomberg Back Office. Eligible Exchanges and Equity Security Types The eligible exchanges for developed and emerging markets are shown in Appendix A: Eligible Exchanges. Eligible securities consist of all common equity securities traded on primary eligible exchanges, and preferred shares in countries where preferred shares are economically equivalent to common, issued by companies that are assigned to countries classified by RAFI as developed and emerging markets. Table 1 DEVELOPED MARKETS* EMERGING MARKETS* Americas Europe Asia Latin America EMEA Asia Canada Austria Australia Brazil Czech Rep China United States Belgium Hong Kong Chile Egypt India Denmark Japan Colombia Greece Indonesia Finland New Zealand Mexico Hungary South Korea France Singapore Peru Kuwait Malaysia Germany Poland Philippines Ireland Qatar Taiwan Israel Russia Thailand Italy Saudi Arabia Netherlands South Africa Norway Turkey Portugal UAE Spain Sweden Switzerland United Kingdom *As of March 2021, there are 23 developed market countries and 25 emerging market countries eligible for inclusion. This Version: March, 2021 Country Assignment RAFI assigns companies to countries and promulgates that assignment to securities. The country assignments are based on country of primary listing, domicile, and incorporation. When these factors conflict, additional factors are considered. Eligible Investible Equity Securities Securities and companies are eligible to be included in the GEIU by meeting certain criteria defined below: 1. -

The Nordic Ceos for a Sustainable Future, the Norwegian Finance Ministry, and the Oslo Stock Exchange Declare Support for the TCFD Recommendations

The Nordic CEOs for a Sustainable Future, the Norwegian Finance Ministry, and the Oslo Stock Exchange Declare Support for the TCFD Recommendations 21 May 2021 The joint stance behind the Task Force on Climate-related Financial Disclosures (TCFD) comes as the Nordic CEOs for a Sustainable Future release a guide to help other Nordic companies begin the process of implementing the TCFD recommendations. May 21, 2021 – Today, the Norwegian Finance Ministry, the Nordic CEOs for a Sustainable Future, and the Oslo Stock Exchange declared their support for the recommendations of the Task Force on Climate- related Financial Disclosures (TCFD), demonstrating a commitment to building a more resilient financial system and safeguarding against climate risk through better disclosures. Norway joins other Nordic countries – Sweden and Denmark – in its support of the TCFD, bringing the total number of national governments endorsing the Task Force’s work to 12. To help boost further TCFD support across Nordic countries, the Nordic CEOs for a Sustainable Future developed a guide – “Climate Risk Management, a Guide to Getting Started” – based on their own experiences on how to get started with implementing the TCFD recommendations. The Nordic CEOs for a Sustainable Future was created in 2018 to inspire joint leadership and action towards delivery of the UN Sustainable Development Goals (SDGs). Companies represented in the group include Equinor, Marel, Swedbank, Storebrand Group, GSMA, Íslandsbanki, Finnair, Telia Company, Posten Norge, SAS, Schibsted, Telenor Group and Yara International. Many of the group’s members already report aligned with the TCFD recommendations, and those who are not already reporting, commit to doing so starting from the reporting year 2021. -

Asetek A/S Applies for Listing on the Oslo Stock Exchange

Asetek A/S applies for listing on the Oslo Stock Exchange NOT FOR DISTRIBUTION OR RELEASE, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES, CANADA, AUSTRALIA, HONG KONG OR JAPAN OR ANY OTHER JURISDICTION IN WHICH THE DISTRIBUTION OR RELEASE WOULD BE UNLAWFUL PLEASE SEE THE IMPORTANT NOTICE AT THE END OF THIS STOCK EXCHANGE NOTICE Bronderslev, 31 January 2013 - Asetek A/S ("Asetek or the "Company") announces today that they have sent an application for listing on the Oslo Stock Exchange, alternatively Oslo Axess. The application for listing is expected to be considered at the Oslo Stock Exchange board meeting to be held on or about 27 February 2013. Asetek is the leading provider of energy-efficient liquid cooling systems for data centers, servers, workstations, gaming and high performance PCs. The Company's products are used for reducing power and greenhouse gas emissions, lowering acoustic noise, and achieving maximum performance by leading OEMs and channel partners around the globe. Asetek's products are based upon the Company's patented all-in-one liquid cooling technology, with more than 1.3 million liquid cooling units sold and deployed in the field. In connection with the contemplated listing, Asetek intends to raise new equity capital in order to accelerate the Company's growth within its data center business segment. The global shift towards cloud computing and increasing demand for data centers has opened up a significant market opportunity with a large unmet need for energy efficient liquid cooling solutions. The data center market is growing fast, and currently approximately one percent of the total global electricity consumption is spent on cooling data centers. -

EMAS Offshore Limited – Delisting of Shares from the Oslo Stock Exchange

EMAS Offshore Limited – Delisting of shares from the Oslo Stock Exchange 1. Introduction The matter relates to whether the shares of EMAS Offshore Limited (“EMAS” or the “Company”, and together with its consolidated subsidiaries, the “EMAS Group”) are no longer suitable for listing on the Oslo Stock Exchange. The Company published the audited annual report for the financial year 2016 and the half-yearly report for the first six months of 2017, cf. section 5-5 and 5-6 the Norwegian Securities Trading Act (the “STA”), with significant delay. In addition, the Company has not published the audited annual report for 2017 within the deadline of 31 December 2017. The question is whether this entails that the Company’s shares are not suitable for listing and accordingly shall be delisted from trading, cf. section 15.1 of the Continuing obligations of stock exchange listed companies (the “Continuing Obligations”), cf. section 25 (1) of the Stock Exchange Act. Under section 3 below, the Exchange will give an account of the factual circumstances of the case. The legal background for the assessment of the Company’s suitability for listing is set out under section 4. The Company’s account of the case is provided under section 5. Under section 6, the Exchange will provide its assessment of the case. 2. About the Company The Company was listed on the Oslo Stock Exchange on 3 October 2007 with the name EOC Limited and changed its name to EMAS Offshore Limited on 15 September 2014. The Company completed a dual listing on the Singapore Stock Exchange (the “SGX”) in October 2014. -

Market Infrastructures and Market

Market infrastructures and market integrity: A post-crisis journey and a vision for the future Market infrastructures and market integrity: A post-crisis journey and a vision for the future Copyright 2018 Oliver Wyman and World Federation of Exchanges 1 CONTENTS 1 2 THE EVOLVING SUPERVISORY ROLE OF MARKET INTRODUCTION AND INFRASTRUCURE EXECUTIVE SUMMARY FIRMS page 2 page 9 3 TRENDS IN FINANCIAL MARKETS AND CHANGES TO THE BUSINESS ENVIRONMENT page 14 Copyright 2018 Oliver Wyman and World Federation of Exchanges 2 4 5 A VISION FOR THE FUTURE ROLE AND CAPABILITIES OF MARKET INFRASTRUCTURES IN ENSURING ROBUST CONCLUSION MARKET INTEGRITY AND APPENDIX page 28 page 38 Copyright 2018 Oliver Wyman and World Federation of Exchanges 3 1 INTRODUCTION Exchanges and clearinghouses / central counterparties (CCPs), (hereinafter referred to collectively as market infrastructures, or MIs), serve two main functions: 1. Fostering economic growth by enabling the efficient allocation of capital, including providing access to capital (for issuers) and providing avenues for investment and risk management (for investors) 2. Supporting market integrity by (amongst others) strengthening systemic stability, ensuring adherence to transparency obligations by listed companies, and adherence to rules by market participants, and investors Copyright 2018 Oliver Wyman and World Federation of Exchanges 2 The World Federation of Exchanges (WFE) and UNCTAD1 published a report focusing on the first objective in September 2017, titled The Role of Stock Exchanges in Fostering Economic Growth and Sustainable Development. This report focuses on the second purpose – the role of MIs in supporting market integrity. Market integrity is a cornerstone of fair and efficient markets, ensuring that participants enjoy equal access to markets, that price discovery and trading practices are fair, and that high standards of corporate governance are met. -

The Problem with European Stock Markets

THE PROBLEM WITH EUROPEAN STOCK MARKETS Analysis of the fragmented stock exchange landscape in Europe, how it is holding back growth in capital markets – and what we can do about it March 2021 by William Wright & Eivind Friis Hamre SUMMARY It is not new news that Europe has a complex patchwork of equity markets, stock exchanges and post-trade infrastructure, but this short paper paints this problem in particularly stark terms. The genesis of this paper came from two simple thought experiments: first, can we draw a diagram of the structure of European equity markets on one page? And second, what would the US stock market look like if every state has its own stock exchange? If you read nothing else in this report, please look at the map of the US market on page three and the diagram of European equity markets on page six. Here is a quick summary of this paper: > The elephant in the room The complex patchwork of European equity markets is a huge obstacle to building bigger and better capital markets at a time when the European economy needs them more than ever. We can tinker at the edges with the detail of regulation, but so as long as Europe has 22 different stock exchange groups operating 35 different exchange for listings, 41 exchanges for trading, and nearly 40 different CCPs and CSDs, not much will change. > Punching below its weight The European equity market is less than half the size of the US but has three times as many exchange groups; more than 10 times as many exchanges for listings; more than twice as many exchanges for trading; and roughly 20 times as many post-trade infrastructure providers.